Concrete Admixtures Market Report Scope and Overview:

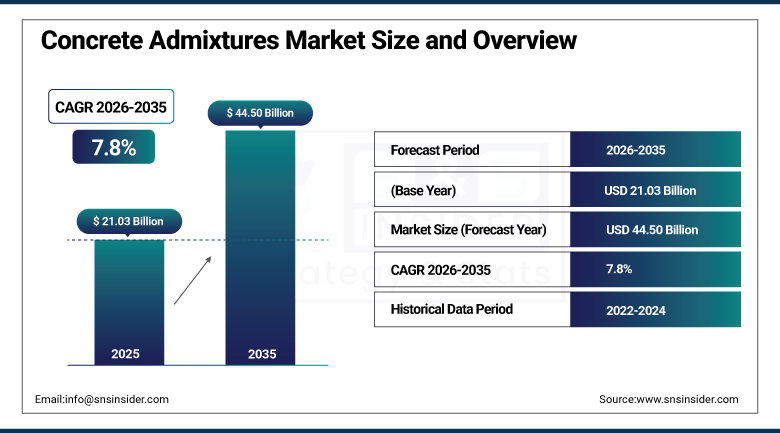

The Concrete Admixtures Market was valued at USD 21.03 Billion in 2025 and is projected to reach USD 44.50 Billion by 2035, registering a CAGR of 7.8% from 2026 to 2035.

Concrete admixtures are chemical or mineral compounds added to concrete mixtures during production to modify specific properties, including workability, setting time, durability, and resistance to environmental stress. The demand for concrete admixtures continues increasing steadily due to rapid urbanization, large-scale infrastructure development, and rising construction activities across both emerging and developed economies. Demand is moving toward performance-engineered mixes that accelerate setting, limit embodied carbon, and cut on-site labor, and infrastructure investment programs across major economies continue tying funding to lower water-cement ratios, which directly lifts superplasticizer consumption. Growing use of precast concrete and ready-mix concrete, alongside rising construction projects and escalating demand for high-performance concrete, continues boosting market growth across a genuinely broad range of applications spanning residential, commercial, industrial, and public infrastructure construction.

Sika continued expanding its portfolio of low-carbon, performance-engineered admixture formulations throughout 2025, targeting construction customers seeking to reduce embodied carbon in concrete production while maintaining workability, strength development, and durability performance across infrastructure and building projects worldwide.

Market Size and Forecast

-

Market Size in 2026E: USD 22.64 Billion

-

Market Size by 2035: USD 44.50 Billion

-

CAGR: 7.8% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Concrete Admixtures Market - Request Free Sample Report

Concrete Admixtures Market Trends

-

Demand continues moving toward performance-engineered mixes that accelerate setting, limit embodied carbon, and cut on-site labor requirements.

-

Infrastructure investment programs across major economies continue tying funding to lower water-cement ratios, directly lifting superplasticizer consumption.

-

The trend toward sustainable construction practices continues driving adoption of innovative concrete admixtures that enhance performance while reducing environmental footprint.

-

Innovations in green building materials and advancements in nanotechnology-based cement enhancers continue creating new opportunities across the industry.

-

Growing use of precast concrete continues supporting demand for admixtures optimized for accelerated curing and consistent quality control in factory settings.

U.S. Concrete Admixtures Market Outlook

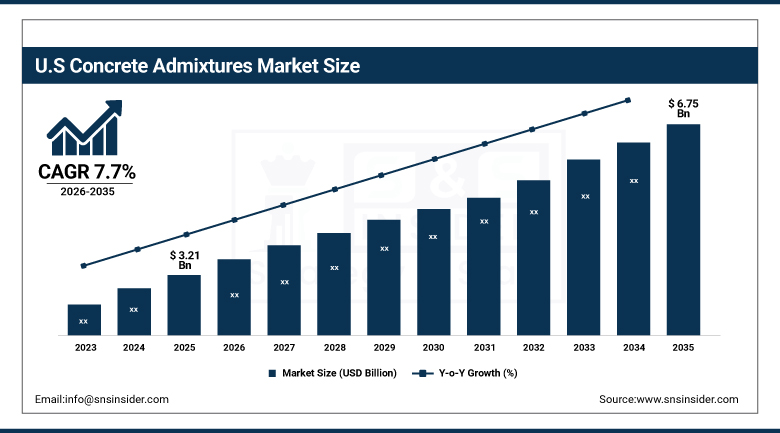

The US Concrete Admixtures Market was valued at approximately USD 3.21 Billion in 2025 and is projected to reach approximately USD 6.75 Billion by 2035, registering a CAGR of approximately 7.7% from 2026 to 2035.

The US demand for concrete admixtures was driven by the presence of a strong housing market and more construction activities due to increased number of households and demand for residential structures. Rising cost of construction and focus on high-performing building materials was one of the major factors influencing the adoption of domestic admixtures. Government programs promoting infrastructure improvement projects were increasing the demand for concrete admixtures in the country. Sustainable construction methods were another factor leading to the adoption of new concrete admixtures in the country.

BASF continued expanding its Master Builders Solutions admixture portfolio throughout 2025, targeting American ready-mix and precast concrete producers seeking advanced water-reduction and set-control chemistry to meet increasingly stringent infrastructure performance specifications nationwide.

Concrete Admixtures Market Segment Analysis

-

By Type, water-reducing admixtures led the market with an estimated 47.8% share in 2025, while air-entraining admixtures was the fastest-growing type, tracking a projected 10.1% CAGR.

-

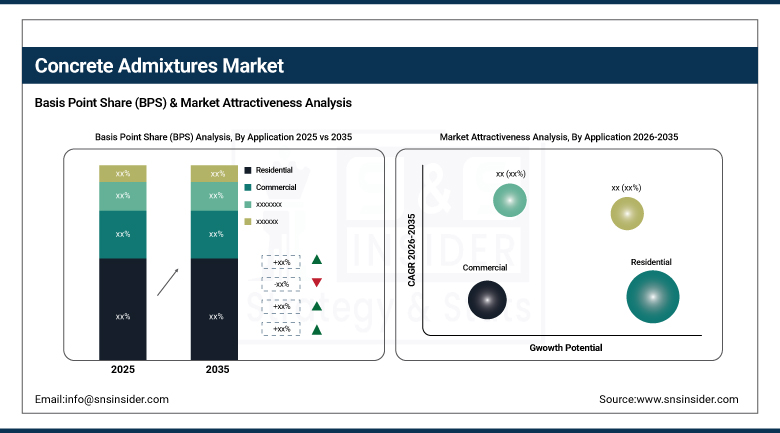

By Application, residential led the market with an estimated 32% share in 2025, while public infrastructure was the fastest-growing application, tracking rising government infrastructure investment.

By Type, Water-Reducing Admixtures led the market, Air-Entraining Admixtures grew fastest

Water-Reducing Admixtures held the largest type share in 2025, at approximately 47.8%. The large market share of this segment was attributed to rising adoption of water-reducing admixtures to improve concrete durability by lowering the water-cementitious ratio, reducing permeability, increasing air content, and creating a concrete mix with genuinely improved workability that construction crews across virtually every application category continued relying upon.

Air-Entraining Admixtures are expected to grow at the fastest CAGR of 10.1% during the forecast period. This growth continues being primarily driven by their role in improving concrete's workability and resistance to freeze-thaw cycles, as regions experiencing genuine seasonal temperature extremes increasingly specify air-entraining agents to prevent the internal cracking and surface scaling that repeated freezing and thawing cycles can otherwise cause in unprotected concrete structures.

By Application, Residential led the market, Public Infrastructure grew fastest

The Residential segment accounted for the largest application share in 2025, at approximately 32%. The large market share of this segment was attributed to the rising global population, increasing demand for high-rise apartments and condominiums, and government initiatives to assist in developing affordable housing, with major developers continuing to announce substantial new residential project pipelines to meet growing consumer demand across both emerging and developed housing markets.

Public Infrastructure is expected to register the highest CAGR during the forecast period among application categories. Government infrastructure modernization programs continue driving this growth, as funding increasingly gets tied to performance specifications including lower water-cement ratios that directly lift admixture consumption, and expanding public transportation, bridge, and utility infrastructure projects worldwide continue creating sustained demand for genuinely high-performance concrete solutions.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

37.15% |

|

North America |

United States |

79.60% |

|

Europe |

Germany |

23.75% |

|

Middle East and Africa |

UAE |

26.35% |

|

Latin America |

Brazil |

34.90% |

North America Concrete Admixtures Market Insights

North America is expected to grow at a significant CAGR of 8.0% over the forecast period, owing to a robust housing sector and increased construction activities. Rising household formations and strong demand for residential properties continued serving as key factors contributing to this growth, keeping the continent positioned as the fastest-growing market tracked in this report even as it trails Asia Pacific in overall market size.

The United States held a significant share of North American revenue, driven by rising construction costs and an emphasis on high-performance building materials. Canada added further regional demand through its own growing construction and infrastructure sector, and that combined strength, reinforced by government initiatives supporting infrastructure improvement projects, kept North America the fastest-growing regional market for concrete admixture vendors through the forecast period.

Europe Concrete Admixtures Market Insights

Europe held a meaningful share of global revenue, supported by stringent building regulations and a growing focus on green building materials across the region's major economies. Continued emphasis on sustainable construction practices kept reinforcing steady demand for innovative, environmentally responsible admixture formulations across the continent.

Germany led demand at roughly 23.75% of European revenue, supported by its substantial construction and infrastructure manufacturing base. The UK and France contributed substantial additional demand, and continued European regulatory emphasis on sustainable building materials should keep regional demand climbing through the forecast period.

Asia Pacific Concrete Admixtures Market Insights

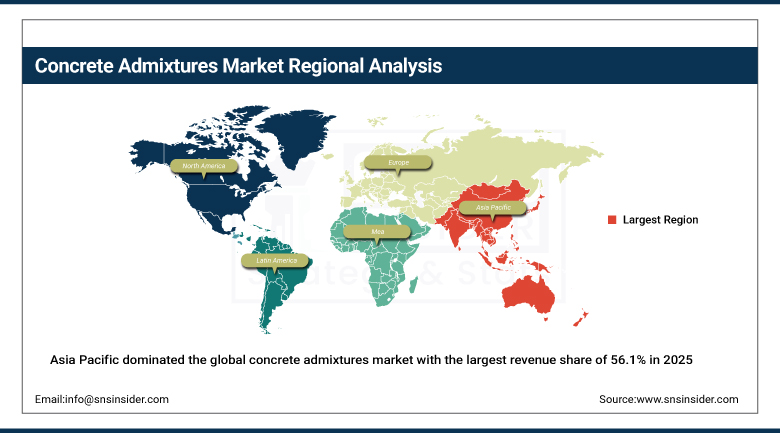

Asia Pacific dominated the global concrete admixtures market with the largest revenue share of 56.1% in 2025, attributed to the robust growth of the construction and other industries in major economies across the region. Rapid urbanization and large-scale infrastructure projects across the region's largest economies continued reinforcing this dominant position by a considerable margin over every other region tracked in this report.

China accounted for the largest market revenue share within Asia Pacific in 2025, supported by the country's massive construction and infrastructure development activity. India and Southeast Asian economies contributed meaningful additional demand, with rapid industrialization and large-scale infrastructure projects across the broader region continuing to reinforce Asia Pacific's structural dominance in both production and consumption of concrete admixtures.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA and Latin America Concrete Admixtures Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding construction and infrastructure investment, growing urbanization, and rising government focus on affordable housing development across both areas. As these markets continued building out modern construction infrastructure, admixture adoption grew correspondingly from a considerably smaller base than in more mature construction markets.

The UAE led Middle East and Africa demand, supported by substantial construction and infrastructure investment tied to the region's continued urban development. Saudi Arabia contributed further demand through its own large-scale infrastructure programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing residential and infrastructure construction continuing to anchor regional demand for concrete admixtures.

Market Dynamics

Growth Drivers: Rapid Urbanization and Infrastructure Development

The demand for concrete admixtures continues increasing steadily due to rapid urbanization, large-scale infrastructure development, and rising construction activities across both emerging and developed economies. The need for better-performing concretes and longer-lasting structures remains a primary factor accelerating market growth, further supported by the magnificent rise in construction of the residential sector due to growing urbanization.

The growing use of precast concrete and ready-mix concrete continues driving market growth, as precast concrete is adaptable and recyclable with high strength and durability that enhances the setting up of modern construction units and pre-factored buildings. The rise in demand for green buildings continues raising precast concrete demand, and that combination of structural performance requirements and genuine sustainability momentum is exactly what keeps demand climbing at such a sustained pace across the global construction industry.

Restraints: Raw Material Price Volatility and Regulatory Compliance Costs

Raw material price volatility continues posing a genuine restraint on stable margin planning across the concrete admixtures supply chain, as key input chemicals remain subject to petrochemical feedstock pricing swings that manufacturers can't always pass through to customers without genuine competitive pressure. That volatility keeps long-term supply agreements between admixture producers and concrete manufacturers genuinely complicated to negotiate.

Compliance costs associated with increasingly stringent building regulations and environmental standards continue adding real operational complexity for admixture manufacturers, as formulations must satisfy both performance requirements and tightening sustainability disclosure expectations across an increasingly broad range of jurisdictions. That compliance burden keeps smaller, less-established manufacturers at a genuine competitive disadvantage relative to well-resourced global players.

Opportunities: Sustainable Formulation Innovation and Emerging Market Expansion

Innovations in green building materials represent a genuinely significant opportunity, as manufacturers investing in nanotechnology-based cement enhancers and low-carbon admixture formulations stand to capture meaningful share as environmental regulation and corporate sustainability commitments keep intensifying across the construction industry. Vendors that can demonstrate genuine embodied-carbon reduction alongside proven performance stand to capture disproportionate share of this expanding, technically demanding formulation category.

Expansion in emerging markets offers a second substantial opportunity, as rapid urbanization and large-scale infrastructure development across developing economies continue creating fresh demand for advanced concrete admixture technology. Vendors positioned early in these expanding construction markets stand to capture meaningful share as governments across emerging economies keep prioritizing infrastructure modernization and affordable housing development at genuinely large scale.

Recent Developments:

-

2025: MAPEI continued expanding its range of sustainable, low-carbon admixture solutions, targeting construction customers seeking to reduce embodied carbon while maintaining concrete performance and durability standards.

-

2025: Saint-Gobain continued advancing its construction chemicals portfolio, integrating enhanced water-reduction and specialty admixture technology for ready-mix and precast concrete producers across global markets.

-

2024: Tata Housing Development Company announced plans to launch 10 million square feet of residential projects over the next two to three years to meet growing consumer demand across the Indian market.

Concrete Admixtures Market Key Players are:

-

Sika AG

-

Saint-Gobain S.A.

-

BASF SE

-

MAPEI S.p.A.

-

RPM International Inc.

-

Jiangsu Subote New Material Co., Ltd.

-

Dow Inc.

-

Fosroc International Limited

-

Boral Limited

-

Buzzi Unicem SpA

-

Elkem ASA

-

CEMEX S.A.B. de C.V.

-

CAC Admixtures, Inc.

-

Cementaid International Limited

-

Kao Corporation

-

Arkema S.A.

-

W.R. Grace & Co.

-

Pidilite Industries Limited

-

Mapei Corporation

-

Euclid Chemical Company

Concrete Admixtures Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.03 Billion |

| Market Size by 2035 | USD 44.50 Billion |

| CAGR | CAGR of 7.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Water-Reducing Admixtures, Waterproofing Admixtures, Air-Entraining Admixtures, Accelerating Admixtures, Retarding Admixtures, Others) • By Application (Residential, Commercial, Industrial, Public Infrastructure) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sika AG, Saint-Gobain S.A., BASF SE, MAPEI S.p.A., RPM International Inc., Jiangsu Subote New Material Co., Ltd., Dow Inc., Fosroc International Limited, Boral Limited, Buzzi Unicem SpA, Elkem ASA, CEMEX S.A.B. de C.V., CAC Admixtures, Inc., Cementaid International Limited, Kao Corporation, Arkema S.A., W.R. Grace & Co., Pidilite Industries Limited, Mapei Corporation, and Euclid Chemical Company |

Frequently Asked Questions

The major growth factor is rapid urbanization, large-scale infrastructure development, and rising construction activities across both emerging and developed economies.

The Water-Reducing Admixtures segment dominated the Concrete Admixtures Market by type, representing an estimated 47.8% of revenue in 2025.

The Concrete Admixtures Market was valued at approximately USD 21.03 Billion in 2025, based on triangulation across multiple independent research sources.

Get in Touch