Waterborne Epoxy Resin Market Report Scope & Overview:

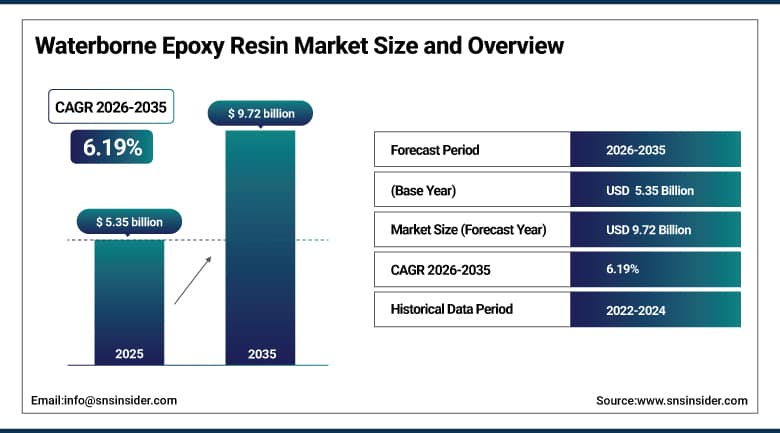

The Waterborne Epoxy Resin Market size was valued at USD 5.35 Billion in 2025 and is projected to reach USD 9.72 Billion by 2035, growing at a CAGR of 6.19% during 2026-2035.

Market growth can be attributed to the increased need for eco-friendly coatings owing to stringent VOC regulations in the construction and automobile industries. There is also increased infrastructure development, fast-paced urbanization, and the trend towards sustainability that boosts the use of these resins. They provide good bonding, corrosion resistance, and high durability, which makes them suitable for industrial uses. In addition, the growth of electronic industry, packaging industry, and protective coatings industry is boosting market growth.

Market Size and Forecast:

-

Market Size in 2025: USD 5.35 Billion

-

Market Size by 2035: USD 9.72 Billion

-

CAGR: 6.19% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Waterborne Epoxy Resin Market - Request Free Sample Report

Key Waterborne Epoxy Resin Market Trends

-

Increasing adoption of low-VOC, eco-friendly coatings driven by stringent environmental regulations across industries globally.

-

Rising demand from construction sector due to infrastructure expansion and need for durable protective coatings.

-

Technological advancements improving performance, durability, and curing efficiency of waterborne epoxy resin formulations worldwide.

-

Growing use in automotive and transportation industries for lightweight, corrosion-resistant, and high-performance coating solutions.

-

Expansion in electronics and packaging applications driven by demand for sustainable, high-adhesion material solutions.

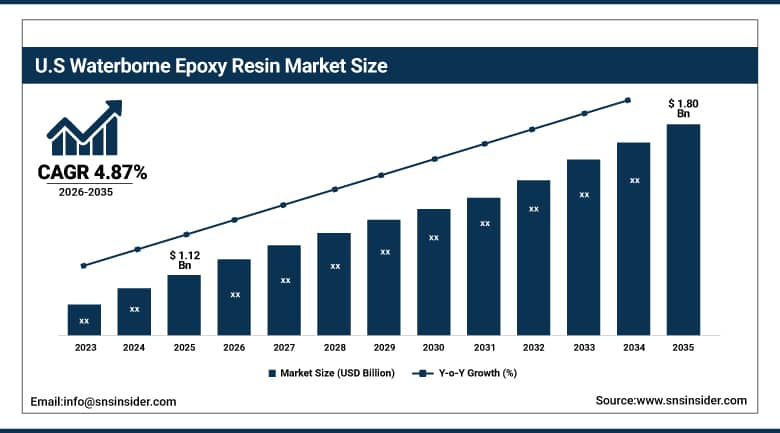

The U.S. Waterborne Epoxy Resin Market size was valued at USD 1.12 Billion in 2025 and is projected to reach USD 1.80 Billion by 2035, growing at a CAGR of 4.87% during 2026-2035. The U.S. market is the dominant national market within North America, anchored by a mature industrial coatings sector that has been transitioning toward waterborne chemistries under EPA VOC regulations and OSHA occupational exposure limits for many years, combined with a large construction and infrastructure maintenance market that consumes waterborne epoxy floor coatings, concrete sealers, and structural adhesives across commercial, industrial, and infrastructure applications at volumes that make the U.S. the most significant single consumer of waterborne epoxy resins in the region.

Waterborne Epoxy Resin Market Growth Drivers:

-

Green Coatings Surge as Sustainability Regulations Accelerate Waterborne Epoxy Resin Market Expansion Globally

Environmental laws and policies advocating green coatings are the major drivers for the Waterborne Epoxy Resin Market. The increase in demand for water-based epoxy resins in construction and infrastructure projects in emerging economies owing to their high durability and ability to resist corrosion will drive the market. Moreover, the use of water-based epoxy resins in automotive and transportation industries for their lightweight and protective properties will propel the market growth. Growth in technology enhancing the performance of these resins and their curing process is another driving factor influencing market growth.

Waterborne Epoxy Resin Market Restraints:

-

Performance Limitations and High Costs Challenge Widespread Adoption of Waterborne Epoxy Resin Solutions Globally

Even though there is an immense scope for growth, the industry is bound by constraints such as high prices when compared to other coatings, which makes it difficult to operate in areas where price is the primary consideration. Slow reaction and sensitivity to environmental elements such as humidity affect performance in terms of application efficiency. Furthermore, some formulations do not possess adequate resistance against chemicals and moisture, thereby limiting the applicability of water-based coatings in tough industrial settings. These are just some of the many constraints faced by the industry.

Waterborne Epoxy Resin Market Opportunities:

-

Emerging Applications and Technological Innovations Unlock New Growth Opportunities in Waterborne Epoxy Resin Market Worldwide

There exist considerable opportunities for growth due to the rising investment in research and development aimed at improving the performance characteristics of water-based epoxy resins. An increase in the number of applications for such epoxy resin products in electronics, renewable energy systems, and packaging industries will open up new avenues for growth. Urbanization and infrastructural developments taking place in emerging markets are also creating demand for green coatings. Curing technology innovations and hybrid resins will help make the production process more efficient and facilitate new opportunities within other industries.

Waterborne Epoxy Resin Market Segment Analysis

-

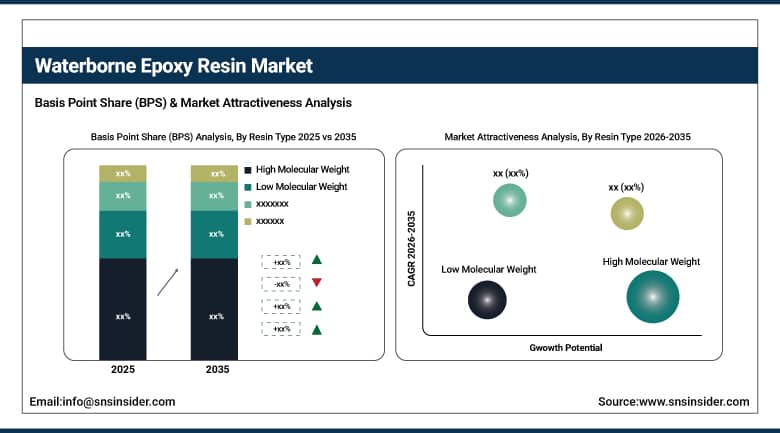

By Resin Type, High Molecular Weight dominated with 62.48% in 2025, and Low Molecular Weight is expected to grow at the fastest CAGR of 7.04% from 2026 to 2035.

-

By Application, Coatings dominated with 48.27% in 2025, and Adhesives are expected to grow at the fastest CAGR of 7.18% from 2026 to 2035.

-

By End-Use Industry, Construction dominated with 39.72% in 2025, and Automotive & Transportation is expected to grow at the fastest CAGR of 7.04% from 2026 to 2035.

-

By Curing Agent Type, Amine-Based dominated with 57.63% in 2025, and Others are expected to grow at the fastest CAGR of 7.31% from 2026 to 2035.

By Resin Type, High Molecular Weight Leads Waterborne Epoxy Resin Market While Low Molecular Weight Set for Fastest Growth 2026 to 2035

The High Molecular Weight segment leads the global market owing to its excellent mechanical strength, high chemical resistance, and durability. These attributes make this resin category highly preferable for use in industrial coatings and constructions. On the other hand, the growth of the Low Molecular Weight segment is attributed to its high processing abilities, flexibility, and high penetration capability. The rising demand for high-end resins in various application segments, such as adhesives and specialty coatings, is contributing significantly to its popularity among diverse end users.

By Application, Coatings Lead Waterborne Epoxy Resin Market While Adhesives Show Fastest Growth 2026 to 2035

The coatings category holds the largest market share in the Waterborne Epoxy Resins Market owing to widespread application in the fields of protection, decoration, and industry, especially in construction and infrastructure-related applications. The superior performance of these resins as adhesives is one of the key factors driving their popularity in various industries. Adhesives represent the highest-growth category, mainly due to growing demand for efficient, long-lasting, and environmentally compliant adhesive products in applications like automobiles, packaging, and electronics.

By End-Use Industry, Construction Leads Waterborne Epoxy Resin Market While Automotive & Transportation Shows Fastest Growth 2026 to 2035

The construction sector is leading the market owing to the rapid pace of urbanization and infrastructural developments. Additionally, the increased demand for robust and durable coatings is contributing to the growth of the market. The automotive & transportation industry segment is experiencing the highest growth rate due to the increased demand for corrosion-resistant and high-performance materials. With the growth in vehicle production and the emphasis on reducing emissions, the use of waterborne epoxy resins is expected to increase.

By Curing Agent Type, Amine-Based Leads and Others Show Fastest Growth in Waterborne Epoxy Resin Market 2026 to 2035

Amine Curing Agents represent the major players in the industry owing to their high curing speeds, strong adhesions, and compatibility with aqueous epoxy coating products. Moreover, the consistency of their quality and low prices have made amine-based curing agents leaders in the market. "Others" represents the fastest growing segment, which has emerged due to constant improvements and innovations in curing technology. R&D in the field has introduced new curing agents with better strength, flexibility, and efficacy, enabling their quick adoption in different industrial processes.

Waterborne Epoxy Resin Market Regional Analysis

North America Waterborne Epoxy Resin Market Insights

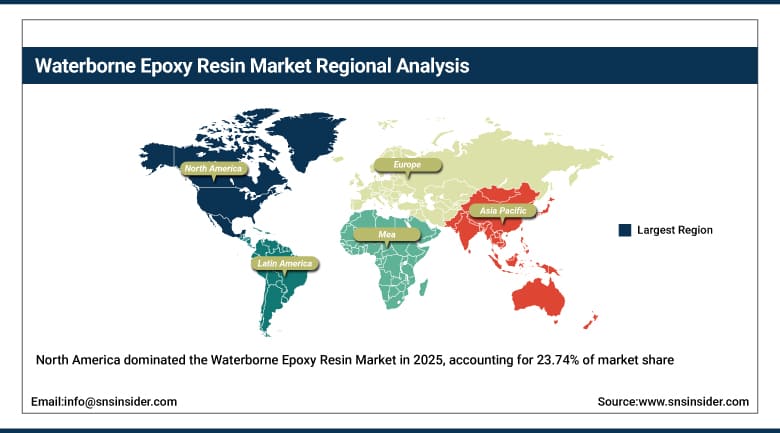

North America held a 23.74% share of the global Waterborne Epoxy Resin Market in 2025 at USD 1.27 Billion, growing at a CAGR of 5.16% through 2035. The region's market is anchored by a mature industrial coatings sector that has undergone extensive reformulation toward waterborne chemistries over the past two decades in response to stringent state and federal air quality regulations, combined with a large construction and infrastructure maintenance market that consumes waterborne epoxy floor coatings, concrete protection systems, and structural adhesives at stable volumes across commercial, industrial, and public infrastructure applications. Dow Inc. and Huntsman Corporation maintain significant waterborne epoxy resin production and commercial operations in the United States that anchor the regional supply chain, and the presence of a sophisticated downstream formulation industry creates a technically demanding domestic customer base that drives product development investment across resin performance dimensions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Waterborne Epoxy Resin Market Insights

The United States dominated North America's waterborne epoxy resin market at 88.46%, USD 1.12 Billion in 2025. The U.S. market is characterized by high-specification demand across floor coating, industrial maintenance, and electronics applications where performance requirements are as important as VOC compliance in product selection decisions. U.S.-based resin producers including Hexion and Olin Corporation are significant participants in the domestic waterborne epoxy market, and the presence of major downstream coatings and adhesives manufacturers including Sherwin-Williams, PPG Industries, and Henkel provides a large and technically sophisticated customer base that drives continuous product development investment in waterborne epoxy resin performance and formulation compatibility.

Europe Waterborne Epoxy Resin Market Insights

Europe held 26.18% at USD 1.40 Billion in 2025, growing at a CAGR of 5.39% through 2035. Europe is the most advanced regional market for waterborne epoxy resin adoption in terms of the proportion of total epoxy resin consumption that has shifted to waterborne systems, reflecting the longer history of stringent VOC regulation under the EU's Decopaint Directive and Industrial Emissions Directive that has driven formulation transition at a pace ahead of most other global regions. Germany, France, the Netherlands, and Scandinavia are the highest-volume national markets within the region, driven by industrial coatings manufacturing, automotive OEM and supplier painting operations, and construction activity in commercial and logistics buildings. BASF SE's Ludwigshafen operations and Allnex GmbH's European manufacturing base make Europe a significant global production center for waterborne epoxy resins as well as the world's most advanced consumption market.

Germany Waterborne Epoxy Resin Market Insights

Germany was the leading national market for waterborne epoxy resins in Europe in 2025, driven by the country's large automotive manufacturing sector that is among the most advanced globally in its adoption of waterborne coating and adhesive systems across OEM and Tier 1 supplier operations, the presence of BASF SE's global resin business and Allnex GmbH's coating resin manufacturing, and a construction industry that operates under some of Europe's most stringent indoor air quality and building material emission standards, creating strong demand for low-VOC waterborne epoxy floor coatings and structural bonding products in new commercial and industrial construction.

Asia Pacific Waterborne Epoxy Resin Market Insights

Asia Pacific is the largest and fastest-growing region at a CAGR of 7.16% through 2035, valued at USD 2.39 Billion in 2025 and projected to reach USD 4.76 Billion by 2035. China is the dominant national market within the region and globally the single largest consumer of waterborne epoxy resins by volume, driven by the country's enormous construction activity, the scale of its electronics and automotive manufacturing sectors, and increasingly stringent national VOC emission standards for architectural and industrial coatings that are driving waterborne adoption among Chinese coatings manufacturers. South Korea is a significant regional market in its own right, hosting Kukdo Chemical, one of Asia's largest epoxy resin producers, and a sophisticated electronics and automotive manufacturing base that consumes high-specification waterborne epoxy systems. India's growing commercial and industrial construction market and expanding electronics manufacturing sector are generating accelerating demand for waterborne epoxy coatings and adhesives at rates that make it one of the fastest-growing national markets within Asia Pacific.

China Waterborne Epoxy Resin Market Insights

China was the dominating country in the Asia Pacific Waterborne Epoxy Resin Market because of industrialization and large scale construction projects. Furthermore, the automotive industry and electronics industry also supported the dominance of China in the Asia Pacific region.

Latin America (LATAM) and Middle East & Africa (MEA) Waterborne Epoxy Resin Market Insights

Latin America was valued at USD 0.18 Billion in 2025 and is growing at a CAGR of 5.51% through 2035, with Brazil and Mexico representing the two largest national markets driven by industrial coatings demand in manufacturing facilities, construction activity in commercial and infrastructure segments, and growing regulatory pressure on VOC emissions from coatings and adhesives applications. Brazil's industrial base, including automotive assembly, food and beverage processing, and chemical manufacturing, provides consistent demand for waterborne epoxy floor and equipment coatings, while Mexico's automotive supply chain manufacturing in Nuevo Leon, Coahuila, and Guanajuato is generating growing waterborne adhesive and primer demand aligned with the VOC standards of the OEM customers those suppliers serve. Middle East and Africa was valued at USD 0.11 Billion in 2025 and is growing at the fastest regional CAGR of 6.61% through 2035, reflecting the region's growing construction activity in Gulf states and the gradual adoption of higher-specification, lower-emission coating and adhesive products in commercial and industrial projects where international contractors and building owners are applying global material standards.

Competitive Landscape for Waterborne Epoxy Resin Market:

The BASF company is the leading supplier of waterborne epoxy resins in the European paints and coatings industry. Among BASF's water-based epoxy resins are its Epikote and Epikure products that consist of a wide range of formulations for floor coating, concrete sealing, primer and structural adhesives. Due to their technical expertise in formulation services, BASF has developed its unique position in the coatings market among companies that require formulation assistance along with raw materials supply.

-

In 2024, BASF SE introduced an expanded range of low-emission waterborne epoxy dispersion grades for commercial construction flooring applications, specifically formulated to meet the increasingly stringent European indoor air quality emission test requirements including AgBB and EMICODE certification that German, Austrian, and Swiss building operators specify for occupied commercial and institutional building projects.

Huntsman Corporation, headquartered in The Woodlands, Texas, is a major global producer of epoxy resin systems including waterborne dispersions under its ARALDITE brand, supplying coatings, adhesives, and composite applications across construction, automotive, electronics, and wind energy markets. Huntsman's advanced materials division has invested in waterborne epoxy product development as part of a broader portfolio strategy to increase the share of its epoxy resin revenue derived from products that address sustainability-driven reformulation requirements in its key end markets, and its global manufacturing footprint across the United States, Europe, and Asia allows it to serve multinational formulator customers with regionally manufactured products that reduce supply chain complexity.

- In 2024, Huntsman Corporation expanded its ARALDITE waterborne epoxy product portfolio for wind energy composite applications, introducing a low-viscosity waterborne infusion resin system designed for large-format blade manufacturing that addresses the growing sustainability pressure from wind turbine OEMs to reduce the VOC and styrene content of composite manufacturing processes at blade production facilities operating under increasingly restrictive European and North American air emission permits.

Waterborne Epoxy Resin Market Key Players:

-

BASF SE

-

Dow Inc.

-

Huntsman Corporation

-

Olin Corporation

-

Hexion Inc.

-

Allnex GmbH

-

Arkema S.A.

-

Evonik Industries AG

-

Kukdo Chemical Co., Ltd.

-

Nan Ya Plastics Corporation

-

Aditya Birla Chemicals

-

DIC Corporation

-

ADEKA Corporation

-

Reichhold LLC

-

Sika AG

-

Air Products & Chemicals Inc.

-

Spolchemie A.S.

-

Resoltech

-

Helios Resins

-

Kumho P&B Chemicals

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.35 Billion |

| Market Size by 2035 | USD 9.72 Billion |

| CAGR | CAGR of 6.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Charger Type (Single-Arm Pantograph Chargers, Dual-Arm Pantograph Chargers, Roof-Mounted Pantograph Chargers, and Side-Mounted Pantograph Chargers) • By Power Rating (< 150 kW (Low-Power), 150-350 kW (Mid-Power), 350-600 kW (High-Power), and > 600 kW (Ultra-High-Power)) • By Application (Public Transit Vehicles (Electric Buses/Trams), Rail Transit (Electric Trains/Light Rail), Commercial EV Fleets (Logistics & Delivery Vehicles), and Industrial & Depot Charging (Warehouses, Bus Depots)) • By End-User (Transit Authorities & Municipal Operators, Private Fleet Operators (Logistics & Delivery), Commercial EV Charging Infrastructure Providers, and Industrial & Enterprise Facility Owners) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Huntsman Corporation, Olin Corporation, Hexion Inc., Allnex GmbH, Arkema S.A., Evonik Industries AG, Kukdo Chemical Co., Ltd., Nan Ya Plastics Corporation, Aditya Birla Chemicals, DIC Corporation, ADEKA Corporation, Reichhold LLC, Sika AG, Air Products & Chemicals Inc., Spolchemie A.S., Resoltech, Helios Resins, Kumho P&B Chemicals. |

Frequently Asked Questions

Asia Pacific led the Waterborne Epoxy Resin Market in 2025 with a 44.67% share.

High Molecular Weight resin dominated the Waterborne Epoxy Resin Market with a 62.48% share in 2025.

Key drivers include tightening VOC emission regulations on industrial coatings and adhesives, growing adoption of green building certification standards that credit low-emission materials, and increasing automotive OEM reformulation programs toward waterborne epoxy systems across coating and adhesive applications.

The Waterborne Epoxy Resin Market size was USD 5.35 Billion in 2025 and is projected to reach USD 9.72 Billion by 2035.

The Waterborne Epoxy Resin Market is expected to grow at a CAGR of 6.19% from 2026-2035.

Get in Touch