Heat Transfer Fluids Market Report Scope & Overview:

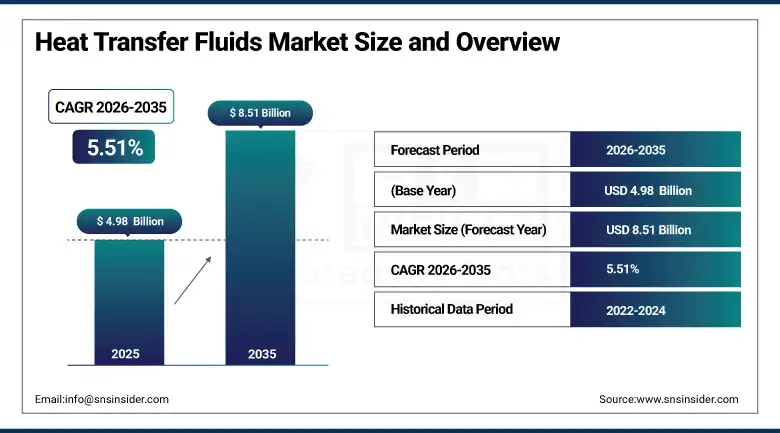

The Heat Transfer Fluids Market was valued at USD 4.98 Billion in 2025 and is expected to reach USD 8.51 Billion by 2035, growing at a CAGR of 5.51% from 2026–2035.

The market for global heat transfer fluids continues to develop since industrial users such as those in chemical processing, oil and gas refining, power production, and renewables continue to invest in sophisticated heat transfer fluids that will help them achieve temperature stability and low energy costs while improving overall efficiency where standard methods of cooling and heating have failed. Heat transfer fluids include mineral oils that are known to be economically viable and available, synthetic fluids that can operate effectively in very high temperatures, and glycols, which because of their corrosion and anti-freeze properties are suitable for use in the automobile industry and HVAC equipment.

In June 2023, Dow Inc. partnered with an oil and gas company to supply high-performance heat transfer fluids for a new offshore drilling project in the Gulf of Mexico, reflecting the growing demand for thermic fluids in the oil and gas sector and Dow’s continued investment in the industry. The collaboration demonstrated heat transfer fluid suppliers’ strategic positioning toward high-value offshore energy infrastructure projects whose extreme operating environment and safety-critical thermal management requirements create premium product specification opportunities beyond conventional industrial heating applications.

Market Size and Forecast

- Market Size in 2026E: USD 5.25 Billion

- Market Size by 2035: USD 8.51 Billion

- CAGR: 5.51% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: Asia Pacific

To Get more information On Heat Transfer Fluids Market - Request Free Sample Report

Heat Transfer Fluids Market Trends

-

Concentrated solar power and geothermal renewable energy projects are creating growing high-temperature heat transfer fluid demand globally.

-

Synthetic fluid formulations with enhanced thermal stability are replacing mineral oils in extreme-temperature chemical processing applications.

-

Eco-friendly and long-life fluid formulations are reducing thermal degradation risk while supporting safer disposal practices.

-

Energy efficiency regulations are driving industrial process heating upgrades that specify advanced heat transfer fluid systems.

-

Biofuel and renewable feedstock-derived heat transfer fluid development is advancing as sustainability requirements tighten across industrial sectors.

The U.S. Heat Transfer Fluids Market Outlook

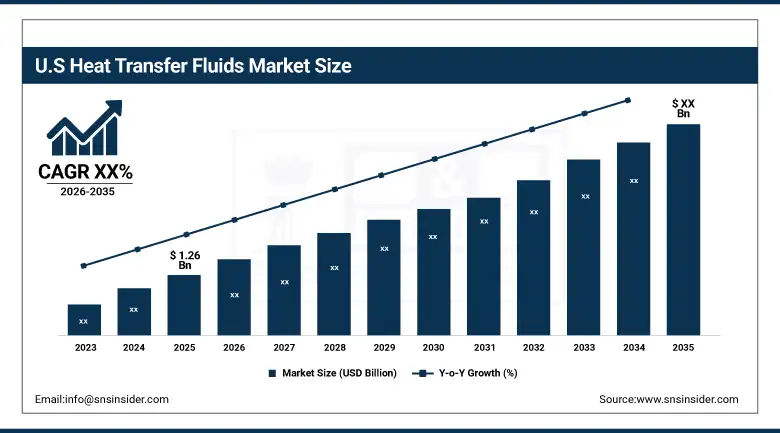

The U.S. Heat Transfer Fluids Market is estimated to be USD 1.49 Billion in 2025 and is projected to reach USD 2.67 Billion by 2035, growing at a CAGR of 6.01% during 2026–2035.

The United States leads North American heat transfer fluids revenues through its large chemical and petrochemical processing industry’s thermal management requirements, the extensive oil and gas refining sector’s process heating demand, and growing renewable energy infrastructure investment including concentrated solar power and geothermal systems. Eastman Chemical, Dow Inc., and Huntsman International sustain U.S. market leadership through their comprehensive synthetic and mineral oil-based heat transfer fluid portfolios.

In 2024, Eastman Chemical Company expanded its Therminol heat transfer fluid product line with enhanced thermal stability formulations targeting concentrated solar power applications, providing utility-scale solar thermal plant operators with fluids capable of sustained operation at temperatures exceeding 400 degrees Celsius without significant degradation. The expansion addressed the growing renewable energy sector’s demand for high-performance thermal fluids whose extended service life reduces the operational cost of large-scale solar thermal energy storage and generation systems.

Heat Transfer Fluids Market Segment Analysis

-

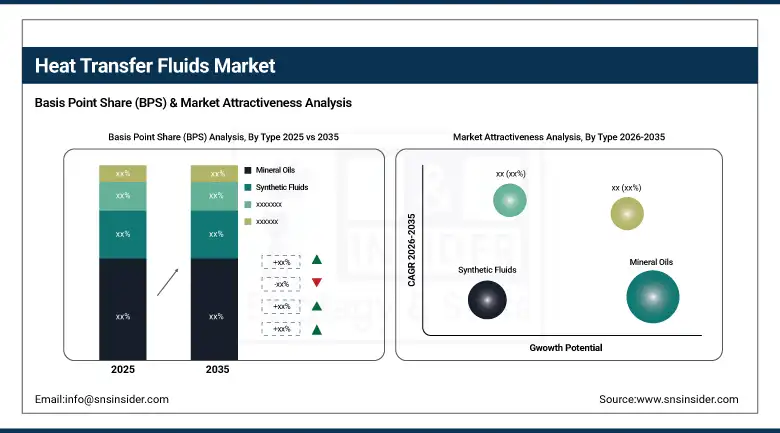

By Type, the mineral oils segment dominated the heat transfer fluids market in 2025, accounting for approximately 42.8% of total market revenue, while the synthetic fluids segment is projected to be the fastest-growing during 2026–2035, expanding at a CAGR of approximately 6.9%.

-

By End-Use Industry, the chemical & petrochemicals segment dominated the heat transfer fluids market with the largest share through extensive thermal management requirements, while renewable energy is the fastest-growing end-use driven by concentrated solar power and geothermal project investment.

By Type, mineral oils dominate, synthetic fluids grow fastest

Mineral oils retained the dominant type position with the largest share of the heat transfer fluids market, due to their cost-effectiveness, wide availability, and reliable performance across a broad range of industrial heating applications. These fluids are widely used in sectors such as chemical processing, food manufacturing, and oil and gas refining, where stable thermal conductivity and operational efficiency are essential. Their compatibility with existing heat transfer systems and relatively lower maintenance requirements continue to support strong adoption across industrial facilities whose process heating temperature requirements fall within mineral oil’s effective operating range.

Synthetic fluids are the fastest-growing type because their superior thermal stability at extreme temperatures, oxidation resistance, and performance in extreme conditions make them a preferred option for mission-critical applications operating above 200 degrees Celsius, including concentrated solar power plants, high-temperature chemical synthesis, and specialty petrochemical processing. Each new high-temperature industrial process or renewable energy installation that specifies synthetic fluid capability beyond mineral oil’s thermal limits creates above-baseline synthetic fluid procurement whose premium pricing reflects the specialized performance characteristics required.

By End-Use Industry, chemical & petrochemicals dominate, renewable energy grows fastest

Chemical and petrochemicals retained the dominant end-use position with the largest share of the heat transfer fluids market due to its extensive and continuous demand for precise thermal management solutions. This sector encompasses a wide range of processes such as distillation, polymerization, and chemical synthesis, which require accurate temperature control to maintain product quality and process efficiency. Heat transfer fluids are essential in these processes for maintaining optimal reaction conditions, ensuring process safety, and enhancing energy efficiency, with the rapid expansion of the global chemical industry, particularly in Asia-Pacific countries like China and India, amplifying demand for heat transfer fluids to support rising production capacities in plastics, fertilizers, and specialty chemicals.

Renewable energy is the fastest-growing end-use industry as governments worldwide heavily invest in renewable energy projects where thermic fluids play a critical role in heat transfer processes, such as in concentrated solar power and geothermal systems. The high demand for clean energy is thought to be a major factor driving the segment’s growth, with power generation from solar photovoltaic increasing substantially and concentrated solar thermal projects requiring specialized high-temperature heat transfer fluid systems whose installation creates substantial new fluid procurement independent of conventional industrial heating demand cycles.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

48.6% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Middle East & Africa |

Saudi Arabia |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Heat Transfer Fluids Market Insights

North America held a significant market share in the heat transfer fluids market in 2025, driven by the rising adoption of advanced thermal management solutions and high demand from chemical processing, oil and gas, HVAC, and food and beverage industries where effective temperature control is essential for operational efficiency. The United States accounts for approximately 82.5% of North American revenues through Eastman Chemical, Dow Inc., and Huntsman International’s comprehensive heat transfer fluid portfolios.

Canada contributes supplementary North American revenues through its oil and gas extraction sector’s process heating requirements, the growing renewable energy sector’s thermal fluid procurement for solar and geothermal installations, and the chemical processing industry’s consistent demand for reliable thermal management across its industrial base.

Europe Heat Transfer Fluids Market Insights

Europe is a significant heat transfer fluids market where stringent environmental regulations promote eco-friendly and long-life fluid formulations, the established chemical and pharmaceutical manufacturing base creates consistent thermal management demand, and growing renewable energy investment under EU climate targets sustains fluid procurement growth. Germany accounts for approximately 22.4% of European revenues through its large chemical processing industry and advanced industrial technology sector.

France’s nuclear and renewable energy infrastructure’s thermal management requirements, Italy’s pharmaceutical manufacturing sector’s process heating needs, and the Nordics’ advanced industrial efficiency standards collectively sustain European heat transfer fluids market development. EU regulatory frameworks favoring sustainable and non-toxic fluid formulations are progressively shaping product specification across the continent.

Asia Pacific Heat Transfer Fluids Market Insights

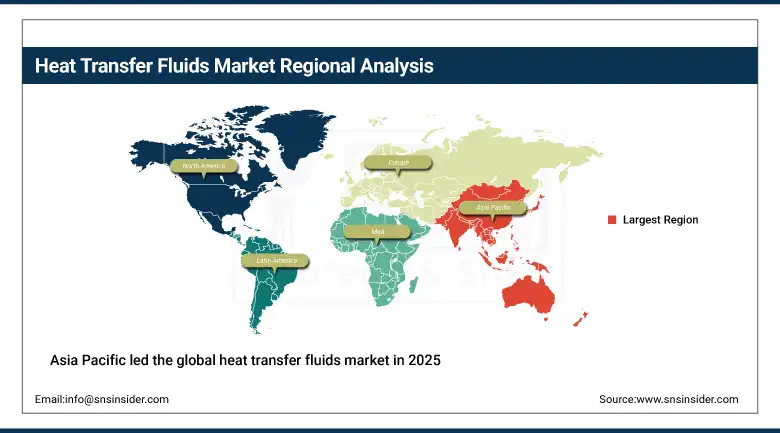

Asia Pacific led the global heat transfer fluids market in 2025, accounting for approximately 38.7% of total market revenue, driven by significant growth in the pharmaceuticals and chemical processing industries, increasing adoption of concentrated solar power, and rapid industrialization across the region. China accounts for approximately 48.6% of Asia Pacific revenues through its large-scale industrial production and rapid expansion of the chemical, petrochemical, and manufacturing sectors that create substantial thermal management fluid demand.

India’s rapidly growing chemical and pharmaceutical manufacturing sector, Japan’s advanced industrial process technology adoption, and South Korea’s sophisticated petrochemical industry collectively sustain Asia Pacific’s dominant and fastest-growing regional trajectory. Government initiatives promoting energy-efficient technologies and increasing manufacturing capacity across the region contribute to rising adoption of synthetic and mineral oil-based heat transfer fluids.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Heat Transfer Fluids Market Insights

Saudi Arabia leads MEA revenues through its massive petrochemical and oil refining industry’s thermal management requirements, the growing renewable energy sector’s concentrated solar power investment under Vision 2030, and expanding industrial diversification creating new heat transfer fluid demand. The UAE’s growing manufacturing and energy sectors contribute secondary regional demand.

Brazil leads Latin American revenues through its large chemical and petrochemical processing sector, the growing food and beverage manufacturing industry’s thermal processing requirements, and expanding renewable energy infrastructure investment. Mexico’s oil and gas sector and growing manufacturing base contribute substantial secondary regional demand.

Market Dynamics

Growth Drivers: Energy efficiency demand across industrial sectors and renewable energy infrastructure expansion creating sustained heat transfer fluid procurement

The demand for heat transfer fluids is primarily driven by the need for energy efficiency and process optimization across industrial sectors. Industries are increasingly investing in advanced heat transfer systems to maintain stable temperatures, reduce energy consumption, and improve overall operational efficiency, with fluids offering higher thermal stability and better heat capacity allowing facilities to operate safely under extreme conditions. Growing chemical and petrochemical industries which drive market growth create proportional thermal fluid procurement as each new processing facility and capacity expansion requires comprehensive thermal management system fluid charging and ongoing replenishment.

Government initiatives promoting clean energy worldwide, where thermic fluids play a critical role in heat transfer processes such as concentrated solar power and geothermal systems, create substantial new fluid procurement independent of conventional industrial cycles. Each new solar thermal power plant and geothermal energy installation that requires specialized high-temperature fluid systems creates heat transfer fluid demand whose growth trajectory tracks the broader global renewable energy infrastructure investment cycle accelerating across both developed and emerging markets.

Restraints: Petroleum feedstock price volatility and thermal degradation disposal challenges constraining heat transfer fluid market economics

Heat transfer fluid production’s dependence on petroleum-derived feedstocks for mineral oil and certain synthetic fluid formulations creates manufacturing cost volatility that producers cannot fully hedge through long-term supply contracts, creating margin pressure when crude oil and refined product prices experience significant fluctuation. Each feedstock price spike that increases heat transfer fluid production costs creates pricing pressure that producers may struggle to pass through to customers in competitive commodity-grade fluid markets.

Thermal degradation of heat transfer fluids during extended high-temperature service creates disposal and environmental compliance challenges, as degraded fluids may require specialized hazardous waste handling and disposal procedures whose cost and regulatory complexity create operational burden for industrial facilities. Each fluid degradation event that triggers system-wide fluid replacement creates significant maintenance cost and downtime that industrial facility operators must factor into thermal fluid system total cost of ownership calculations.

Opportunities: Concentrated solar power expansion and bio-based fluid development creating premium heat transfer fluid market categories

Concentrated solar power’s continued global expansion, supported by government clean energy initiatives and falling renewable energy technology costs, creates substantial new high-temperature heat transfer fluid demand whose specialized performance requirements at sustained temperatures above 400 degrees Celsius create premium product opportunities for synthetic fluid manufacturers. Each new utility-scale CSP installation requires comprehensive fluid system charging whose volume and value substantially exceed conventional industrial heating fluid procurement on a per-installation basis.

Bio-based and renewable feedstock-derived heat transfer fluid development, responding to tightening environmental regulations and growing industrial sustainability commitments, creates a certified sustainable product category whose environmental credentials support customer ESG reporting requirements. Each industrial facility whose sustainability commitment specifies bio-based thermal fluid alternatives creates commercial opportunity for manufacturers investing in renewable feedstock fluid formulation research and development.

Recent Developments:

-

2024: Eastman Chemical Company expanded its Therminol heat transfer fluid product line with enhanced thermal stability formulations targeting concentrated solar power applications, supporting sustained operation at temperatures exceeding 400 degrees Celsius.

-

2024: Huntsman International launched a new synthetic heat transfer fluid grade with extended service life and enhanced oxidation resistance for high-temperature chemical processing applications, reducing fluid replacement frequency for industrial customers.

-

2023: Dow Inc. partnered with an oil and gas company to supply high-performance heat transfer fluids for a new offshore drilling project in the Gulf of Mexico, reflecting growing demand for thermic fluids in the oil and gas sector.

Heat Transfer Fluids Market Key Players are:

-

Eastman Chemical Company

-

The Dow Chemical Company

-

Huntsman International LLC

-

Shell PLC

-

BASF SE

-

Chevron Corporation

-

Exxon Mobil Corporation

-

BP International Limited

-

Indian Oil Corporation Ltd.

-

Hindustan Petroleum Corporation Limited

-

Dynalene Inc.

-

KOST USA Inc.

-

Delta Western Petroleum LLC

-

Solutia Inc. (Eastman Chemical)

-

PetroChina Company Limited

-

Reliance Industries Limited

-

Total Energies SE

-

Phillips 66 Company

-

Sinopec Corporation

-

Lubrizol Corporation

Heat Transfer Fluids Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.98 Billion |

| Market Size by 2035 | USD 8.51 Billion |

| CAGR | CAGR of 5.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Mineral Oils, Synthetic Fluids, Glycol-Based Fluids, Others) • By End-Use Industry (Chemical & Petrochemicals, Oil & Gas, Power Generation, Renewable Energy, Automotive, Pharmaceuticals, Food & Beverages, HVAC, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Eastman Chemical Company, The Dow Chemical Company, Huntsman International LLC, Shell PLC, BASF SE, Chevron Corporation, Exxon Mobil Corporation, BP International Limited, Indian Oil Corporation Ltd., Hindustan Petroleum Corporation Limited, Dynalene Inc., KOST USA Inc., Delta Western Petroleum LLC, Solutia Inc. (Eastman Chemical), PetroChina Company Limited, Reliance Industries Limited, TotalEnergies SE, Phillips 66 Company, Sinopec Corporation, and Lubrizol Corporation |

Frequently Asked Questions

The Heat Transfer Fluids Market is expected to grow at a CAGR of 5.51% from 2026 to 2035.

The Heat Transfer Fluids Market was valued at USD 4.98 Billion in 2025.

Energy efficiency and process optimization demand across industrial sectors, growing chemical and petrochemical industries, renewable energy infrastructure expansion including concentrated solar power, and increasing emphasis on sustainability are the primary growth factors.

The Mineral Oils segment dominated the Heat Transfer Fluids Market with the largest share through cost-effectiveness and wide availability.

Asia Pacific led the Heat Transfer Fluids Market with the highest revenue share in 2025.

Get in Touch