Ozempic Market Report Scope & Overview:

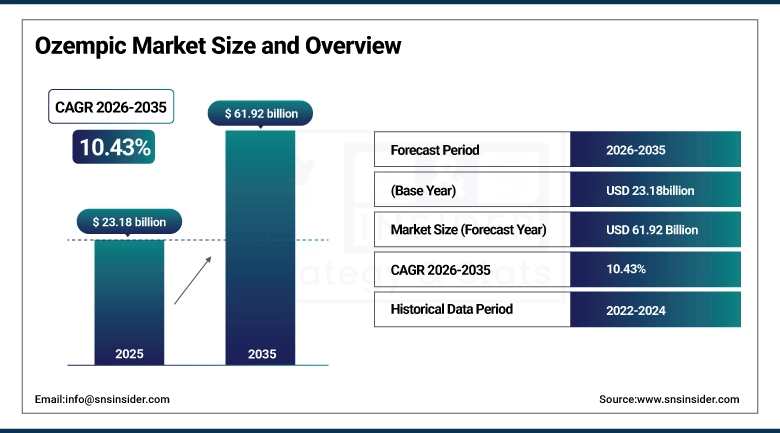

The Ozempic Market size is valued at USD 23.18 Billion in 2025 and is projected to reach USD 61.92 Billion by 2035, growing at a CAGR of 10.43% during the forecast period 2026–2035.

Ozempic Market Insights report gives an insightful analysis of market trends, drug developments, and therapeutics. Growth in the prevalence of type 2 diabetes and obesity, rising uptake of GLP 1 receptor agonist therapies for weight loss, rising adoption of oral and injectable formats, and favorable reimbursement policies will propel significant growth in the market during 2026–2035.

More than 25 million prescriptions have been recorded from the utilization of Ozempic in 2025 due to the rise in diabetes incidence rate and obesity treatment demand.

Market Size and Forecast:

-

Market Size in 2025: USD 23.18 Billion

-

Market Size by 2035: USD 61.92 Billion

-

CAGR: 10.43% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Ozempic Market - Request Free Sample Report

Ozempic Market Trends:

-

The growing burden of type 2 diabetes and obesity increases demand for GLP 1 medicines.

-

The weight loss management therapy becomes the fastest growing application segment.

-

Oral dosage forms (Rybelsus) become popular among users as they prefer non-injectable routes.

-

The cardioprotective benefits become an important indication for Ozempic utilization.

-

E-commerce becomes the leading route in the sales channels.

-

Convenient payment policies and insurance coverage become key contributors to adoption.

-

Supply chain disruption and scalability issues become the major concerns.

-

Major competition from Eli Lilly’s Mounjaro and other GLP 1 drug comes into the picture.

-

The rising awareness about lifestyle diseases becomes an important factor behind adoption.

U.S. Ozempic Market Insights:

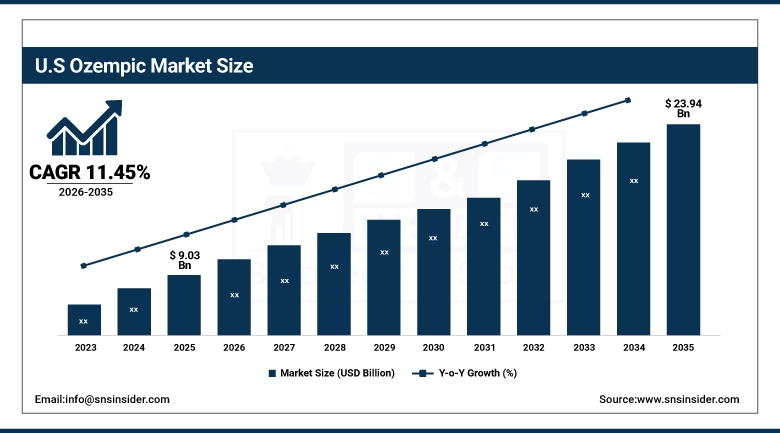

The U.S. Ozempic Market is projected to grow from USD 9.03 Billion in 2025 to USD 23.94 Billion by 2035, at a CAGR of 11.45%. Ozempic’s growth will be propelled by increasing incidences of type 2 diabetes and obesity, an increase in the use of GLP 1 agonists for weight loss, indications that have extended into cardiovascular risks, and the increasing demand for new formulations of the drug, including its oral form, and its injectable forms.

Ozempic Market Growth Drivers:

-

Rising prevalence of type 2 diabetes and obesity is driving demand for advanced GLP‑1 therapies.

Widening the use of Ozempic in hospitals, specialist clinics, and retail drugstores points to its involvement in glucose regulation, body weight control, and prevention of cardiovascular risks. With advancements in terms of oral administration, injectable delivery, and extended-release options, along with increased safety and efficacy, together with high compliance levels, more users of Ozempic are being reported.

Over 52% of hospitals, specialty clinics, and retail pharmacies have used Ozempic in 2025 for the management of diabetes and obesity conditions.

Ozempic Market Restraints:

-

High treatment costs, limited reimbursement in certain regions, and ongoing supply shortages are key restraints for the Ozempic Market.

The pharmaceutical companies that distribute their products and the clinical service providers that offer them may be faced with the challenge of satisfying increasing demands due to limitations in terms of production capabilities and prices. The competition among other GLP 1 product including the one developed by Eli Lilly, also known as Mounjaro, and the scrutiny by the regulatory authorities on its off-label usage for weight management could hinder its ability to grow.

In 2025, more than 42% of healthcare service providers had encountered problems in obtaining the drug consistently.

Ozempic Market Opportunities:

-

Growing development of advanced GLP‑1 receptor agonists and personalized metabolic therapies presents significant opportunities for the Ozempic Market.

The care delivery points within the healthcare system are becoming more dependent on Ozempic in the management of diabetes, obesity, and cardiovascular diseases. The pharmaceutical firms that develop new and safer drug forms for use through oral, injection, and extended-release routes may benefit from this development. Drug delivery systems continue to evolve, thus increasing the effectiveness, adherence, and coverage.

More than 47% of healthcare professionals began utilizing targeted Ozempic treatments in 2025 due to the increase in cases of diabetes and need for weight management.

Ozempic Market Segmentation Analysis:

-

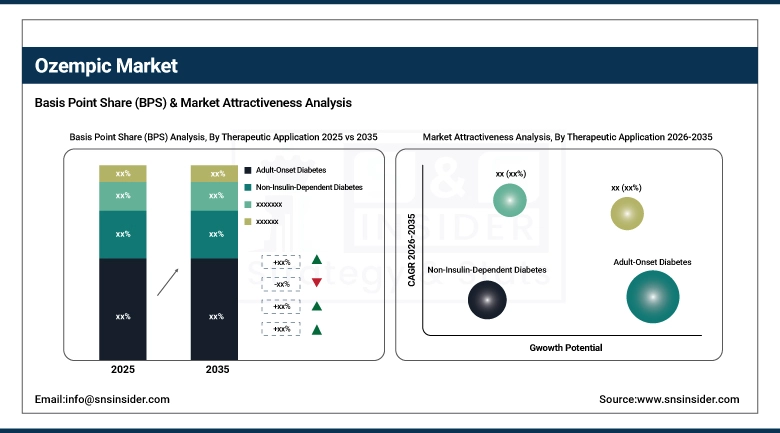

By Therapeutic Application, Adult-Onset Diabetes held the largest market share of 56.32% in 2025, while Non-Insulin-Dependent Diabetes are expected to grow at the fastest CAGR of 11.34% during 2026–2035.

-

By Drug Formulation / Delivery, Injectable (Ozempic Pen) dominated with 69.87% market share in 2025, whereas Extended-Release Formulations are projected to record the fastest CAGR of 13.80% through 2026–2035.

-

By Sales Channel, Direct Sales (to hospitals/clinics) accounted for the highest market share of 34.67% in 2025, while Online Platforms are expected to grow at the fastest CAGR of 11.74% during the forecast period.

-

By Distribution Channel, Hospital Pharmacies dominated with a 39.16% share in 2025, while Online Pharmacies are anticipated to expand at the fastest CAGR of 11.89% through 2026–2035.

By Therapeutic Application, Adult-Onset Diabetes Dominates While Non‑Insulin‑Dependent Diabetes Grows Rapidly:

Adult-Onset Diabetes continues to be the dominant area of use based on its high prevalence and existing clinical acceptance among various health care providers. The excellent efficiency of the treatment in managing glucose levels ensures that Ozempic continues to hold the position as the most popular therapy option in this category.

Non-Insulin Dependent Diabetes appears to be the fastest growing use category. This can be attributed to increased awareness levels, early diagnoses, and expanded criteria for treatment. Rising preference for GLP‑1 therapies as effective alternatives to insulin further accelerates adoption, improving patient outcomes and adherence.

By Drug Formulation / Delivery, Injectable (Ozempic Pen) Dominates While Extended‑Release Formulations Grow Rapidly:

The injectable dosage forms, especially the Ozempic Pen, remain dominant segment owing to their effectiveness, easy-to-use nature, and high medical practitioner preference in treating diabetes and obesity. Their extensive use in clinics and patients' familiarity have made them the dominant players in this space.

The Extended-Release Dosage Forms are becoming the fastest growing group thanks to the continuous improvement in the drug delivery system, enhanced compliance by patients, and demand for slow-release medications. Their ability to reduce dosing frequency and improve convenience is further strengthening adoption across diverse healthcare settings.

By Sales Channel, Direct Sales Lead While Online Platforms Expand Rapidly:

Direct sales to hospitals and clinics continue to be the dominant route, aided by the high level of trust placed by physicians, effective purchasing procedures, and constant demand from patients for GLP 1-based treatments. This approach guarantees an adequate supply and availability for patients who need continuous treatment for diabetes and obesity.

Online sales have become the fastest-growing route due to increasing adoption of technology in healthcare, ease of delivery, and higher patient preference for receiving drugs remotely. With advancements in e-commerce capabilities and increased insurance coverage, online sales will play a key role in driving the market for Ozempic forward.

By Distribution Channel, Hospital Pharmacies Dominate While Online Pharmacies Expand Rapidly:

The Hospital Pharmacy continues to dominant segment as the main channel of distribution due to the existence of well-defined systems of purchasing, control by physicians, and steady supply of GLP 1 drugs to patients. This explains the continued importance of the hospital pharmacy as the main distribution channel.

The Online Pharmacy is fast becoming one of the most rapidly expanding channels for distribution of Ozempic. The rising number of individuals accessing healthcare services through digital means, convenience of ordering from home, and the patient's desire for more accessible medication are among the reasons for rapid growth in this channel.

Ozempic Market Regional Analysis:

North America Ozempic Market Insights:

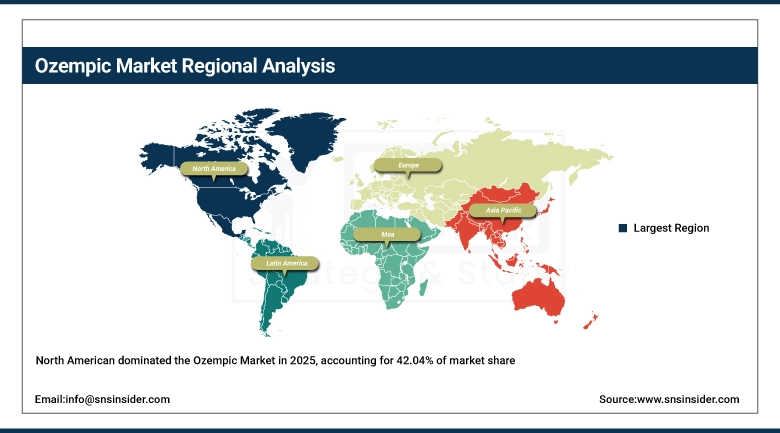

North America Ozempic Market holds dominance with a market share of 42.04%, driven by an excellent healthcare system and higher incidences of type 2 diabetes and obesity in both the U.S. and Canada. The extensive use of GLP-1 receptor agonists, solid reimbursement structures, and clinicians' experience contribute to market expansion. Diversification of uses from managing risks for cardiovascular disease and obesity strengthens its position. Constant innovations in both oral and injectable medicines, along with patient compliance, make North America the most advanced market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Ozempic Market Insights:

North America is a leader in the Ozempic Market, led by the United States on account of the country having a huge diabetic and obese population, superior health care infrastructure, and high acceptance rate of physicians in adopting GLP 1 drugs. Increase in specialty care clinics, new drug delivery methods, and availability of insurance support help enhance the adoption process. Recognition about the advantages related to heart health and lifestyle diseases adds impetus to Ozempic's position in the market.

Asia Pacific Ozempic Market Insights:

The Asia Pacific Market for Ozempic is experiencing significant growth at a CAGR of 11.94%, due to the increasing incidences of diabetes, urbanization trends, and obesity in the region. Countries such as India, Japan, and Australia have contributed significantly to this trend owing to the increased infrastructure in the healthcare sector and greater awareness among physicians regarding GLP 1. With growing access to both oral and injection forms, and the development of new technologies and government programs, the Asia Pacific region is expected to be the fastest-growing market for Ozempic.

China Ozempic Market Insights:

China’s Market for Ozempic is growing very quickly due to China having a large number of patients with diabetes, obesity rates on the rise, and government emphasis on treating chronic illnesses. Growth drivers include significant investments made in healthcare facilities, growing awareness of GLP 1 drugs, and an increased use of oral drugs.

Europe Ozempic Market Insights:

Europe Ozempic Market is influenced by sophisticated healthcare infrastructure, high acceptance rates by physicians, and public awareness about GLP 1 treatments. An increasing number of type 2 diabetics and obese patients in developed nations such as the U.K., France, and Italy increases demand. Therapeutic use cases extending to managing cardiovascular risks and weight loss boost the growth prospects. Effective reimbursement strategies, drug delivery innovations, and consumer inclination toward oral medications drive adoption.

Germany Ozempic Market Insights:

Germany is one of the biggest Ozempic markets in Europe due to the large number of diabetics, strong medical care systems, and advanced application of GLP-1 therapies in clinical settings. The positive inclination of doctors toward newer versions of the drug in combination with favorable insurance plans leads to its swift acceptance. The increasing prevalence of obesity and recognition of heart disease benefits will continue to propel its demand in the market.

Latin America Ozempic Market Insights:

The Latin America Ozempic market is growing at a steady rate due to the growing number of people suffering from diabetes, growing cases of obesity, and improved access to health facilities in countries such as Brazil, Mexico, and Argentina. The use of GLP 1 medications is becoming more widespread as more people realize the importance of managing lifestyle diseases.

Middle East & Africa Ozempic Market Insights:

The Middle East & Africa Market for Ozempic is growing, fueled by high prevalence rates of diabetes and obesity, increasing urbanization, and higher levels of investment in healthcare. Nations such as Saudi Arabia, United Arab Emirates, and South Africa are at the forefront of this trend, aided by better infrastructure and increased awareness among doctors about the benefits of GLP 1 drugs.

Ozempic Market Competitive Landscape:

Novo Nordisk

Novo Nordisk is a top Danish pharma company that invented the revolutionary GLP 1 receptor agonist drug, Ozempic (Semaglutide). Its drug range consists of many medications focused on managing various metabolic diseases. These include a great emphasis on treating obesity, lowering the risks of heart complications, and developing new oral drugs such as Rybelsus. Novo Nordisk is leading the market thanks to efficient logistical operations and effective pricing policies, as demonstrated by a significant decrease in the prices of its drugs in India to compete with generics.

-

In January 2026, Novo Nordisk reduced Ozempic and Wegovy prices in India by up to 48% following semaglutide patent expiry, intensifying competition with local generics.

Eli Lilly

Eli Lilly is an American biopharmaceutical firm that is one of Novo Nordisk’s competitors in the GLP 1 market. Eli Lilly is known for producing several blockbuster drugs, including the treatment for obesity and diabetes known as Zepbound® (tirzepatide) and the recently FDA-approved Foundayo™ (orforglipron), an orally administered pill. Innovation, direct to consumer marketing, and extensive pharmacy partnerships are among the key characteristics of its strategy, which has resulted in rapid growth in both revenue and business within the GLP 1 sector.

-

In November 2025, the U.S. FDA approved Eli Lilly’s Foundayo™, the first oral GLP‑1 pill from the company, intensifying competition with Novo Nordisk’s Wegovy pill.

Sanofi

Sanofi is a pharmaceutical company headquartered in France that has established itself in the marketplace as a company specializing in providing services in the field of diabetes treatment. Unlike companies such as Novo Nordisk and Eli Lilly, Sanofi does not have any direct innovations in GLP 1 but has been actively involved in promoting insulin products in the diabetes market. In addition, the company concentrates its efforts on developing affordable products, introducing support programs for patients, and building healthcare partnerships.

-

In August 2025, Sanofi highlighted its diabetes care initiatives, focusing on innovation, access, and patient support to address the rising burden of type 1 and type 2 diabetes.

Ozempic Market Key Players:

Some of the Ozempic Market Companies are:

-

Novo Nordisk

-

Eli Lilly

-

Sanofi

-

AstraZeneca

-

Pfizer

-

Merck & Co.

-

Johnson & Johnson (Janssen)

-

Roche

-

Novartis

-

Boehringer Ingelheim

-

Amgen

-

Takeda Pharmaceutical

-

Bayer

-

GSK (GlaxoSmithKline)

-

Bristol Myers Squibb

-

AbbVie

-

Teva Pharmaceutical

-

Sun Pharma

-

Cipla

-

Dr. Reddy’s Laboratories

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.18 Billion |

| Market Size by 2035 | USD 61.92 Billion |

| CAGR | CAGR of 10.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Therapeutic Application (Adult-Onset Diabetes, Non-Insulin-Dependent Diabetes, Hyperglycemia Management, Glucose Control Disorders, Others), • By Drug Formulation / Delivery (Injectable [Ozempic Pen), Oral (Rybelsus), Extended-Release Formulations, Combination Therapies, Others), • By Sales Channel (Direct Sales to Hospitals/Clinics, Wholesalers/Distributors, Online Platforms, Government Procurement, Others), • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novo Nordisk, Eli Lilly, Sanofi, AstraZeneca, Pfizer, Merck & Co., Johnson & Johnson (Janssen), Roche, Novartis, Boehringer Ingelheim, Amgen, Takeda Pharmaceutical, Bayer, GSK (GlaxoSmithKline), Bristol Myers Squibb, AbbVie, Teva Pharmaceutical, Sun Pharma, Cipla, Dr. Reddy’s Laboratories. |

Frequently Asked Questions

North America dominated with a 42.04% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 11.94% during 2026–2035.

Injectable (Ozempic Pen) dominated with a 69.87% share in 2025, while Extended-Release Formulations are projected to grow at the fastest CAGR of 13.80% during 2026–2035.

Growth is rising diabetes and obesity prevalence, expanding use of GLP‑1 agonists for weight management, and supportive reimbursement policies.

The market is valued at USD 23.18 Billion in 2025 and is projected to reach USD 61.92 Billion by 2035.

The Ozempic Market is projected to grow at a CAGR of 10.43% during 2026–2035.

Get in Touch