Endocavity Transducer Market Size & Trends:

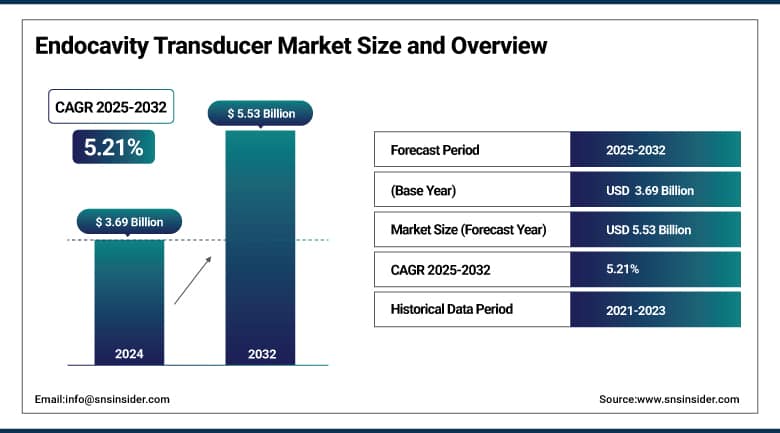

The Endocavity Transducer Market size was valued at USD 3.69 billion in 2024 and is expected to reach USD 5.53 billion by 2032, growing at a CAGR of 5.21% over 2025-2032.

The global endocavity transducer market is seeing strong demand growth, which is fueled by the rapid adoption of non-invasive diagnostic technologies, the increasing occurrence of gynecological and prostate disorders, and innovation in ultrasound imaging. Internal exam, such as transvaginal and transrectal ultrasonography, requires the use of these transducers, and as evidence has shown to be widespread, they are used in OB/GYN clinics, urology centers, and hospitals. Increasing prevalence of early-stage cancer detection and fetal diagnostics is also expected to drive the endocavity transducer market forward. Hospital-acquired infection risks have driven enforcement of strict disinfection protocols, translating into growth of demand for disposable covers and automatic high-level disinfection systems, directly impacting device usage rates, as reported by NIH and RSNA.

A further driving factor is the recent increase in regulatory focus, such as FDA, CDC guidelines for ultrasound probe hygiene, and endocavity transducer market players’ investments into R&D and compliance-centric innovation. This is reflected in companies, such as CIVCO and Esaote, which are working to integrate the AI and 3D imaging functions into probe design.

Growing procedure volumes also bode well for the U.S. endocavity transducer market, in which yearly OB/GYN transvaginal scans are believed to number in the millions, and an expanding aging population is resulting in increased urological procedures. The endocavity transducer market growth and sizing of the endocavity transducer are being influenced by hospital infrastructure upgrades and technological integrations globally. The development of the ultrasound systems is also backed by the proliferation in the investment in diagnostic imaging, and partnership for infection control is performed by the diagnostic imaging makers.

To Get More Information On Endocavity Transducer Market - Request Free Sample Report

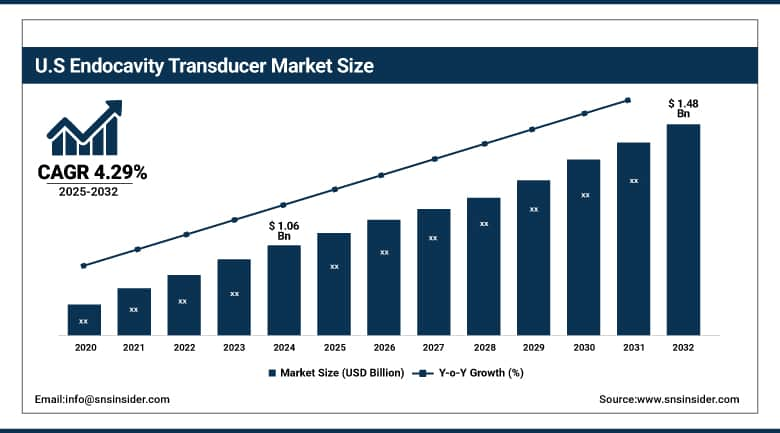

The U.S. Endocavity Transducer Market size was valued at USD 1.06 billion in 2024 and is expected to reach USD 1.48 billion by 2032, growing at a CAGR of 4.29% over 2025-2032. The region had a significant market share in 2024, attributed to a high volume of procedures for OB/GYN and urology in the U.S., coupled with the early implementation of AI-enabled transducer systems. Indeed, according to the RSNA (2023), there were more than 21 million pelvic ultrasound imaging procedures carried out in the U.S. Further, extensive use of high-level disinfection systems and stringent regulatory control from the FDA is contributing to market maturity.

Endocavity Transducer Market Dynamics:

Drivers:

-

Rising Demand for Precision Diagnostics, Infection Control Measures, and Technological Innovations

Rising need for precise diagnostic imaging techniques, rising awareness about the early identification of gynecological and urological issues, and stringent guidelines for the prevention of nosocomial infections are also propelling the market for endocavity transducers. Increased incidence of reproductive and prostatic disorders has led to a remarkable increase in ultrasound use, specifically for internal examination. Diagnostic ultrasound uses for pelvic evaluation increased by 25% in outpatient settings according to a 2023 PubMed study. Finally, elastography and high-frequency 3D imaging added to endocavity probes are enhancing diagnostic certainty.

CDC and ECRI recommendations for probe disinfection procedures, limit process reengineering options, and have spurred substantial investment in automated reprocessing systems and disposable covers, which have only increased device utilization and demand. According to study reports that manufacturers are devoting significant R&D budgets to ergonomic probe design and image optimization, devoting around 8% of their annual revenue to these projects. Philips and GE HealthCare have introduced probes embedded with AI software that provide real-time pathology mapping. The prolonged infusion of funding and the inter-disciplinary nexus of imaging and AI companies are driving innovation in the global endocavity transducer market. In addition, positive FDA 510(k) clearances around new bio-safety driven endocavity models are driving increased clinical adoption, further supporting the endocavity transducer market share and product trajectory.

Restraints:

-

High Cost of Ownership, Disinfection Complexity, and Supply Chain Disruptions Hamper Market Growth

The high price of high-level transducers, which typically range between USD 7,000–10,000, limits the application in small healthcare venues and private clinics. The need for dedicated reprocessing machines, such as automated high-level disinfectors, which cost more than USD 20,000, increases operational costs even more. A 2024 Radiographics article reported that 31% of outpatient centers did not have standardized disinfection practices because of staffing and education limitations. Furthermore, the Joint Commission and FDA level mandates on tracking, labeling, and documenting of transducer reprocessing add another layer of headache to administration.

Global supply chain disruptions have caused shortages of semiconductor components and medical-grade materials, which have led to production and delivery delays and higher prices for the procurement of chips and supplies. Lead times of 6–8 weeks for some probe models were reported by OEMs. This delay limits inventory flexibility and disrupts the replacement circuit. Additionally, an extensive training for safe and skilled hand-held endocavity scanning is also required, which is invaluable, especially in low-resource areas, and acts as a hindrance to the universal clinical adoption. These factors together can impede the growth of the market, even though there is strong clinical demand, which could slow down the market penetration and adoption in some regions of the world for the endocavity transducer market.

Endocavity Transducer Market Segmentation Analysis:

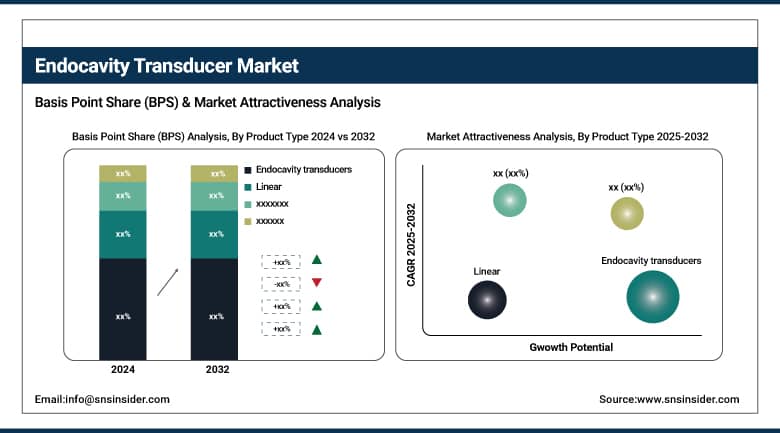

By Product Type

In 2024, endocavity transducers will continue to be the leading products, which will contribute to the growth of the market on the basis of the broad application of endocavity transducers in transvaginal and transrectal imaging for gynecology and urology. They are especially popular in OB/GYN and urology offices, as both their ergonomic design and superior image clarity for deep-tissue structures. By type of product, the segment of phased array is expected to grow at the fastest rate due to its increasing usage in advanced CVS and abdominal imaging. Phased array head probes are becoming more and more common in portable ultrasound due to their small size and ability to penetrate moving organs sensitive to motion, such as the heart, particularly in point-of-care and emergency applications.

By Application

The application of obstetrics and gynecology accounted for 56.8% market share by 2024. The high volume of prenatal and pelvic exams globally, early anomaly detection, and the need for regular reproductive health screening drive this dominance. Transvaginal Ultrasound has become a standard of care in women’s health, and as a result, probes are used more and more frequently.

Urology, on the other hand, is likely to be the fastest-growing application segment. Increasing prevalence of prostate-related diseases, along with increasing use of real-time ultrasound for biopsies and placement of catheters, has been making a substantial contribution toward the overall endocavity transducer market growth, particularly among elderly males.

By End-User

Hospitals are projected to continue as the largest end-user, accounting for 49.2% of the global market share in 2024. These are the common machines due to the high number of patients, availability of complete diagnostic facilities, and widespread presence of multi-disciplinary departments in obstetrics, gynecology, and urology for endocavity transducers use. Hospitals also have more financial and technical resources to equip with high-end ultrasound machines and probe disinfection facilities. Conversely, ambulatory surgical centers (ASCs) are projected to be the fastest-expanding end-use segment and are stimulated by the growing transfer of diagnosis and minimal surgical practices from inpatient locations. ASCs provide efficient, specialized care with faster turnover, which is appealing for common pelvic and prostate applications with endocavity transducers.

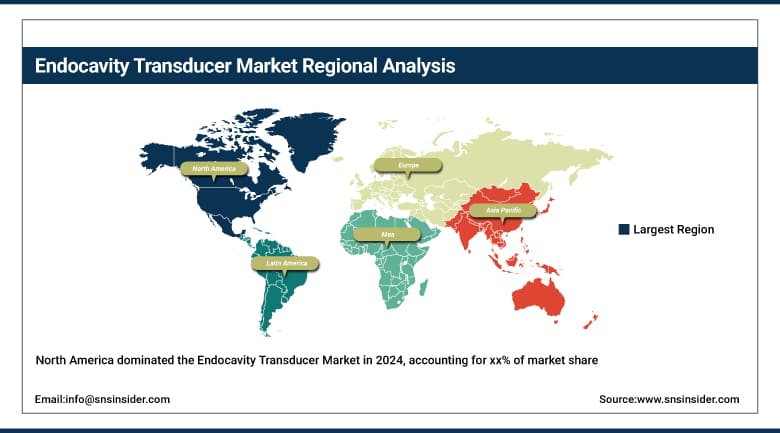

Endocavity Transducer Market Regional Insights:

North America held the maximum share of the global endocavity transducer market, owing to the advanced healthcare infrastructure, a large base of diagnostic imaging users, and well-developed infection control regulations.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Canada is conducive to growth as healthcare becomes increasingly digitized and positive reimbursement models emerge. Mexico presents growing access to ultrasound through public health programs. The market by country reflects that the fastest-growing country in the region is Canada due to the high government investments in the women's health sector and growing adoption of point-of-care ultrasound in the outpatient setting.

The endocavity transducer market is the second largest in Europe, as a result of the presence of universal healthcare coverage, high clinical recommendations, and growing preference for non-invasive diagnostic procedures. Germany dominates the region with the presence of a large number of specialty diagnostic centers and a strong commitment to upgrading ultrasound devices. According to the German Federal Statistical Office (2023), the number of gynecological sonography procedures was 19% higher in comparison with the previous year.

France and the U.K. are also not too far behind the AI-based imaging project for cancer screening. Eastern Europe, Poland, and Turkey in particular, are also seeing a higher investment in hospital infrastructure and diagnostic capability. The fastest-growing country is Italy, due to national women's health programs and the growth in ambulatory care provision of OB/GYN imaging.

The APAC region is the largest market for the endocavity ultrasound transducers market, which is growing due to the rising birth rates, aging population, followed by increasing healthcare infrastructure, and the need for early diagnostics. China takes the lead with such high procedure volumes and growing hospital investment, with the Chinese Health and Sciences Commission observing naturally 27% rise in OB/GYN Diagnostic Visits in 2023. India is next on the list with a fast movement among urban diagnostic centers towards the use of low-cost portable hand-held transducers. Also, government schemes, such as Ayushman Bharat, are promoting diagnostic availability. Japan has a growing market because of development and an elderly population, and there is a high requirement for prostate and pelvic imaging. South Korea is betting on AI-based ultrasound systems, and Singapore is notable for its regulatory fast-tracking of high-level disinfection devices. India is the fastest-growing market in the region, driven by growing awareness of population health and diagnostic investments from the private sector.

Endocavity Transducer Market Key Players:

-

Siemens Healthineers

-

Philips

-

Canon Medical Systems

-

Fujifilm Holdings

-

Hitachi Medical Systems

-

Toshiba Medical Systems

-

Providian Medical

-

Mindray Medical

Recent Developments in the Endocavity Transducer Market:

In April 2024 - CIVCO Medical Solutions announced its expansion of the high-level disinfection product line, integrating automated tracking software to align with CDC compliance standards, streamlining probe sterilization processes.

In March 2024 - A publication in Ultrasound in Medicine & Biology highlighted a novel AI-assisted endocavity transducer capable of real-time tissue characterization, enhancing diagnostic precision in prostate and cervical cancer screenings.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.69 billion |

| Market Size by 2032 | USD 5.53 billion |

| CAGR | CAGR of 5.21% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Curvilinear, Phased array, Endocavity transducers, and Linear) • By Application (Obstetrics/Gynaecology, Urology) • By End User (Hospitals, Ambulatory surgical centers, Clinics, and Diagnostic centers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | GE Healthcare, Siemens Healthineers, Philips, Canon Medical Systems, Fujifilm Holdings, Samsung Medison, Hitachi Medical Systems, Toshiba Medical Systems, Providian Medical, and Mindray Medical |

Frequently Asked Questions

North America dominated the Endocavity Transducer market.

The high price of high-level transducers, which typically range between USD 7,000–10,000, limits the application in small healthcare venues and private clinics.

Rising Demand for Precision Diagnostics, Infection Control Measures, and Technological Innovations.

The market is expected to reach USD 5.53 billion by 2032, increasing from USD 3.69 billion in 2024.

The Endocavity Transducer market is anticipated to grow at a CAGR of 5.21% from 2025 to 2032.

Get in Touch