Supplementary Cementitious Materials Market Report Scope & Overview:

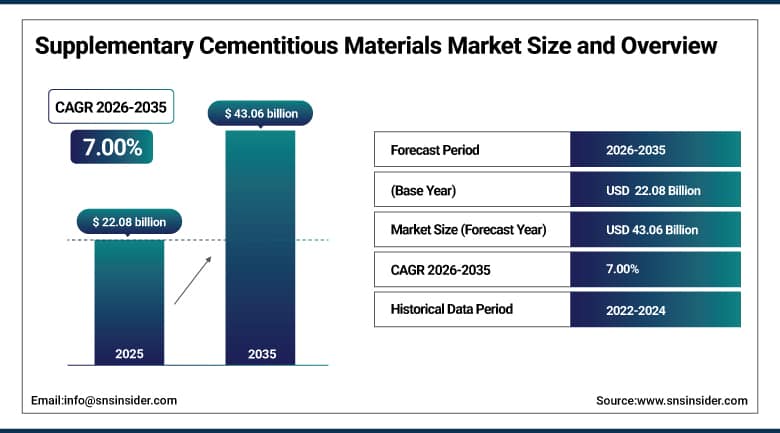

The Supplementary Cementitious Materials (SCM) Market size is valued at USD 22.08 Billion in 2025 and is projected to reach USD 43.06 Billion by 2035, growing at a CAGR of 7.00% during the forecast period 2026–2035.

The Supplementary Cementitious Materials (SCM) Market Insights report offers an in-depth evaluation of market trends, material advancements, and construction application areas. The high demand for low-carbon sustainable materials, rapid infrastructure development, strict environmental policies, and increased use of blended cement systems are key drivers that propel the market's steady growth in 2026-2035.

Supplementary Cementitious Material (SCM) consumption in cement and concrete manufacturing surpassed 410 billion tons in 2025.

Market Size and Forecast:

-

Market Size in 2025: USD 22.08 Billion

-

Market Size by 2035: USD 43.06 Billion

-

CAGR: 7.00% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Supplementary Cementitious Materials Market - Request Free Sample Report

Supplementary Cementitious Materials Market Trends:

-

Rising demand for low-carbon and sustainable construction materials is accelerating adoption of supplementary cementitious materials (SCMs) in cement production.

-

Increasing infrastructure development, urbanization, and mega construction projects are driving higher consumption of blended cement and SCM-based concrete.

-

Stringent environmental regulations and carbon reduction targets are boosting replacement of clinker with SCMs to reduce CO₂ emissions.

-

Growing shift toward high-performance and durable concrete is increasing usage of fly ash, GGBFS, silica fume, and calcined clay.

-

Expansion of green building certifications and sustainable construction standards is supporting long-term SCM integration in construction projects.

-

Declining availability of fly ash in some regions is accelerating innovation and adoption of alternative SCMs such as calcined clay and engineered pozzolans.

U.S. Supplementary Cementitious Materials Market Insights:

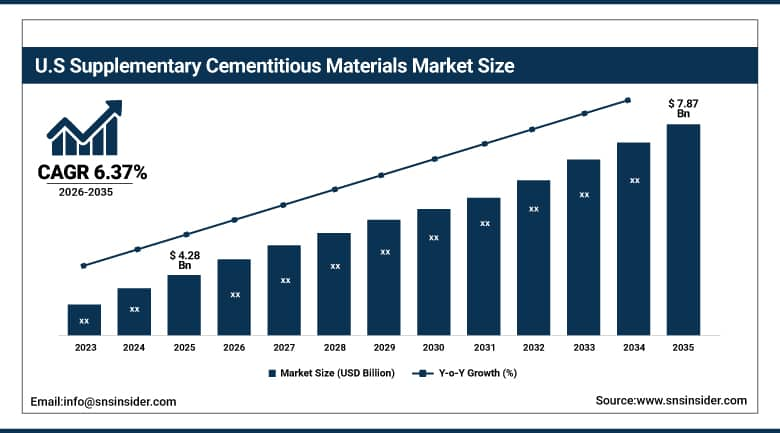

The U.S. Supplementary Cementitious Materials (SCM) Market in the United States is projected to grow from USD 4.28 Billion in 2025 to USD 7.87 Billion by 2035, at a CAGR of 6.37%. Growth will be fueled by increased infrastructure rehabilitation projects, increased use of low-carbon sustainable construction materials, stricter environmental laws that promote clinker replacement, and high demand for high performance concrete in highways, bridges, and commercial constructions within the construction industry in the United States.

Supplementary Cementitious Materials Market Growth Drivers:

-

Rising demand for sustainable and low-carbon construction materials is driving increased adoption of supplementary cementitious materials (SCMs) in cement and concrete production.

Increasing infrastructure development, urbanization, and extensive construction projects are among the critical factors fueling the growth of the SCM market. Increasingly, construction firms, cement producers, and ready-mixed concrete makers have begun using SCMs including fly ash, GGBFS, silica fume, and calcined clay, thus enhancing their durability, strength, and sustainability while minimizing the use of clinker and CO₂ emissions. Technical improvements in blended cement technology and increasing environmental laws are driving the adoption of SCMs in various construction activities, leading to market growth over time.

More than 62% of total cement and concrete output made use of supplementary cementitious materials in 2025.

Supplementary Cementitious Materials Market Restraints:

-

High dependence on clinker-based cement production and fluctuating availability of supplementary cementitious material (SCM) by-products are restraining consistent market growth.

The inconsistency in the supply of vital SCMs including fly ash and GGBFS due to closures in coal power plants and variations in steel manufacturing is one of the most prominent obstacles faced by the Supplementary Cementitious Materials Market. Other than that, a lack of processing capability, inadequate logistics, and non-uniform quality of SCMs hamper mass acceptance of the same among cement producers and construction firms. On top of all, increased processing costs and limited regulation in terms of SCM usage pose another significant barrier to market adoption.

Supplementary Cementitious Materials Market Opportunities:

-

Growing adoption of carbon reduction policies and net-zero construction targets is creating significant opportunities for supplementary cementitious materials (SCMs) in the construction industry.

Increased focus on decarbonization within the cement and construction industry creates tremendous opportunities for the SCM market. In this regard, cement producers, contractors, and infrastructure builders are increasingly relying on SCMs such as calcined clay, slag, and synthetic pozzolan to decrease clinker usage while achieving sustainability requirements. Furthermore, the development of green infrastructure initiatives, the provision of carbon credits, and the promotion of sustainable building materials contribute immensely to the increased uptake of SCMs in large infrastructure projects.

More than 50% of new infrastructure and green buildings built in 2025 adopted the use of blended cement technologies utilizing SCMs.

Supplementary Cementitious Materials Market Segmentation Analysis:

-

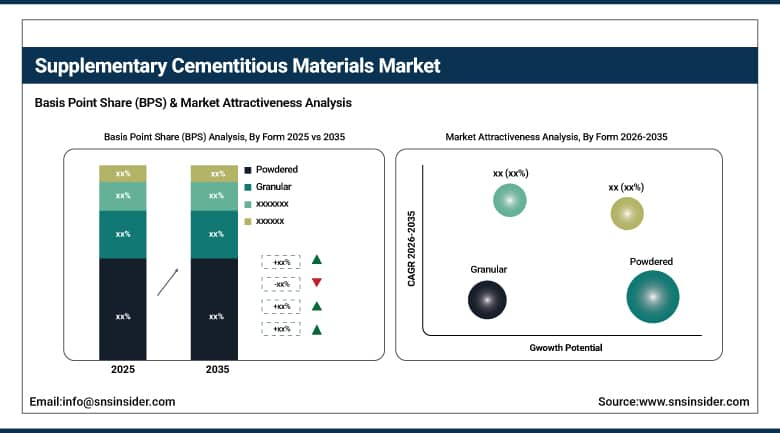

By Form, Powdered SCMs accounted for the highest market share of 62.12% in 2025, while Processed / Engineered SCMs are projected to grow at the fastest CAGR of 7.24% during 2026–2035.

-

By Type, Fly Ash held the largest market share of 42.75% in 2025, while Silica Fume is expected to grow at the fastest CAGR of 8.06% during 2026–2035.

-

By Application, Ready-Mix Concrete dominated with 38.05% market share in 2025, Mass Concrete (Infrastructure Projects) is projected to grow at the fastest CAGR of 9.38% during 2026–2035.

-

By End-Use Industry, Infrastructure (Roads, Bridges, Dams, Railways) held the largest share of 35.85% in 2025, while Marine & Coastal Construction is expected to grow steadily at 4.45% CAGR during 2026–2035.

-

By Technology, Mechanical Processing (Grinding & Activation) dominated with 35.23% market share in 2025, while Chemical/Engineered SCM Systems are expected to grow at the fastest CAGR of 8.54% during 2026–2035.

By Form, Powdered SCMs Dominate While Processed / Engineered SCMs Grow Rapidly:

Powdered SCMs segment dominated the market due to its high usage in manufacturing of cement and producing ready-mix concretes due to their ease of mixing nature. Their ability to integrate into large constructions along with cement processing helps in maintaining their market lead.

Processed / Engineered SCMs is the fastest-growing segment, due to their increasing demand among construction firms that aim to construct high-performance and environment friendly structures.

By Type, Fly Ash Dominates While Silica Fume Grows Rapidly:

Fly Ash segment dominated the market due to high availability due to coal-fired power plants and wide usage in making blended cement and concrete. Cost efficiency and improved concrete durability as a result of blending with clinker will keep Fly Ash at the top in terms of usage for constructing purposes.

Silica Fume is the fastest-growing segment, due to increased usage in ultra-high-performance concrete and constructions where durability is vital. Infrastructure projects such as bridges and tunnels have contributed toward this growth trend.

By Application, Ready-Mix Concrete Dominates While Mass Concrete (Infrastructure Projects) Grows Rapidly:

Ready-Mix Concrete segment dominated the market in terms of market share owing to the extensive use of this concrete in residential, commercial, and infrastructure projects, with constant demand from contractors and major construction developers. The efficiency of the concrete in large-scale transportation, uniformity in quality, and compatibility with SCM blending ensures its superiority in construction.

Mass Concrete (Infrastructure Projects) is the fastest-growing segment, owing to increasing construction of large infrastructure projects including dams, foundations, bridges, and other heavy civil works.

By End-Use Industry, Infrastructure Dominates While Marine & Coastal Construction Grows Rapidly:

Infrastructure (Roads, Bridges, Dams, Railways) segment dominated the market as a result of huge investments being made in infrastructural development and requirement of durability for large scale projects. This segment’s close connection with national policies for infrastructural development and urbanization ensures its dominance in SCM consumption.

Growth in Marine & Coastal Construction was fastest, due to increasing number of projects of coast protection, port development, and resilient infrastructure development. Growing need for robust construction materials owing to harsh environmental conditions is propelling growth in this segment.

By Technology, Mechanical Processing Dominates While Chemical/Engineered SCM Systems Grow Rapidly:

Mechanical Processing (Grinding & Activation) segment dominated the market share due to its extensive use in improving the reactivity and performance of fly ash, slag, and other waste products from industries. Its matured industrial base and affordable processing technologies ensure high adoption levels among cement manufacturers.

chemical/Engineered SCM Systems is the fastest-growing sector owing to rising concerns toward decarbonization, performance enhancement, and innovative cements.

Supplementary Cementitious Materials Market Regional Analysis:

Asia-Pacific Supplementary Cementitious Materials Market Insights:

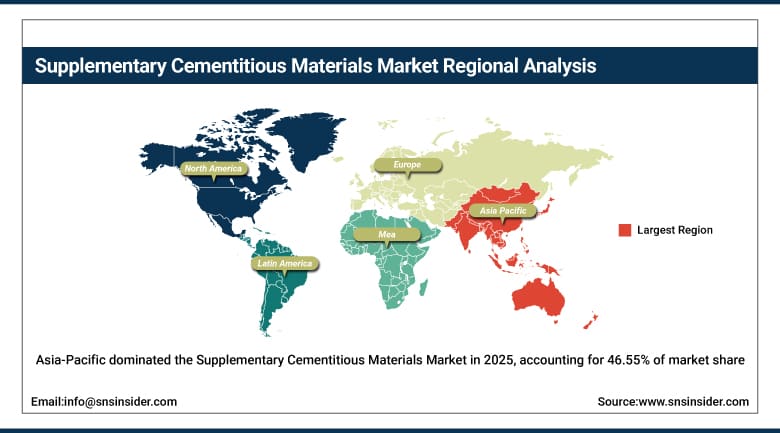

The Asia-Pacific SCM Market is dominated, holding a 46.55% share in 2025 and also a fastest-growing region, projected to expand at a CAGR of 7.76% during 2026–2035The growth is fueled by rapid urbanization, infrastructure development, and major construction activities in countries such as China, India, and Southeast Asia. Increased demand for housing, transport, and other infrastructure projects has led to rising consumption of SCM for cement and concrete production. Increasing use of calcined clay, fly ash, and slag-based materials in addition to government-backed initiatives aimed at sustainability and carbon reductions are fueling the growth of the market. Growth in capacity and interest in low-cost construction materials are driving growth within the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

China Supplementary Cementitious Materials Market Insights:

China SCM market is fueled by infrastructure development, rapid urbanization, and huge construction activity in all sectors of construction, whether residential, commercial, or industrial. Availability of ample production capacity of cement, along with the widespread availability of industrial waste materials which includes fly ash and slag, helps in driving high SCM consumption in blended cement products.

North America Supplementary Cementitious Materials Market Insights:

The North America SCM Market is an established region backed by advanced construction standards and wide prevalence of blended cement technologies. The region witnesses significant demand from infrastructure revamp programs, highway reconstruction efforts, and heavy commercial construction activities in both the United States and Canada. Significant usage of fly ash, GGBFS, and silica fume in ready-mix and high-performance concrete applications ensures stability within the region. Strong environmental compliance measures for carbon reductions and replacement of clinkers combined with advanced construction techniques and supply chain network ensures consistent growth of SCMs within the region.

US Supplementary Cementitious Materials Market Insights:

The US SCM Market is characterized by significant infrastructure renewal programs in terms of bridges, highways, and utilities along with strong demand for environmentally friendly construction materials. The extensive use of fly ash and slag in cement manufacturing for ready-mix and precast products further fuels the growth of the market. Sustainability focus, LEED and carbon neutrality requirements among others fuel the adoption of SCMs in various construction projects in the country.

Europe Supplementary Cementitious Materials Market Insights:

Environmentally strict policies, robust sustainability goals, and popularly used low carbon building materials are some key factors supporting the Europe SCM Market. Germany, France, and UK among other nations are fueling the demand for advanced infrastructure developments, stringent building standards, and higher usage of blended cement in buildings. Higher acceptance rate of calcined clay, slag cement, and silica fumes ensures efficient performance of building materials and increased durability of products. Strong policy backing for carbon reduction, circular economy programs, and innovative construction technologies is contributing to Europe being one of the key markets.

Germany Supplementary Cementitious Materials Market Insights:

Among the European SCM Market, Germany ranks top due to its leading construction technologies, environmental stringency, and need for durable infrastructure materials. Higher usage of blended cement in the development of roads, factories, and residential buildings helps the nation in maintaining continuous SCM consumption. The country’s efforts in limiting clinker usage and higher industrial waste recycling rates in the form of slag ensure higher market growth.

Latin America Supplementary Cementitious Materials Market Insights:

The Latin America SCM Market is experiencing consistent growth owing to the increase in infrastructure development, urbanization, and rise in the construction sector. Several countries in Latin America such as Brazil, Mexico, and Argentina have seen an uptick in the use of blended cements for improving their cost-effectiveness and building strength. The presence of industrial wastes and growing emphasis on sustainable building practices is helping in the adoption of supplementary cementitious materials.

Middle East and Africa Supplementary Cementitious Materials Market Insights:

The Middle East & Africa SCM Market is witnessing substantial growth owing to extensive infrastructure development projects, urbanization drives, and the need for resilient construction materials. Countries such as Saudi Arabia, UAE, and South Africa are fueling the growth owing to their mega projects and developments in smart cities and transportation infrastructure. An increased focus on sustainability, water-resistant construction materials, and durable concrete structures is also contributing to SCM utilization.

Supplementary Cementitious Materials Market Competitive Landscape:

Holcim is a leader in the construction materials industry with a strong presence in the supplementary cementitious materials (SCM) market, offering extensive solutions including fly ash-based blended cement, slag cement, calcined clay integration, and low-carbon concrete technologies through its ECOPact and ECOPlanet product lines. Its leadership is driven by large-scale cement production capacity, strong SCM integration across ready-mix and infrastructure projects, and continuous investment in decarbonization technologies. Holcim’s circular construction model, supply chain strength, and focus on reducing clinker intensity reinforce its dominant position in sustainable construction materials.

-

In September 2025, Holcim expanded its ECOPact low-carbon concrete portfolio across Europe and North America, increasing SCM-based cement adoption in large infrastructure and commercial construction projects, strengthening its leadership in sustainable building materials.

Holcim, a prominent player in the construction materials sector, maintains a significant position within the supplementary cementitious materials (SCM) market. The company provides a wide range of solutions, including fly ash-based blended cement, slag cement, calcined clay integration, and low-carbon concrete technologies, all available through its ECO Pact and ECO Planet product lines. Holcim's leadership is attributable to its substantial cement production capacity, strong SCM integration across ready-mix and infrastructure projects, and ongoing investments in decarbonization technologies. Holcim’s circular construction approach, combined with its robust supply chain and commitment to lowering clinker intensity, solidifies its leading role in the sustainable construction materials sector.

-

In August 2025, Heidelberg Materials advanced its evoBuild low-carbon cement range, increasing the share of alternative raw materials and SCM integration across major infrastructure projects in Europe, supporting large-scale decarbonization initiatives.

CEMEX S.A.B. de C.V. is a major building materials company with a strong position in the SCM market, driven by its Vertua low-carbon product line and widespread use of industrial by-products such as fly ash and slag in cement and ready-mix concrete production. The company emphasizes sustainable construction solutions, carbon reduction strategies, and high-performance blended cement systems tailored for infrastructure and urban development projects. Its strong presence in the Americas and Europe, combined with digital construction solutions and circular economy initiatives, reinforces its market competitiveness.

-

In July 2025, CEMEX expanded its Vertua portfolio across North America, increasing SCM-based cement adoption in infrastructure and housing projects, supporting its long-term net-zero and carbon reduction roadmap.

Supplementary Cementitious Materials Market Key Players:

-

Holcim

-

Heidelberg Materials

-

CEMEX S.A.B. de C.V.

-

CRH plc

-

UltraTech Cement Ltd.

-

Boral Limited

-

Ecocem

-

Charah Solutions Inc.

-

ECO Material Technologies

-

ArcelorMittal S.A.

-

Tata Steel Ltd.

-

JSW Cement Ltd.

-

Dangote Cement Plc.

-

Votorantim Cimentos

-

Siam Cement Group (SCG)

-

Taiheiyo Cement Corporation

-

Nippon Steel Blast Furnace Slag Cement Co. Ltd.

-

Ferroglobe PLC

-

Sika AG

-

BASF SE

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 22.08 Billion |

| Market Size by 2035 | USD 43.06 Billion |

| CAGR | CAGR of 7.00% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fly Ash, Ground Granulated Blast Furnace Slag (GGBFS / Slag Cement), Silica Fume, Calcined Clay, Natural Pozzolans, Others) • By Application (Ready-Mix Concrete, Precast Concrete, High-Performance Concrete, Mass Concrete (Infrastructure Projects), Mortars & Grouts, Others) • By End-Use Industry (Residential Construction, Commercial Construction, Infrastructure (Roads, Bridges, Dams, Railways), Industrial Construction, Marine & Coastal Construction, Others) • By Form (Powdered, Granular, Processed / Engineered SCMs, Others) • By Technology (Thermal Processing (Calcination-based SCMs), Mechanical Processing (Grinding & Activation), By-product Recovery Systems, Chemical/Engineered SCM Systems, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Holcim, Heidelberg Materials, CEMEX S.A.B. de C.V., CRH plc, UltraTech Cement Ltd., Boral Limited, Ecocem, Charah Solutions Inc., ECO Material Technologies, ArcelorMittal S.A., Tata Steel Ltd., JSW Cement Ltd., Dangote Cement Plc., Votorantim Cimentos, Siam Cement Group (SCG), Taiheiyo Cement Corporation, Nippon Steel Blast Furnace Slag Cement Co. Ltd., Ferroglobe PLC, Sika AG, BASF SE |

Frequently Asked Questions

Asia Pacific dominated with a 46.55% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 7.76% during 2026–2035.

Fly Ash dominated with a 42.75% share in 2025, while Silica Fume are projected to grow at the fastest CAGR of 8.06% during 2026–2035.

Growth is driven by rising infrastructure development, increasing demand for low-carbon and sustainable construction materials, stringent environmental regulations, and growing adoption of blended cement technologies.

The market is valued at USD 22.08 Billion in 2025 and is projected to reach USD 43.06 Billion by 2035.

The Supplementary Cementitious Materials Market is projected to grow at a CAGR of 7.00% during 2026–2035.

Get in Touch