Semiconductor IP Market Report Scope & Overview:

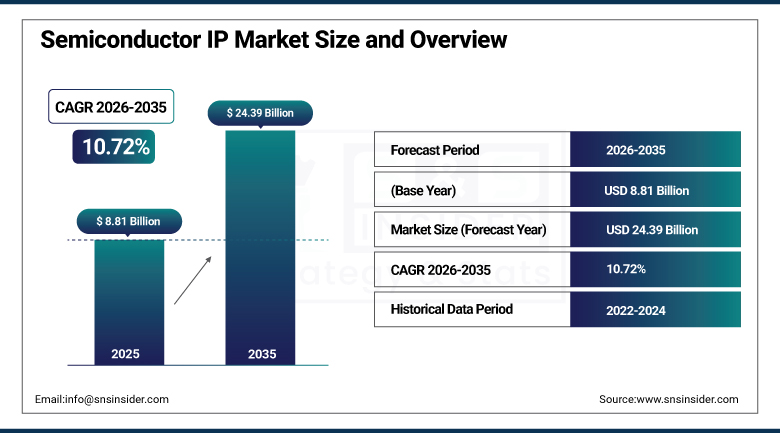

The Semiconductor IP Market size was valued at USD 8.81 Billion in 2025 and is expected to reach USD 24.39 Billion by 2035, growing at a CAGR of 10.72% from 2026 to 2035.

The Semiconductor Intellectual Property Market continues to expand as escalating design complexity across artificial intelligence, 5G, and Internet of Things applications pushes chipmakers to rely more heavily on third-party intellectual property rather than developing every functional block in-house. Vendors offering turnkey subsystems that bundle processor, radio frequency, and secure-element intellectual property continue capturing design wins because they let original equipment manufacturers integrate advanced connectivity without expanding their internal engineering teams. Competitive intensity within processor intellectual property has increased considerably due to the entry of RISC-V entrants, prompting incumbent vendors to widen their differentiation through integrated AI acceleration and power management enhancements built directly into licensable cores.

Synopsys completed its acquisition of Ansys in 2024 in a transaction valued at approximately thirty-five billion dollars, combining Synopsys' semiconductor design and intellectual property portfolio with Ansys' simulation software to create a more comprehensive design-to-silicon platform for chipmakers navigating increasingly complex system-on-chip development.

Market Size and Forecast

-

Market Size in 2026E: USD 9.75 Billion

-

Market Size by 2035: USD 24.39 Billion

-

CAGR: 10.72% from 2026 to 2035

-

Fastest Growing Region: South America

-

Largest Region: Asia Pacific

To Get more information On Semiconductor IP Market - Request Free Sample Report

Semiconductor IP Market Trends

-

RISC-V entrants are intensifying competition within processor IP, prompting incumbents to widen differentiation through integrated AI acceleration.

-

Record shipments of smart meters, wearables, and asset-tracking tags are driving surging demand for low-power processor and sensor-hub IP.

-

Edge architectures are increasingly favoring domain-specific blocks that execute real-time inference close to the data source.

-

Vendors bundling processor, RF, and secure-element IP into turnkey subsystems are capturing design wins from OEMs seeking faster integration.

-

Expanding 5G infrastructure and WiFi 7 adoption are propelling wireless interface IP demand at a pace outstripping processor IP growth.

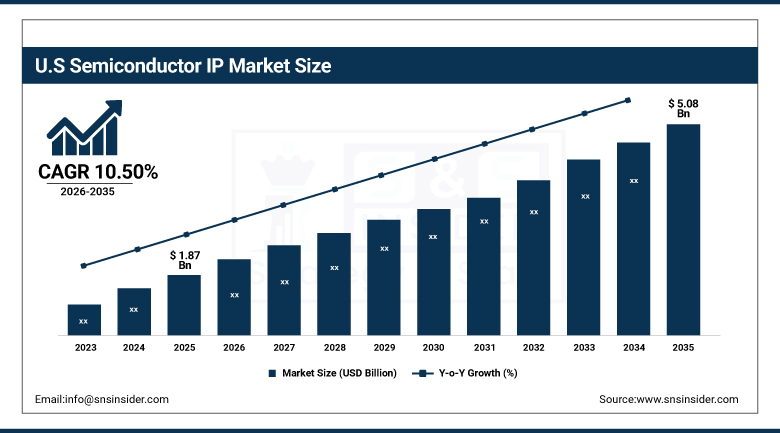

United States Semiconductor IP Market Size Outlook

The United States Semiconductor IP Market was valued at USD 1.87 Billion in 2025 and is expected to reach USD 5.08 Billion by 2035, growing at a CAGR of 10.50% from 2026 to 2035.

The United States maintained a leading position in North American semiconductor intellectual property demand, supported by a concentrated base of leading IP core developers and sustained enterprise investment in advanced system-on-chip design. Continued growth in AI accelerator and high-performance computing chip design, combined with rising RISC-V ecosystem adoption among domestic fabless semiconductor companies, kept the country among the more commercially significant national markets for this technology throughout the year.

SiFive, headquartered in San Mateo, California, continued strengthening its position as a leading developer of licensable RISC-V processor core intellectual property, supporting fabless semiconductor companies designing custom silicon for AI, automotive, and data center applications without dependence on proprietary instruction set architectures.

Semiconductor IP Market Segment Analysis

-

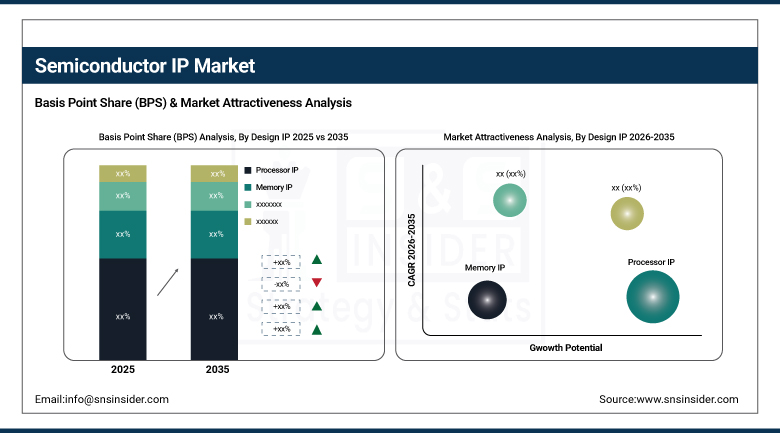

By Design IP, the Processor IP segment held approximately 45.88% share in 2025, while the Interface IP segment is the fastest growing, with a CAGR of approximately 7.05%.

-

By IP Core, the Hard IP segment held the larger share in 2025, while the Soft IP segment is the fastest growing, with a CAGR of approximately 15.90%.

-

By IP Source, the Royalty segment held the larger share in 2025, while the Licensing segment is the fastest growing.

-

By End User, the Consumer Electronics segment held the larger share in 2025, while the Automotive segment is the fastest growing.

By Design IP, Processor IP led the market, Interface IP grew fastest

The Processor IP sub-segment emerged as the leader in the design IP market share in 2025, capturing approximately 45.88% of the market share owing to the essential inclusion of CPU cores in practically all of the systems on chips developed today. The basic necessity of processing capabilities in any chip makes the Processor IP the top sub-segment of the design IP segmentation.

The Interface IP sub-segment including wireless interface technology is expected to show the highest CAGR growth of around 7.05% over the forecast period due to increasing 5G networks, Wi-Fi 7, and Bluetooth LE Audio developments. With semiconductor companies developing multiple standard radios requiring pre-made radio frequency, baseband, and coexistence logic capable of meeting certification standards throughout the world, interface IP is leading in terms of growth compared to the design IP segmentation.

By IP Core, Hard IP led the market, Soft IP grew fastest

The Hard IP sector has been dominant in terms of IP cores in 2025 owing to its optimized performance and power efficiency made possible through the physical layer, silicon-specific designs that cannot be achieved using soft IP. The performance of such IP cores makes them more favorable for high volume performance-oriented applications where power and area optimization make the difference.

The Soft IP segment is expected to register the highest CAGR of about 15.90% over the forecast period due to its flexible and customizable nature as a synthesizable register transfer level code that semiconductor companies can customize to suit their needs. Such flexibility will be more beneficial to organizations manufacturing custom chips for Internet of Things, Artificial Intelligence, and automotive devices where the functionality of the device is more important than power optimization.

By IP Source, Royalty led the market, Licensing grew fastest

The Royalty segment held the larger IP source share in 2025, reflecting the established industry practice of per-unit royalty payments tied to actual chip shipment volumes rather than upfront licensing fees alone. That volume-based revenue model continues keeping royalty arrangements the dominant IP source structure across the majority of high-volume consumer electronics and mobile device semiconductor programs.

The Licensing segment is projected to grow at the fastest CAGR during the forecast period, as more fabless semiconductor companies and startups prefer predictable upfront licensing costs over variable, volume-dependent royalty structures during early-stage product development. That preference for cost predictability continues pushing licensing arrangements ahead of the broader IP source segmentation, particularly among smaller design teams with constrained development budgets.

By End User, Consumer Electronics led the market, Automotive grew fastest

The Consumer Electronics segment held the larger end user share in 2025, anchored by sustained global demand for smartphones, wearables, and connected devices that all depend on licensed semiconductor IP for their core processing and connectivity functions. That broad-based, sustained consumer demand keeps this end-user category firmly at the center of overall semiconductor IP consumption across nearly every major semiconductor market worldwide.

The Automotive segment is projected to grow at the fastest CAGR during the forecast period, driven by rising semiconductor content per vehicle across advanced driver-assistance systems, infotainment, and electric vehicle powertrain electronics. Continued vehicle electrification and growing semiconductor complexity per vehicle continue pushing automotive end-user demand ahead of the broader end-user segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

38.80% |

|

North America |

United States |

86.40% |

|

Europe |

Germany |

27.20% |

|

Middle East & Africa |

UAE |

26.90% |

|

Latin America |

Brazil |

37.40% |

Asia Pacific Semiconductor IP Market Insights

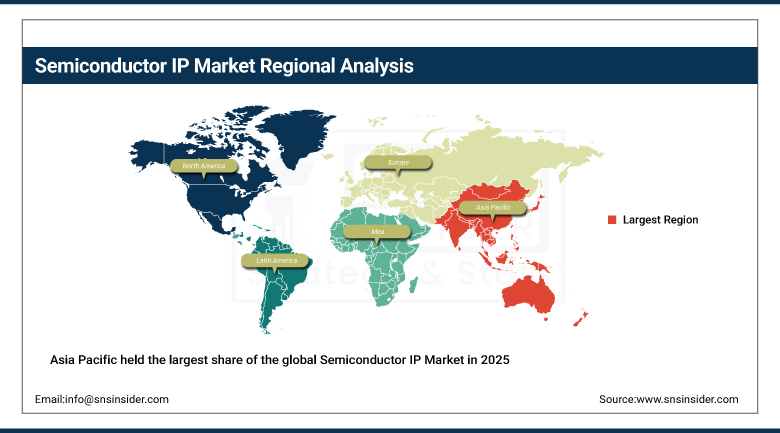

Asia Pacific held the largest share of the global Semiconductor IP Market in 2025, at approximately 52.14%, anchored by the region's overwhelming concentration of semiconductor design and fabrication capacity across China, Taiwan, South Korea, and Japan. That manufacturing and design depth continues keeping Asia Pacific firmly ahead of every other region in overall semiconductor IP licensing and consumption.

China accounted for roughly 38.80% of regional revenue, supported by aggressive domestic semiconductor policy and expanding fabless chip design activity. Taiwan, South Korea, and Japan contributed significant additional regional demand through their own advanced semiconductor manufacturing and design ecosystems, reinforcing Asia Pacific's position as the clear global center of semiconductor IP consumption.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Semiconductor IP Market Insights

North America held a substantial share of the global Semiconductor IP Market in 2025, supported by the region's concentration of leading IP core developers and sustained enterprise investment in AI accelerator and high-performance computing chip design. Continued domestic semiconductor research investment kept the region among the more commercially significant markets for this technology throughout the year.

The United States accounted for roughly 86.40% of regional revenue, reflecting its dense concentration of leading semiconductor IP developers and downstream fabless chip design customers. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding semiconductor design ecosystem, keeping North America among the most commercially significant regional markets for semiconductor IP throughout the year.

Europe Semiconductor IP Market Insights

Europe has been one of the major market participants in the Global Semiconductor IP Market in 2025, driven by robust automotive semiconductor design activities and rising industrial IoT applications in Europe. Germany has a share of around 27.20% in the region due to its presence of numerous automotive and semiconductor companies designing semiconductor IP in their vehicles.

The trend was similar in France, the UK, and the Netherlands due to increasing investments in automotive electrification and industrial automation which would lead to increased adoption of semiconductor IP in Europe. Increasing use of automotive semiconductor will continue to drive European demand for the remaining period of forecast.

MEA & Latin America Semiconductor IP Market Insights

The Middle East and Africa region recorded steady growth in semiconductor IP adoption in 2025, driven by expanding domestic semiconductor design initiatives and growing technology sector investment across the Gulf states in particular. The UAE accounted for roughly 26.90% of regional revenue, supported by national technology diversification strategies and rising enterprise interest in domestic chip design capability.

Latin America, and South America specifically, was projected to register the highest regional CAGR through the forecast period, led by Brazil at roughly 37.40% of regional revenue, where growing domestic electronics design activity continued to support category growth. Mexico and Argentina followed a similar trajectory as regional semiconductor design ecosystem investment expanded further through the remainder of the forecast period.

Market Dynamics

Growth Drivers: Rising SoC complexity and RISC-V ecosystem expansion

The increasing complexity of semiconductor designs, driven by the continued evolution of artificial intelligence, 5G, and Internet of Things technologies, continues to be the central force behind semiconductor IP market growth. These devices require highly specialized, high-performance IP cores to meet escalating requirements for faster processing, lower power consumption, and enhanced functionality that in-house development alone cannot economically deliver.

The decline in chip design costs and advancements in multicore technology continue supporting broader semiconductor IP adoption across consumer electronics, automotive, and telecommunications sectors. Growing entry of RISC-V entrants into the processor IP landscape continues intensifying competition and accelerating innovation, while rising outsourcing of semiconductor design activities keeps reinforcing structural demand for licensable, pre-validated IP cores across nearly every major chip design program worldwide.

Restraints: Technological expenditure and IP security concerns

The continuing evolution of technology and consequent increases in the amount of R&D spending pose a real challenge to the growth of the semiconductor IP market, as IP providers have to consistently enhance their IP offering in order to stay ahead of the fast-moving process node requirements. Such an ongoing commitment may have some serious implications for small-scale IP providers who do not have the financial means to compete with well-known and big players.

IP security and protection issues remain a consistent hindrance to growth, as the licensed IP is always at risk of being used without authorization or even reverse engineered after it is incorporated into the customer design.

Opportunities: Edge AI acceleration and turnkey subsystem bundling

Growing demand for domain-specific blocks that execute real-time inference close to the data source presents substantial opportunity for IP vendors positioned to serve the expanding edge AI application category. Vendors capable of delivering low-latency, power-efficient inference IP stand to capture a growing share of demand as edge architectures continue proliferating across industrial and consumer applications.

Rising vendor success bundling processor, radio frequency, and secure-element IP into turnkey subsystems presents a further significant growth avenue, as original equipment manufacturers increasingly favor integrated solutions that let them launch connected devices without expanding internal engineering teams. IP vendors capable of delivering these comprehensive, certification-ready subsystems stand to capture meaningful new revenue streams as this bundling trend continues through 2035.

Recent Developments:

-

2025: Arm Holdings continued expanding its Neoverse server-class processor IP portfolio, targeting data center and AI infrastructure customers seeking energy-efficient alternatives to traditional x86 architecture for large-scale computing deployments.

-

2024: CEVA continued advancing its wireless connectivity and sensor fusion IP portfolio, strengthening its position serving IoT and wearable device manufacturers requiring low-power, integrated connectivity solutions.

-

2025: Imagination Technologies continued expanding its graphics processing unit IP licensing business, targeting automotive and mobile device manufacturers requiring efficient, high-performance graphics rendering capability for advanced infotainment and display applications.

Semiconductor IP Companies are:

-

Synopsys, Inc.

-

Cadence Design Systems, Inc.

-

CEVA, Inc.

-

Imagination Technologies Limited

-

SiFive, Inc.

-

Alphawave IP Group plc

-

eMemory Technology Inc.

-

Andes Technology Corporation

-

VeriSilicon Holdings Co., Ltd.

-

Faraday Technology Corporation

-

Lattice Semiconductor Corporation

-

Achronix Semiconductor Corporation

-

Silvaco Group, Inc.

-

Codasip GmbH

-

MIPS Technologies, Inc.

-

Efinix, Inc.

-

Siemens EDA

-

Ansys, Inc.

Semiconductor IP Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.81 Billion |

| Market Size by 2035 | USD 24.39 Billion |

| CAGR | CAGR of 10.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Design IP (Processor IP, Memory IP, Interface IP) • by IP Core (Hard IP, Soft IP) • by IP Source (Royalty, Licensing) • by End User (Consumer Electronics, Automotive, Telecommunications) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Arm Holdings plc, Synopsys, Inc., Cadence Design Systems, Inc., CEVA, Inc., Imagination Technologies Limited, SiFive, Inc., Rambus Inc., Alphawave IP Group plc, eMemory Technology Inc., Andes Technology Corporation, VeriSilicon Holdings Co., Ltd., Faraday Technology Corporation, Lattice Semiconductor Corporation, Achronix Semiconductor Corporationl, Silvaco Group, Inc., Codasip GmbH, MIPS Technologies, Inc., Efinix, Inc., Siemens EDA, Ansys, Inc. |

Frequently Asked Questions

The Semiconductor Intellectual Property (IP) Market is expected to grow at a CAGR of 10.72% from 2026 to 2035.

The Semiconductor Intellectual Property (IP) Market was valued at USD 8.81 Billion in 2025.

Rising semiconductor design complexity across AI, 5G, and IoT applications combined with expanding RISC-V ecosystem adoption is the major growth factor.

The Processor IP segment held approximately 45.88% share in 2025.

Asia Pacific held the largest share of the Semiconductor Intellectual Property (IP) Market in 2025, at approximately 52.14%, while South America was projected to register the fastest CAGR.

Get in Touch