Surgical Helmet Market Size & Trends:

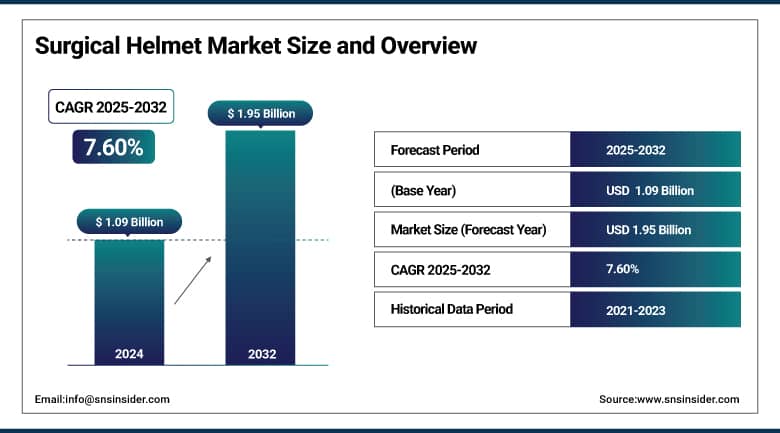

The Surgical Helmet Market size was valued at USD 1.09 billion in 2024 and is expected to reach USD 1.95 billion by 2032, growing at a CAGR of 7.60% over the forecast period of 2025-2032.

The global surgical helmet market is growing at a significant rate as a result of the quickly growing need for sterilization in operating rooms, particularly for orthopedic and trauma surgeries. Some of the factors responsible for the growth of the market are a rise in surgical volumes, an increase in awareness regarding occupational safety, and the use of helmet systems. In addition, with rising adoption in ambulatory surgical centers and preparedness after several global health situations, the market wisely get a boost in overall demand.

To Get More Information On Surgical Helmet Market - Request Free Sample Report

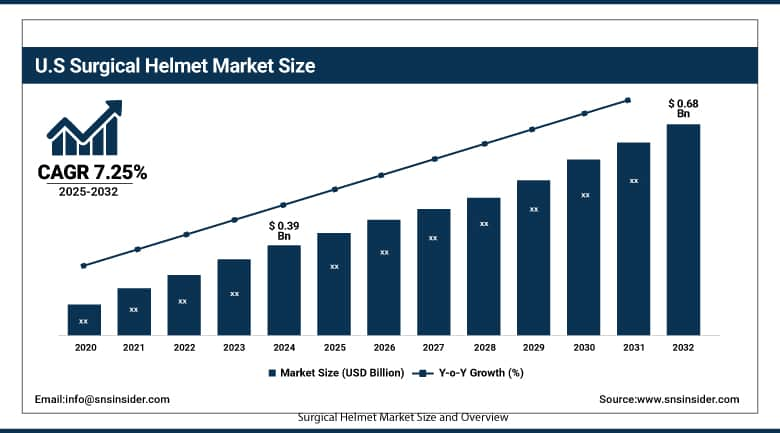

The U.S. Surgical Helmet Market size was valued at USD 0.39 billion in 2024 and is expected to reach USD 0.68 billion by 2032, growing at a CAGR of 7.25% over the forecast period of 2025-2032.

The U.S. dominates the North American surgical helmet market, a result of a high number of orthopedic and trauma surgeries conducted in the country, its highly developed healthcare infrastructure, and great concern regarding surgical staff safety. Moreover, a high presence of key market players and innovation in the personal protective equipment industry will support the growth of the country in the forecast period.

Surgical Helmet Market Dynamics:

Drivers

-

Increasing Global Surgical Volume is Driving the Market Growth

The growth in the number of surgeries performed globally, specifically orthopaedic, joint replacement, trauma care, and spinal surgeries, is considered an impending growth factor for the surgical helmet market. The patient pool is broadening for surgical treatments as the population ages and more people need care for chronic conditions such as arthritis and osteoporosis. Surgical helmets that are essential to protect against airborne particles and other bodily fluids are being increasingly perceived as personal protective equipment for safety as well as sterility during an operation. An increase in elective surgeries and emergency surgeries around the globe has further raised the requirement for reusable helmet systems and deployable protective consumables.

PubMed estimates that approximately 310 million surgeries are performed each year globally, including 40–50 million in the U.S. and around 20 million in Europe.

-

Technological Advancements in Helmet Systems are Accelerating the Market Growth

Modern surgical helmet systems have developed from simple protective head coverings to provide many essential features, including integrated airflow systems, anti-fog visors, illumination, and friable ergonomic designs to improve surgeon comfort and efficiency. These innovations not only optimize end-user experience but also allow for more effective OR infection prevention. Greater visibility, reduced fatigue during long procedures, and improved airflow for comfort are important advantages that have fueled adoption. With manufacturers investing more and more to validate the performance and safety of helmets through R&D, healthcare facilities are leveling up their next-gen systems.

Stryker has layered on additional airflow and lighting systems to their T7 surgical helmet, and the fact that 71.2% of surgical helmets had integrated LED in 2022 details a solid preference for these high-tech systems.

Restraint

-

High Cost of Advanced Helmet Systems is Restraining the Market from Growing

The high cost of advanced helmet systems that are permanently provided with features such as filtered ventilation, LED lighting, anti-fog visors, and ergonomic head support is one of the major restraints in the surgical helmet market growth. Although these features indeed improve the comfort of users as well as infection control, they come at a steep premium to the systems. In many healthcare facilities—especially for rural hospitals, small clinics, and ambulatory surgical centers—the expense associated with buying and maintaining these helmets may be prohibitively high.

Besides the upfront capital expenses, ongoing expenses are incurred for disposable components, including filters, hoods, and face shields, driving up the total cost of ownership. This reduces adoption, especially in environments with restricted budgets or in underdeveloped countries where hospitals will choose to purchase supplies with more immediate need or cost benefit. This ultimately limits the usage of surgical helmets despite their merits as a safety device because they are expensive end-products that require many resources to implement in many healthcare setups.

Surgical Helmet Market Segmentation Analysis:

By End Use

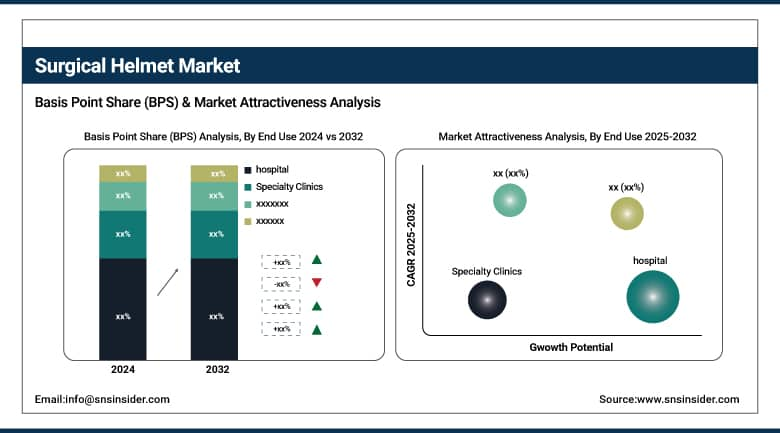

The hospital segment held the largest share in the surgical helmet market with a 50.36% in 2024 due to the high number of surgical procedures carried out in hospitals, especially orthopedic, trauma, and high-risk surgeries. Hospitals generally have bigger surgical units and high foot-falls, resulting in stringent infection control practices and higher protection for surgical personnel. Moreover, hospitals have more accessible financial resources and procurement, so they can purchase more advanced protective equipment (such as surgical helmet systems) and disposable consumables on a routine basis.

The Ambulatory Surgical Centers (ASCs) segment is anticipated to show significant growth during the forecast period due to several surgical procedures being moved from inpatient hospital settings to outpatient facilities. Ambulatory surgical centers (ASCs) feature faster procedure times, reduced costs, and higher efficiency, making them an appealing solution for low-acuity and less invasive surgery. Increasing cases of spinal surgeries have strategically contributed to the higher adoption of surgical helmets as ASCs increase surgical volumes and safety & infection control, a trend expected to continue driving segment growth.

By Product

Increase in preference for single-use protective components, reducing risk of cross-contamination and healthcare-associated infections (HAIs), is driving the disposable consumable segment, which dominated in the surgical helmet market in 2024 with a 16.90% market share. Considering the increasing number of surgeries being performed again, hospitals, surgical centers are focusing on keeping displace face shields, filters, and surgical hood covers for hygiene standards, especially during orthopedic and trauma surgeries. Furthermore, the global expansion of regulatory focus on infection control, coupled with the attractiveness of disposable consumables to reduce cleaning and sterilization cycles, are some added factors contributing towards the growth of this market.

The fastest-growing segment in the surgical helmet market during the forecast period is the helmet system segment, due to continuous helmet design innovations, built-in airflow systems, and other comfort features for users. Due to the growing need for cost-effective, reusable systems with better protection capabilities, hospitals and ambulatory surgical centers are focusing on purchasing advanced helmet systems. Additionally, the continued increase in the number of surgical procedures being performed, coupled with the long-term cost-effectiveness of disposable systems, is driving the growth of the segment in the developed as well as developing healthcare markets.

By Distribution Channel

The offline segment led the surgical helmet market with a 74.2% market share in 2024, driven by the most healthcare institutions prefer purchasing surgical equipment through conventional offline channels, which include various distributors, medical supply stores, and direct company representatives. The channels provide advantages for demonstrating a product, bulk purchase, after-sales service, and having better confirmation about product authenticity and safety standards. Surgical helmets are high-value, safety-critical equipment, and thus, hospitals and surgical centers leverage highly trusted offline networks to procure.

Due to the rapid digitalization of the healthcare industry, the online segment is expected to show substantial growth during the forecast period. Online platforms are gaining popularity for availing medical supplies as they offer ease of purchasing, a wider range of products to choose from, and better pricing. The rise of e-commerce-driven platforms, coupled with logistics and digital purchasing systems, is allowing healthcare facilities (such as small clinics and ambulatory surgical centers) to begin to prepare to transition to online purchasing of surgical helmets and their associated consumables.

Surgical Helmet Market Regional Insights:

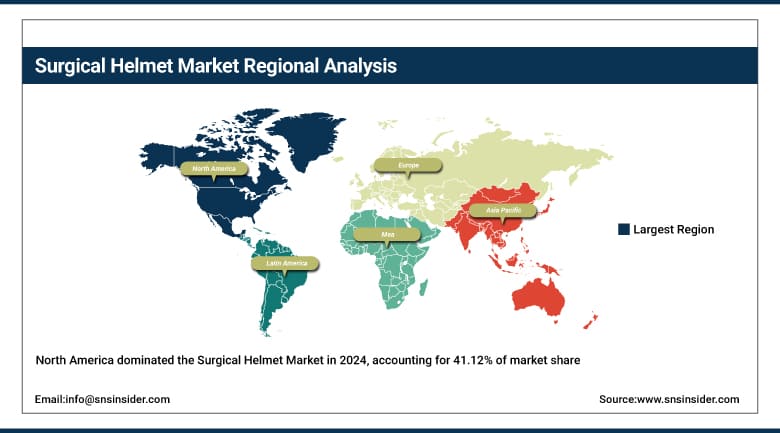

North America dominated the surgical helmet market with a 41.12% market share in 2024 due to the well-established healthcare infrastructure, high surgical volumes, and significant emphasis on infection control in operating rooms. These local key surgical helmet companies include Stryker, Zimmer Biomet, etc., that bring innovations and launch advanced Surgical Helmet Systems. In addition, strict regulation standardization along with the rising awareness pertaining to occupational health and safety amongst surgical personnel has resulted in the adoption of these protective systems among a large segment of the population, such as orthopedic and other high-risk surgical procedures.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific is anticipated to be the significantly growing region in the surgical helmet market with a 7.63% CAGR over the forecast period due to the healthcare expenditure cost, awareness towards infection, and the rising number of surgeries. Hospital development and investment in advanced surgical equipment are rapidly expanding in these countries, with growth in China, India, and Japan. Moreover, government initiatives focused on enhancing the quality of healthcare and increasing the usage of surgical helmets in ambulatory surgical centres are propelling the demand for surgical helmets in the region.

Strong investments in healthcare infrastructure, coupled with increasing surgical volumes and a high focus on infection control among patients and healthcare workers, are driving the surgical helmet market in Europe. The region has a relatively robust regulatory infrastructure and an extensive hospital and clinic network, which are complemented by fast-growing adoption of innovative technologies, especially disposable helmet systems in core German, French, and U.K. markets. the growing elderly population in Europe, coupled with the rising number of orthopedic and trauma surgeries performed in this region, is also expected to continue to boost the demand for high-quality surgical helmets. Continuous innovations in filters, such as filter systems, comfort, design, and disposable availability, are increasing attractiveness and will further support the strong market momentum in 2032.

The Latin American surgical helmet market is growing moderately due to advancements in healthcare infrastructure, increasing awareness pertaining to infection control practices, and a gradual rise in the number of surgical procedures, particularly related to orthopedics and trauma care. An increasing number of people belonging to the middle class and a slowly growing number of private healthcare facilities are urging hospitals and surgical centers to use high-end personal protective devices, including surgical helmets.

Growth in the Middle East & Africa (MEA) region is at a steady pace as healthcare investments grow and there is an increased demand for surgical procedures. However, surgical care capacity is ramping up in nations such as Saudi Arabia, the UAE, and South Africa, and protective surgical apparel is slowly becoming the norm. However, although uneven access to advanced medical technologies persists in the region, increasing initiatives for improving surgical safety and overdose prevention are promoting the surgical helmet market analysis growth of the region.

Surgical Helmet Market Key Players:

-

Stryker Corporation

-

Zimmer Biomet Holdings

-

Ecolab Inc.

-

THI Total Healthcare Innovation GmbH

-

Tronex International

-

Sentinelle Medical

-

Cardinal Health

-

Orthopaedic Innovations

Recent Developments

-

March 2025 – Stryker, a leading global medical technology company, released details of its newest personal protective equipment (PPE) innovation, the Steri-Shield 8 Personal Protection System. Engineered from years of research, testing, and consultation with actual front-line healthcare providers, Steri-Shield 8 is a breakthrough in surgical safety and infection control.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.09 Billion |

| Market Size by 2032 | USD 1.95 Billion |

| CAGR | CAGR of 7.60% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Helmet System, Disposable Consumable) • By End Use (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics) • By Distribution Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Stryker Corporation, Zimmer Biomet Holdings, Ecolab Inc., DuPont de Nemours, THI Total Healthcare Innovation GmbH, Tronex International, Sentinelle Medical, Cardinal Health, Tidi Products, Orthopaedic Innovations, and other players. |

Frequently Asked Questions

North America dominated the Surgical Helmet Market in 2024.

The “Disposable Consumable” segment dominated the Surgical Helmet Market.

Technological advancements in helmet systems are accelerating the market growth.

The Surgical Helmet Market was USD 1.09 billion in 2024 and is expected to reach USD 1.95 billion by 2032.

The Surgical Helmet Market is expected to grow at a CAGR of 7.60% from 2025 to 2032.

Get in Touch