Fire Resistant Lubricants Market Size & Overview:

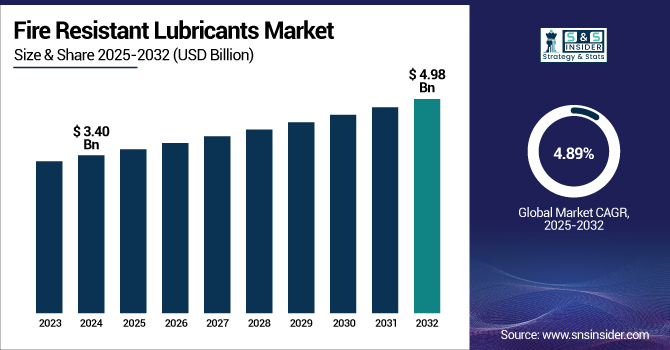

The Fire Resistant Lubricants Market size was USD 3.40 billion in 2024 and is expected to reach USD 4.98 billion by 2032 and grow at a CAGR of 4.89% over the forecast period of 2025-2032.

To Get more information on Fire Resistant Lubricants Market - Request Free Sample Report

Rising usage in the metal processing & mining industry drives the fire resistant lubricants market growth. The increasing use of fire-resistant lubricants in the metal processing and mining industries is a significant factor due to the nature of these high-risk and high-temperature environments. Extreme heat and heavy loads in metal processing increase the fire hazard of conventional lubricants. Flame retardant replacements not only ensure the safety and efficiency of operation, but also help attain rigid safety standards set out by various industries.

The fire resistant lubricants market companies focused on development. For instance, in January 2024, Shell U.K. Limited purchased synthetic and natural ester-based transformer fluids, MIDEL and MIVOLT brands, from M&I Materials Ltd., offering solutions with improved fire safety and environmental performance.

Fire Resistant Lubricants Market Dynamics:

Drivers:

-

Expansion of Automation and Robotics in Industry Drive Market Growth

The rise in automation and robotics in diverse industries is majorly contributing to the fire resistant lubricants industry expansion, as such systems require specialized lubricants to function in high-performance and automated systems. With industries, from manufacturing to mining to the automotive sector, evolving to more robotic processes and automated machines, the equipment becomes greater and more complicated, resulting in a higher risk of it overheating and facing a mechanical breakdown.

For instance, in 2024, The market saw its industrial robot density increase to 470 robots per 10,000 workers, more than twice its figure of 2019, to overtake Germany's level and to become third globally after South Korea and Japan. This increase in automation is driven by huge investments in automation, and China is already in first place in robot adoption, even before Japan and Germany.

Moreover, with a growing dependence on automated systems in industries, the need for fire resistant lubricants is expected to increase to facilitate the operation of high-performance machinery safely and effectively.

Restraints:

-

Complexity in Formulation and Application May Hamper the Market Growth

Complexity in the formulation and application of fire-resistant lubricants can hinder the growth of the market. Many fire-resistant lubricants use special synthetic blends and formulations to maintain extreme temperatures and pressures without sacrificing performance. Generating these specialty formulations necessitates extensive research, technical capabilities, and high-end raw materials, which all result in elevated production prices. The use of these lubricants also demands both equipment and specialized knowledge for their application, mainly in mining, manufacturing, and aerospace sectors.

Trends:

-

Development of Smart Lubricants Trends Propel Market Growth

Smart lubricants development is one of the trends that is expected to witness growth in demand in the fire resistant lubricants market. These newly advanced lubricants are embedded with a sensor that can help to monitor lubricant health through real-time data transmission by monitoring various parameters, such as temperature, viscosity, contamination, and overall lubricant health. This allows for predictive maintenance, minimal equipment downtime, and improved operational safety, especially for industries, such as metal processing, mining, and power generation, where equipment malfunction could pose fire risks.

In 2024, several key players focused on the fire resistant lubricants market trends, came up with substantial developments in smart lubricants that utilize sensor technologies and real-time surveillance. Such innovations are designed to improve safety, performance, and lower maintenance costs in aggressive industrial applications.

For instance, ExxonMobil launched new smart thermally conductive fire-resistant lubricants and anchoring sensors that allow real-time monitoring of temperature and other lubricant condition and performance metrics. The advancement allows for predictive maintenance and improves operational efficiency in industries, such as metal processing and power generation.

Fire Resistant Lubricants Market Segmentation Analysis:

By Type

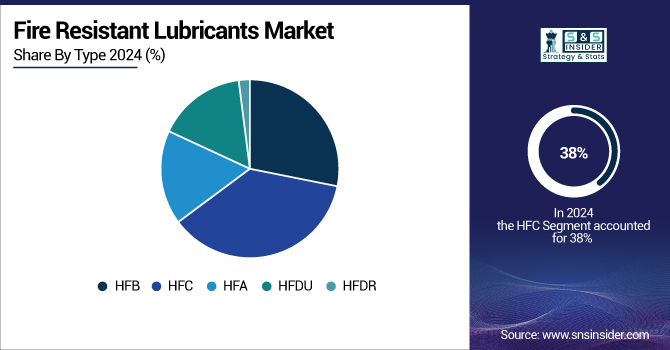

HFC held the largest fire resistant lubricants market share, around 38%, in 2024 owing to their favorable safety features and broad industrial acceptability. These are water-based lubricants that provide superior fire resistance, minimizing the risk of burning in high-temperature or high-pressure applications. Being non-flammable, they are suited for use in high-danger regions including steel production factories, mining, and generating regions, in which the danger of fire is excessive. Moreover, HFC fluids not only offer automatic lubrication and corrosion protection but are also the cheapest alternative to other, more costly fire-resistant alternatives, such as phosphate esters.

HFDU held a significant market share due to the great performance characteristics of these fluids in high-temperature and high-pressure industrial applications. HFDU fluids are fully synthetic and not water-based alternatives, which gives them an additional boost in thermal stability, oxidation resistance, and their lubricating properties.

By End-Use Industry

In 2024, the construction segment held the largest market share of approximately 38%. This is due to the construction relies on machinery including excavators, cranes, bulldozers, and hydraulic systems that need lubricants able to endure tough working conditions and maintain equipment safety. Fire-resistant lubricants are essential to mitigate fire risks in these high-risk applications, particularly in confined spaces or high-heat areas of construction such as tunnels, high-rise buildings, and infrastructure projects.

Mining segment held a significant market share. The segment’s expansion is driven by the high exposure to accident at the work site, inherent dangers of mining operations, and a heavy usage of power-driven machines in a limited space of a combustible atmosphere. Drills, conveyors, crushers, hydraulic systems, and similar machinery work in extreme conditions of extreme pressure and temperature and under high friction rates, which increases the fire hazard. Fireproof lubricants play a crucial role in minimizing these hazards by lowering the risk of ignition and ensuring proper functioning in critical conditions.

Fire Resistant Lubricants Market Regional Outlook:

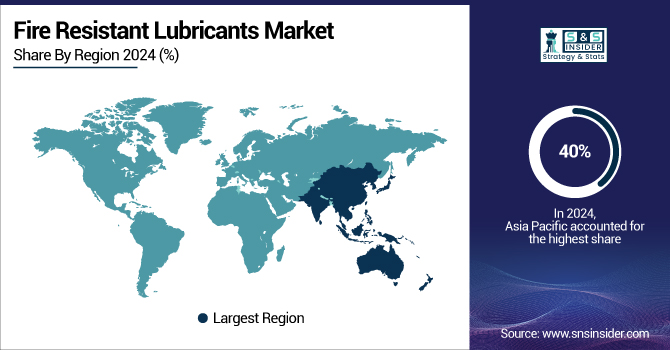

Asia Pacific held the largest market share of approximately 40% in 2024. The region’s growth is driven by the rapid industrialization in the region, along with higher demand for industrial safety solutions and a large manufacturing base. The hydraulic machinery and high-performance lubricants market has continued to grow rapidly in countries such as China, India, Japan, and South Korea, on the back of booming sectors including construction, mining, steel, automotive, and power generation. This is further being supported by increasing implementation of workplace safety regulations and growing adoption of automated and heavy-duty equipment, boosting the regional demand for fire resistant lubricants.

For instance, in 2024, Chevron Oronite's OLOA® 59361 won the F&L Asia Product Development of the Year Award. FORMULA 1400 is a next-generation additive for heavy-duty lubricants used in a wide range of engines, including those in Asia Pacific countries, such as China and India. Its compatibility with re-refined base oils and biodiesel blends most often found in markets abroad, including Indonesia, Malaysia, and Thailand, also demonstrates its ability to adapt to regional market requirements.

North America held a significant market share and is expected to be the fastest-growing segment during the forecast period due to its well-established advanced manufacturing industry, along with a strong industrial core and stringent regulatory system. High-performance lubricants that provide safe operation under extreme conditions are required by industries, which are common throughout the U.S. and Canada, including aerospace, metal processing, construction, and mining.

The U.S held the largest market share, which was around 76% in 2024, and is projected to growth with the highest CAGR of 6.17% during the forecast period. The region’s growth is driven by the companies' focus on production. In 2022, Eastman Chemical Company announced its investment in new capacity at the Anniston, Alabama, plant to expand production of its fire-resistant fluid for Therminol 66 heat transfer fluid. Scheduled to be completed in 2024, this expansion will increase the U.S.-based capacity by 50%, strengthening Eastman's capacity to support the growing demand for fire resistant lubricants used across many industrial applications.

Europe is expected to hold a significant market share during the forecast period due to the existence of stringent government regulations backed with advanced technology, along with the presence of various industries that require high-performance lubricants. With strict safety and environmental standards implemented in the European Union, industries, such as aerospace, automotive, mining, pan & plant, and manufacturing, have switched to fire-resistant lubricants as per the need for compliance with the regulations that are accomplishing requirements for fire safety.

Middle East & Africa also held a significant market share. The region has substantial oil & gas and mining activities, which require high-performance lubrication under extreme conditions. Saudi Arabia, the UAE, South Africa, etc. have some of the planet's biggest oil refineries and mineral extraction operations, and fire hazards are significant in high-pressure, high-temperature machinery. As a result, these industries also need specific fire-resistant lubricants to ensure safe and going operations. Moreover, the adoption of the region's lubricants is boosted by government regulations and industry standards towards worker safety and environmental protection.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players:

The fire resistant lubricants market companies include ExxonMobil Corporation, Shell plc, BP p.l.c, TotalEnergies SE, Fuchs Petrolub Se, Quaker Houghton, Chevron Corporation, The Dow Chemical Company, Eastman Chemical Company, and American Chemical Technologies Inc.

Recent Developments:

-

In 2024, Kodiak acquired Aztech Lubricants to enhance its specialty chemical portfolio to provide new markets and high-performance fire-resistant hydraulic fluids. The acquisition is expected to position Kodiak to expand its offering of advanced fluid solutions to industries.

-

In 2024, Shell U.K. Limited announced the completion of the acquisition of MIDEL and MIVOLT brands from M&I Materials Ltd., placing Shell in the pole position for fire-resistant hydraulic fluids.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.40 Billion |

| Market Size by 2032 | USD 4.98 Billion |

| CAGR | CAGR of 4.89% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (HFA, HFB, HFC, HFDU, HFDR) •By End-Use Industry (Metal Processing, Mining, Power Generation, Aerospace, Marine, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ExxonMobil Corporation, Shell plc, BP p.l.c., TotalEnergies SE, Fuchs Petrolub Se, Quaker Houghton, Chevron Corporation, The Dow Chemical Company, Eastman Chemical Company, American Chemical Technologies Inc. |

Frequently Asked Questions

Asia Pacific led the Fire Resistant Lubricants Market in the region with the highest revenue share in 2024.

Expansion of automation and robotics in industry drives the market growth.

Construction will grow rapidly in the Fire Resistant Lubricants Market from 2025 to 2032.

The expected CAGR of the global Fire Resistant Lubricants Market during the forecast period is 4.89%

The Fire Resistant Lubricants Market was valued at USD 3.40 billion in 2024.

Get in Touch