3D Imaging Market Report Scope & Overview:

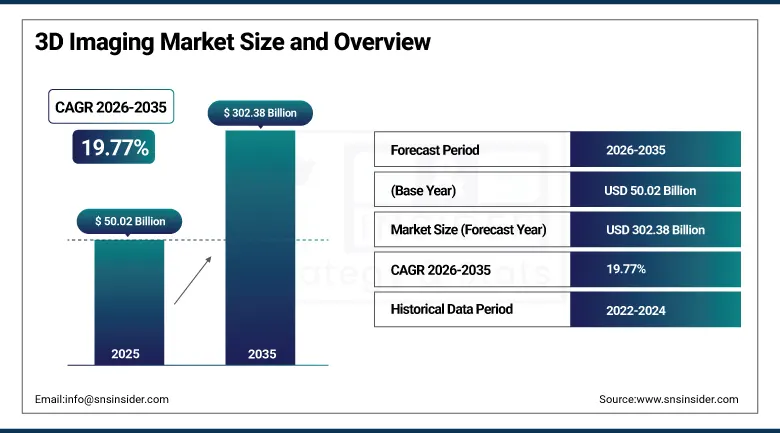

The 3D Imaging Market was valued at USD 50.02 Billion in 2025 and is expected to reach USD 302.38 Billion by 2035, growing at a CAGR of 19.77% from 2026–2035.

The global 3D imaging market is evolving rapidly with rapid development in performance, efficiency, and acceptance across industries. New and improved hardware advances including higher-resolution and higher-frame-rate depth cameras with tight depth accuracy tolerances, more efficient data processing, lower latency, and faster rendering times are driving overall performance and efficiency improvements. The 3D imaging market is driven by several converging factors including the rise in demand for 3D imaging technology for medical diagnostics, surgical and dental planning, increasing demand for 3D content in entertainment, gaming, and virtual reality applications, growing automotive adoption in vehicle design, navigation, and safety systems, and technological advancements in sensors, cameras, and imaging software that are enhancing accuracy and affordability.

In 2024, Apple launched the Vision Pro spatial computing headset integrating LiDAR-based 3D imaging for environment mapping, hand tracking, and spatial audio that creates fully immersive mixed reality experiences for enterprise productivity and consumer entertainment applications. The product launch demonstrates the most commercially significant consumer 3D imaging platform introduction, integrating depth sensing technology previously confined to industrial and medical applications into a mass-market consumer computing device whose spatial computing paradigm creates new application categories for embedded 3D imaging technology.

Market Size and Forecast

-

Market Size in 2026E: USD 59.91 Billion

-

Market Size by 2035: USD 302.38 Billion

-

CAGR: 19.77% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On 3D Imaging Market - Request Free Sample Report

3D Imaging Market Trends

-

Declining LiDAR sensor costs are expanding the adoption of 3D imaging technologies across industrial inspection, construction surveying, agriculture, and infrastructure monitoring applications

-

Growing use of digital twins is driving demand for high-precision 3D imaging solutions that support manufacturing optimization, asset management, and smart city planning

-

Advancements in AI-powered medical imaging are enhancing diagnostic accuracy, surgical planning, and patient-specific anatomical modeling, boosting healthcare adoption

-

Increasing integration of 3D depth-sensing technologies in AR/VR devices is creating strong demand for advanced 3D imaging sensors and components

-

Rising adoption of photogrammetry and structured light scanning in e-commerce, virtual showrooms, and virtual try-on applications is expanding the commercial use of 3D imaging technologies beyond traditional sectors

U.S. 3D Imaging Market Outlook

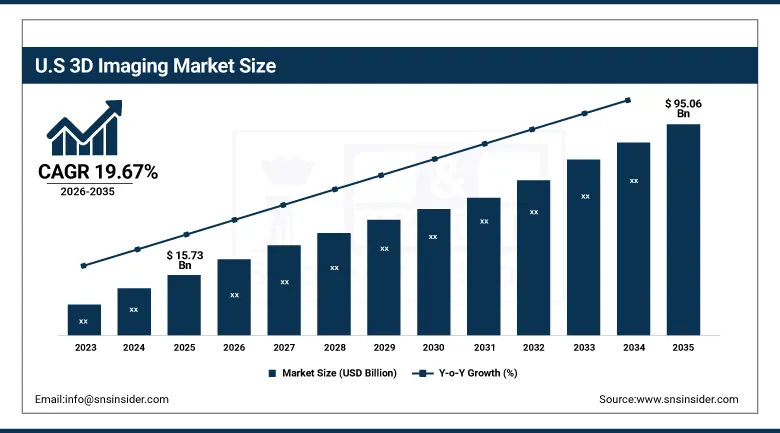

The U.S. 3D Imaging Market was valued at approximately USD 15.73 Billion in 2025 and is expected to reach approximately USD 95.06 Billion by 2035, growing at a CAGR of approximately 19.67%.

The U.S. is the most commercially sophisticated 3D imaging market within North America's dominant revenue position. Apple, Microsoft (Hololens), Meta (Quest), Sony, Matterport, FARO Technologies, and Leica Geosystems’ U.S. operations collectively define the domestic 3D imaging commercial landscape. The healthcare sector’s medical imaging adoption, the automotive industry’s ADAS LiDAR procurement, the entertainment and media sector’s volumetric content capture investment, and the construction industry’s BIM integration with 3D scanning create the most commercially diverse 3D imaging demand environment of any national market. Apple Vision Pro’s commercial launch created the most commercially significant consumer 3D imaging platform deployment in history.

In 2023, FARO Technologies launched the FARO Laser Projector FARO Cobalt Array Imager for high-resolution 3D scanning of industrial parts with sub-millimeter accuracy in manufacturing quality control environments, enabling inline inspection at production line speeds. The product launch demonstrates the commercial direction of industrial 3D imaging toward real-time production integration whose speed and accuracy requirements exceed what portable scanning alternatives can provide in high-throughput manufacturing quality assurance applications.

3D Imaging Market Segment Analysis

-

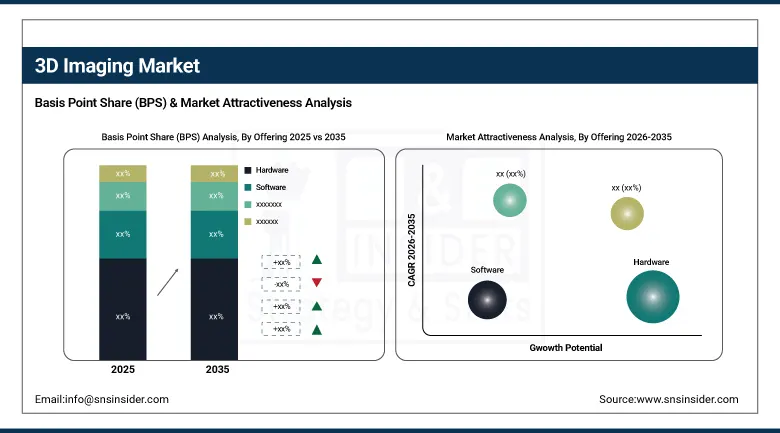

By Offering, the Hardware segment dominated the 3D Imaging Market with approximately 55% share in 2025, while the Software segment is the fastest growing.

-

By Deployment, the On-Premise segment dominated the 3D Imaging Market with approximately 62% share in 2025, while the Cloud deployment segment is the fastest growing.

-

By Organization Size, the Large Enterprises segment dominated the 3D Imaging Market with approximately 68% share in 2025, while the SMEs segment is the fastest growing.

-

By End-use, the Healthcare & Life Sciences segment dominated the 3D Imaging Market with approximately 28% share in 2025, while the Automotive & Transportation segment is the fastest growing.

By Offering, hardware dominates, software grows fastest

Hardware retained the dominant offering position with approximately 55% of the 3D imaging market in 2025. The foundational requirement for 3D imaging sensors, depth cameras, and scanner hardware whose deployment is the prerequisite for all downstream software processing and service delivery creates hardware’s commercial dominance. Medical CT scanners, industrial LiDAR sensors, structured light projection systems, and photogrammetry camera rigs each represent hardware categories whose commercial aggregate across healthcare, automotive, industrial, and entertainment applications sustains the hardware segment’s market leadership. The automotive sector’s LiDAR adoption for ADAS, whose per-vehicle hardware procurement multiplied by global vehicle production creates volume commercial relationships, represents the fastest-growing single hardware procurement category within the dominant segment.

Software is the fastest-growing offering because the expanding 3D imaging hardware installed base creates growing demand for AI-powered point cloud processing, digital twin creation, 3D model optimization, and augmented reality rendering platforms whose value compounds with the hardware installation count. Each new 3D scanner installation creates software procurement whose recurring subscription revenue and capability expansion through AI feature integration sustains above-hardware growth rates. The digital twin market’s extraordinary expansion, using 3D imaging data as the physical measurement input for virtual model creation, creates 3D imaging software demand that compounds with digital twin investment across manufacturing, infrastructure, and construction sectors.

By End-use, healthcare dominates, automotive grows fastest

Healthcare and life sciences retained the dominant end-use position with approximately 28% of the 3D imaging market in 2025. Medical diagnostic imaging whose CT, MRI, and 3D ultrasound systems create patient-specific anatomical 3D models for surgical planning, radiation therapy treatment planning, and prosthetics design defines the most commercially established and highest-per-system-value 3D imaging application category. 3D dental scanning’s replacement of conventional impressions with intraoral scanning creates consistent procurement across dental practices whose patient-facing workflow improvement and laboratory integration sustain commercial adoption growth. Surgical simulation’s use of patient-specific 3D anatomical models for pre-operative planning creates premium imaging software procurement whose value is measured in surgical outcome improvement.

Automotive and transportation is the fastest-growing end use because ADAS LiDAR sensor integration across vehicle production lines, autonomous vehicle perception system development, and automotive design digital prototyping create above-average embedded 3D imaging procurement growth that compounds with both ADAS regulatory mandate adoption and AV development programme investment. Each ADAS-equipped vehicle that integrates one or more LiDAR, structured light, or ToF depth sensor creates 3D imaging hardware procurement whose per-vehicle content grows with ADAS feature sophistication. Autonomous vehicle development programme’s data collection requirements, using 3D imaging to capture precise environment geometry for HD map creation and system training, create above-average development-phase procurement.

By Deployment, on-premise dominates, cloud grows fastest

On-premise deployment retained the dominant position with approximately 62% of the 3D imaging market in 2025. Industrial quality control, medical imaging, and precision manufacturing applications’ real-time processing requirements whose latency sensitivity prevents cloud-dependent processing create specification preference for locally-deployed 3D imaging processing infrastructure. Medical imaging’s HIPAA patient data protection requirements, combined with the critical care environment’s continuous availability requirement for diagnostic imaging systems, creates on-premise deployment preference that cloud alternatives cannot satisfy at equivalent reliability. Industrial 3D scanning’s integration with production line automation control systems whose network connectivity requirements are managed within the facility’s internal network creates additional on-premise deployment preference.

Cloud deployment is the fastest-growing segment because large-scale 3D point cloud storage, geographically distributed team access to shared 3D models, and AI-powered 3D analysis platforms create demand for cloud-delivered 3D imaging processing whose collaborative value and elastic storage economics create commercial motivation that on-premise infrastructure cannot match. Each construction project that uses 3D scanning for progress monitoring creates cloud storage demand for accumulated point cloud data whose volume compounds with scan frequency. Each enterprise digital twin programme that consolidates 3D imaging data from multiple facilities creates cloud-delivered 3D model management demand that sustains the segment’s fastest-growing status.

By Organization Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant organization size position with approximately 68% of the 3D imaging market in 2025. The substantial capital investment required for industrial CT systems, enterprise LiDAR survey platforms, medical imaging equipment, and comprehensive 3D processing software suites creates adoption concentration among organizations with above-average technology capital budgets. Each major automotive OEM’s design studio, each hospital network’s radiology department, and each aerospace manufacturer’s quality engineering facility creates 3D imaging procurement whose commercial relationships sustain long-duration equipment and software partnerships with major 3D imaging system providers.

SMEs are the fastest-growing organization size because portable handheld 3D scanners whose commercial price has declined from tens of thousands to thousands of dollars, 3D imaging subscription software, and 3D imaging-as-a-service outsourcing are progressively making professional 3D scanning capability commercially accessible at business scales that previously required enterprise capital budgets. Each SME manufacturer that adopts handheld structured light scanning for quality inspection, each small dental practice that adopts intraoral scanning, and each architecture firm that adopts point cloud survey data creates 3D imaging procurement whose aggregate compounds with SME sector technology adoption growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America 3D Imaging Market Insights

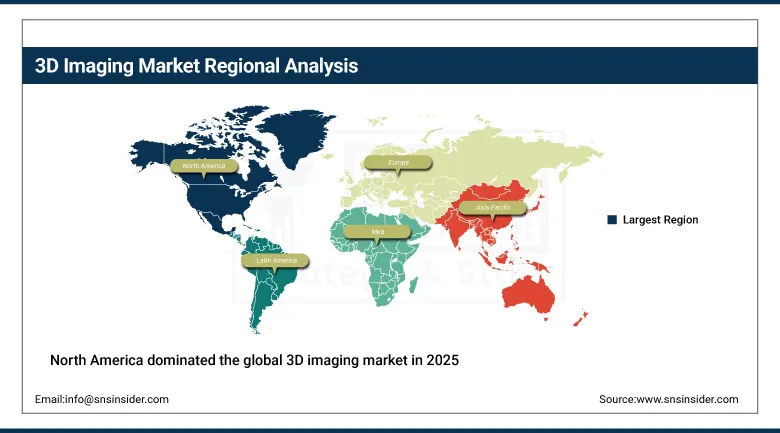

North America dominated the global 3D imaging market in 2025 through its concentration of leading 3D imaging technology developers including Apple, Microsoft, Meta, FARO Technologies, and Leica Geosystems, combined with the most commercially advanced healthcare imaging, automotive, and entertainment industry adoption environments. The United States accounts for approximately 87.4% of North American revenues through its technology sector leadership, medical imaging investment, and aerospace and defense 3D measurement programme.

Canada contributes approximately 12.6% of North American revenues through its aerospace manufacturing sector’s 3D inspection investment, the growing construction sector’s BIM-integrated scanning adoption, and the natural resources industry’s LiDAR survey deployment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe 3D Imaging Market Insights

Europe is a technically sophisticated 3D imaging market where the automotive manufacturing sector’s design and quality engineering investment, the manufacturing industry’s inline inspection adoption, and the healthcare sector’s medical imaging infrastructure create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive OEM sector’s 3D design and ADAS LiDAR investment, the manufacturing quality engineering sector’s precision measurement adoption, and Zeiss and Artec Europe’s domestic 3D imaging commercial presence.

The United Kingdom, France, and the Netherlands are significant secondary markets where the aerospace industry’s precision measurement investment, healthcare imaging adoption, and the creative media sector’s volumetric content capture create consistent 3D imaging commercial demand.

Asia Pacific 3D Imaging Market Insights

Asia Pacific is the fastest-growing regional 3D imaging market, driven by China's extraordinary electronics and automotive manufacturing scale, Japan's precision engineering and robotics investment, South Korea's semiconductor and electronics manufacturing quality adoption, and India's growing manufacturing and healthcare sectors. China accounts for approximately 44.8% of Asia Pacific revenues through its automotive production’s LiDAR investment, the electronics manufacturing sector’s 3D inspection adoption, and the government’s smart city 3D mapping programme.

Japan and South Korea represent technically sophisticated secondary markets where semiconductor manufacturing’s precision 3D inspection, automotive design’s digital prototyping, and the consumer electronics sector’s AR device depth sensor procurement create consistent above-average per-industry 3D imaging investment.

MEA & Latin America 3D Imaging Market Insights

UAE leads MEA revenues at approximately 38.4% through its smart city 3D mapping investment, the construction sector’s BIM-integrated scanning adoption, and the growing healthcare sector’s medical imaging infrastructure. Brazil leads Latin American revenues at approximately 44.2% through its automotive and aerospace manufacturing quality inspection, the mining sector’s LiDAR survey adoption, and the healthcare sector’s medical imaging expansion. Saudi Arabia’s NEOM smart city 3D mapping programme and South Africa’s mining industry LiDAR deployment collectively sustain growing regional 3D imaging market development through 2035.

Market Dynamics

Growth Drivers: Healthcare diagnostic imaging and automotive LiDAR ADAS adoption creating structured procurement

Healthcare diagnostic imaging is the 3D imaging market’s most commercially established structural growth driver. Medical CT, 3D MRI, 3D ultrasound, and intraoral dental scanning collectively represent the most commercially mature 3D imaging application categories whose per-system commercial value and renewal cycle create predictable long-duration procurement relationships. The ageing global population’s growing diagnostic imaging requirement, the surgical planning simulation market’s 3D model demand, and the orthopedic implant design sector’s patient-specific 3D anatomical model requirement collectively sustain healthcare’s dominant end-use position while creating above-average per-application commercial value.

Automotive LiDAR ADAS adoption is creating the most commercially dynamic volume procurement growth for 3D imaging sensors. Each ADAS-equipped vehicle that integrates LiDAR for adaptive cruise control, automatic emergency braking, and lane keeping creates per-vehicle 3D imaging hardware procurement whose aggregate across global vehicle production compounds with ADAS feature penetration growth. NCAP mandatory ADAS requirements and NHTSA AEB mandates create defined regulatory adoption timelines whose commercial procurement is predictable across annual vehicle production volumes.

Restraints: High initial investment and data management complexity for large-scale 3D imaging deployment

High capital investment for industrial-grade 3D scanning systems, medical imaging equipment, and enterprise LiDAR platforms creates adoption barriers that limit 3D imaging deployment to organizations whose capital budgets accommodate the system’s purchase, installation, and integration cost. Each organization whose IT infrastructure cannot efficiently process, store, and manage the large point cloud data volumes that 3D imaging systems generate creates deployment limitation whose data management investment requirement adds to the total cost of ownership.

Integration complexity between 3D imaging hardware, data processing software, and downstream ERP, PLM, and CAD systems creates implementation engineering investment whose cost and timeline create adoption barriers for organizations without specialist 3D imaging integration expertise. Each custom integration requirement extends the time-to-value timeline that justifies 3D imaging procurement investment.

Opportunities: Digital twin adoption and consumer AR/VR 3D sensor volume market

Digital twin adoption using 3D imaging as the physical measurement input for virtual model creation represents the most commercially transformative near-term 3D imaging market opportunity. Each manufacturing facility digital twin, each infrastructure asset digital twin, and each healthcare anatomical model digital twin creates 3D imaging procurement whose commercial relationship compounds with digital twin update cycle investment. The digital twin market’s extraordinary expansion creates structured 3D imaging procurement that sustains above-average market growth independently of traditional quality inspection and medical imaging demand cycles.

Consumer AR/VR 3D sensor volume market represents the most commercially significant near-term hardware volume growth opportunity whose per-device procurement multiplication across consumer device shipment volumes creates aggregate sensor demand substantially exceeding professional market equivalents. Apple Vision Pro’s commercial launch establishes the consumer spatial computing category whose market expansion creates 3D depth sensing hardware procurement at consumer device volume economics.

Recent Developments:

-

2024: Apple launched the Vision Pro spatial computing headset in 2024 integrating LiDAR-based 3D imaging for environment mapping, hand tracking, and spatial audio, creating the most commercially significant consumer 3D imaging platform and establishing the spatial computing device category.

-

2024: FARO Technologies launched the FARO Cobalt Design SX structured light 3D scanner in 2024 with enhanced scanning speed and sub-millimeter accuracy for industrial design verification and reverse engineering applications targeting the automotive and aerospace manufacturing quality engineering markets.

-

2024: Matterport launched Matterport Pro3 camera enhancements in 2024 with improved LiDAR accuracy, extended range scanning, and enhanced cloud processing integration for commercial real estate, construction progress monitoring, and insurance documentation applications.

-

2023: FARO Technologies launched the FARO Laser Projector Cobalt Array Imager in 2023 for high-resolution 3D scanning of industrial parts with sub-millimeter accuracy in manufacturing quality control environments, enabling inline inspection at production line speeds.

-

2023: Leica Geosystems launched the Leica BLK2GO PULSE mobile LiDAR scanner in 2023 with real-time 3D color point cloud capture during walking survey, targeting construction site progress monitoring, heritage documentation, and infrastructure inspection applications requiring rapid large-area 3D data capture.

3D Imaging Market Key Players

-

Apple Inc.

-

Microsoft Corporation (HoloLens)

-

Meta Platforms Inc.

-

Sony Corporation

-

FARO Technologies Inc.

-

Leica Geosystems AG

-

Matterport Inc.

-

Artec 3D

-

Riegl Laser Measurement Systems

-

Trimble Inc.

-

Teledyne Technologies

-

Cognex Corporation

-

Keyence Corporation

-

Creaform

-

Nikon Metrology

-

Perceptron Inc.

-

GOM GmbH

-

Photoneo s.r.o.

-

Mech-Mind Robotics

-

LiDAR USA

3D Imaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 50.02 Billion |

| Market Size by 2035 | USD 302.38 Billion |

| CAGR | CAGR of 19.77% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Offering (Hardware, Software, Services) • by Deployment (On-Premise, Cloud) • by Organization Size (Large Enterprises, Small and Medium-sized Enterprises) • by End-use (Automotive & Transportation, Manufacturing, Healthcare & Life Sciences, Architecture & Construction, Media & Entertainment, Security & Surveillance, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Apple Inc., Microsoft Corporation (HoloLens), Meta Platforms Inc., Sony Corporation, FARO Technologies Inc., Leica Geosystems AG, Matterport Inc., Artec 3D, Riegl Laser Measurement Systems, Trimble Inc., Teledyne Technologies, Cognex Corporation, Keyence Corporation, Creaform, Nikon Metrology, Perceptron Inc., GOM GmbH, Photoneo s.r.o., Mech-Mind Robotics, LiDAR USA |

Frequently Asked Questions

The 3D Imaging Market is expected to grow at a CAGR of 19.77% from 2026 to 2035.

The 3D Imaging Market was valued at USD 50.02 Billion in 2025.

Healthcare diagnostic imaging demand from medical CT, 3D MRI, and surgical planning creating commercially established procurement, and automotive LiDAR ADAS sensor adoption creating volume 3D imaging hardware procurement that compounds with global vehicle production and ADAS regulatory mandate adoption.

Healthcare & Life Sciences dominated the 3D Imaging Market with approximately 28% share in 2025, while Automotive & Transportation is the fastest growing segment.

North America dominated the 3D Imaging Market in 2025, while Asia Pacific is the fastest-growing region driven by China's automotive and electronics manufacturing scale.

Get in Touch