Pharma 4.0 Market Report Scope & Overview:

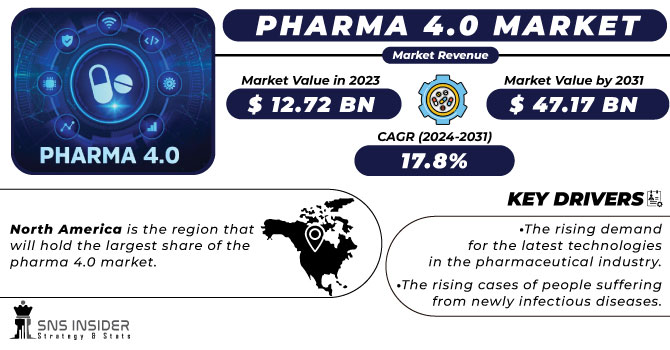

According to SNS INSIDER, the Pharma 4.0 Market Size was valued at 12.72 Bn in 2023 and is expected to reach 47.17 Bn by 2031, and grow at CAGR of 17.8% over the forecast period of 2024-2031.

Get more information on Pharma 4.0 Market - Request Free Sample Report

The healthcare industry seems to be very diversified and complex. When we mention complex there are different diseases that are associated with different symptoms. The rising technological advancement and the infrastructure related to the same is the major element that promises the growth of the healthcare industry. Now, when we particularly focus on the pharmaceutical sector COVID-19 gave a boost to this particular sector in terms of advancement, investments from government organizations, and so forth. According to the statistics, the rise in the disease all around the world is extremely high. The rising disease is creating opportunities for the pharmaceutical industry to develop new drugs, and vaccines. However, the old patterns and the traditional equipment is not match up the speed and help the innovators throughout the product life cycles. This particular statement has been stated by the operational head of Abbott company.

The opportunity for advancement in the pharmaceutical industry is very promising because of the rising demand for the latest techniques and technological advancement. The innovation of the smart factory in pharmaceuticals mainly known as Pharma 4.0 is considered as the real game changer. The only objective and goal of the pharmaceutical companies are to implement automation and the digitalization platform in their entire process. Ai in drugs and delivery can be considered the major element for pharma 4.0.

Pharma 4.0 is very much focused on data integrity, robotics, automation, and so forth. The use of the data is been done to analyze the quality control and user feedback which will eventually help the key players in revising their products and services. The need for advancement is surreal as the rise in the new infectious disease is high. According to the survey conducted by the Centers for Disease Control and Prevention (CDCP), the threat to people living in developed and emerging countries is very high. Keeping these factors in mind the only concern for the pharmaceutical industry in this scenario is related to the production, longer duration, and fluctuations in the prices of raw materials. Pharma 4.0 might be the antidote that will help pharmaceutical companies solve the problems that we have mentioned above.

Market Dynamics:

Driver

- The rising demand for the latest technologies in the pharmaceutical industry.

- The rising cases of people suffering from newly infectious diseases.

The rising number of chronic diseases all around the globe because of unhealthy lifestyles and other reasons is the driving factor for the pharmaceutical industry as of now. The major companies in the pharmaceutical industry have assured the real importance of digitalization in the pharmaceutical industry. Pharma 4.0 promises the improvement of data quality and reduction in the cycle times which are related to the product/drug innovation. For instance, Pfizer is using real-world data to help improve cancer care.

Opportunity

- The rising R&D investments for this particular market.

- Rising awareness of the digitalization and automation in the pharmaceutical industry.

- The rise in drug development and clinical trials.

The rise in drug development by pharmaceutical companies is on the highest pitch. For instance, Pfizer is in the midst of launching 19 new products which include vaccines and medicines that cover various diseases such as prostate cancer, flu, migraine, sickle cell disease and others. Siemens Healthcare has stated that the increase in R&D activities is completely focusing on implementation of the AI and data analytics tools. The only concern for the companies while developing drugs/vaccines is the high labor wages. So, the use of the latest technologies can help them reduce the cost. These are some of the facts and the statement that showcases the opportunity for the market to grow during the forecasted period.

Challenges

- The threat related to cybersecurity and data breaching.

The digitalization and the software-based services are dependent on the data. The rising cases of data breaches can violate the privacy of patients which can have a negative impact on the market.

Other major risk factors include the rising inflation pressure which can impact clinical trials, also the shortage of labor can affect the market negatively.

Impact of Recession:

Pharmaceutical businesses may cut back on their R&D spending during recessions. The creation and application of cutting-edge technologies in the sector, such as Pharma 4.0, may be impacted by this. Companies may put a higher priority on cost-cutting strategies, potentially postponing or reducing projects involving technical developments. Companies may be reluctant to invest in new technologies during a recession due to financial restrictions. This can delay the uptake and use of Pharma 4.0 projects. Companies might, at least initially, place a greater emphasis on cost-cutting methods than on making investments in cutting-edge technology.

Impact of Russia-Ukraine War:

The conflict's effects on economic and geopolitical stability may extend to the pharmaceutical industry as a whole. Pharmaceutical product pricing and profitability may be impacted by market turbulence and changing exchange rates. Pharma 4.0 technology may not be adopted and used as planned if businesses are hesitant to make investments due to the uncertain business environment.

Governments frequently place a higher priority on national security during times of conflict, and they may enact regulations or limitations that have an influence on the pharmaceutical sector. The free flow of technology and intellectual property associated with Pharma 4.0 may be impacted by new rules, export restrictions, or import prohibitions. Advanced technology installation may be slowed down or made more difficult for businesses by increasing compliance requirements.

Regional Analysis:

North America is the region that will hold the largest share of the pharma 4.0 market. The rising clinical trials and the developments by the key players which are operating in this region is the driving factor for this market. The developed countries in this region have a great hold on the overall market. For instance, the U.S. is the major country for pharmaceutical companies for generating more of their revenues. The support from the FDA in terms of approving the latest technological advancement which will be used for the drug innovation contributes to the growth of the market.

APAC is the region that will have the largest CAGR growth rate, as the rising government funding and the development of the healthcare infrastructure will enhance the growth of the market. There are various programs and plans which are been designed by governments of developed countries like China, and Japan which support the growth of the pharma 4.0 market during the forecasted period.

Need any customization research on Pharma 4.0 Market - Enquiry Now

Key Players

The major key players are Pfizer, Koninklijke Philips N.V, Abbott Laboratories, Medtronic Plc, GlaxoSmithKline plc, Boston Scientific, GE Healthcare, Johnson & Johnson, Lonza Group Ag, Glatt GmbH, Vertex and others.

Abbott Laboratories-Company Financial Analysis

Recent Developments

Boston Scientific: The official announcement done by the company in where they acquired a majority stake of Acotec Scientific Holdings Limited. Acotec is said to be a Chinese medical technology company that offers diversified solutions.

Lonza: The acquisition of Synaffix which strengthens the Antibody-Drug Conjugates offerings. The company is innovative which will improve Lonza company’s technology platform and offering capabilities.

“The only objective behind mentioning the M&A is to showcase the current situation of the Pharma 4.0 market. The major key players are acquiring the companies in order to improve their process in terms of product development and providing the services.”

| Report Attributes | Details |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Design (Capabilities, Digital Maturity, Data Integrity) • By Technology (Big Data Analytics, Cloud Computing, Cyber-physical Systems, Other) • By End User (Hospitals, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Pfizer, Koninklijke Philips N.V, Abbott Laboratories, Medtronic Plc, GlaxoSmithKline plc, Boston Scientific, GE Healthcare, Johnson & Johnson, Lonza Group Ag, Glatt GmbH, Vertex |

| Key Drivers | • The rising demand for the latest technologies in the pharmaceutical industry • The rising cases of people suffering from newly infectious diseases |

| Market Opportunities | • Rising awareness of digitalization and automation in the pharmaceutical industry. • The rise in drug development and clinical trials. |

Frequently Asked Questions

The rising demand for the latest technologies in the pharmaceutical industry.

The threat related to the cybersecurity and data breaching.

North America is the region which will hold the largest share of the pharma 4.0 market.

The pharma 4.0 is very much focused on data integrity, robotics, automation and so forth.

The rising R&D investments for this particular market.

Get in Touch