Semiconductor Capital Equipment Market Size Analysis:

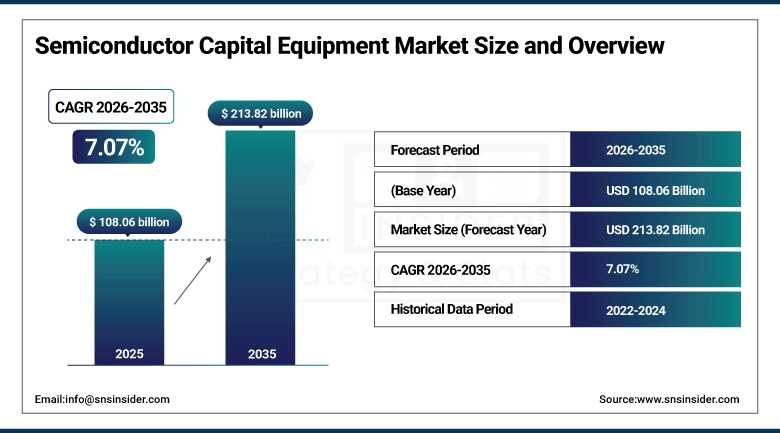

The Semiconductor Capital Equipment Market size was valued at USD 108.06 Billion in 2025 and is projected to reach USD 213.82 Billion by 2035, growing at a CAGR of 7.07% during 2026–2035.

The semiconductor capital equipment market is experiencing robust growth spurts due to rapid demand for advanced chips utilized in AI, high-performance computing, and data center hardware infrastructure. Emerging applications with artificial intelligence requirement are driving the demand for advanced manufacturing equipment like EUV lithography, etching, deposition, inspection, and advanced packaging systems. Further scaling towards sub-5nm and angstrom-level process technologies is driving even greater device complexity and capital equipment investments. Moreover, increasing fab expansion globally, over Asia-Pacific and North America, also boost equipment demand in the long run. At the same time, limited availability for supplies and equipment are still major impediments, but automation is continuously maturing, with AI-enabled manufacturing increasing production efficiency across the sector.

In March 2026, ASML was positively impacted by SK Hynix announcement of a USD 8 billion capacity investment into next-generation memory chip production to be partially realized using advanced EUV lithography systems by 2027 providing ASML with visibility of ongoing strong demand from the semiconductor sector driven by AI expansion.

Market Size and Growth:

-

Market Size in 2025: USD 108.06 Billion

-

Market Size by 2035: USD 213.82 Billion

-

CAGR: 7.07% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Semiconductor Capital Equipment Market - Request Free Sample Report

Semiconductor Capital Equipment Market Trends Highlights:

-

Strong demand growth driven by AI, HPC, and advanced node (sub-5nm and angstrom-scale) chip manufacturing.

-

EUV and High-NA lithography systems remain critical enablers for next-generation semiconductor fabrication.

-

Rising complexity of chip design is increasing need for etch, deposition, and advanced inspection equipment.

-

Advanced packaging (3D stacking, HBM integration) is becoming a major equipment growth segment.

-

Global fab expansion in Asia-Pacific (Taiwan, South Korea, China) is boosting capital equipment investments.

-

Industry faces constraints from supply chain bottlenecks and limited skilled engineering workforce.

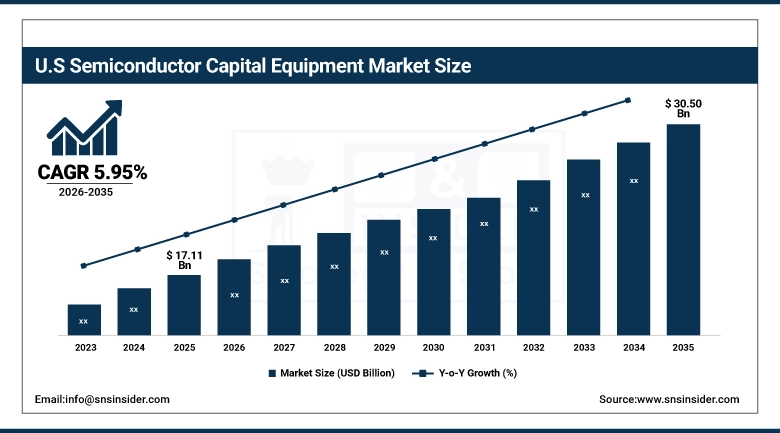

U.S. Semiconductor Capital Equipment Market Size Outlook:

The U.S. Semiconductor Capital Equipment Market size was valued at USD 17.11 Billion in 2025 and is projected to reach USD 30.50 Billion by 2035, growing at a CAGR of 5.95% during 2026–2035, attributed to a solid governmental support by enabling acts as the CHIPS Act that resulted in stimulating the domestic semiconductor manufacturing and - supplying chain dependency. However, an increase in advanced nodes, AI, high-performance computing, and 5G investments continue to drive up equipment demand. Furthermore, the growing number of top foundries, rising research & development (R&D) operations, increasing adoption of next-generation lithography and process technologies are also fuelling market growth across the country during the forecast period.

Market Drivers: AI-Driven Lithography Optimization Boosts Semiconductor Manufacturing Efficiency

AI-powered accelerated computing is pulling a massive change in computational lithography, the most advanced and resource-heavy phase of semiconductor manufacturing. According to the study, the increasing demand for advanced nodes such as high-NA extreme ultraviolet (EUV) and angstrom-scale chips has caused the cost and energy consumption in chip fabrication workflows to push past traditional computing constraints. Combining AI-based surrogate models with high-performance computing platforms, like NVIDIA cuLitho for enhanced semiconductor process simulation performance and accuracy accomplishes orders of magnitude simulations cycles faster and high-fidelity process description. By having this shift, it increases both EUV, and also the capability of next-gen lithography, therefore directly assisting in modular scalability and productivity in the semiconductor capital equipment ecosystems.

Research submitted on January 27, 2026 shows that AI combined with accelerated computing is transforming computational lithography, the most complex stage of semiconductor manufacturing, by significantly reducing compute time and energy use.The study reports up to 57× faster simulation performance, improving process accuracy and enabling advanced semiconductor capital equipment capabilities for high-NA EUV and angstrom-scale chip production.

Market Restraints: Equipment Bottlenecks and Talent Shortage Slow Semiconductor Capital Expansion

A key restraint in the semiconductor capital equipment market is the growing imbalance between surging AI-driven chips and a global shortage of advanced manufacturing tools and specialists. Shortages of key semiconductor processing technology namely EUV lithography systems, deposition, etching and inspection systems are holding back scale-up at semiconductor fabs. Also, the talent bandwidth for process engineering and fab operations are constraining new production line deployment. These challenges are compounded by geopolitical restrictions and concentration of supply chains that constrained the transfer of technology and critical equipment. All these factors combined are limiting how fast semiconductor manufacturing capacity cells can be expanded globally.

Market Opportunities: AI Supply Shock Reshapes Global Demand for Semiconductor Capital Equipment

Severe shortages of wafer fabrication capacity in lithography, etching, deposition, and inspection equipment elements are driven by a surge in chip demands from upcoming AI adoption. Now, these industry bottlenecks are moving not just down from chip design but to manufacturing tools with limited supply throttling fab expansion worldwide. Meanwhile, advanced packaging and high-bandwidth memory manufacturing process steps have become new supply constraints, increasing the need for capital investment. Such a backdrop is resulting in resilient long-term demand for next-generation semiconductor capital equipment, especially in AI server supply chains and advanced node manufacturing ecosystems.

Chinese semiconductor industry leaders stated at SEMICON China 2026 that China is still 5–10 years behind in AI data center chips, while rapid AI demand is creating severe bottlenecks in semiconductor manufacturing equipment, talent availability, and supply chain capacity.

Semiconductor Capital Equipment Market Segment Highlights:

-

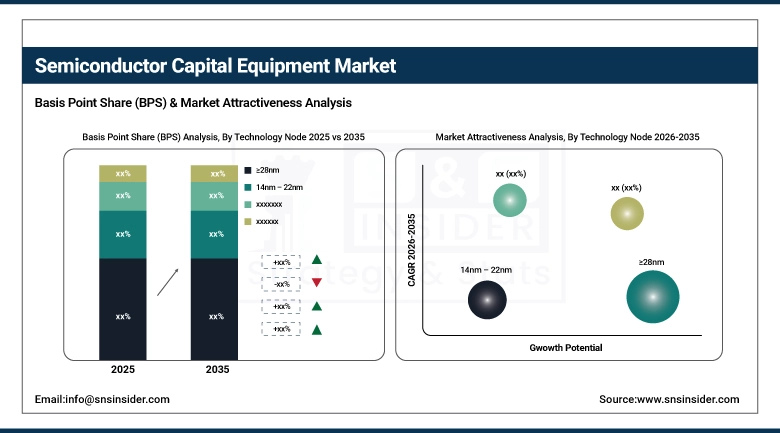

By Technology Node: Dominant – ≥28nm (33.50% in 2025 → 21.50% in 2035); Fastest Growing – 3nm and below (11.50% in 2025 → 23.50% in 2035)

-

By Wafer Size: Dominant – 300mm (39.00% in 2025 → 31.00% in 2035); Fastest Growing – ≥450mm (5.50% in 2025 → 9.50% in 2035)

-

By Distribution Channel: Dominant – Direct Sales (54.50% in 2025 → 50.50% in 2035); Fastest Growing – Distributors/VARs (20.30% in 2025 → 22.70% in 2035)

-

By Application: Dominant – Logic IC Manufacturing (30.40% in 2025 → 33.60% in 2035); Fastest Growing – Logic IC Manufacturing (strongest growth from 30.40% in 2025 → 33.60% in 2035)

By Technology Node ≥28nm (Dominant) and 3nm and below (Fastest-Growing)

The ≥28nm technology node segment holds the dominant share due to its widespread adoption in legacy semiconductor manufacturing, cost efficiency, and extensive use across mature applications such as industrial electronics and consumer devices. Its established fabrication ecosystem and high production stability continue to support strong market presence. Conversely, the 3nm and below segment is witnessing the fastest growth due to increasing demand for ultra-high-performance computing, advanced AI processors, and next-generation mobile chipsets. Continuous innovation in miniaturization, enhanced energy efficiency, and superior processing power is driving rapid adoption of leading-edge nodes in advanced semiconductor manufacturing.

By Wafer Size (Dominant – 300mm; Fastest-Growing – ≥450mm)

The 300mm wafer size segment holds the dominant share due to its widespread adoption in high-volume semiconductor manufacturing, optimized cost efficiency per chip, and strong integration across advanced fabrication facilities worldwide. Its mature ecosystem and proven scalability continue to make it the industry standard for mainstream production. In contrast, the ≥450mm wafer size segment is emerging as the fastest-growing category, driven by the need for higher productivity, reduced cost per die, and improved manufacturing efficiency in next-generation semiconductor fabs, despite its early-stage adoption and high infrastructure requirements.

By Distribution Channel (Dominant – Direct Sales; Fastest-Growing – Distributors/VARs)

The Direct Sales segment dominates the market due to strong manufacturer–client relationships, better pricing control, and customized supply agreements with large semiconductor foundries and integrated device manufacturers. This channel ensures streamlined procurement and technical alignment for high-value semiconductor equipment. Meanwhile, the Distributors/VARs segment is witnessing the fastest growth as smaller fabs and emerging electronics companies increasingly rely on third-party intermediaries for flexible sourcing, faster delivery cycles, and expanded access to diverse product portfolios.

By Application (Dominant & Fastest-Growing – Logic IC Manufacturing)

Logic IC manufacturing remains both the dominant and fastest-growing application segment, supported by rising demand for advanced processors used in AI computing, data centers, smartphones, and high-performance computing systems. Continuous advancements in chip design complexity and the shift toward smaller technology nodes are further accelerating the need for logic-based integrated circuits, reinforcing their central role in next-generation semiconductor innovation and global digital transformation.

Semiconductor Capital Equipment Market Regional Highlights:

-

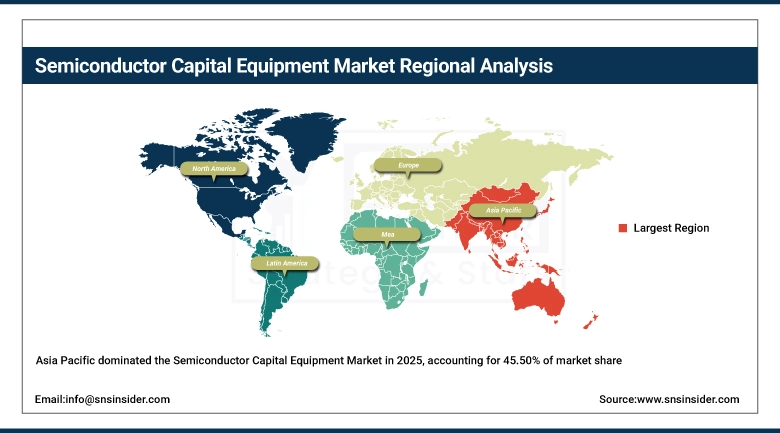

Asia-Pacific: 45.50% (2025) → 49.50% (2035), Fastest-Growing and Dominant Region driven by massive semiconductor manufacturing capacity, strong electronics production base, and heavy investments in China, Taiwan, South Korea, and Japan, supporting large-scale adoption of semiconductor capital equipment (CAGR 7.97%)

-

North America: 23.90% (2025) → 23.10% (2035), Mature Growth Region with strong semiconductor ecosystem, advanced R&D capabilities, and high adoption across AI, data centers, and advanced manufacturing applications (CAGR 6.70%)

-

Europe: 17.90% (2025) → 17.10% (2035), Stable Growth Region supported by automotive semiconductor demand, industrial automation, EU Chips Act initiatives, and precision engineering capabilities (CAGR 6.58%)

-

South America: 5.90% (2025) → 5.10% (2035), Emerging Region with gradual growth driven by electronics assembly expansion, limited fabrication base, and rising foreign investments in manufacturing hubs (CAGR 5.51%)

-

Middle East & Africa: 6.80% (2025) → 5.20% (2035), Developing Region driven by digital infrastructure expansion, diversification initiatives, and early-stage investments in advanced semiconductor-related technologies (CAGR 4.20%)

Asia-Pacific Semiconductor Capital Equipment Market Insights:

The Asia-Pacific Semiconductor Capital Equipment Market is driven by rapid expansion of semiconductor fabrication facilities, increasing government investments in chip manufacturing, and strong demand from consumer electronics, automotive, and 5G applications. Countries like China, Taiwan, South Korea, and Japan dominate production capacity, supported by advanced foundries and OSAT facilities. Rising adoption of AI, IoT, and electric vehicles further accelerates equipment demand, while ongoing localization strategies and supply chain resilience initiatives strengthen regional market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Semiconductor Capital Equipment Market Insights:

The China Semiconductor Capital Equipment Industry is driven by the significant governmental support for semiconductor fabs, the ambition of obtaining autonomy on chip supplies and increasing investment in fabs in the country. Local equipment manufacturers are also ramping up quickly due to increasing restrictions on imports.

North America Semiconductor Capital Equipment Market Insights:

The North America Semiconductor Capital Equipment Market is driven by strong R&D leadership, advanced semiconductor design capabilities, and significant investments under initiatives like the CHIPS and Science Act. The region hosts major players in equipment innovation, automation, and advanced lithography support systems. Growing demand for AI chips, data centers, and high-performance computing is accelerating equipment deployment. Additionally, reshoring of semiconductor manufacturing, expansion of fabs in the U.S., and strong collaboration between government and industry are further strengthening market growth across the region.

United States Semiconductor Capital Equipment Market Insights:

The United States Semiconductor Capital Equipment Industry is driven by CHIPS Act funding, rising domestic fab construction, and strong demand for AI chips, data centers, and advanced semiconductor manufacturing technologies.

Europe Semiconductor Capital Equipment Market Insights:

The Europe Semiconductor Capital Equipment Market has been increasing from higher investment in high tech chip production, another driver is the increasing automotive and industrial semiconductors and the European Union push with a European Chips Act. Increasing penetration of EVs, renewable energy systems, and high-performance electronics is fuelling the uptake of equipment. It is also enhancing domestic fabrication capabilities and minimizing reliance on external suppliers by means of strategic partnerships and technology development initiatives.

Germany Semiconductor Capital Equipment Market Insights:

The demand for automotive semiconductors, growth in industrial automation, and the investments in chip manufacturing supported by the EU are factors that are expected to drive the Germany Semiconductor Capital Equipment Industry. The ramp-up of local fabs and R&D facilities is also enhancing the adoption of the equipment and further development of the technology.

Latin America Semiconductor Capital Equipment Market Insights:

The Latin America Semiconductor Capital Equipment Market is driven by growing electronics manufacturing, increasing foreign investments, and rising demand for consumer devices and automotive electronics. Countries like Brazil and Mexico are emerging as key hubs for assembly, testing, and packaging activities. Expansion of industrial automation, digital transformation, and supply chain diversification by global semiconductor firms is further supporting market growth. However, limited fabrication infrastructure and high dependency on imports continue to restrict large-scale equipment deployment in the region.

Brazil Semiconductor Capital Equipment Market Insights:

The demand for automotive semiconductors, growth in industrial automation, and the investments in chip manufacturing supported by the EU are factors that are expected to drive the Germany Semiconductor Capital Equipment Industry. The ramp-up of local fabs and R&D facilities is also enhancing the adoption of the equipment and further development of the technology.

Middle East & Africa (MEA) Semiconductor Capital Equipment Market Insights:

The Middle East & Africa Semiconductor Capital Equipment Market is driven by increasing investments in digital infrastructure, diversification into high-tech manufacturing, and government-led initiatives to develop semiconductor and electronics industries. Countries like the UAE, Saudi Arabia, and Israel are focusing on advanced technology ecosystems, including AI, data centers, and smart manufacturing. Rising demand for consumer electronics, automotive electronics, and telecom infrastructure is further boosting equipment adoption. However, limited fabrication capacity and reliance on imports continue to challenge large-scale market expansion in the region.

Israel Semiconductor Capital Equipment Market Insights:

Israel leads the region in semiconductor design, R&D, and advanced chip innovation, supported by a strong high-tech ecosystem. The UAE is rapidly emerging as a key hub driven by investments in AI, data centers, and advanced digital infrastructure, while Saudi Arabia is expanding its semiconductor presence through Vision 2030 initiatives focused on manufacturing, electronics, and smart industry development. Together, these countries are shaping the region’s semiconductor growth landscape.

Semiconductor Capital Equipment Market Competitive Landscape:

ASML is a semiconductor equipment manufacturer. The company is a world leader in advanced lithography systems, including its state-of-the art EUV and High-NA EUV technologies for manufacturing leading-edge logic and memory chips at leading-edge node of 3nm and below.

-

On March 2026, ASML stock was highlighted as a “top pick” citing strong demand from DRAM and memory-chip makers upgrading semiconductor equipment. The outlook reflects continued strength in lithography demand driven by AI and advanced memory production in the ASML ecosystem.

Lam Research is a semiconductor equipment company established in 1980 and headquartered in the United States. It specializes in wafer fabrication equipment, particularly etch and deposition systems used in advanced logic, memory, and AI chip manufacturing. The company supports semiconductor scaling at advanced nodes, enabling high-performance computing and next-generation electronic device production.

-

On October 2025, Lam Research forecast upbeat second-quarter revenue above Wall Street estimates, driven by strong demand for chipmaking tools used in AI semiconductor production. The company reported increased orders for etch and deposition equipment, reflecting rising investments from chipmakers expanding advanced logic and AI-driven manufacturing capacity.

Semiconductor Capital Equipment Companies are:

-

ASML

-

Lam Research

-

Tokyo Electron

-

KLA Corporation

-

Advantest

-

Teradyne

-

ASM International

-

Hitachi High-Tech Corporation

-

Canon Inc.

-

Nikon Corporation

-

DISCO Corporation

-

Lasertec Corporation

-

Axcelis Technologies

-

Onto Innovation

-

Kokusai Electric

-

NAURA Technology Group

-

Advanced Micro-Fabrication Equipment Inc. (AMEC)

-

ACM Research

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 108.06 Billion |

| Market Size by 2035 | USD 213.82 Billion |

| CAGR | CAGR of 7.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology Node(≥28nm, 14nm – 22nm,7nm – 10nm, 5nm and 3nm and below) • By Wafer Size(150 mm, 200 mm, 300 mm, 300 mm and 450 mm and ≥450 mm) • By Distribution Channel(Direct Sales, System Integrators and Distributors/VARs) • By Application(Logic IC Manufacturing, Memory (DRAM, NAND) Manufacturing, Foundry Operations, Integrated Device Manufacturers (IDMs) and Outsourced Semiconductor Assembly and Testing (OSAT)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ASML, Applied Materials, Lam Research, Tokyo Electron, KLA Corporation, SCREEN Holdings, Advantest, Teradyne, ASM International, Hitachi High-Tech Corporation, Canon Inc., Nikon Corporation, DISCO Corporation, Lasertec Corporation, Axcelis Technologies, Onto Innovation, Kokusai Electric, NAURA Technology Group, Advanced Micro-Fabrication Equipment Inc. (AMEC), ACM Research. |

Frequently Asked Questions

Asia-Pacific dominated the Semiconductor Capital Equipment Market in 2025.

The “≥28nm” segment dominated during the projected period.

Key drivers of the Semiconductor Capital Equipment market include growing demand for advanced semiconductor devices, miniaturization of electronic components, increasing adoption of EUV lithography, expansion of nanotechnology applications in healthcare and energy, and rising investments in next-generation chip manufacturing.

The Semiconductor Capital Equipment market size was USD 108.06 Billion in 2025 and is expected to reach USD 213.82 Billion by 2035.

The Semiconductor Capital Equipment market is expected to grow at a CAGR of 7.07% from 2026-2035

Get in Touch