Concrete Restoration Market Report Scope & Overview:

Get More Information on Concrete Restoration Market - Request Sample Report

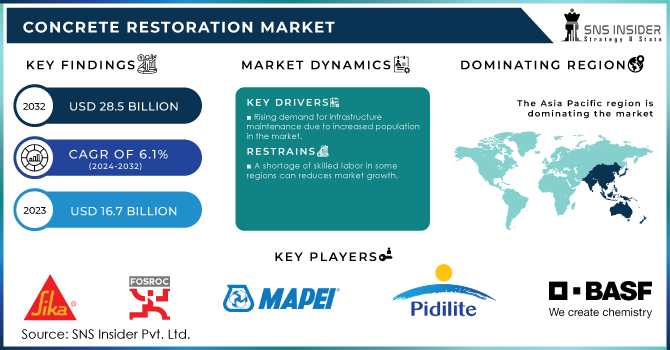

The Concrete Restoration Market size was valued at USD 17.1 Billion in 2023. It is expected to grow to USD 31.8 Billion by 2032 and grow at a CAGR of 6.4% over the forecast period of 2024-2032.

The concrete restoration market is experiencing growth due to a notable increase in investments in renovation and remodeling activities. With the change of emphasis on extending relatively new structures instead of rebuilding new ones have seen a large increase in demand for concrete restoration. Structural Safety and Economic Building Strategy Homeowners and businesses focus on utmost structural integrity while also economizing how buildings can be made more durable. Home remodeling is on an upward trend as heightened awareness of maintaining and upgrading existing buildings has become central to national construction studies, according to the National Association of Home Builders (NAHB). The lifestyle changes, higher property prices, and the necessity for modern amenities in antiquated buildings are further contributing to this trend. Moreover, the government has taken this to new heights with incentives and funding assistance for infrastructure upgrades. These factors as mentioned above, along with the increasing focus on sustainable and eco-friendly practices are driving the necessity of concrete restoration which is one of the key trends in this market.

According to the U.S. Census Bureau, expenditures on residential improvements and repairs in the United States reached approximately USD 538 billion in 2023, reflecting a steady increase from previous years. This growth indicates rising investments in renovation and remodeling activities as property owners focus on extending the lifespan of their existing structures.

Increased influence of environmental concerns in the concrete restoration market. The restoration market is influenced by the pressure to shift from traditional methods that led to carbon pollution and push towards sustainable restoration practices. As awareness of climate change grows and there is a reduction in carbon emissions, the market for eco-friendly repairing and restoration solutions is setting in. Some of the key best practices are to use recycled aggregate concrete (RAC), a type of sustainable concrete made with demolished waste concrete, and low-carbon and polymer-modified repair products. Such innovations are not only reducing the environmental footprint but also contributing to global sustainability targets like the UN's Sustainable Development Goals (SDGs). Moreover, more restoration companies are getting certified in green standards which promotes eco-friendly practices. With governments taking a more serious stand on environmentally friendly methods, green building is a growing social trend. For example, governments in the EU have introduced incentives and standards for the use of recycled content in construction. This means that efforts to push the market in a more sustainable direction are both growing and solving important environmental issues such as resource depletion and waste.

According to the European Environment Agency (EEA), the use of recycled aggregates in construction reached approximately 12% of total aggregates used in the EU in 2022, reflecting increasing efforts to promote sustainable construction and reduce waste. This shift is driven by policies under the EU Waste Framework Directive, which aims to achieve a 70% recycling target for construction and demolition waste by 2025.

Drivers

-

Durability, and cost-effectiveness of restoration projects.

-

Rising demand for infrastructure maintenance due to increased population in the market.

Growing demand for infrastructure upkeep is one of the major factors expected to drive the concrete restoration market size over upcoming years, in line with the ongoing rise in population levels. Growing urban populations consume higher use of existing infrastructure roads, bridges, water systems, and public buildings and increase the rate of wear. Such events create an impetus to continue regular maintenance and restoration projects by local governments and authorities in order to maintain public safety and continuous services. Rapid population influx into urban areas quickly exposes the reliability of older infrastructure, since experienced usage is magnified by until-recent rapid growth. On top of that, governments are putting in big budgets for maintenance projects to correct structural defects and extend the lifetime serviceability of public assets. For instance, in 2021, the U.S. government passed the Infrastructure Investment and Jobs Act with USD 110 billion for roads, bridges, and large-scale infrastructure projects. These projects are vital in maintaining and repairing infrastructure as urban populations continue to grow, which is driving up demand for concrete restoration services.

Restraint

-

Regulatory hurdles in developed in the concrete restoration markets

-

A shortage of skilled labor in some regions can reduce market growth.

High Regulation in Developed Regions, a Restraint for the Concrete Restoration Market Restoration is often made more difficult by very strict building codes and safety regulations, that require compliance at the local, state, as well as federal levels concerning rebuilding. But outside of the need for this energy, there is a level of complexity in places such as the U.S. with the Occupational Safety and Health Administration (OSHA) and Environmental Protection Agency through which project costs can increase due to stringent guidelines around worker safety, material handling, and environmental impacts that lengthens timelines. Following these regulations requires compliance not just with protocols for safety, but also approved materials and techniques that may not reflect the latest in restoration. Likewise, in the EU the Construction Products Regulation imposes high demands on quality standards and certification aspects that add additional levels of documentation. Although these regulatory frameworks are necessary to ensure safety and quality, they can also have the effect of creating a lot of administrative and financial overhead that restricts what restoration firms can do and use when developing new solutions. Developed markets, particularly the European Union (EU), create a challenge for concrete restoration product manufacturers due to stringent regulations. The EU's EN 1504 regulation mandates strict quality standards for raw materials used in restoration products. This ensures product effectiveness and durability, but can also make manufacturing more complex. Manufacturers must adhere to specific control and testing guidelines outlined in the regulation. this ensures product quality, but it can be a costly and time-consuming process.

Opportunities

-

Increased government spending on infrastructure projects.

-

Surging adoption of renewable energy sources in the Concrete Restoration Market.

As governments invest in repairing and upgrading existing infrastructure like roads, bridges, dams, and buildings, the demand for concrete restoration services will rise significantly. This creates more business opportunities for companies specializing in concrete repair. Increased spending might also prioritize preventative maintenance projects to extend the lifespan of existing infrastructure. This could lead to more frequent, smaller-scale concrete restoration jobs, further benefiting the market.

Market segmentation

By Material Type

Quick-setting cement mortar dominated the concrete restoration market with the largest revenue share of about 48% in 2023. This mortar is popularly used because of its fast-setting properties, which can be in a few minutes to hours so you can complete the project faster and minimize downtime. This rapid strength gain is important for restoration work in high-traffic applications, such as road reconstruction, bridge repair, and even commercial areas, where extended closures can affect daily living and increase costs. Besides, when it comes to repairing the cracks in the concrete foundation about connection void, nothing beats quick-setting cement mortar that is strong enough for speedy and durable adhesion on existing concrete. It is also very suitable for all infrastructures subject to strong conditions or various chemical spills, because of its resistance to water and chemicals. To satisfy the non-relaxed Das at work during government infrastructure projects and maintenance works, quick-setting cement mortar is quite in demand to fit urgent timelines and give sustenance to repairs. These attributes contribute to it being the preferred choice for contractors and project managers alike, which leads to its market dominance.

By Target Application

Buildings and balconies segment dominated the concrete restorations market with the highest revenue share of about 40% in 2023. Buildings and balconies represent the highest share of the concrete restoration market since such structures require the most frequent repair and maintenance activities. Residential and commercial buildings are exposed all the time to moisture, temperature, and pollution which causes deterioration of concrete. As these are exposed to the outside environment, balconies are a prime suspect for structural damage and vulnerability such as cracks, corroded reinforcing steel, and water leakage. There is also a constant factor of foot traffic and weight load that contribute to areas often needing restoration. Apart from this, increasing urbanization and growing population in the cities are escalating stress on residential and commercial buildings thereby compelling frequent restoration works. Moreover, safety issues and regulatory standards also warrant balcony and building facade repair soon to prevent any accidents as well as structural failures. The above-mentioned factors, along with an increase in the renovation of buildings in turn boost the demand for concrete restoration services, and therefore, buildings & balconies are likely to remain as largest end-use segment.

Regional Analysis

The Asia-Pacific region led the concrete restoration market which occupied 55% of the market share in 2023. This dominance is driven by a rapidly growing population in countries like China and India. These surging populations strain existing concrete infrastructure, demanding regular maintenance and restoration to prevent collapse. Furthermore, APAC's booming economies fuel extensive infrastructure projects urbanization, modernization, and industrial expansion all necessitating repairs to bridges, pipelines, buildings, and other structures. Large-scale infrastructure restoration initiatives across the region further propel demand for concrete restoration solutions.

North America is the second dominating region in the concrete restoration market. Here, demand is driven by the need for restoration across various infrastructure categories. The need to maintain and repair aging commercial and residential buildings fuels the market. Additionally, restoration projects on transportation infrastructure like bridges, pipelines (including oil & natural gas), and water structures are a major driver.

Get Customized Report as per your Business Requirement - Request For Customized Report

Key Players

-

Sika AG (Sika MonoTop)

-

Fosroc International Ltd (Renderoc HB2)

-

Mapei S.p.A (Planitop 400)

-

BASF SE (MasterEmaco S 488)

-

Saint-Gobain Weber S.A. (Webercem HB30)

-

Master Builders Solutions (MasterBrace ADH 1460)

-

Fyfe Co. LLC (Tyfo Fibrwrap)

-

The Euclid Chemical Company (Duralflex Fastpatch)

-

RPM International Inc. (Rust-Oleum EpoxyShield)

-

Pidilite Industries Ltd (Dr. Fixit Pidicrete URP)

-

3M Company (3M Concrete Repair Self-Leveling)

-

Cemex S.A.B. de C.V. (Proconcrete Repair M)

-

Parchem Construction Supplies Pty Ltd (Emer-Proof Aqua-Barrier)

-

GCP Applied Technologies Inc. (Silcor 900 HA)

-

Ardex Group (Ardex A 38 MIX)

-

W.R. Meadows Inc. (Meadow-Patch T1)

-

Laticrete International Inc. (NXT Level Plus)

-

Simpson Strong-Tie Company Inc. (SET-XP Epoxy Anchoring Adhesive)

-

Kryton International Inc. (Krystol T1 Concrete Waterproofing)

-

Nafico Ltd. (Nafico Mortar L1)

Recent Development:

-

In May 2023, Sika AG significantly bolstered its global presence through the strategic acquisition of MBCC. This move expands their reach across all regions and grants them a wider range of products and services, allowing them to cater to the entire construction life cycle.

-

In September 2022, Fosroc strategically extended its reach into the Qatari market by appointing Mannai Trading Company as its exclusive distributor. This partnership ensures the comprehensive supply of Fosroc's high-performance construction chemicals across various sectors, including the construction, infrastructure, oil, and gas industries.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 17.1 Billion |

| Market Size by 2032 | US$ 31.8 Billion |

| CAGR | CAGR of 6.4% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Shotcrete, Quick setting cement mortar, Fiber concrete, Others (concrete bonding agents, grout, etc.)) • By Application (Water and wastewater treatment, Dams & Reservoirs, Roads, Highways & Bridges, Marine, Buildings & Balconies, Others) |

| Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America |

| Company Profiles | Pidilite Industries, Sika, Fosroc, Mapei S.p.A, BASF SE, Saint-Gobain Weber S.A., Master Builders Solutions, Fyfe, The Euclid Chemical Company, RPM International, and other players. |

| DRIVERS | • Increasing demand for the infrastructure. • Increasing population. |

| Restraints | • The European Union's regulation • Gives material control and testing guidelines |

Frequently Asked Questions

Ans. The projected market size for the Concrete Restoration Market is USD 28.5 Billion by 2032.

Ans: Installed on large concrete foundations and Expanding the use of renewable energy are the opportunity for Concrete Restoration Market.

Ans: Increasing demand for the infrastructure and Increasing population are the drivers for antimicrobial plastics market.

Ans: The unusual coronavirus outbreak had resonated throughout the global economy, affecting global supply chains that transfer materials and components fast across borders and between fabrication locations. As a result, there have been delays or non-arrival of raw materials, messed up money transfers, and an increase in absenteeism among production line workers. The global economy and the performance of numerous industries have been impacted by these issues. The loss of many industries has a direct impact on the market for concrete rehabilitation.

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Get in Touch