Prostate Health Market Report Scope & Overview:

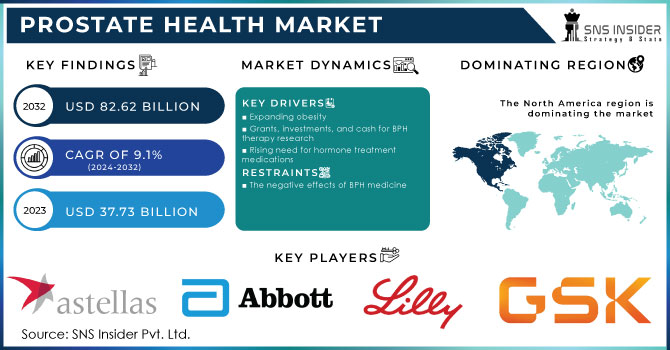

The Prostate Health Market Size was valued at USD 37.73 billion in 2023, and is expected to reach USD 82.62 billion by 2032 and grow at a CAGR of 9.1% over the forecast period 2024-2032.

An organ of the male reproductive system is the prostate gland. Benign prostatic hyperplasia, also known as BPH, is a benign enlargement of the prostate that is the third most prevalent type of prostate illness after inflammation (prostatitis). Men are said to be affected by the condition known as benign prostatic hyperplasia (BPH). It involves non-cancerous prostate gland hypertrophy. The likelihood of developing BPH rises with age, even though it rarely manifests symptoms before the age of 42. Up to 91% of males over the age of 80 and over 50% of men between the ages of 52 and 62 are affected by the disorder. Patients with BPH have received treatment through the use of drugs and surgery.

Get more information on Prostate Health Market - Request Sample Report

MARKET DYNAMICS

DRIVERS

-

Expanding obesity

-

Grants, investments, and cash for BPH therapy research

-

Increasing prostate cancer incidence

-

Rising need for hormone treatment medications

-

Novel treatments for prostate cancer

RESTRAINTS

-

The negative effects of BPH medicine

OPPORTUNITIES

-

Newer markets

-

Favourable product pipeline

CHALLENGES

-

Men's knowledge of prostate health is lacking

-

Prostate health market recalls of products

IMPACT OF COVID-19

The prostate health market experienced a decline in sales, and the pattern persisted through the end of December 2020. The development of this industry is being constrained by unfavorable changes in legislation and standards. Major regulatory bodies from all around the world, including the CDC, WHO, MHRA, TGA, and EMA, have determined that people with cancer are more likely to get COVID-19 infection than healthy adults. So, at hospitals and cancer treatment facilities, screening, diagnostic tests, and surgical procedures are severely limited or delayed. Market upheavals in the field of prostate health are anticipated as a result. Hospitals and caregivers might expect delays in screening procedures and elective surgery as a result of the aforementioned issues.

By Disease Indication

In the global market, the prostate cancer sector is predicted to account for the biggest revenue share. Hormone therapy is typically a successful first-line cancer treatment strategy. Alternatives to hormonal therapy include chemotherapies, radiopharmaceuticals, cancer vaccinations, and follow-up hormone therapies. Within a few months, cancerous cells develop resistance to these medications. As a result, over the course of the projected period, immunotherapies are expected to be extensively used for cancer treatment.

KEY MARKET SEGMENTS:

By Disease Indication:

-

Prostate Cancer

-

AR Directed Therapies

-

Hormone ADT

-

Cytotoxic Agents

-

PARP Inhibitors

-

-

Benign Prostate Hyperplasia

-

Alpha Blockers

-

5 Alpha Reductase

-

-

Prostatitis

-

Prescription

-

Over the counter

-

REGIONAL ANALYSIS

Among the pioneers in the field of health care, North America was developing bladder supplements. The US market increase, which has a major impact on North America's prostate health market, can be attributed primarily to targeted population growth, high incidence of BPH, prostate cancer, prostatitis, and an increase in medical equipment. manufacturers. The expansion of this market is fueled by lucrative refund policies, high losses, strong health care infrastructure, research funding, and new releases.

Need any customization research on Prostate Health Market - Enquiry Now

REGIONAL COVERAGE

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS:

The Major key players are Astellas Pharma, Eli lilly and Company, Glaxo smithkline, Abbott Laboratories, Abbvie, JOHNSON & JOHNSON SERVICES, INC., AstraZeneca, Merck, SANOFI, Pfizer inc, and other players.

| Report Attributes | Details |

| Market Size in 2023 | US$ 37.73 Billion |

| Market Size by 2032 | US$ 82.62 Billion |

| CAGR | CAGR of 9.1% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Disease Indication (Prostate Cancer (AR Directed Therapies, Hormone ADT, Cytotoxic Agents, PARP Inhibitors), Benign Prostate Hyperplasia (Alpha Blockers, 5 Alpha Reductase), Prostatitis (Prescription, Over the counter) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Astellas Pharma, Eli lilly and Company, Glaxo smithkline, Abbott Laboratories, Abbvie, JOHNSON & JOHNSON SERVICES, INC., AstraZeneca, Merck, SANOFI, Pfizer inc, and other players. |

| Key Drivers | • Expanding obesity • Grants, investments, and cash for BPH therapy research • Increasing prostate cancer incidence |

| Restraints | • The negative effects of BPH medicine |

Frequently Asked Questions

-

Expanding obesity

-

Grants, investments, and cash for BPH therapy research

-

Increasing prostate cancer incidence

Ans: The forecast period of the Prostate Health Market is 2024-2032.

-

Men's knowledge of prostate health is lacking

-

Prostate health market recalls of products

Ans: The Prostate Health Market is to grow at a CAGR of 9.1% over the forecast period 2024-2032.

Ans: The Prostate Health Market size is estimated to reach US$ 82.62 Bn by 2032.

Get in Touch