Vascular Snare Market Report Scope & Overview:

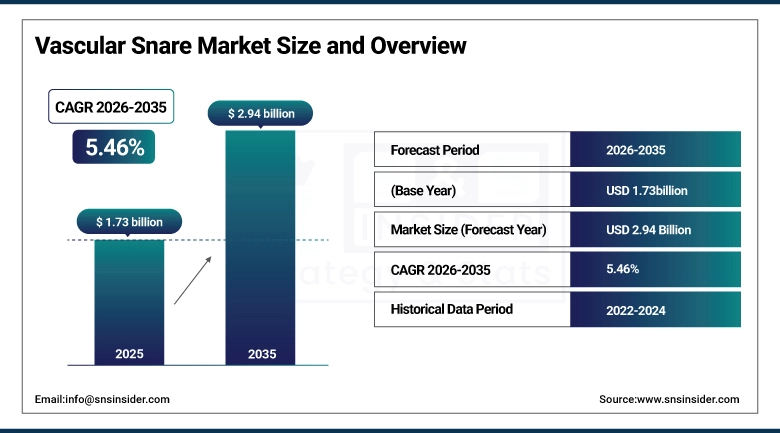

The Vascular Snare Market size is valued at USD 1.73 Billion in 2025 and is projected to reach USD 2.94 Billion by 2035, growing at a CAGR of 5.46% during the forecast period 2026–2035.

This analysis of the Vascular Snare Market report presents an extensive analysis of market dynamics, innovation in products, and clinical applications. The increased use of minimally invasive surgery, the incidence of cardiovascular disease, and demand for foreign body and IVC filter removals are fueling the market's growth between 2026 and 2035.

The vascular snare is widely used more than 5.5 million times in 2025 due to increased interventional radiology and vascular procedures.

Market Size and Forecast:

-

Market Size in 2025: USD 1.73 Billion

-

Market Size by 2035: USD 2.94 Billion

-

CAGR: 5.46% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vascular Snare Market - Request Free Sample Report

Vascular Snare Market Trends:

-

Rising adoption of minimally invasive and interventional procedures is driving increased demand for vascular snare devices.

-

Growing incidence of cardiovascular diseases and related interventions is boosting the need for foreign body and device retrieval solutions.

-

Expansion of advanced snare designs, including multi-loop and nitinol-based devices, is improving precision, flexibility, and procedural success rates.

-

Development of catheter-compatible and imaging-guided snare systems is enhancing procedural efficiency and clinician control.

-

Increasing presence of hospitals, ambulatory surgical centers (ASCs), and specialty clinics is expanding access to interventional vascular procedures.

-

Collaborations between medical device manufacturers, healthcare providers, and research institutions are accelerating product innovation and market adoption.

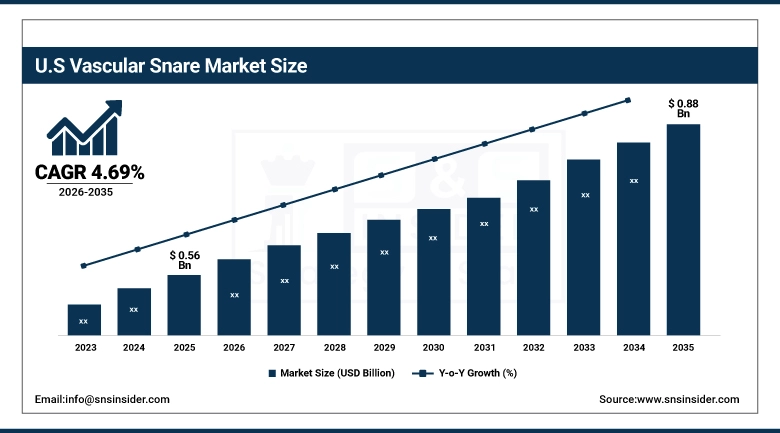

U.S. Vascular Snare Market Insights:

The U.S. Vascular Snare Market is projected to grow from USD 0.56 Billion in 2025 to USD 0.88 Billion by 2035, at a CAGR of 4.69%. Factors responsible for the growth include increased use of minimally invasive and interventional techniques, higher incidence of diseases that require devices to be retrieved, high market share held by top players in the medical device industry, and increased use of snare systems.

Vascular Snare Market Growth Drivers:

-

Rising adoption of minimally invasive and interventional procedures driving demand for advanced vascular snare devices.

The increasing application of minimally invasive and interventional procedures, coupled with the rising prevalence of cardiovascular diseases and complications associated with medical devices, is expected to drive the demand within the Vascular Snare Market. Hospitals, ambulatory surgery centers, and specialty clinics have started making use of advanced snare devices for retrieving foreign objects, removing IVC filters, and conducting complex vascular procedures. Technological advancements such as multi-loop configurations, nitinol material usage, and catheter compatibility are also driving adoption, improving clinical outcomes, and fueling market growth.

More than 62% of hospitals, ambulatory surgery centers, and specialty clinics used advanced vascular snare devices in 2025 for minimally invasive procedures and complex vascular interventions.

Vascular Snare Market Restraints:

-

High device costs and limited reimbursement policies are restraining widespread adoption of advanced vascular snare devices in cost-sensitive markets.

However, the high prices of medical equipment, along with insufficient reimbursement programs, continue to pose major limitations on the growth of the Vascular Snare Market. The high costs associated with the sophisticated snare systems, such as the multi-loop snare system and the nitinol snare, lead to higher operating costs, thus restricting the utilization of these systems in smaller hospitals and ambulatory care centers. Furthermore, inadequate reimbursement policies, budgetary issues, and pricing concerns impede the frequent utilization of the vascular snare systems.

Vascular Snare Market Opportunities:

-

Increasing integration of advanced imaging and precision-guided interventional technologies presents significant market expansion opportunities.

The expanding application of advanced imaging technologies and precision-guided intervention methods presents promising opportunities within the Vascular Snare Market. Contemporary hospitals and specialized medical facilities are progressively adopting state-of-the-art snare instruments, characterized by enhanced adaptability and compatibility with real-time imaging systems, to facilitate intricate vascular procedures. This burgeoning trend is advantageous for innovative snare systems developed by medical technology companies. Enhancements in catheter guidance technology, ergonomic design, and imaging compatibility are fostering their extensive use in complex retrievals and interventional therapies.

More than 49% of healthcare organizations are utilizing sophisticated imaging-compatible vascular snare devices in 2025 due to the rising need for precision-based vascular interventions.

Vascular Snare Market Segmentation Analysis:

-

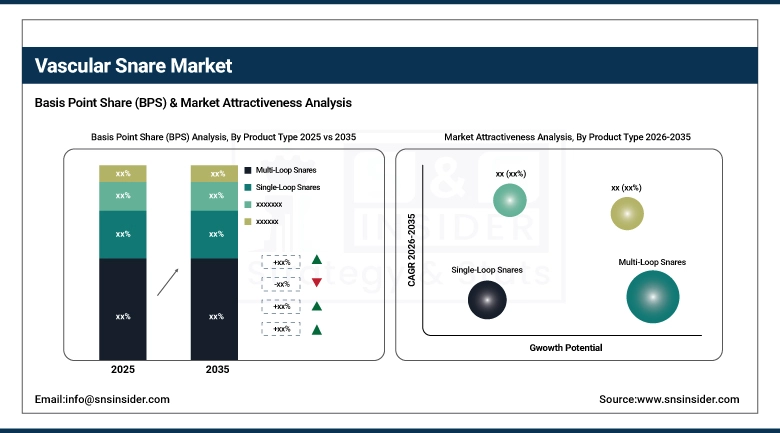

By Product Type, Multi-Loop Snares held the largest market share of 42.25% in 2025, while Nitinol Snares are expected to grow at the fastest CAGR of 6.59% during 2026–2035.

-

By Application, Foreign Body Retrieval dominated with a 38.25% market share in 2025, whereas Inferior Vena Cava (IVC) Filter Retrieval is projected to record the fastest CAGR of 7.19% through 2026–2035.

-

By End User, Hospitals held the largest share of 65.25% in 2025, while Ambulatory Surgical Centers (ASCs) are expected to grow at the fastest CAGR of 6.90% during the forecast period.

-

By Material Type, Nitinol accounted for the highest market share of 52.12% in 2025 and is also expected to grow at the fastest CAGR of 6.30% during 2026–2035.

By Product Type, Multi-Loop Snares Dominate While Nitinol Snares Grow Rapidly:

Multi-Loop Snares segment dominated the market due to their superior capture efficiency, enhanced flexibility, and widespread use in complex foreign body and device retrieval procedures across hospitals and ambulatory surgical centers. In 2025, usage exceeded 2.3 million procedures, reflecting strong preference among interventional specialists for reliable and precise retrieval performance.

Nitinol Snares are the fastest-growing segment, driven by increasing demand for advanced materials offering shape memory, durability, and improved maneuverability. Adoption surged, with over 1.2 million procedures utilizing nitinol-based devices in 2025, particularly in complex vascular interventions requiring high precision and flexibility.

By Application, Foreign Body Retrieval Dominates While IVC Filter Retrieval Grows Rapidly:

Foreign Body Retrieval segment dominated the market, widely used in interventional radiology and cardiology procedures for removing fractured devices, catheters, and embolized materials. In 2025, over 2.1 million procedures were performed, highlighting strong reliance among hospitals and specialty clinics for routine and emergency interventions.

Inferior Vena Cava (IVC) Filter Retrieval is the fastest-growing segment, fueled by increasing awareness regarding long-term complications of implanted filters and rising procedural volumes. Usage reached over 1.3 million procedures in 2025, especially in developed healthcare systems, reflecting rapid adoption and expanding clinical necessity.

By End User, Hospitals Dominate While Ambulatory Surgical Centers Grow Rapidly:

Hospitals segment dominated the market due to high patient inflow, availability of advanced imaging infrastructure, and presence of skilled interventional specialists performing complex vascular procedures. In 2025, hospitals accounted for over 3.5 million snare-assisted procedures, demonstrating their central role in interventional care delivery.

Ambulatory Surgical Centers are the fastest-growing segment, driven by increasing preference for cost-effective outpatient procedures and shorter recovery times. Procedure volumes exceeded 1.4 million in 2025, particularly for minimally invasive interventions, highlighting rapid expansion and growing adoption outside traditional hospital settings.

By Material Type, Nitinol Dominates While Advanced Alloy-Based Snares Grow Rapidly:

Nitinol segment dominated the market, widely preferred due to its superior flexibility, shape memory properties, and high durability in complex vascular procedures. Interventional specialists continue to favor nitinol-based snares for their ability to maintain loop integrity and performance in challenging anatomical conditions.

Advanced alloy-based snares are the fastest-growing segment, driven by continuous material innovations and increasing demand for enhanced strength and maneuverability. In 2025, usage surpassed 1.5 million procedures, particularly in complex and minimally invasive interventions, highlighting growing adoption of next-generation materials to improve procedural success and clinical outcomes

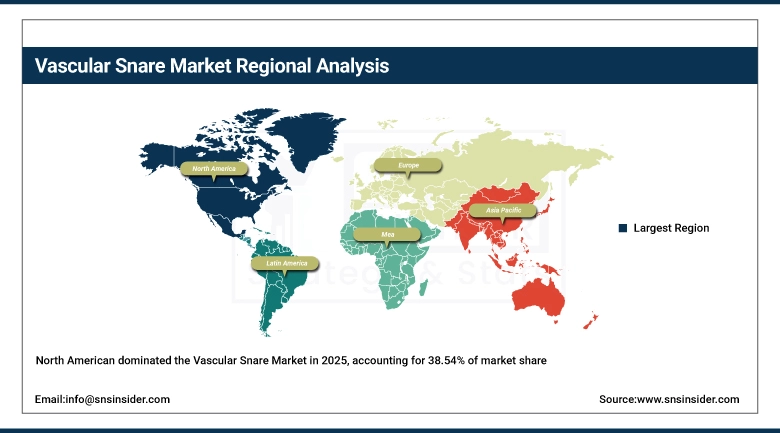

Vascular Snare Market Regional Analysis:

North America Vascular Snare Market Insights:

The North America Vascular Snare Market is dominant, holding a 38.54% share in 2025 supported by a high volume of interventional procedures and advanced healthcare infrastructure across the U.S. and Canada. Strong utilization of multi-loop and nitinol-based snare devices in hospitals and ambulatory surgical centers drives market growth. Increasing incidence of cardiovascular conditions, rising demand for minimally invasive retrieval procedures, and availability of skilled interventional specialists further strengthen adoption. Continuous product innovations, integration with advanced imaging systems, and favorable reimbursement frameworks reinforce North America’s leadership in this mature and technology-driven market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Vascular Snare Market Insights:

The U.S. Vascular Snare Market is driven by a large number of interventional radiology and cardiology procedures, along with widespread adoption of advanced snare devices. High demand for foreign body retrieval and IVC filter removal, combined with strong presence of leading medical device manufacturers, supports market expansion. Well-established hospital networks, increasing shift toward outpatient procedures, and ongoing technological advancements in device design and precision further position the U.S. as the leading contributor within North America.

Asia-Pacific Vascular Snare Market Insights:

The Asia-Pacific Vascular Snare Market is the fastest-growing region, projected to expand at a CAGR of 6.97% during 2026–2035. It is driven by expanding healthcare infrastructure and rising adoption of minimally invasive procedures across China, India, Japan, and Southeast Asia. Increasing burden of cardiovascular diseases, growing awareness of interventional treatments, and improving access to advanced medical devices are accelerating demand. Rapid expansion of hospitals and ambulatory surgical centers, coupled with investments in healthcare modernization and training of interventional specialists, is supporting strong growth and increasing penetration of vascular snare devices across the region.

China Vascular Snare Market Insights:

Some of the factors propelling the growth of China Vascular Snare Market include an increased rate of procedures, higher burden of cardiovascular disorders, and fast development of hospitals' infrastructures. The increased usage of advanced types of vascular snare systems, such as multi-loop, and the nitinol variety, alongside with the growth of tertiary care centers and interventional radiology facilities, will positively influence the procedure rate. Improved accessibility to minimally invasive treatments, various government healthcare initiatives, and growing experience of clinicians will lead to China becoming one of the largest contributors in Asia Pacific market.

Europe Vascular Snare Market Insights:

Europe Vascular Snare Market is expected to be fuelled by the country's highly developed healthcare industry, growing number of interventions, and growing popularity of minimally invasive approaches to disease treatment. The increased number of procedures performed with the help of advanced vascular snare devices is driving the regional market growth, especially for countries such as Germany, France, and the UK. Increased prevalence of outpatient care centers, growing adoption of precision-based treatment techniques, and proper reimbursement rates will lead to higher device usage. Increased prevalence of outpatient care centers, growing adoption of precision-based treatment techniques, and proper reimbursement rates will lead to higher device usage.

Germany Vascular Snare Market Insights:

As one of the key markets in the European Vascular Snare region, Germany is characterized by well-developed medical infrastructure and high rates of interventional radiology procedures. Germany's contribution in regional market growth is fueled by the increasing use of advanced snare systems, large number of specialized hospitals, and constant improvements in the area of healthcare infrastructure.

Latin America Vascular Snare Market Insights:

One of the main drivers for Latin America Vascular Snare Market is the increased adoption of minimally invasive procedures and growing healthcare accessibility throughout the region. Some of the key factors influencing Latin American market growth include the high adoption of vascular snare devices in Latin America nations such as Brazil, Mexico, and Argentina, along with the development of hospital networks and interventional capabilities.

Middle East and Africa Vascular Snare Market Insights:

The Middle East & Africa Vascular Snare Market is expanding due to improving healthcare infrastructure and increasing adoption of interventional procedures. Growing use of advanced snare devices in hospitals and specialty centers is driving demand, with countries such as Saudi Arabia, the UAE, and South Africa emerging as key regional markets. Investments in healthcare modernization, rising availability of skilled professionals, and increasing focus on minimally invasive treatments are supporting market development across the region.

Vascular Snare Market Competitive Landscape:

Medtronic plc is a dominant player in the vascular snare market, leveraging its leadership in endovascular and catheter-based intervention systems. The company benefits from deep integration across the vascular procedure ecosystem, including guidewires, catheters, and access devices, which strengthens cross-selling of snare products. Its scale, physician relationships, and strong hospital penetration enable consistent demand across complex interventional procedures. Medtronic’s strategic focus on neurovascular and peripheral interventions positions it well to capture growth from increasing minimally invasive procedures and complex retrieval cases.

-

In March 2026, Medtronic announced the acquisition of Scientia Vascular for approximately USD 550 million, strengthening its microcatheter and access platform, which directly enhances compatibility and performance of vascular snare procedures in complex interventions.

Boston Scientific Corporation holds a strong competitive position in the vascular snare market due to its specialization in interventional cardiology and radiology devices. The company’s strength lies in continuous innovation in device precision, control mechanisms, and integration with imaging-guided systems, which are critical in retrieval procedures. Its aggressive expansion strategy through acquisitions and portfolio diversification enables it to compete across the full vascular intervention workflow. Boston Scientific also benefits from strong physician training programs, driving higher adoption of its devices in complex cases.

-

In January 2026, Boston Scientific announced the acquisition of Penumbra, Inc., significantly expanding its thrombectomy and vascular intervention capabilities, thereby strengthening its ecosystem relevance and increasing procedural demand for complementary devices such as vascular snares.

Cook Medical is a specialized and highly respected player in the vascular snare market, particularly strong in interventional radiology. The company’s competitive advantage lies in its focused product portfolio, strong brand trust among clinicians, and early-mover expertise in vascular retrieval devices. Cook’s snares are widely used due to their reliability and procedural familiarity among physicians. Unlike diversified giants, Cook benefits from niche dominance and deep clinical relationships, especially in complex foreign body retrieval procedures.

-

In July 2025, Cook Medical expanded its vascular intervention portfolio with new endovascular device launches, reinforcing its positioning in complex procedural environments and indirectly driving sustained demand for its established vascular snare product line.

Vascular Snare Market Key Players:

Some of the Vascular Snare Market Companies are:

-

Medtronic plc

-

Boston Scientific Corporation

-

Cook Medical

-

Merit Medical Systems, Inc.

-

Becton, Dickinson and Company (BD)

-

Teleflex Incorporated

-

Terumo Corporation

-

Cardinal Health

-

Integer Holdings Corporation

-

Olympus Corporation

-

Edwards Lifesciences Corporation

-

Abbott Laboratories

-

Stryker Corporation

-

AngioDynamics, Inc.

-

Penumbra, Inc.

-

Argon Medical Devices, Inc.

-

Acandis GmbH

-

Lepu Medical Technology

-

MicroPort Scientific Corporation

-

Surmodics, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.73 Billion |

| Market Size by 2035 | USD 2.94 Billion |

| CAGR | CAGR of 5.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Multi-Loop Snares, Single-Loop Snares, Nitinol Snares, Others) • By Application (Foreign Body Retrieval, Inferior Vena Cava (IVC) Filter Retrieval, Thrombus Removal, Guidewire Manipulation, Others) • By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Others) • By Material Type (Nitinol, Stainless Steel, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Boston Scientific Corporation, Cook Medical, Merit Medical Systems, Inc., Becton, Dickinson and Company (BD), Teleflex Incorporated, Terumo Corporation, Cardinal Health, Integer Holdings Corporation, Olympus Corporation, Edwards Lifesciences Corporation, Abbott Laboratories, Stryker Corporation, AngioDynamics, Inc., Penumbra, Inc., Argon Medical Devices, Inc., Acandis GmbH, Lepu Medical Technology, MicroPort Scientific Corporation, Surmodics, Inc. |

Frequently Asked Questions

North America dominated with a 38.54% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 6.97% during 2026–2035.

Multi-Loop Snares dominated with a 42.25% share in 2025, while Nitinol Snares are projected to grow at the fastest CAGR of 6.59% during 2026–2035.

Growth is driven by rising adoption of minimally invasive and interventional procedures driving demand for advanced vascular snare devices.

The market is valued at USD 1.73 Billion in 2025 and is projected to reach USD 2.94 Billion by 2035.

The Vascular Snare Market is projected to grow at a CAGR of 5.46% during 2026–2035.

Get in Touch