Capillary Blood Collection Devices Market Report Scope & Overview:

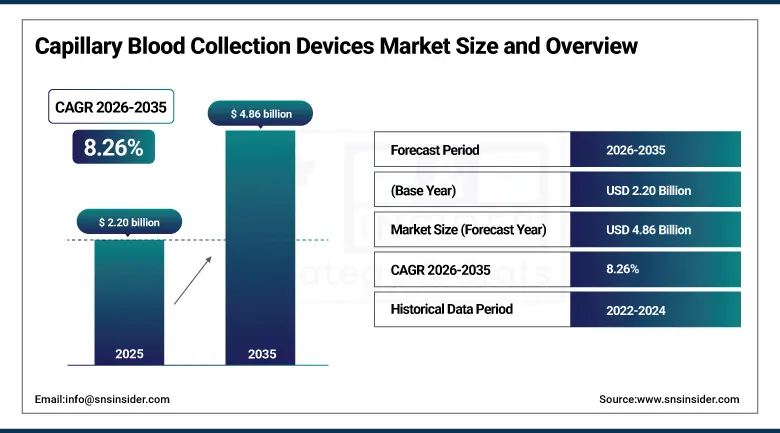

The Capillary Blood Collection Devices Market was valued at USD 2.20 Billion in 2025 and is expected to reach USD 4.86 Billion by 2035, growing at a CAGR of 8.26% from 2026–2035.

The Capillary Blood Collection Devices Market growth is attributed to increasing need for minimally invasive diagnostic procedures and preference for point-of-care tests. Increase in the number of patients suffering from chronic conditions including diabetes, heart problems, and anemia has increased the need for blood tests. Home-based care along with self-monitoring practices is adding to the increase in demand for such devices as lancets and micro-sampling devices. Technological innovations that have led to better accuracy of blood samples, safety, and convenience for patients are contributing to the growth of the market.

According to the World Health Organization (WHO), noncommunicable diseases (NCDs) account for approximately 74% of global deaths, significantly driving continuous demand for routine blood diagnostics such as glucose, lipid, and hemoglobin testing. The International Diabetes Federation (IDF) estimates that 537 million adults were living with diabetes in 2021, with numbers expected to rise further, increasing the need for frequent blood glucose monitoring and capillary sampling. Additionally, the WHO reports that anemia affects nearly 1.9 billion people globally, particularly women and children, requiring repeated diagnostic blood testing and further supporting demand for capillary blood collection devices.

Capillary Blood Collection Devices Market Size and Forecast:

-

Market Size in 2026E: USD 2.38 Billion

-

Market Size by 2035: USD 4.86 Billion

-

CAGR: 8.26% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Capillary Blood Collection Devices Market - Request Free Sample Report

Capillary Blood Collection Devices Market Trends:

-

Rising prevalence of chronic diseases such as diabetes and cardiovascular disorders driving demand for capillary blood collection devices for routine diagnostics

-

Growing shift toward point-of-care testing and home healthcare monitoring increasing the adoption of minimally invasive blood sampling solutions

-

Increasing preference for painless, safe, and low-volume blood collection methods improving patient comfort and compliance in diagnostic procedures

-

Expanding use in neonatal and pediatric testing where venous blood draws are challenging, boosting demand for capillary-based sampling devices

-

Continuous advancements in micro-sampling technologies and integrated diagnostic systems enhancing accuracy, efficiency, and usability of blood collection devices

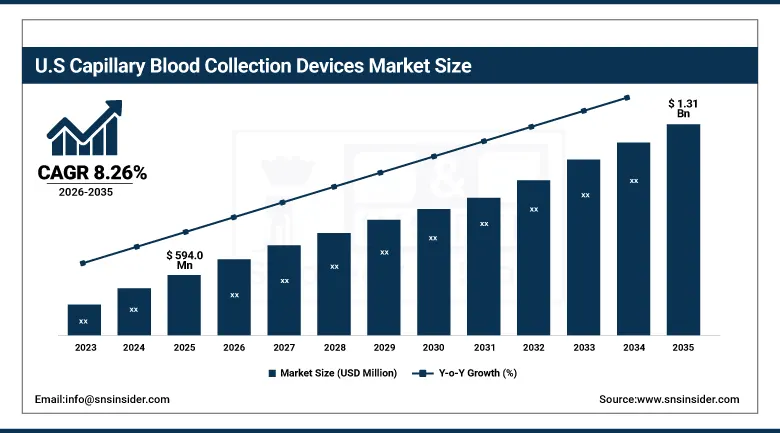

U.S. Capillary Blood Collection Devices Market Outlook:

The U.S. Capillary Blood Collection Devices Market was valued at approximately USD 594.0 Million in 2025 and is expected to reach approximately USD 1.31 Billion by 2035, growing at a CAGR of approximately 8.26%.

The United States leads North American revenues through its world-leading diabetes patient population creating the largest individual application base for capillary glucose monitoring, the comprehensive point-of-care diagnostic testing infrastructure at pharmacies and urgent care centres, and the newborn screening programme’s universal mandatory capillary heel puncture creating consistent institutional procurement. BD, Sarstedt, and Greiner Bio-One sustain U.S. market leadership through established GPO distribution relationships and clinical facility formulary positioning. CDC’s chronic disease prevention programmes sustain above-average home-based capillary testing adoption.

According to the U.S. Centers for Disease Control and Prevention (CDC), 38.4 million Americans have diabetes, representing 11.6% of the population, driving strong demand for frequent blood glucose monitoring using capillary blood collection devices.

Capillary Blood Collection Devices Market Segment Analysis:

-

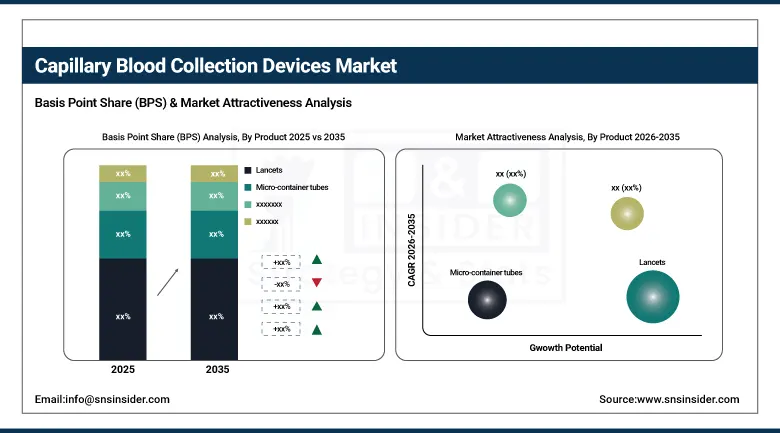

By Product, Lancets segment dominated the Capillary Blood Collection Devices Market in 2025 with 46% share; Micro-container tubes segment is the fastest growing segment.

-

By Material, Plastic segment dominated the market in 2025 with 61% share; Ceramic segment is the fastest growing segment.

-

By Application, Whole Blood segment dominated the market in 2025 with 39% share; Dried Blood Spot Tests segment is the fastest growing segment.

-

By End Use, Hospitals and Clinics segment dominated the market in 2025 with 44% share; Home Diagnosis segment is the fastest growing segment.

By Product, lancets segment dominates the capillary blood collection devices market, while micro-container tubes segment is the fastest-growing segment

The Lancets segment dominated the Capillary Blood Collection Devices Market because it was widely used for blood sampling, blood glucose monitoring, and point-of-care diagnosis. The use of lancets was due to their simple design, low cost, and minimally invasive nature, which make them suitable for clinical and personal usage at home. The increased incidences of diabetes and other chronic diseases have contributed to their dominance in the market. Product innovation through improvements in safety and usability also contributes to their dominance in the market.

The Micro-container tubes segment is the fastest growing due to high demand for more precise, contamination-free, and volume-wise small-blood sample collection. These containers are now increasingly being adopted in complex diagnostic processes, newborn diagnostics, and other laboratory testing purposes. Increasing importance and demand for accurate diagnosis results are some of the factors behind their fast-growing status. Advancements in micro sampling and increase in laboratory testing procedures are fueling their growth in the market.

By Material, plastic segment dominates the capillary blood collection devices market, while ceramic segment is the fastest-growing segment

The Plastic segment dominated the market due to the light weight, economical nature, and durability of the material used for blood collection devices. The use of plastic eliminates any chances of damage and provides safety during blood collection, transportation, and storing. The ability to produce large volumes of plastic products and their suitability for single usage has boosted demand. Also, the rising demand for disposable medical devices to prevent infections has contributed to the dominance of plastic capillary blood collection devices.

The Ceramic segment is the fastest growing due to rising demand for precision, chemical stability, and non-contaminated blood collection material. This material is highly durable, which makes it ideal for use in medical diagnostic purposes. Rapid advancements in the medical diagnostics industry have boosted its growth. In addition to this, there has been an increased emphasis on precision tests and innovative ceramic material in the medical industry.

By Application, whole blood segment dominates the capillary blood collection devices market, while dried blood spot tests segment is the fastest-growing segment

The Whole Blood segment dominated the market due to extensive usage of whole blood samples in diagnostic testing, screening for diseases, and emergency care applications. It has been observed that the application of whole blood samples is quite wide across various diagnostic and medical facilities. The factors such as increased incidences of chronic diseases, increasing need for point-of-care testing, and high adoption rate in clinical diagnostics drive the segment. Moreover, easy-to-collect nature and broad applicability in various tests drive market dominance across the globe.

The Dried Blood Spot Tests segment is the fastest growing due to increasing adoption of minimally invasive sampling techniques and improved sample stability. These tests require only small blood volumes and are widely used in neonatal screening, infectious disease testing, and remote diagnostics. Growing demand for home-based testing and telehealth services is driving expansion. Additionally, advancements in analytical technologies and improved accuracy of dried blood spot analysis are accelerating global adoption rapidly.

By End Use, hospitals and clinics segment dominates the capillary blood collection devices market, while home diagnosis segment is the fastest-growing segment

The Hospitals and Clinics segment dominated the market due to high patient inflow, advanced diagnostic infrastructure, and widespread use of capillary blood collection devices in routine testing. These facilities perform large volumes of blood tests for disease diagnosis, monitoring, and emergency care. Increasing prevalence of chronic diseases and growing demand for accurate diagnostic services further strengthen their position. Additionally, availability of skilled healthcare professionals ensures efficient and reliable sample collection processes globally.

The Home Diagnosis segment is the fastest growing due to increasing adoption of self-monitoring devices and rising preference for convenient healthcare solutions. Patients with chronic conditions such as diabetes are increasingly using capillary blood collection devices for at-home testing. Growing awareness of preventive healthcare, expansion of telemedicine services, and advancements in user-friendly diagnostic kits are driving growth. Additionally, rising demand for cost-effective and time-saving testing solutions is accelerating adoption globally.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Capillary Blood Collection Devices Market Insights

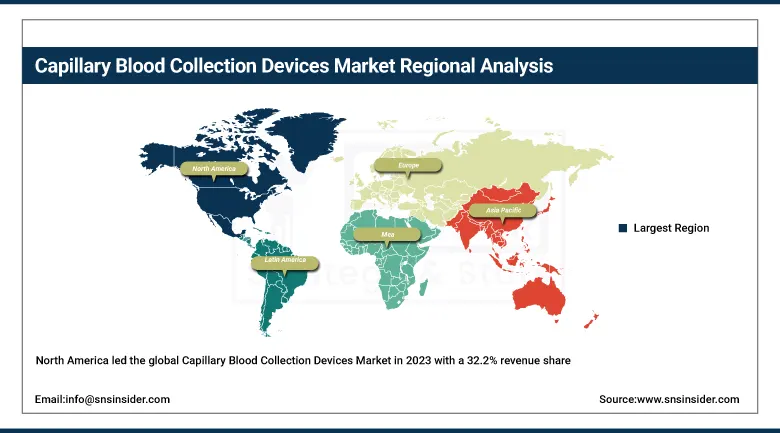

North America led the global Capillary Blood Collection Devices Market in 2023 with a 32.2% revenue share, driven by the world’s largest diabetes management device market, comprehensive newborn screening programme’s universal heel puncture mandate, and advanced point-of-care diagnostic testing infrastructure. The United States accounts for approximately 82.5% of North American revenues through BD, Sarstedt, and Greiner Bio-One’s GPO-based distribution and established clinical facility formulary positioning.

The CDC also reports that around 1 in 2 U.S. adults has cardiovascular disease, significantly increasing the need for routine diagnostic blood testing and long-term health monitoring through minimally invasive sampling methods.

The U.S. National Institutes of Health (NIH) highlights increasing adoption of home-based diagnostic testing and self-monitoring technologies, supporting the shift toward convenient, patient-centric care and rising use of capillary blood collection devices.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Capillary Blood Collection Devices Market Insights

Europe is a significant capillary blood collection devices market where the comprehensive universal newborn screening programmes of Germany, France, the United Kingdom, and the Netherlands, the large type 1 and type 2 diabetes patient population’s self-monitoring requirements, and the advanced point-of-care diagnostic infrastructure at European primary care practices collectively create consistent device procurement. Germany accounts for approximately 22.4% of European revenues through Sarstedt’s domestic manufacturing leadership and the comprehensive German diabetes care programme.

The European Centre for Disease Prevention and Control (ECDC) reports that chronic diseases represent a major healthcare burden in Europe, with cardiovascular diseases causing nearly 1.7 million deaths annually, increasing demand for routine diagnostic blood testing and monitoring.

The WHO Europe region reports a rising prevalence of diabetes across member countries, with millions of patients requiring regular blood glucose monitoring and repeated diagnostic testing, supporting demand for capillary blood collection devices.

Asia Pacific Capillary Blood Collection Devices Market Insights

Asia Pacific is the fastest-growing regional capillary blood collection devices market with a CAGR of approximately 8.5%, driven by the world’s largest and fastest-growing diabetic population, expanding newborn screening programme coverage in China, India, and Southeast Asia, and the progressive investment in point-of-care diagnostic infrastructure at primary care facilities. China accounts for approximately 44.8% of Asia Pacific revenues through its 140 million diabetic patients creating massive self-monitoring lancet consumption.

The International Diabetes Federation (IDF) reports that the Asia-Pacific region accounts for over 60% of global diabetes cases, significantly increasing demand for frequent blood glucose monitoring and capillary blood testing across healthcare settings.

India is the most commercially dynamic emerging market within Asia Pacific, where the world’s second-largest diabetes patient population’s rapidly growing self-monitoring adoption, the national newborn screening programme expansion to include metabolic disorders, and the growing point-of-care diagnostic infrastructure at urban and rural health centres create above-regional-average capillary collection device demand.

India’s Ministry of Health and Family Welfare (MoHFW) reports a rising burden of noncommunicable diseases such as diabetes and hypertension, driving the need for regular diagnostic monitoring and increased use of capillary blood collection devices.

MEA & Latin America Capillary Blood Collection Devices Market Insights

The UAE leads MEA revenues at approximately 22.8% through the Gulf region’s high diabetes prevalence among its population creating substantial self-monitoring lancet consumption, the advanced hospital sector’s neonatal screening programmes, and the growing point-of-care diagnostic testing investment in UAE health centres. Saudi Arabia’s large diabetic population and South Africa’s growing laboratory diagnostics sector create growing regional demand.

Brazil leads Latin American revenues at approximately 43.8% through its large type 2 diabetes patient population’s self-monitoring market, the national newborn screening programme’s mandatory heel lancet procurement, and the expanding laboratory network’s capillary collection tube and microcollection container demand. Mexico and Colombia contribute growing secondary demand through their healthcare infrastructure expansion and growing chronic disease patient populations.

Market Dynamics:

Growth Drivers: Rising diabetes prevalence and point-of-care testing expansion are driving strong demand for capillary blood collection devices globally.

The capillary blood collection devices market’s most structurally certain growth driver is the global diabetes epidemic whose 537 million adult patients in 2021 growing toward a projected 783 million by 2045 creates proportional lancet procurement growth from self-monitoring programmes. Each new diabetes diagnosis creates annual lancet consumption at one to multiple units per day per patient whose aggregate across the growing diabetic population creates sustained above-GDP device market growth. The progressive adoption of continuous glucose monitoring whose calibration requires periodic capillary reference measurements and the expansion of structured self-monitoring protocols among type 2 diabetes patients whose adherence improves glycaemic outcomes sustain above-baseline lancet consumption growth.

Point-of-care diagnostic testing expansion into pharmacy, urgent care, and physician office settings is creating new capillary blood collection device procurement channels whose patient access convenience and healthcare cost efficiency advantages over centralised laboratory testing sustain growing institutional adoption. Each pharmacy that implements capillary-based lipid panel, HbA1c, and INR point-of-care testing creates device procurement above traditional hospital and laboratory purchasing channels.

Restraints: Haemoconcentration and sample quality variability limiting capillary collection adoption for some quantitative biomarker assays

Capillary blood’s compositional difference from venous blood, where tissue fluid dilution, haemoconcentration from cold extremities, and the mixing of arterial, venous, and interstitial fluid creates sample matrix variability that affects quantitative assay results for some analytes including potassium, glucose, and haemoglobin whose capillary-to-venous reference range equivalence requires assay-specific validation before capillary specimens can be reported against venous blood reference intervals. Each clinical laboratory that identifies capillary-venous analytical discrepancy in key assays creates clinical adoption barriers that delay capillary collection programme expansion.

Finger puncture pain and compliance challenges for patients requiring frequent daily glucose monitoring create device user experience limitations whose severity motivates patient preference for continuous glucose monitoring systems that eliminate fingerstick requirements. Each CGM-adopting diabetes patient represents a potential lancet consumption reduction that partly offsets the market’s diabetes patient volume growth, creating headwinds in the traditional self-monitoring lancet segment.

Opportunities: Volumetric microsampling validation and expansion of home-based remote monitoring are creating premium capillary blood collection device market segments

The progressive clinical validation of volumetric absorptive microsampling devices for quantitative biomarker measurement in clinical laboratory assay panels represents the most commercially significant near-term expansion opportunity for the capillary blood collection device market. Each new peer-reviewed validation study demonstrating analytical equivalence of VAMS-based microsamples and conventional venous blood specimens for therapeutic drug monitoring, lipid panel measurement, or endocrine function assessment creates clinical acceptance that progressively expands the assay panel accessible through capillary home-based self-collection, creating a new clinical testing category whose addressable patient population spans all chronic disease management patients.

Home-based remote patient monitoring programme expansion, where capillary blood self-collection enables periodic biomarker assessment outside clinical visits whose frequency and cost create healthcare system access barriers for chronic disease management, creates growing demand for user-optimised capillary collection devices whose ergonomics, sample volume reliability, and packaging for mail-based specimen return sustain above-average premium device pricing relative to standard lancet and collection tube commodities.

Recent Developments:

-

2025: Tasso Inc. and ARUP Laboratories partnered to validate multiple clinical assays using capillary blood microsamples, supporting expansion of minimally invasive home-based diagnostic testing into clinical laboratory workflows for biomarker monitoring protocols previously requiring venous specimens.

-

2024: BD and Babson Diagnostics expanded fingertip blood collection and testing technologies for U.S. healthcare systems, enabling capillary-based diagnostic testing at urgent care centres, physician offices, and ambulatory settings without trained phlebotomy staff requirements.

-

2024: Vitestro Holding BV received CE marking for its AI-powered automated blood drawing device integrating ultrasound-guided imaging and robotics for precise capillary and venous blood collection, becoming the first CE-certified automated blood collection device of its kind.

Capillary Blood Collection Devices Market Key Players are:

-

Becton, Dickinson and Company (BD)

-

Terumo Corporation

-

Greiner Bio-One International GmbH

-

Sarstedt AG & Co. KG

-

Abbott Laboratories

-

Roche Diagnostics

-

Medtronic plc

-

Cardinal Health, Inc.

-

Henry Schein, Inc.

-

Nipro Corporation

-

Smiths Medical (ICU Medical)

-

Fresenius Kabi AG

-

Narang Medical Limited

-

Hindustan Syringes & Medical Devices Ltd.

-

Owen Mumford Ltd.

-

StatLab Medical Products

-

SEKISUI Medical Co., Ltd.

-

EKF Diagnostics Holdings plc

-

Improve Medical Instruments Co., Ltd.

-

Shanghai International Holding Corp. (SIIC) Medical Group

Capillary Blood Collection Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.20 Billion |

| Market Size by 2035 | USD 4.86 Billion |

| CAGR | CAGR of 8.26% from 2026–2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Lancets, Micro-container tubes, Micro-hematocrit tubes, Warming devices, Others) • By Material (Plastic, Glass, Stainless steel, Ceramic, Others) • By Application (Whole Blood, Plasma/ serum protein Tests, Comprehensive metabolic panel tests, Liver panel/ liver profile/ liver function tests, Dried blood spot tests) • By End Use (Hospitals and Clinics, Blood Donation Centers, Diagnostic Centers, Home Diagnosis, Pathology Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Becton, Dickinson and Company (BD), Terumo Corporation, Greiner Bio-One International GmbH, Sarstedt AG & Co. KG, Abbott Laboratories, Roche Diagnostics, Medtronic plc, Cardinal Health, Inc., Henry Schein, Inc., Nipro Corporation, Smiths Medical (ICU Medical), Fresenius Kabi AG, Narang Medical Limited, Hindustan Syringes & Medical Devices Ltd., Owen Mumford Ltd., StatLab Medical Products, SEKISUI Medical Co., Ltd., EKF Diagnostics Holdings plc, Improve Medical Instruments Co., Ltd., Shanghai International Holding Corp. (SIIC) Medical Group |

Frequently Asked Questions

The Capillary Blood Collection Devices Market is expected to grow at a CAGR of 8.26% from 2026 to 2035.

The Capillary Blood Collection Devices Market was valued at USD 2.20 Billion in 2025.

Global diabetes prevalence creating mass-market lancet demand, point-of-care testing expansion in ambulatory care settings, home-based chronic disease monitoring adoption, and newborn screening programme expansion are the primary growth factors.

The Lancets segment dominated the Capillary Blood Collection Devices Market in 2025.

North America dominated the Capillary Blood Collection Devices Market in 2025.

Get in Touch