Regenerative Agriculture Market Report Scope & Overview:

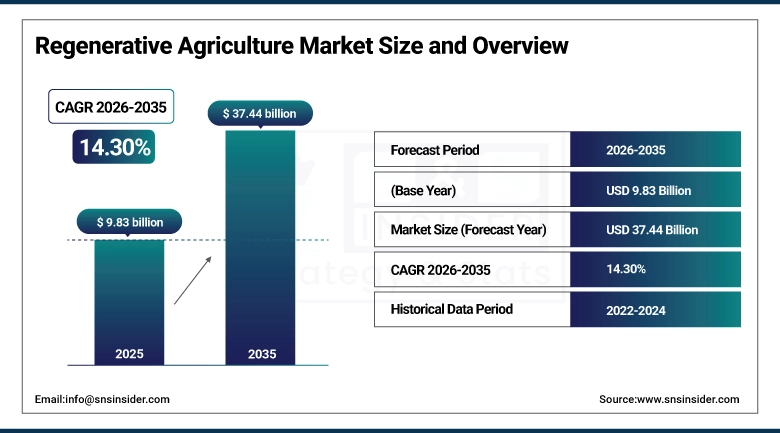

The Regenerative Agriculture Market size was valued at USD 9.83 Billion in 2025 and is projected to reach USD 37.44 Billion by 2035, growing at a CAGR of 14.30% during 2026–2035.

Increasing demand for sustainable food products, rising concern for soil erosion and global warming, and growing adoption of eco-friendly agricultural practices are anticipated to fuel the growth of the global regenerative agriculture market during the forecast period. There are also governments incentivizing farmers to practice regenerative agriculture, aiming at carbon reduction and soil health. In addition, organizations vowing to reduce their carbon footprints, being thereby urging farmers to adopt regenerative agriculture, are acting as the key growth driver for the Regenerative Agriculture Market, enabled by means of a technology like precision agriculture respectively.

Regenerative Agriculture Market Size and Growth:

-

Market Size in 2025: USD 9.83 Billion

-

Market Size by 2035: USD 37.44 Billion

-

CAGR: 14.30% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Regenerative Agriculture Market - Request Free Sample Report

Regenerative Agriculture Market Key Trends:

-

Increasing adoption of sustainable farming practices such as no-till farming, cover cropping, and crop rotation is driving the transformation toward soil health restoration and long-term agricultural productivity.

-

Rising focus on carbon sequestration and carbon credit programs is encouraging farmers to adopt regenerative agriculture techniques to reduce greenhouse gas emissions and generate additional income streams.

-

Growing consumer demand for organic and sustainably sourced food products is pushing food companies to integrate regenerative practices into their supply chains.

-

Advancements in precision agriculture technologies, including AI, IoT, and satellite monitoring, are improving farm efficiency, resource optimization, and soil management.

-

Increasing partnerships between agribusiness companies, governments, and farmers are accelerating the adoption of regenerative agriculture practices globally.

-

Expansion of sustainable agriculture initiatives in emerging economies is boosting awareness and adoption of regenerative farming methods.

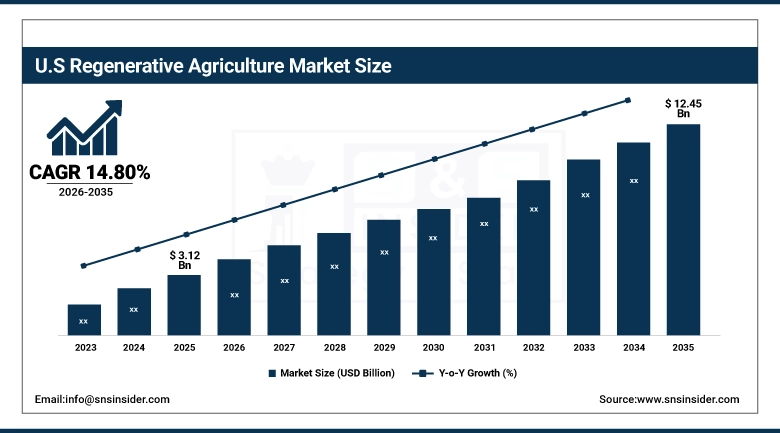

U.S. Regenerative Agriculture Market Size Outlook:

The U.S. Regenerative Agriculture Market size was valued at approximately USD 3.12 Billion in 2025 and is projected to reach around USD 12.45 Billion by 2035, growing at a CAGR of 14.80% during 2026–2035. Growth is driven by rising demand for sustainable food, increasing soil health awareness, government incentives, corporate sustainability commitments, and adoption of regenerative farming practices supported by advanced agricultural technologies.

Regenerative Agriculture Market Key Drivers:

-

Rising demand for sustainable and organic food products driving adoption of regenerative farming practices.

Regenerative Agriculture Market Dynamics The high demand for eco-friendly and chemical-free food is the key reason which is supporting growth of the Regenerative Agriculture Market. Farmers have also started adopting regenerative agriculture practices like no-till method and rotational cropping because of awareness regarding the soil and biodiversity health and global warming. Moreover, initiatives by governments and businesses to adopt sustainable business models will also drive the market.

Regenerative Agriculture Market Key Restraints:

-

High transition costs and lack of standardized certification limiting widespread adoption.

The process of moving from conventional to regenerative farming is a costly process for training and equipment and changing farming practices. This is a challenge for mid and small-scale farmers. Secondly, there is a lack of certification and measurable results, and this creates uncertainty around market value. These challenges hinder the adoption of regenerative farming despite the increased market demand for sustainable agriculture.

Regenerative Agriculture Market Key Opportunities:

-

Growing carbon credit markets and sustainable supply chain initiatives creating new revenue streams.

The expansion of carbon credit programs also provides financial incentives for farmers who use regenerative farming practices that improve carbon sequestration in soils. Furthermore, partnerships between food companies and farmers in developing sustainable food systems are creating new growth opportunities. More investment in precision agriculture technologies also helps improve efficiency and productivity.

Regenerative Agriculture Market Segments:

-

By Component: Dominant – Solutions (64.00% → 58.00%, CAGR 13.10%); Fastest-Growing – Services (36.00% → 42.00%, CAGR 15.20%)

-

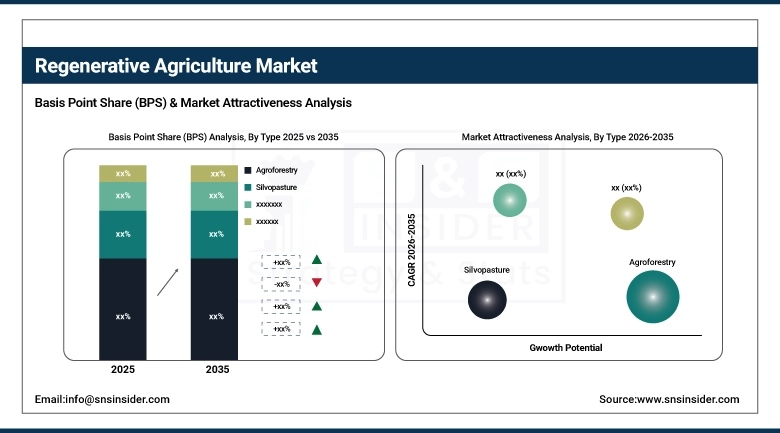

By Type: Dominant – Agroforestry (41.50% → 38.20%, CAGR 12.80%); Fastest-Growing – Aquaculture (18.20% → 22.90%, CAGR 15.60%)

-

By End-User: Dominant – Farmers (52.30% → 47.80%, CAGR 13.40%); Fastest-Growing – Financial Institutions (14.50% → 19.60%, CAGR 16.10%)

-

By Application: Dominant – Soil Health Improvement (46.80% → 42.50%, CAGR 13.20%); Fastest-Growing – Carbon Sequestration (28.40% → 34.70%, CAGR 16.50%)

By Component, Solutions Dominate While Services Are Fastest Growing:

The segment of solutions was a major contributor to the market due to the increasing demand for sustainable inputs, technologies, and platforms. Solutions include tools such as soil management, biological products, and digital farming. The awareness of farmers regarding the importance of soil health and optimizing crop yields was a major contributor to the demand side of the market in 2025.

Services is the segment that is growing the fastest, driven by increased demand for services. Farmers need guidance from experts regarding the shift from conventional farming to regenerative farming, which has increased the growth rate of this segment.

By Type, Agroforestry Dominates While Aquaculture Is Fastest Growing:

The agroforestry segment held the largest share of the market due to its potential to improve biodiversity, soil fertility, and generate multiple income streams. This type of farming is used on a large scale due to its long-term environmental and economic benefits.

Aquaculture is the fastest-growing segment of regenerative farming due to the increased need for sustainable seafood production and regenerative ocean practices. Investments in sustainable aquaculture systems and regenerating marine ecosystems are on the rise.

By End-User, Farmers Dominate While Financial Institutions Are Fastest Growing:

The farmers’ segment dominated this market, as they are the major adopters of regenerative agriculture practices. Awareness of soil health, crop productivity, and sustainability has encouraged people from farming communities to adopt regenerative agriculture practices.

The Financial Institutions segment is expected to witness the highest growth in the regenerative agriculture market, as more investments are being made in sustainable agriculture and green financing.

By Application, Soil Health Improvement Dominates While Carbon Sequestration Is Fastest Growing:

The Soil Health Improvement segment was leading in the market due to its direct impact on crop productivity and long-term sustainability. As regenerative practices mainly focus on improving soil health, this was the leading segment.

The Carbon Sequestration segment is growing the fastest in the market. This is due to the increased awareness of climate change and carbon credits. Regenerative practices are being used to sequester carbon and provide additional income for farmers.

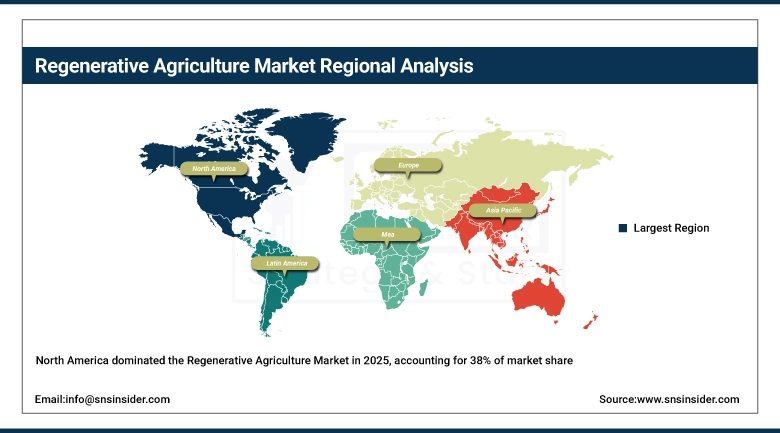

Regenerative Agriculture Market Regional Analysis:

North America Regenerative Agriculture Market Insights:

North America has the highest Regenerative Agriculture Market share, contributing to more than 38% of the overall market share. The key factors contributing to the dominance of the Regenerative Agriculture Market in the North American region are the favorable government initiatives, favorable regulations, and the presence of large-scale commercial farms. The increasing commitments of companies to sustainable sourcing, particularly by large food and beverage companies, are also contributing to the growth of the Regenerative Agriculture Market. The increasing awareness of the importance of soil health, carbon sequestration, and climate change mitigation is also contributing to the growth of the Regenerative Agriculture Market, as farmers are adopting this method of agriculture.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Regenerative Agriculture Market Insights:

Asia-Pacific is the fastest-growing segment in the Regenerative Agriculture Market, which is expected to grow at a CAGR of more than 15.5% from 2026 to 2035. This is attributed to the increasing population and the need for more food products, the growing need for sustainable farming practices, and the increasing concern over soil erosion. The government is promoting eco-friendly farming practices in countries like India, China, and Australia. In addition, the increasing agricultural activities and the use of modern farming practices are contributing to the growth of the market.

Europe Regenerative Agriculture Market Insights:

The Regenerative Agriculture Market is witnessing steady growth in Europe due to stringent environmental regulations and supportive government policies for sustainable agriculture. The region has a well-established organic farming industry, and increasing emphasis is being placed on carbon neutrality and biodiversity. This is resulting in the increased adoption of regenerative agriculture. The government is also encouraging farmers to shift from conventional farming to regenerative farming through subsidies and sustainability programs. In addition, increasing consumer demand for organic food is also contributing to the growth of the Regenerative Agriculture Market.

Latin America Regenerative Agriculture Market Insights:

Moderate growth is being recorded in Latin America, driven by the availability of huge agricultural land coupled with favorable climatic conditions for regenerative farming. This is particularly true for countries such as Brazil and Argentina, driven by the growing awareness of the importance of conserving soils through sustainable farming methods. Moreover, the growing demand for exported agricultural products is also driving growth in the region. Agroforestry and pasture-based regenerative farming are also becoming popular in the region.

Middle East & Africa (MEA) Regenerative Agriculture Market Insights:

The Middle East & Africa is becoming a segment of the Regenerative Agriculture Market as land needs conservation through good and sustainable management of the land due to the fact that there is no water as the land is dry and arid. With a ballooning population in West Africa, governments are pouring money into new irrigation technology and sustainable agriculture to boost food production in the region. Although the market is in its nascent phase in this region, growing concerns regarding soil degradation & climate change, coupled with increasing investments & technological advancements is expected to aid the regional market to grow steadily.

Regenerative Agriculture Market Competitive Landscape:

Vayda, established in the United States in 2020, seeks to catalyze the shift to regenerative agriculture by offering digital tools, agronomic support, and financial rewards to farmers. The company works with food companies and the food value chain to deliver large-scale regenerative agriculture practices, healthy soils, and carbon reduction. It is recognized for its data-driven strategy and farmer-centric solutions that increase sustainability and productivity.

-

In 2024, Vayda expanded its regenerative agriculture programs across North America, strengthening partnerships with major food companies to promote sustainable sourcing and carbon reduction initiatives.

Terramera Inc., a Canada-based company established in 2010, develops plant-based crop protection solutions and leverages artificial intelligence to improve agricultural productivity while reducing environmental impact. The company integrates regenerative principles with advanced technology to create sustainable alternatives to conventional agrochemicals. It serves farmers, agribusinesses, and environmental stakeholders with innovative and eco-friendly solutions.

-

In 2024, Terramera Inc. advanced its AI-driven agricultural platform to enhance crop protection efficiency and support regenerative farming practices globally.

Regenerative Agriculture Companies are:

-

Vayda

-

Agreed.Earth

-

Biotrex

-

Ecorobotix SA

-

Ruumi

-

Continuum Ag

-

Indigo Ag, Inc.

-

Tortuga Agricultural Technologies, Inc.

-

Astanor Ventures

-

SATELLIGENCE

-

Nestlé S.A.

-

Danone S.A.

-

General Mills, Inc.

-

Cargill Incorporated

-

Unilever PLC

-

Grounded

-

Soil Capital Belgium SPRL

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.83 Billion |

| Market Size by 2035 | USD 37.44 Billion |

| CAGR | CAGR of 14.30% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Type (Agroforestry, Silvopasture, Aquaculture) • By End-User (Farmers, Service Organizations, Financial Institutions, Advisory Bodies) • By Application (Carbon Sequestration, Soil Health Improvement, Water Management) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Vayda, Terramera Inc., Agreed.Earth, Biotrex, Ecorobotix SA, Ruumi, Continuum Ag, Aker Technologies, Inc., Indigo Ag, Inc., Tortuga Agricultural Technologies, Inc., Astanor Ventures, SATELLIGENCE, Nestle SA, Danone SA, General Mills, Inc, Cargill Incorporated, Unilever PLC, Grounded, Soil Capital Belgium SPRL. |

Frequently Asked Questions

The Regenerative Agriculture Market is expected to grow at a CAGR of 14.3% during 2026–2035.

The Regenerative Agriculture Market size was valued at USD 9.83 Billion in 2025 and is projected to reach USD 37.44 Billion by 2035.

The key drivers of the Regenerative Agriculture Market include rising demand for sustainable and organic food, increasing focus on soil health and carbon sequestration, supportive government policies, and corporate sustainability initiatives.

The Solutions segment dominated during the projected period.

North America dominated the Regenerative Agriculture Market in 2025.

Get in Touch