Functional Cosmetics Market Report Scope & Overview:

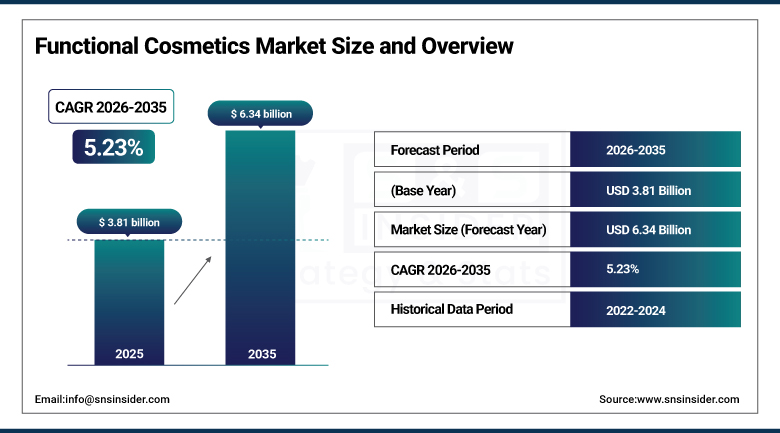

The Functional Cosmetics Market was valued at USD 3.81 Billion in 2025 and is expected to reach USD 6.34 Billion by 2035, growing at a CAGR of 5.23% from 2026–2035.

The market for functional cosmetics is on an accelerated path because there is demand for products which have a real and quantifiable effect on skin care, rather than only a cosmetic effect, with anti-aging, whitening, UV protection, being among the key characteristics behind product selection. Major companies are increasingly exploring biotech and AI in an attempt to provide customized skincare, as shown in the case of L’Oréal partnering with Tru Diagnostic and in its purchase of Dr.G. Ingredients, expanded e-commerce sales channels, and scientific substantiation continue to be the key factors pushing the functional skincare market forward, as shown in L'Oréal’s reported growth in like-for-like dermo-cosmetics consumption by 2.7% in one quarter.

In January 2024, Estee Lauder introduced its Skin Longevity platform, anchored by the Re-Nutriv Ultimate Diamond Transformative Brilliance Soft Crème featuring proprietary SIRTIVITY-LP technology, claimed to visibly reverse signs of aging within 14 days. The launch, supported by a partnership with the Stanford Center on Longevity, reflects a broader industry pivot from conventional anti-aging positioning toward biotech-driven longevity science across the functional cosmetics category.

Market Size and Forecast:

-

Market Size in 2026E: USD 4.01 Billion

-

Market Size by 2035: USD 6.34 Billion

-

CAGR: 5.23% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Functional Cosmetics Market - Request Free Sample Report

Functional Cosmetics Market Trends:

-

Biotech-driven ingredient innovation is accelerating the development of personalized functional cosmetics and advanced skincare solutions.

-

Clean-label and plant-based formulations are gaining popularity as consumers seek safer, transparent, and sustainable cosmetic products.

-

AI-powered skin diagnostics and digital beauty platforms are transforming consumer product selection and purchasing experiences.

-

Growing investment in peptide- and retinoid-based active ingredients is driving clinically proven anti-ageing and skincare innovations.

-

Expansion of omnichannel retail and e-commerce is increasing accessibility and sales of functional cosmetics worldwide.

U.S. Functional Cosmetics Market Outlook:

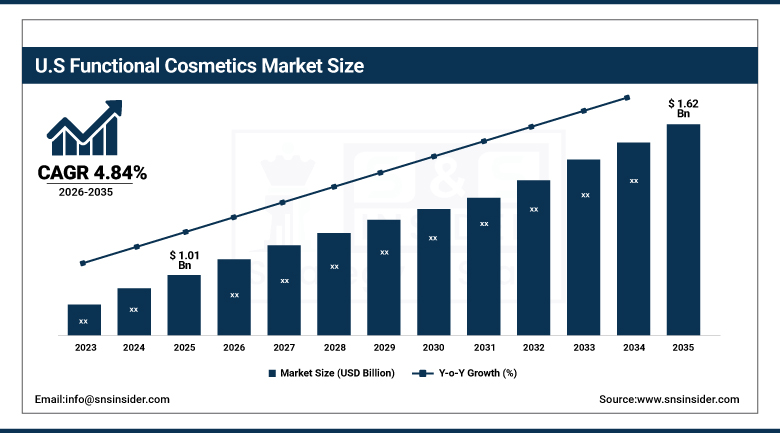

The U.S. functional cosmetics market was valued at approximately USD 1.01 Billion in 2025 and is expected to reach approximately USD 1.62 Billion by 2035, growing at a CAGR of approximately 4.84%.

According to the Personal Care Products Council, the U.S. cosmetics market ranks among the largest in the world, contributing USD 308.7 billion to U.S. GDP and supporting a workforce of over 4.6 million jobs, indicating considerable growth potential within the broader functional cosmetics category specifically. Functional cosmetics market trends in the U.S. continue mirroring developments in the broader functional cosmetic ingredients space, as brands concentrate development efforts on proven actives, retinoids and AHAs among them, to capture share through new launches built around demonstrated efficacy as a core positioning proposition.

In its fiscal 2025 second quarter results, the Estée Lauder Companies reported launching a disruptively priced anti-aging serum under its GF 15% Solution line in January 2025, alongside continued Re-Nutriv longevity platform expansion into eye care that same month. These launches reflect intensifying competition around accessibly priced, clinically substantiated anti-aging formulations across the U.S. functional cosmetics market.

Functional Cosmetics Market Segment Analysis:

-

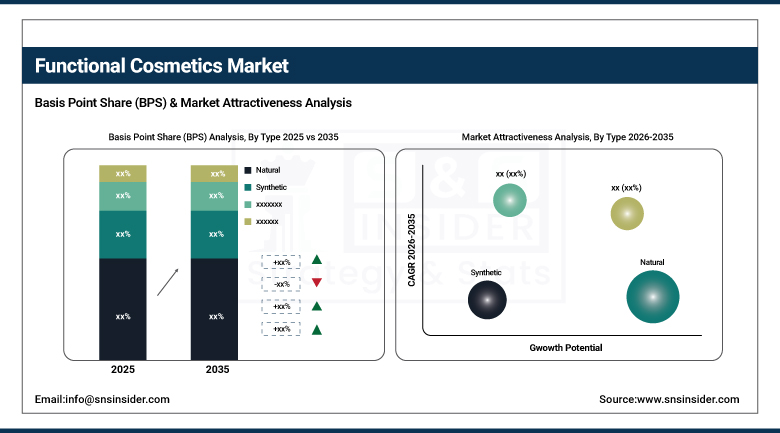

By Type, the natural segment dominated the functional cosmetics market with a 53.8% revenue share in 2025, while the synthetic segment is the fastest growing with a CAGR of 5.51%.

-

By Product Type, the alpha hydroxy acids segment dominated the functional cosmetics market with a 22.5% revenue share in 2025, while the retinoid segment is the fastest growing with a CAGR of 6.51%.

-

By Form, the cream & lotion segment dominated the functional cosmetics market with approximately 38.5% share in 2025, while the serums segment is the fastest growing with a CAGR of 6.86%.

-

By Functionality, the conditioning agents segment dominated the functional cosmetics market with a 31.4% revenue share in 2025, while the anti-ageing agents segment is the fastest growing, with a CAGR of 6.18%.

-

By Distribution Channel, the online segment dominated the functional cosmetics market with a 46.5% revenue share in 2025, while the offline segment is the fastest growing with a CAGR of 5.6%.

By Type, natural dominate, synthetic grow fastest

Ingredients that are natural are forecasted to dominate the functional cosmetic market with an estimated market share of 53.8% in 2025, largely due to the plant-based ingredients category, considering that there is an increased preference towards products that are eco-friendly and organic among consumers. The demand for natural cosmetics has been increasing because of their skin-friendly, environment-friendly, and user-friendly nature, an aspect that organizations such as the Natural Products Association promote.

The synthetic segment is witnessing the highest growth rate with CAGR being 5.51%. Peptides and retinoids have taken an important place in the above-mentioned segment because of their effectiveness and supportive scientific evidence. The demand for functional cosmetics with synthetic components continues to increase, which is proven by increased investments in R&D in the development of these combinations by leading companies such as L'Oreal and Estee Lauder.

By Product Type, alpha hydroxy acids dominate, retinoid grows fastest

Alpha Hydroxy Acids held the market share of 22.5% in 2025 due to their reputation for being effective skin exfoliants. This product remains popular because of its ability to treat several skin problems, such as acne, pigmentation, and wrinkles. It is important to note that Alpha Hydroxy Acids have proven their efficiency in practice, as well as through certification from dermatological organizations, such as the American Academy of Dermatology.

Retinoid is the segment witnessing the fastest growth and highest CAGR of 6.51%, since the number of instances where retinoids are used in functional products because of the scientifically validated anti-wrinkle and fine line property keeps increasing. Leading companies like Johnson & Johnson and Procter & Gamble have continued to capitalize on the growing popularity of retinoids by launching products, while the endorsement of retinoids from more dermatologists owing to their scientifically validated skin benefits has further increased the rate of expansion in the market.

By Form, cream and lotion dominates, serums grow fastest

Creams and lotions accounted for the largest market share of 38.5% in 2025 in the functional cosmetics industry, where the moisturizing cream segment holds immense popularity due to its multi-beneficial nature that ranges from moisturization to repairing the skin barrier and even acting as an anti-aging product. Easy application and availability of the products in both premium as well as drugstore products have ensured that creams remain the first choice of consumers, who include companies such as Neutrogena and Olay among others.

The growth in serums is fastest in terms of value and CAGR is estimated at 6.86%. This is especially true for serums containing vitamin C and hyaluronic acid as they have proven themselves to be the best in targeting particular problems due to quick absorption properties. Serums are increasingly replacing the use of creams for solving specific skin-related problems because of their efficacy.

By Distribution Channel, online dominates, offline grows fastest

The online channel dominated the functional cosmetics market in 2025, with a 46.5% share, driven substantially by the brand websites subsegment as customers increasingly turn to convenient online shopping. E-commerce players such as Amazon and beauty specific online stores have been driving this trend, where product diversity, recommendation engines and discounts have all played an important role in keeping online retail as a relevant player in this category.

Offline retail is the fastest growing route-to-market with a compound annual growth rate (CAGR) of 5.6%. Department stores form the key growth engine for the offline channel due to consumer preference for tactile product testing. Increased focus on luxurious retail experience is also driving offline channel growth, with physical retail players increasingly able to win over consumers through personalized consultation and beauty services.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

78.0% |

|

Europe |

Germany |

25.0% |

|

Asia Pacific |

China |

38.0% |

|

Latin America |

Brazil |

36.0% |

|

Middle East & Africa |

UAE |

27.0% |

North America Functional Cosmetics Market Insights

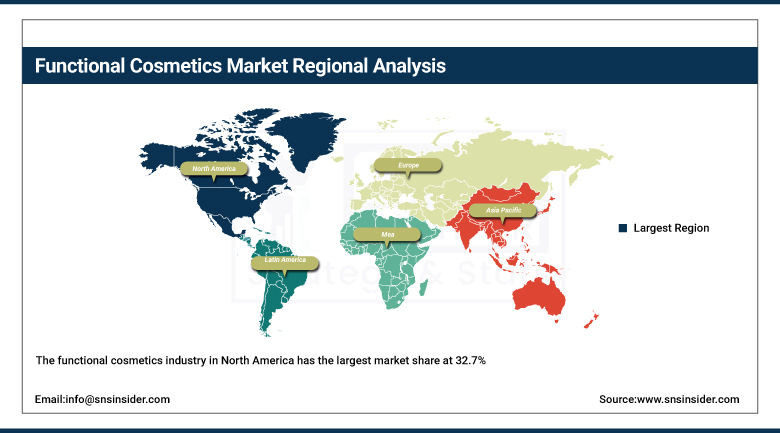

The functional cosmetics industry in North America has the largest market share at 32.7%, primarily due to the rising consumer inclination towards eco-friendly and natural personal care products, along with high-end skin care products. In addition to this, the US is the largest country in the North American market and accounts for 40% of the total revenue of Galderma.

A rise in treatments addressing so-called Ozempic face and growing demand for anti-aging products among an aging population have both bolstered regional market growth. Canada is also a significant contributor, where 54% of Canadians say product quality is their standard for purchase, a preference that continues to drive growth in premium, functional skincare products across the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Functional Cosmetics Market Insights

Europe ranks second in terms of the functional cosmetics market share at 28.9% in 2025 because of the increased need for natural beauty products and multi-functional cosmetic solutions. Germany and France account for the largest regional market shares, while the customers are interested in products that have both relaxing and beauty properties.

The trend related to health has significantly affected the market of this region, as the products combining beauty and health aspects have become particularly popular. Continued focus on natural ingredients and eco-friendly packaging across the region continues to reinforce market growth, positioning Europe as a technically sophisticated, sustainability-focused market relative to other global regions.

Asia Pacific Functional Cosmetics Market Insights

Asia Pacific is the fastest-growing market for functional cosmetics, expanding at a CAGR of 6.06%. This growth is powered by rising demand for skincare products offering genuine health benefits, including sun protection and anti-aging properties, across the region's largest economies.

In terms of Asia-Pacific countries, China, South Korea, and Japan dominate. The trend of K-beauty and J-beauty influences the region and drives new innovative ingredients like snail mucin, cica, and hyaluronic acid. The rapid expansion of e-commerce in the region has also helped boost the development of the market. It is expected that the Asia-Pacific region will determine the direction of future developments in this segment.

MEA & Latin America Functional Cosmetics Market Insights

The Middle East and Africa are experiencing steady growth in functional cosmetics adoption, driven by expanding personal care manufacturing and growing consumer interest in premium skincare across the UAE and Saudi Arabia. South Africa contributes meaningfully as well, supported by its more established consumer goods sector.

Latin America is seeing gradual growth led by Brazil, where consumers are increasingly incorporating functional skincare into daily routines alongside continued demand for natural, botanically derived formulations. Argentina follows as a smaller but growing contributor, and both regions remain more price-sensitive than North America, Europe, or Asia Pacific, keeping accessible product tiers the more common choice across broader consumer segments.

Market Dynamics:

Growth Drivers: Plant-based ingredient demand fuels cosmetics innovation

Rising demand for clean-label and plant-based actives among end users represents one of the primary growth drivers within the functional cosmetics market. With growing demand for safe and sustainable ingredients, leading functional cosmetics firms are reformulating with botanical extracts including green tea polyphenols and niacinamide. In a study conducted by the Personal Care Products Council in 2023, it was revealed that 63% of consumers in the United States consider natural ingredients in their selection process when purchasing skin care products.

The market of functional cosmetic ingredients is growing since formulators use more often bio-based substances in order to be more transparent and traceable. It helps not only increase the size of the whole market for functional cosmetics but also expand the market share of brands that demonstrate efficacy with the help of scientific evidence.

Restraints: Consumer skepticism limits adoption of novel products

Consumer confidence remains a key limiting factor even as science-based preparations continue to advance. Research conducted in 2024 by Consumer Federation of America has shown that 48% of the customers doubt claims that are written on the packaging of the cosmetics and especially in case these claims concern new actives such as peptides and growth factors. This trend is driving the need for independent validation and clinical trials.

The current trends increase the expenses of promotion by approximately 8% for each launch of the product, based on the available information. Companies may lose their competitive advantage if they fail to prove that the claims about ingredients are justified with the help of peer-reviewed researches.

Opportunities: Biotech partnerships unlock substantial growth potential

Continued integration of biotechnology and artificial intelligence into functional cosmetics development represents a substantial growth opportunity for manufacturers positioned to lead this convergence. L'Oréal's partnership with Tru Diagnostic and its acquisition of Dr.G illustrate how established beauty companies are increasingly acquiring or partnering with specialized capability to deliver genuinely personalized skincare solutions rather than one-size-fits-all formulations.

As AI-based skin diagnostics and interactive virtual try-on tools continue improving conversion rates, reportedly by as much as 25% according to recent industry reporting, companies investing in digital personalization infrastructure stand to capture disproportionate growth within an increasingly competitive functional cosmetics landscape. Niche brands in particular are using these digital tools to build functional cosmetics market share without the constraints of traditional brick-and-mortar distribution networks.

Recent Developments:

-

2024: In January 2024, Estee Lauder introduced its Skin Longevity platform, anchored by the Re-Nutriv Ultimate Diamond Transformative Brilliance Soft Crème featuring proprietary SIRTIVITY-LP technology, in partnership with the Stanford Center on Longevity.

-

2024: In October 2024, the Philippines FDA revised the ASEAN Cosmetic Directive, updating ingredient lists to align with global standards and improve product safety compliance.

-

2025: In January 2025, the FDA advanced its F-Pop initiative, easing regulations to empower local functional cosmetics manufacturers and promote exports with reduced compliance costs.

Functional Cosmetics Market key players are:

-

L'Oreal S.A.

-

The Estee Lauder Companies Inc.

-

Procter & Gamble Co.

-

Unilever PLC

-

Shiseido Company, Limited

-

Beiersdorf AG

-

Kenvue Inc.

-

Amorepacific Corporation

-

Kao Corporation

-

Colgate-Palmolive Company

-

Coty Inc.

-

Galderma Group AG

-

LG Household & Health Care

-

Revlon, Inc.

-

Natura &Co Holding S.A.

-

Pierre Fabre Dermo-Cosmétique

-

NAOS Group

-

LVMH

-

Mary Kay Inc.

-

Oriflame Holding AG

Functional Cosmetics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.81 Billion |

| Market Size by 2035 | USD 6.34 Billion |

| CAGR | CAGR of 5.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Natural, Synthetic) • By Product Type (Alpha Hydroxy Acids, Polyhydroxy Acids, Beta Hydroxy Acid, Hydroquinone, Kojic Acid, Retinoid, L-Ascorbic Acid, Others) • By Form (Cream & Lotion, Gel, Mask, Powders, Serums) • By Functionality (Conditioning Agents, UV Filters, Anti-Ageing Agents, Skin-Lightening Agents, Others) • By Distribution Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | L'Oreal S.A., The Estee Lauder Companies Inc., Procter & Gamble Co., Unilever PLC, Shiseido Company, Limited, Beiersdorf AG, Kenvue Inc., Amorepacific Corporation, Kao Corporation, Colgate-Palmolive Company, Coty Inc., Galderma Group AG, LG Household & Health Care, Revlon, Inc., Natura &Co Holding S.A., Pierre Fabre Dermo-Cosmétique, NAOS Group, LVMH, Mary Kay Inc., Oriflame Holding AG |

Frequently Asked Questions

The Functional Cosmetics Market is expected to grow at a CAGR of 5.23% from 2026 to 2035.

The Functional Cosmetics Market was valued at USD 3.81 Billion in 2025.

Natural ingredients lead the Functional Cosmetics Market with a 53.8% share in 2025.

In the Functional Cosmetics Market, 48% of consumers distrust efficacy claims, demanding third-party validation and clinical evidence for product performance.

North America leads the Functional Cosmetics Market with a 32.7% share.

Get in Touch