LNG Bunkering Market Report Scope & Overview:

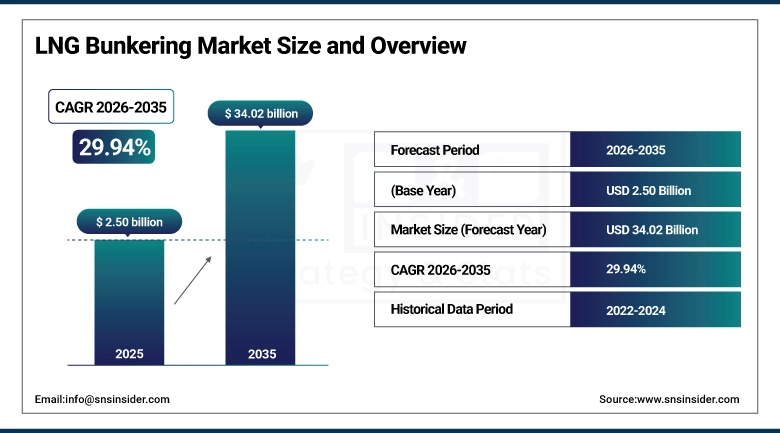

The LNG Bunkering Market was valued at USD 2.50 billion in 2025 and is expected to reach USD 34.02 billion by 2035, growing at a CAGR of 29.94% from 2026-2035.

LNG Bunkering Market growth is fueled by the rising trend across the globe towards the reduction of emissions from marine transportation and the shift towards sustainable fuel sources. Strict environmental regulations have compelled shipping companies to switch to LNG as a green energy source that replaces traditional sources of energy. The rapid development of the LNG-fueled vessel fleet and the growth of infrastructure for the bunkering process will further propel market growth.

According to research, global demand for LNG as a marine fuel is expected to at least double by 2030, driven by emissions regulations and fuel supply expansion. LNG bunkering volumes could exceed 4 million tonnes by 2025 and reach around 15 million tonnes by 2030. The same report notes the number of dual‑fuel ships using LNG is projected to rise from about 781 today to over 1,400 by 2030, with global bunkering hubs led by Singapore, China, and the Netherlands.

Furthermore, according to the International Energy Agency (IEA), international shipping accounts for about 2–3 % of global CO₂ emissions, underscoring the sector’s importance in global decarbonization efforts and the relevance of cleaner fuels like LNG to meet regulatory targets.

LNG Bunkering Market Size and Growth Forecast

-

LNG Bunkering Market Size in 2025: USD 2.50 Billion

-

LNG Bunkering Market Size by 2035: USD 34.02 Billion

-

CAGR: 29.94% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on LNG Bunkering Market - Request Free Sample Report

LNG Bunkering Market Trends

-

Rising adoption of LNG as a cleaner marine fuel is driving the LNG bunkering market.

-

Growing demand from shipping companies to comply with IMO sulfur emission limits is boosting market growth.

-

Expansion of LNG-powered vessels and retrofitting of existing ships is fueling deployment.

-

Increasing focus on safe, efficient, and flexible bunkering solutions is shaping adoption trends.

-

Advancements in LNG storage, transfer technologies, and port infrastructure are enhancing operational efficiency.

-

Rising government incentives and environmental regulations promoting low-emission fuels are supporting market expansion.

-

Collaborations between LNG suppliers, shipping operators, and port authorities are accelerating innovation and global adoption.

U.S. LNG Bunkering Market Size Outlook:

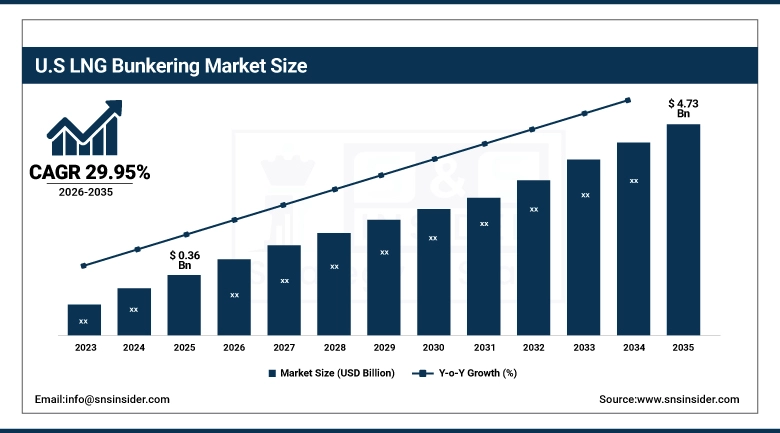

The U.S. LNG Bunkering Market was valued at USD 0.36 billion in 2025 and is expected to reach USD 4.73 billion by 2035, growing at a CAGR of 29.95% from 2026-2035. The factors that are responsible for the growth of U.S. LNG Bunkering Market include abundance of natural gas sources, expansion of infrastructure facilities associated with export and bunkering of liquefied natural gas, and emission regulations favoring utilization of eco-friendly marine fuel types.

On February 28, 2025, the U.S. Department of Energy (DOE) issued an order to remove regulatory barriers for the use of liquefied natural gas (LNG) as marine fuel, clarifying that ship‑to‑ship LNG transfers for bunkering at U.S. ports, U.S. waters, or international waters are no longer considered LNG “exports” under the Natural Gas Act. This change significantly reduces regulatory burdens and supports expanded bunkering operations at coastal facilities like JAX LNG.

The DOE noted that LNG use as a marine fuel has been rising, with the International Energy Agency (IEA) estimating LNG‑fueled vessels could nearly double above 1,200 by 2028 due to more stringent emissions standards.

In March 2026, U.S. LNG exports hit a record high of 11.7 million metric tons, reflecting strong natural gas production and export infrastructure growth that also underpins growing domestic LNG availability for bunkering

LNG Bunkering Market Growth Drivers:

-

Stringent emission regulations and global maritime decarbonization targets accelerating adoption of cleaner LNG fuel alternatives across shipping industry worldwide

The implementation of rigorous environment laws that have been introduced worldwide by international bodies overseeing the maritime industry has played a major role in fostering LNG use as a maritime fuel. Measures introduced in attempts to cut down the emission of sulfur oxide, nitrogen oxide, and carbon dioxide have compelled shipping firms to adopt new fuels to curb pollution. LNG has proven efficient at cutting down emissions, making it the fuel of choice for such purposes. Rising pressures from governments and environmental activists have been contributing to this trend. Also, the awareness of fleet owners regarding sustainability and economic viability has contributed.

Regulatory and Emission Drivers Boosting LNG Adoption

|

Initiative |

Details / Impact |

|

Expansion of Emission Control Areas (ECAs) |

From 1 March 2026, the Canadian Arctic and the Norwegian Sea became designated ECAs under IMO MARPOL Annex VI, enforcing stricter limits on NOx, SOx, and particulate emissions. Within these ECAs, the sulphur content of fuel used by ships must not exceed 0.10 %, encouraging adoption of low‑emission fuels like LNG. |

|

IMO GHG Strategy and Net‑Zero Targets |

In July 2023, IMO members adopted an enhanced strategy to significantly reduce greenhouse gas emissions from shipping, aiming for net‑zero GHG by around 2050 with intermediate checkpoints by 2030 and 2040. Measures like EEXI and CII push shipowners toward cleaner fuels to improve energy efficiency ratings and long-term compliance. |

|

Verified Emission Reduction Benefits of LNG |

Studies highlighted by SEA‑LNG and the World Ports Organization show LNG can reduce GHG emissions by up to 23 % compared with conventional oil-based fuels (well-to-wake basis), depending on engine/technology. LNG emits virtually no SOx and can cut NOx emissions by up to 95 %, helping vessels meet IMO and ECA standards. |

LNG Bunkering Market Restraints:

-

High initial investment requirements for LNG bunkering infrastructure and specialized vessels limiting adoption among small and medium shipping operators globally

The cost factor associated with developing LNG bunker infrastructure and upgrading existing shipping fleets presents another major impediment towards the growth of the market. Investment in terms of money is needed for creating LNG facilities, including LNG terminals, bunkering stations, and LNG-fueled bunker ships. Also, the use of liquefied natural gas in ships necessitates special engine technologies and cryogenic tanks, which further increases the cost. In addition to that, small and medium shipping firms have budgetary limitations and cannot afford these costly initiatives. Furthermore, the long break-even period acts as a deterrent for making any such investments.

A major LNG bunkering terminal, such as the Tacoma LNG facility, with the capacity to produce up to ~500,000 gallons/day and store ~8 million gallons of LNG, was estimated to cost about USD 310 million in construction, highlighting the significant financial commitment required to support large-scale LNG bunkering operations.

LNG Bunkering Market Opportunities:

-

Growing adoption of bio-LNG and synthetic LNG fuels supporting transition toward sustainable and carbon-neutral maritime fuel solutions worldwide

An increasing trend towards sustainability has brought up various opportunities through the use of bio-LNG and synthetic LNG fuels. Bio-LNG and synthetic LNG fuels have a substantial reduction in carbon emissions than conventional LNG fuel and thus comply with international policies aimed at reducing carbon emissions. Shipping companies are taking advantage of these two fuels in an attempt to meet their carbon-neutral objectives and improve environmental performance. There is also governmental support in the form of policies that favor the use of renewable LNG fuel.

In 2025, major Japanese shipping company NYK Line began continuous bio‑LNG bunkering operations for LNG‑powered vessels at the Port of Zeebrugge, using carbon‑neutral bio‑LNG certified on a well‑to‑wake basis. This marks a practical fleet deployment of renewable LNG in commercial shipping.

Additionally, energy major Shell has agreed to supply bio‑LNG to global carrier Hapag‑Lloyd (using ISCC EU‑certified bio‑LNG), underlining a broader industry shift toward renewable LNG fuels beyond pilot projects a positive development for scaling bio‑LNG in liner shipping. This transition toward greener LNG variants is expected to create new growth avenues and strengthen the long-term outlook of the LNG bunkering market.

LNG Bunkering Market Segment Highlights

-

By Product Type, Truck-to-Ship dominated the LNG Bunkering Market with ~41% share in 2025; Ship-to-Ship fastest growing (CAGR).

-

By End-User, Shipping & Maritime Transport dominated the LNG Bunkering Market with ~51% share in 2025; Offshore Oil & Gas fastest growing (CAGR).

-

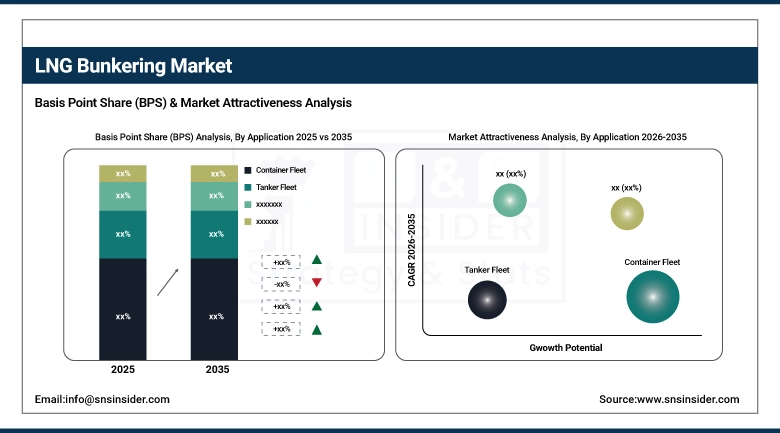

By Application, Container Fleet dominated the LNG Bunkering Market with ~36% share in 2025; Ferries fastest growing (CAGR).

By Application, Container Fleet segment dominates the LNG Bunkering Market, Ferries segment expected to grow fastest

The Container Fleet segment held the largest share in terms of revenue in the LNG Bunkering Market in 2025 because of the huge amount of fuel consumed by container vessels, which will soon switch to cleaner fuels. The increased movement in international trade along with the expansion in shipping lines will increase the use of LNG fuel in vessels.

The Ferries segment is predicted to witness the highest CAGR during the forecast period of 2026-2035 owing to stringent environmental laws in coastal areas and an increasing preference for clean transportation. There is encouragement from governments in adopting LNG fuel in ferry services. This is because ferries have short distances to travel and operate frequently.

By Product Type, Truck-to-Ship segment dominates the LNG Bunkering Market, Ship-to-Ship segment expected to grow fastest

The Truck-to-Ship segment captured the largest market share in terms of revenue in the LNG Bunkering Market in 2025, owing to its ability to provide flexible operation, reduced costs, and negligible infrastructure required for the process. With truck-to-ship bunkering, delivery of LNG is made possible through mobile tanks. This approach facilitates an earlier entry of LNG into the market while offering fast and easy deployment.

The Ship to Ship segment is projected to register the highest growth rate during the forecast period owing to the rising number of LNG bunker ships that are used for large-volume operations in the marine transportation industry. The ship to ship bunkering technique helps in increasing the rate of transfer, and is also suitable for large volume vessels in the long route.

By End-User, Shipping & Maritime Transport segment dominates the LNG Bunkering Market, Offshore Oil & Gas segment expected to grow fastest

The Shipping & Maritime Transport category held the largest market revenue share in 2025 owing to the growth in international maritime freight and the rising adoption of ships running on LNG fuel. Shipping firms are concentrating on reducing emissions and meeting the norms regarding the environment. A significant contribution of large fleet segments such as containerships, bulkers, and tankers contributes immensely to LNG consumption.

The Offshore Oil & Gas segment is projected to have the fastest-growing CAGR from 2026-2035 owing to the growing adoption of LNG-powered offshore support vessels as well as stringent emission policies in offshore operations. The increase in offshore activities is leading to clean fuel use. Operational efficiency and less pollution make LNG a preferred choice for offshore energy organizations globally.

LNG Bunkering Market Regional Analysis

Europe LNG Bunkering Market Insights

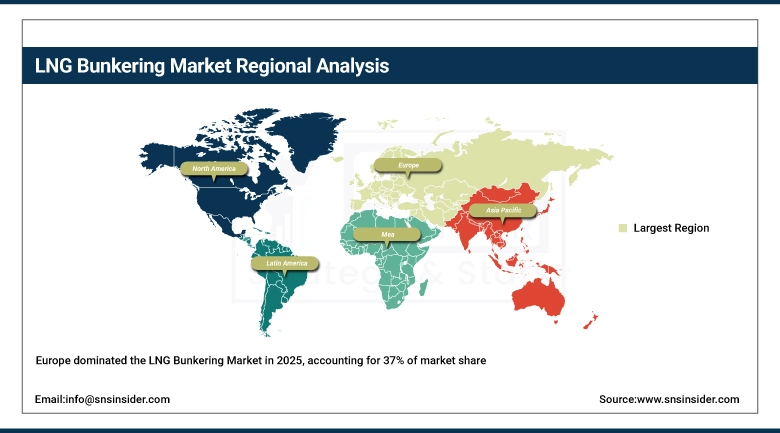

Europe held a major share of approximately 37% in the revenue for the LNG Bunkering Market in 2025 because of established LNG infrastructure, favorable regulatory environment, and early implementation of clean fuel for ships. The strict emission regulations according to the maritime policies in the region have led to faster adoption of LNG technology. In addition, the existence of prominent bunkering hubs like Rotterdam along with significant investments by energy organizations has contributed to market expansion.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific LNG Bunkering Market Insights

The Asia Pacific region is forecasted to have the highest growth rate at a compound annual growth rate (CAGR) of approximately 31.66% from 2026 to 2035 owing to the fast-growing nature of maritime business and investments being made in the infrastructure of liquefied natural gas (LNG). Nations like China, Japan, and South Korea are promoting the usage of LNG as an environmentally friendly fuel in marine vessels. Increased construction of ships and the number of LNG-fueled ships are other contributing factors to the rising demand for LNG bunkers.

North America LNG Bunkering Market Insights

North America occupies a substantial place in the LNG Bunkering Market as a result of the growing popularity of LNG as a marine fuel and investments made in bunkering facilities. The availability of large sources of natural gas along with LNG export facilities in North America favors the supply of fuel. Regulations concerning emissions, coupled with increasing concern over the environmental impact of maritime activities, have motivated ship operators to opt for LNG.

Middle East & Africa and Latin America LNG Bunkering Market Insights

The Middle East & Africa and Latin America segments represent the new areas of growth for the LNG Bunkering Market due to increased investment in the construction of ports and an emphasis on cleaner fuels for shipping vessels. While the Middle East enjoys access to substantial reserves of natural gas along with growing capacity to export LNG, Latin America is steadily building up its capabilities to act as a bunkering location for ships. Increased shipping activity and government policies have led to the adoption of LNG fuel.

LNG Bunkering Market Competitive Landscape:

TotalEnergies SE

TotalEnergies SE is a multinational company based out of Paris, France, that specializes in energy in multiple forms such as oil, gas, renewable energy, and low-carbon fuel solutions. It is one of the key players in LNG, which includes production, trading, and marine bunkering, thus contributing towards clean energy solutions for the shipping industry. TotalEnergies' Marine Fuels business creates LNG solutions for ships to use both LNG and fossil fuels as bunker fuel options.

-

2026: TotalEnergies and CMA CGM formed a 50/50 LNG bunkering joint venture in Rotterdam, planning a 20,000 m³ bunker vessel deployment by 2028.

-

2025: TotalEnergies and CMA CGM launched LNG bunkering logistics across ARA ports, supporting dual-fuel vessels with dedicated on-demand supply systems.

-

2024: TotalEnergies Marine Fuels signed a charter for an 18,600 m³ LNG bunker vessel to expand supply infrastructure across Europe and the Middle East.

-

2023: TotalEnergies completed LNG bunkering operations for dual-fuel VLCCs using the Gas Agility vessel, supporting large-scale maritime decarbonization.

Gasum Oy

Gasum Oy, based in Espoo, Finland, is a Nordic energy company that deals mainly in natural gas, liquefied natural gas (LNG), and biogas products. The company is one of the leading suppliers of LNG bunkering in Northern Europe, with a bunker fleet used in the delivery of fuel to ships. Gasum offers its customers the opportunity to make their shipping operations cleaner by using LNG and bio-LNG in a reliable manner.

-

2025: Gasum’s Coralius LNG bunker vessel completed its 1,000th bunkering operation in Kiel, demonstrating operational reliability for dual-fuel vessel supply.

-

2024: Gasum and Equinor extended a long-term LNG bunkering agreement utilizing Coralius, Kairos, and Coral Energy vessels for dual-fuel shipping.

-

2022: Gasum bunkered the first LNG-fueled cruise vessel built by Chantiers de l’Atlantique using Kairos, marking a milestone in cruise LNG adoption.

Shell plc

Shell plc is an international energy business operating out of its headquarters located in London, United Kingdom. Shell is among the largest energy players in the globe dealing with oil, gas, LNG, and renewable energy. Shell is a major provider of marine fuels and has been at the forefront in the provision of LNG bunkering services._shell is interested in increasing the availability of LNG fuels, promoting dual-fuel ship use, and decarbonizing the maritime industry.

-

2023: Shell signed a multi-year LNG supply and bunkering agreement with CMA CGM/FueLNG, expanding LNG bunker vessel capacity in Singapore.

-

2022: Shell and CMA CGM expanded LNG bunkering collaboration, enhancing FueLNG Bellina readiness for dual-fuel ship fueling in Singapore.

LNG Bunkering Companies are:

-

Shell plc

-

Gasum Oy

-

ENGIE SA

-

Peninsula Petroleum

-

ENN Energy Holdings Ltd

-

Korea Gas Corporation (KOGAS)

-

Harvey Gulf International Marine

-

Naturgy Energy Group SA

-

Crowley Maritime Corporation

-

CMA CGM SA

-

Mitsui O.S.K. Lines (MOL)

-

NYK Line

-

QatarEnergy / Q‑LNG

-

ExxonMobil Marine Fuels

-

Petronas Marine

-

Bunker Holding A/S

-

Fjord Line AS

-

Titan LNG BV

-

Polskie LNG S.A.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.50 Billion |

| Market Size by 2035 | USD 34.02 Billion |

| CAGR | CAGR of 29.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Container Fleet, Tanker Fleet, Cargo Fleet, Ferries, Inland Vessels, Others) • By Product Type (Truck-to-Ship, Port-to-Ship, Ship-to-Ship, Portable Tanks) • By End-User (Shipping & Maritime Transport, Offshore Oil & Gas, Ferries & Passenger Transport, Port & Logistics Operators) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Shell plc, TotalEnergies SE, Gasum Oy, ENGIE SA, Peninsula Petroleum, ENN Energy Holdings Ltd, Korea Gas Corporation (KOGAS), Harvey Gulf International Marine, Naturgy Energy Group SA, Crowley Maritime Corporation, CMA CGM SA, Mitsui O.S.K. Lines (MOL), NYK Line, QatarEnergy / Q‑LNG, ExxonMobil Marine Fuels, Petronas Marine, Bunker Holding A/S, Fjord Line AS, Titan LNG BV, Polskie LNG S.A. |

Frequently Asked Questions

Europe dominated the LNG Bunkering Market in 2025.

The Truck-to-Ship segment dominated the LNG Bunkering Market in 2025.

Stringent emission regulations and global maritime decarbonization targets accelerating adoption of cleaner LNG fuel alternatives across shipping industry worldwide.

The LNG Bunkering Market was valued at USD 2.50 billion in 2025.

The LNG Bunkering Market is expected to grow at a CAGR of 29.94% from 2026 to 2035.

Get in Touch