Strategic Petroleum Reserve Market Report Scope & Overview:

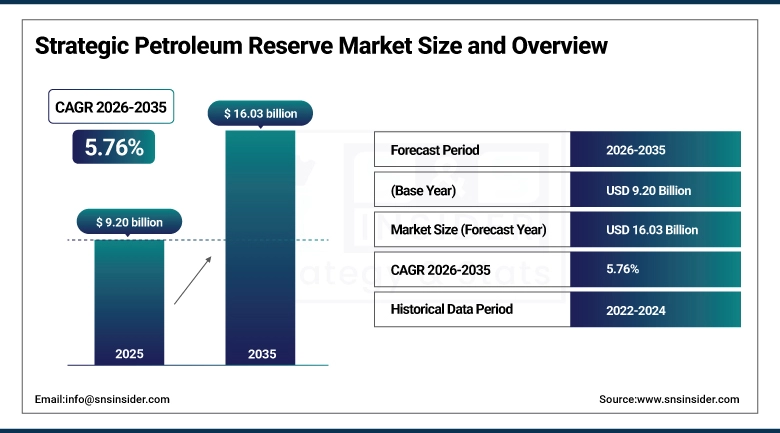

The Strategic Petroleum Reserve Market size was valued at USD 9.20 Billion in 2025 and is projected to reach USD 16.03 Billion by 2035, growing at a CAGR of 5.76% during 2026–2035.

Strategic petroleum reserves exist because oil supply interruptions from geopolitical conflict, natural disasters, infrastructure sabotage, or cartel production decisions move through an economy faster than any other commodity disruption. Governments have maintained emergency petroleum stockpiles since the 1973 oil embargo demonstrated what a sustained supply cut actually costs.

Strategic Petroleum Reserve Market Size and Growth Forecast:

-

Market Size in 2025: USD 9.20 Billion

-

Market Size by 2035: USD 16.03 Billion

-

CAGR: 5.76% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Strategic Petroleum Reserve Market - Request Free Sample Report

Key Strategic Petroleum Reserve Market Trends:

-

Asia Pacific governments particularly China, India, Japan, and South Korea are expanding strategic reserve capacity faster than any other region, driven by oil import dependence that makes supply disruption a macro-level economic risk rather than simply an energy sector problem.

-

The Middle East & Africa region is building petroleum reserve infrastructure at the fastest rate globally, as Gulf state governments recognize that domestic energy security and export market credibility both require demonstrated buffer capacity independent of real-time production.

-

Reserve composition is diversifying beyond crude oil into refined products, jet fuel, and in some programs biofuel blendstocks, reducing the refining bottleneck that has historically constrained how quickly emergency crude reserves can be converted into usable fuel supply.

-

Depleted oil field storage is gaining investment attention as a lower-cost alternative to purpose-built cavern and tank infrastructure, particularly in markets where former producing fields offer geological conditions suitable for large-volume petroleum containment.

-

International Energy Agency member country reserve sharing agreements are becoming more operationally active, with coordinated drawdown exercises and joint release decisions in response to supply events creating demand for reserve management services that cross national boundaries.

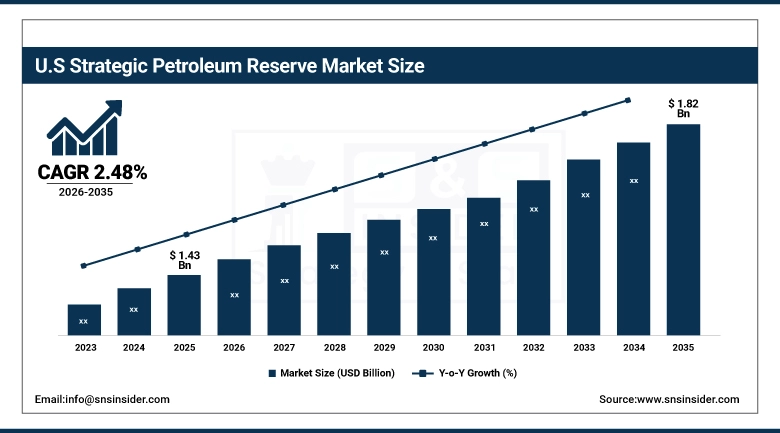

The U.S. Strategic Petroleum Reserve, the world's single largest emergency crude stockpile, was valued at USD 1.43 Billion in market terms in 2025 and is projected to reach USD 1.82 Billion by 2035, growing at a CAGR of 2.48%. The U.S. reserve, stored in salt cavern facilities along the Gulf Coast in Texas and Louisiana, has undergone significant drawdowns in recent years as policy instruments, creating a refill mandate that is driving infrastructure maintenance investment alongside the storage management procurement that constitutes the market's commercial layer.

Strategic Petroleum Reserve Market Growth Drivers:

-

Geopolitical Instability, Rising Import Dependence in Asia, and Government Energy Security Mandates Are Sustaining Capital Flows into Reserve Infrastructure Globally

The investment case for strategic petroleum reserves has not changed since the IEA established the 90-day reserve requirement in 1974 governments dependent on imported oil need a buffer between a supply disruption and the economic damage that disruption would cause hitting consumption directly. What has changed is the scale of economies now making that calculation. China became a net oil importer in 1993 and now imports roughly 70% of its consumption. India's import dependence runs above 80%. Both countries have responded by building reserve infrastructure at a pace their 2010-era capacity did not suggest was coming, and the Belt and Road-linked economies of Southeast Asia are at an earlier point in the same process. Each country that crosses from energy self-sufficiency to meaningful import dependence is a new entrant to the reserve infrastructure investment cycle a cycle that is not one-time, since facilities require maintenance, management, and expansion as economies grow.

Strategic Petroleum Reserve Market Restraints:

-

High Infrastructure Costs, Storage Geology Constraints, and the Policy Complexity of Reserve Management Across Changing Energy Transition Priorities Are Slowing Market Expansion

Building strategic petroleum storage is neither rapid nor low-cost. Salt cavern development for large-scale crude storage requires geological survey, solution mining, brine disposal management, and infrastructure connection that takes years from site selection to operational readiness. The energy transition creates a genuine policy tension: governments are simultaneously committing to reduced long-term petroleum consumption and maintaining or expanding short-term reserve capacity. The two are not necessarily contradictory transition periods are often when supply security matters most, because new energy infrastructure has not yet replaced the old but the political logic of investing in petroleum storage while publicly committing to its obsolescence requires careful management, and in markets where transition advocacy is politically dominant, reserve infrastructure investments face scrutiny that raises costs regardless of the underlying security rationale.

Strategic Petroleum Reserve Market Opportunities:

-

Depleted Field Conversion, Reserve Diversification into Refined Products, and Middle East Infrastructure Investment Are Creating Growth Pathways Beyond Conventional Crude Cavern Programs

Depleted oil and gas fields offer proven storage geology at lower development cost than purpose-built caverns, particularly in markets where salt formations are absent. Field conversion is within the existing oil field services sector's capability, giving programs a faster route to capacity than greenfield alternatives. The shift toward refined product reserves gasoline, diesel, and jet fuel held as immediately usable stocks addresses the operational limitation exposed during COVID, when refinery utilization constraints slowed how quickly crude drawdowns reached fuel consumers. Governments that experienced that gap are restructuring reserve specifications accordingly. The Middle East & Africa growth story reflects Gulf state governments building reserve systems that serve multiple purposes: domestic security, regional price stabilization influence, and the credibility signals that large reserve positions send to international buyers.

Strategic Petroleum Reserve Market Segment Analysis:

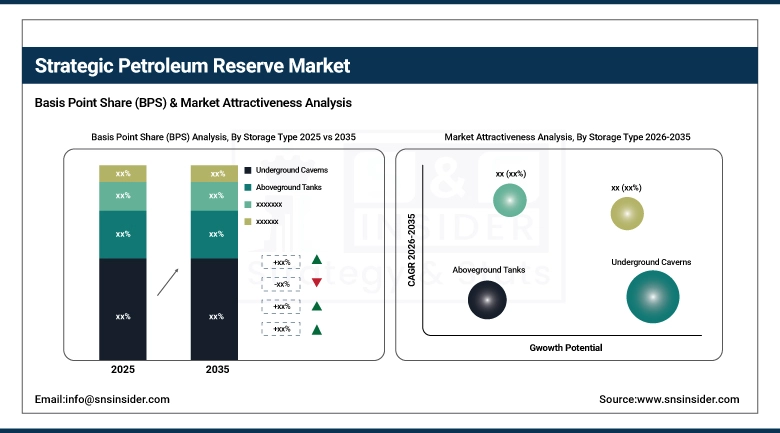

By Storage Type: Underground Caverns Lead While Depleted Oil Fields Drive Fastest Growth Through 2035

Underground Caverns dominated with a 36.24% share in 2025 at USD 3.33 Billion, while Depleted Oil Fields are expected to grow at the fastest CAGR of approximately 10.06% through 2035.

Underground cavern storage, particularly in salt formations, dominates because it offers the best combination of large-volume capacity, geological integrity over long storage periods, rapid drawdown capability, and cost per barrel of storage capacity at scale. The U.S. Strategic Petroleum Reserve's Gulf Coast salt cavern network is the design reference that most major national reserve programs have used as their engineering benchmark. Depleted oil field storage is growing fastest because the cost economics improve significantly as operators accumulate experience with field conversion projects and as the supply of available depleted fields increases with the natural aging of producing basins in Asia Pacific, the Middle East, and Latin America.

By Petroleum Product: Crude Oil Leads While Biofuels / Alternative Fuels Drive Fastest Growth Through 2035

Crude Oil dominated with a 68.45% share in 2025 at USD 6.30 Billion, while Biofuels / Alternative Fuels are expected to grow at the fastest CAGR of approximately 7.69% through 2035.

Crude oil's commanding share reflects the historical design of national reserve systems, which were built around crude storage because refinery capacity was assumed to be available domestically to process drawdown volumes into usable products. That assumption has proven operationally limiting, and the trend toward refined product and alternative fuel inclusion in reserve portfolios is a direct response. Biofuels and alternative fuels are growing fastest from a small base as governments that have made biofuel blending mandates central to their transport fuel policy find it logical to extend reserve holdings to include the biofuel component of the fuel supply they are protecting.

By Storage Purpose: Energy Security & Emergency Supply Leads While Strategic Trade & Export Management Drives Fastest Growth Through 2035

Energy Security & Emergency Supply dominated with a 51.28% share in 2025 at USD 4.72 Billion, while Strategic Trade & Export Management is expected to grow at the fastest CAGR of approximately 8.65% through 2035.

Emergency supply remains the foundational purpose of strategic reserves globally, and the IEA's 90-day requirement continues to anchor national reserve targets for member countries. Strategic trade and export management is growing fastest because major oil-producing nations particularly in the Gulf and among emerging producers in Africa are recognizing that petroleum reserve positions can be used as instruments of market influence, price management, and trade relationship management beyond their traditional emergency supply role.

By End-User: Government / National Energy Agencies Lead While International Energy Organizations Drive Fastest Growth Through 2035

Government / National Energy Agencies dominated with a 55.62% share in 2025 at USD 5.12 Billion, while International Energy Organizations are expected to grow at the fastest CAGR of approximately 10.10% through 2035.

Government agencies hold the overwhelming majority of strategic reserve assets globally because reserve programs are policy instruments rather than commercial investments, and only government entities have both the mandate and the risk tolerance to hold large petroleum positions that may sit unused for years. International energy organizations are growing fastest as the IEA, IEF, and regional equivalents develop more active reserve coordination roles that require their own operational capacity and management infrastructure alongside the member country reserves they help coordinate.

Strategic Petroleum Reserve Market Regional Analysis:

Asia Pacific Strategic Petroleum Reserve Market Insights

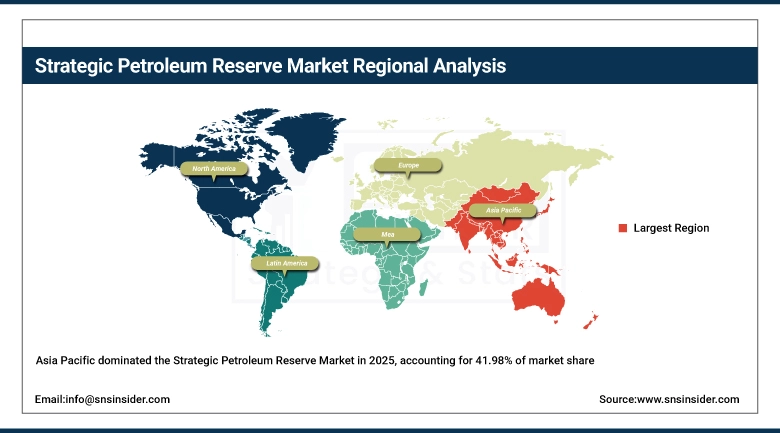

Asia Pacific dominated the Strategic Petroleum Reserve Market in 2025, accounting for 41.98% of market share at USD 3.86 Billion, projected to reach USD 7.19 Billion by 2035 at a CAGR of 6.46%. China is the dominant national market in the region, holding the world's second-largest strategic petroleum reserve after the United States, with ongoing expansion of both salt cavern and aboveground tank capacity across coastal storage hubs in Shandong, Zhejiang, and Liaoning provinces.

China's reserve strategy reflects both energy security calculation and the government's use of reserve release and refill cycles as oil market management tools.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Strategic Petroleum Reserve Market Insights

North America held a 24.12% share in 2025 at USD 2.22 Billion, projected to reach USD 2.93 Billion by 2035 at a CAGR of 2.82%. The United States dominates North American demand with 64.3% of regional share. The U.S. SPR, with capacity of approximately 714 million barrels across four Gulf Coast salt cavern sites, remains the world's largest single emergency reserve, though recent policy-driven drawdowns have reduced its fill level significantly and generated a government-funded refill program.

Europe Strategic Petroleum Reserve Market Insights

Europe held an 18.73% share in 2025 at USD 1.72 Billion, projected to reach USD 2.22 Billion by 2035 at a CAGR of 2.55%. Germany leads the European market as the continent's largest economy and the country with the most complex strategic reserve management obligation under EU and IEA frameworks. The Russian supply disruption following 2022 significantly elevated the political priority of reserve adequacy across European governments, translating into increased funding for reserve maintenance and emergency coordination infrastructure even in markets where the reserve investment growth rate remains modest.

Latin America and Middle East & Africa Strategic Petroleum Reserve Market Insights

Latin America held 7.99% of market share in 2025 at USD 735 Million, expected to reach USD 1.47 Billion by 2035 at a CAGR of 7.18%. Brazil leads the Latin American market, with Petrobras-affiliated storage infrastructure and a national reserve management framework that has expanded its scope as Brazil's role as an oil exporter has grown. Mexico and Argentina hold secondary positions. Middle East & Africa is expected to grow at the fastest regional CAGR of 12.68%, rising from USD 662 Million in 2025 to USD 2.23 Billion by 2035. Saudi Arabia leads the MEA market through Saudi Aramco's strategic storage network, which is among the most technically sophisticated in the world. The UAE, Qatar, and Kuwait are each building reserve positions that match their stated ambitions as long-term oil supply partners to Asian markets.

Competitive Landscape for Strategic Petroleum Reserve Market:

Royal Vopak

Royal Vopak is a Dutch independent tank terminal operator the world's largest by capacity with a network spanning petroleum, chemicals, and gas storage across more than 20 countries. In the strategic reserve market, Vopak operates terminals that serve both commercial and strategic storage mandates, giving governments third-party storage capacity that complements government-owned reserve facilities.

In February 2025, Royal Vopak announced a capacity expansion at its Eemshaven terminal in the Netherlands, adding 200,000 cubic meters of petroleum product storage configured for EU emergency stock mandate compliance, financed partly through a long-term storage agreement with a European national energy agency.

Oiltanking

Oiltanking, a subsidiary of the Marquard & Bahls Group, is one of the world's largest independent tank storage providers, operating over 45 terminals globally across petroleum, chemicals, and gas. Its strategic reserve market participation spans government contract storage in Europe, Asia Pacific, and the Middle East, where terminal infrastructure serves both commercial trading clients and national reserve program mandates.

In April 2025, Oiltanking completed commissioning of a petroleum storage hub in Jubail, Saudi Arabia, developed with Saudi Aramco, adding 1.5 million cubic meters of crude and refined product storage operable under both commercial throughput and strategic reserve mandate configurations.

Strategic Petroleum Reserve Companies are:

-

APTIM

-

BWX Technologies

-

Royal Vopak

-

Oiltanking

-

VTTI

-

NuStar Energy

-

Buckeye Partners

-

Magellan Midstream

-

CNPC

-

Sinopec

-

Saudi Aramco

-

ENEOS

-

Enbridge

-

ExxonMobil

-

Energy Transfer

-

Pertamina

-

Indian Oil Corporation

-

Reliance Industries

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.20 Billion |

| Market Size by 2035 | USD 16.03 Billion |

| CAGR | CAGR of 5.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Storage Type (Underground Caverns, Aboveground Tanks, Salt Domes, and Depleted Oil Fields) • By Petroleum Product (Crude Oil, Refined Products (Gasoline, Diesel, Jet Fuel), Biofuels / Alternative Fuels, and Others) • By Storage Purpose (Energy Security & Emergency Supply, Price Stabilization & Market Intervention, Industrial & Commercial Usage, and Strategic Trade & Export Management) • By End-User (Government / National Energy Agencies, Oil & Gas Companies, Military & Defense Organizations, and International Energy Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Strategic Storage Partners, APTIM, BWX Technologies, Royal Vopak, Oiltanking, Kinder Morgan, VTTI, NuStar Energy, Buckeye Partners, Magellan Midstream, CNPC, Sinopec, Saudi Aramco, ENEOS, Enbridge, ExxonMobil, Energy Transfer, Pertamina, Indian Oil Corporation, Reliance Industries. |

Frequently Asked Questions

Asia Pacific dominated the Strategic Petroleum Reserve Market in 2025

Underground Caverns dominated the Strategic Petroleum Reserve Market with a 36.24% share in 2025.

The key drivers of the Strategic Petroleum Reserve Market are rising geopolitical risk, post-2022 emergency drawdown replenishment mandates, mandatory IEA 90-day stockholding obligations, and large-scale infrastructure modernization and capacity expansion programs across Asia Pacific, the Middle East, and North America.

The Strategic Petroleum Reserve Market size was USD 9.20 Billion in 2025 and is expected to reach USD 16.03 Billion by 2035.

The Strategic Petroleum Reserve Market is expected to grow at a CAGR of 5.76% from 2026 to 2035.

Get in Touch