Personal Protective Equipment Market Report Scope and Overview:

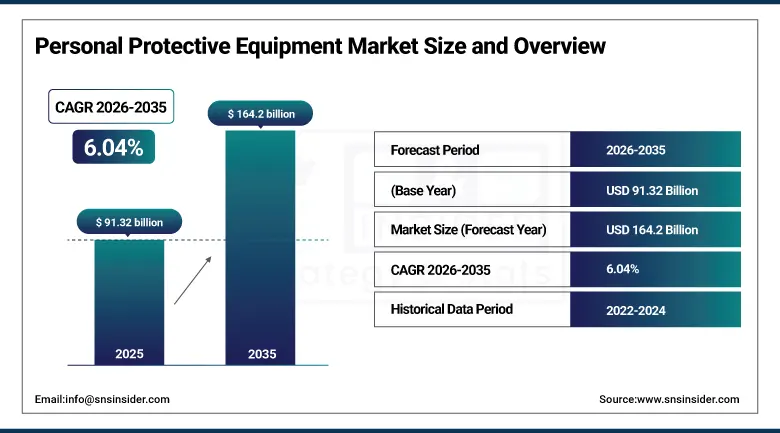

The Personal Protective Equipment Market was valued at USD 91.32 billion in 2025 and is expected to reach USD 164.2 billion by 2035, growing at a CAGR of 6.04% from 2026 to 2035.

Personal protective equipment has always occupied a quiet but indispensable role in global commerce. Every sector that deals with physical risk relies on it — whether that is a construction worker navigating a high-rise project, a chemical plant operator managing hazardous materials, a healthcare professional working in an intensive care unit, or a miner operating hundreds of meters below the earth's surface. What has changed in recent years is the degree to which governments, employers, and workers themselves have elevated safety from a compliance obligation to a genuine organizational priority. That shift in attitude, backed by stricter regulatory enforcement and growing evidence of the economic cost of workplace injuries, is one of the foundational reasons the personal protective equipment market is on a sustained growth trajectory that stretches well beyond any single economic cycle.

The scale of global industrialization underway across Asia Pacific, the Middle East, and Latin America is adding another powerful layer to the demand picture. Billions of dollars in infrastructure, mining, energy, and manufacturing investment across these regions require large workforces operating in conditions that demand appropriate protective equipment. China, India, Indonesia, and Vietnam — all of which are experiencing rapid industrial expansion — are seeing corresponding growth in institutional PPE procurement at a pace that North American and European markets, which are more mature, cannot replicate on their own. The net result is a global market that is broadening its demand base geographically even as it deepens product sophistication in established markets.

Personal Protective Equipment Market Size and Forecast

-

Market Size in 2025: USD 91.32 Billion

-

Market Size by 2035: USD 164.2 Billion

-

CAGR: 6.04% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get more information on Personal Protective Equipment Market - Request Free Sample Report

Personal Protective Equipment Market Trends

-

Growing adoption of smart and connected PPE platforms embedded with IoT sensors, GPS tracking, and real time biometric monitoring enabling proactive hazard detection and worker safety management.

-

Increasing regulatory stringency across global jurisdictions, including updates to OSHA standards in North America, EU-OSHA directives in Europe, and new national safety mandates in rapidly industrializing Asian economies.

-

Rising demand for lightweight, breathable, and ergonomically advanced PPE designs that improve worker comfort and compliance without compromising protection standards during extended wear periods.

-

Accelerating adoption of sustainable and eco-friendly PPE materials, including recycled polymers, biodegradable composites, and reduced-chemical formulations, responding to corporate ESG commitments and regulatory environmental standards.

-

Expanding healthcare PPE demand driven by heightened institutional infection control awareness post-pandemic and increasing healthcare worker safety protocols in hospitals, clinics, and long-term care facilities.

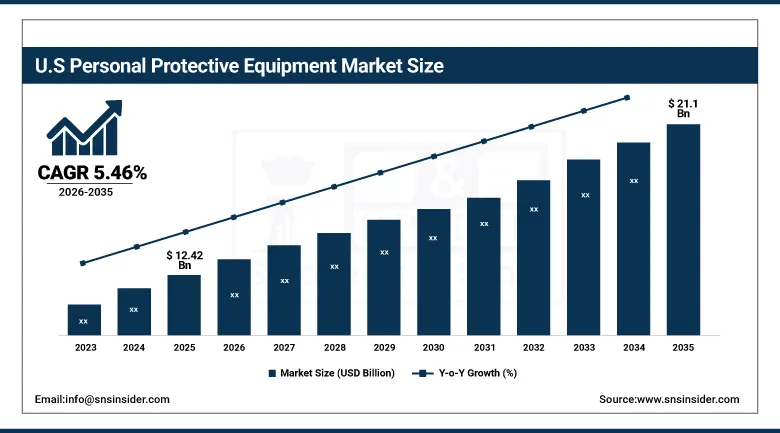

U.S. Personal Protective Equipment Market was valued at USD 12.42 billion in 2025 and is expected to reach USD 21.1 billion by 2035, registering a CAGR of 5.46% during 2026 to 2035.

The United States commands the largest share of the North American PPE market by a considerable margin, and it is one of the most well-regulated and technologically sophisticated PPE markets in the world. OSHA's regulatory framework establishes legally enforceable standards that require employers across construction, manufacturing, healthcare, and hazardous chemical environments to provide appropriate protective equipment as a matter of law. The consequence is a procurement base that is non-discretionary in character: regardless of economic cycle, companies operating in regulated industries must maintain compliant PPE inventories, creating a baseline level of demand resilience that few product categories enjoy. The ongoing legal and regulatory scrutiny that followed several high-profile industrial accidents in the 2010s and early 2020s further reinforced institutional commitment to PPE investment in American industry.

The healthcare industry in the United States represents another important element within the domestic market for PPE that has illustrated its capacity to grow during times of crisis during the COVID-19 pandemic. The governmental response involving the establishment of national stockpiles, domestic production, and diversification of procurement sources has led to the emergence of a more sustainable healthcare PPE market infrastructure post-COVID. In addition to the healthcare industry, the rise of construction activity in line with the provisions of the Infrastructure Investment and Jobs Act and the CHIPS and Science Act provides an increase in demand for construction PPE.

Personal Protective Equipment Market Segment Insights

-

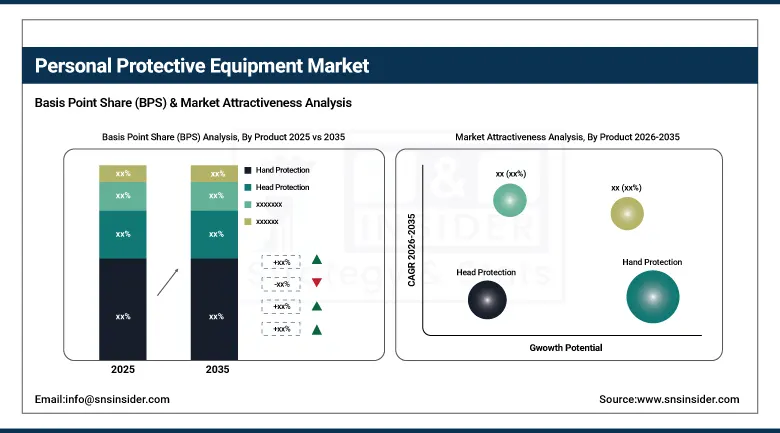

Based on Product, Hand Protection accounted for the largest market share of approximately 28.02% in 2025. Respiratory Protection is expected to be the fastest-growing product segment through 2035.

-

Based on End Use, Manufacturing accounted for the largest market share in 2025, given the high volume of industrial workers requiring comprehensive PPE coverage. Construction is expected to be the fastest-growing end use segment through 2035.

Personal Protective Equipment Market Segment Analysis

By Product, Hand Protection segment dominates the Personal Protective Equipment Market, Respiratory Protection segment expected to grow fastest

Hand protection holds the commanding lead in the personal protective equipment product landscape, accounting for approximately 28% of total market revenue in 2025. The reasoning behind this dominance is straightforward: hand injuries are among the most common and costly occupational injuries across virtually every major industry sector. From cuts and lacerations in food processing and manufacturing environments to chemical burns in laboratory and industrial settings, and thermal injuries in construction and metalworking, the hand is exposed to a remarkable diversity of workplace hazards that require equally diverse protective solutions. The companies making protective gloves have developed a wide range of products including single-use nitrile gloves for medical purposes, cut-proof engineered fiber gloves for assembly in factories, chemical resistant gloves made out of neoprene rubber for working with chemicals, and insulated gloves for electrical applications. Improvements to ergonomics, better grip surfaces, and thinner materials have enabled their use not just in industries but in food services, hospitality, and facilities maintenance as well.

Respiratory Protection holds the potential to witness the fastest CAGR during 2026-2035. There are many factors working behind the trend. Respiratory health has become a rising issue in the wake of increasing air pollution caused by industries, forest fires, and urban particulate matter, making respiratory protection solutions more common than ever before even outside occupational uses in industries. High-end efficiency respirators are still required at higher levels by the healthcare sector post the pandemic than were observed before the outbreak. Industries that are facing challenges of silica dust exposure, asbestos management, isocyanate exposure, and hazardous chemical aerosol exposure are now under the scope of stringent laws requiring respiratory protection equipment. The invention of reusable cartridges with respirators that are light and easy to wear can address this problem.

By End Use, Manufacturing segment dominates the Personal Protective Equipment Market, Construction segment expected to grow fastest

Manufacturing maintained its position as the dominant end use sector for personal protective equipment in 2025, a status reflecting both the scale of global manufacturing employment and the diversity of physical hazards that industrial production environments generate. Automotive assembly plants, electronics fabrication facilities, food processing operations, steel and aluminum production, textile manufacturing, and pharmaceutical production all create distinct combinations of physical, chemical, thermal, and ergonomic risks that require comprehensive PPE programs covering hand, eye, head, respiratory, and body protection. As manufacturing capacity expands in Asia Pacific and nearshoring trends bring new production investment to North America and Mexico, manufacturing sector PPE demand is growing on two fronts: new facility buildout procurement and ongoing consumable replenishment in existing operations.

Construction is expected to register the fastest CAGR among all end use sectors from 2026 to 2035. The global pipeline of infrastructure, residential, and commercial construction investment is massive and sustained. Government-backed infrastructure programs in the United States, India, the European Union, and across Southeast Asia are committing trillions of dollars to projects that require large construction workforces operating in hazardous environments. Fall protection harnesses, hard hats, safety footwear, high-visibility clothing, and eye protection are all consumed in high volumes on active construction sites, and expanding project activity directly translates to PPE demand growth. The increasing use of powered industrial equipment, elevated work platforms, and complex multi-trade coordination in modern construction is also driving demand for more sophisticated protective equipment than traditional construction sites historically required.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~74% |

|

Europe |

Germany |

~27% |

|

Asia Pacific |

China |

~44% |

|

Middle East and Africa |

UAE |

~30% |

|

Latin America |

Brazil |

~50% |

Europe Personal Protective Equipment Market Insights

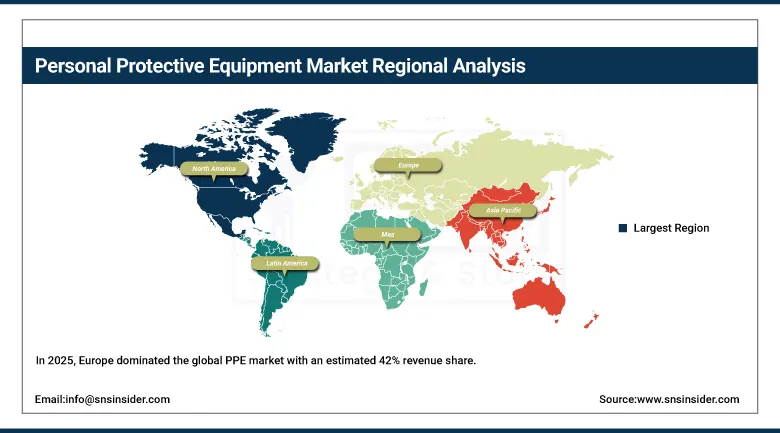

The Europe personal protective equipment market dominated the worldwide PPE market in 2025, with its revenue share estimated to be roughly 42% of the total global market. The dominance of Europe can be attributed to the very stringent regulation environment when it comes to occupational health and safety regulations. The European Agency for Safety and Health at Work ensures comprehensive implementation of directive on usage of PPE within the entire EU countries, while some of the largest industrial economies, like Germany, France, United Kingdom, Italy, and the Netherlands ensure stringent national regulations that create no room for discussion on need for quality protective equipment within the construction, manufacturing, chemicals, and health industries. The German industry companies are known for having stringent PPE programs, while German engineering and chemical manufacturing industries continue to buy PPE regularly and to very high specifications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Personal Protective Equipment Market Insights

Asia Pacific is the fastest growing regional market for personal protective equipment, driven by the massive amount of industrialization and rapid growth in the region. Asia Pacific accounts for a significant share of the growth in the demand for personal protective equipment due to the large workforce in its industries and the regulation introduced by its governments to minimize workplace injuries. The Occupational Safety, Health and Working Conditions Code of India has made it easier for companies operating in Indian industries to comply with the regulations on PPEs, and the enforcement of these regulations is increasingly becoming stricter. In China, the industrial safety regulations have become increasingly stringent over the last ten years, and the manufacturers and constructors face severe punishment for failing to comply. Other Southeast Asian countries such as Vietnam, Indonesia, Thailand, and the Philippines have also experienced rapid industrial growth coupled with rising labor safety consciousness.

North America Personal Protective Equipment Market Insights

In 2025, North America accounted for a significant portion of the global PPE market, with the USA contributing significantly. The advantage of the US market is the presence of stringent OSHA standards concerning PPE use, high employer liability awareness, and an established supply chain, which includes national distributors, GPO contracting for hospitals, and a direct channel of communication with major manufacturers. Canada offers a strong contribution to the market due to its highly developed occupational health and safety legislation and standards. The Mexican market continues to increase its importance as a result of expanding capacity of production due to nearshoring and diversified trading relationships leading to the formation of new PPE markets in Bajio and northern borders of Mexico.

Middle East and Africa and Latin America Personal Protective Equipment Market Insights

The Middle East and Africa and Latin America markets for personal protective equipment are experiencing above-average growth, driven by sustained energy sector activity, infrastructure development, and improving occupational safety regulatory enforcement. The Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are large PPE consumers given the scale of oil and gas operations, construction activity tied to Vision 2030 programs, and the large industrial workforce operating across the petrochemical and logistics sectors. South Africa represents the largest sub-Saharan PPE market, driven by mining, manufacturing, and construction sectors. Brazil is the PPE market leader in Latin America, supported by its large and diverse industrial base spanning agriculture, mining, manufacturing, and oil production. Both regions are expected to sustain consistent PPE market growth through 2035 as industrial investment continues and safety regulation matures.

Personal Protective Equipment Market Growth Drivers:

-

Stringent global occupational safety regulations and rising workplace safety awareness creating sustained non-discretionary PPE demand

The most consistent and reliable driving factor behind the market for personal protective equipment is the regulatory requirement. In many major industrial countries, regulations have been put in place, making it obligatory for organizations to carry out hazard assessments and supply suitable protective equipment to workers who are subjected to such hazards. Failure to comply with such requirements entails financial and even criminal penalties in some cases, as the executives might be held responsible in case of non-compliance. Since there is a mandatory legal provision requiring organizations to have their own PPE program, there will always be a demand floor for the industry that cannot be affected by fluctuations within the economic environment. Apart from the basic requirement, the mounting evidence indicating benefits of such a program including low employee absenteeism, less workers' compensation claims, and higher productivity among other positive results of implementing a good protective equipment program encourages organizations to voluntarily purchase better PPE than they are required by the regulations.

Personal Protective Equipment Market Restraints

-

Price sensitivity in developing markets and counterfeit product circulation undermining safety standards and market integrity

A meaningful restraint on the personal protective equipment market is the persistent circulation of substandard and counterfeit PPE products, particularly in developing markets where procurement decisions are heavily influenced by unit cost rather than certified performance standards. Counterfeit safety helmets, respirators, gloves, and high-visibility garments that do not meet applicable safety certifications but are marketed and sold as compliant products represent a genuine threat to worker safety and create unfair competitive pressure for legitimate manufacturers. The problem is compounded by the complexity of global PPE supply chains, which span multiple countries and trading relationships that are difficult for regulatory authorities to monitor comprehensively. In markets with limited inspection and enforcement capacity, substandard products can achieve significant market penetration before being detected and removed. For legitimate manufacturers, particularly those producing premium, innovation-driven products, competing against artificially low-cost non-compliant alternatives in price-sensitive markets is a structural challenge that suppresses revenue potential and investment returns.

Personal Protective Equipment Market Opportunities

-

Smart PPE integration, emerging market penetration, and sustainable product innovation creating high-value growth opportunities

The integration of digital technology into personal protective equipment represents the most transformative long-term growth opportunity for the PPE industry through 2035. Smart helmets equipped with heads-up displays, environmental sensors, and communication systems are transitioning from innovation showcase items to operational procurement targets for major construction and mining companies. Connected safety vests and wristbands that monitor worker location, posture, heart rate, and ambient temperature are being piloted in large industrial facilities where real-time safety data can be acted upon to prevent incidents before they occur. The market for IoT-enabled PPE is in its early stages, but its growth potential is significant given the size of the addressable installed base across global industry. Manufacturers that successfully transition from hardware suppliers to safety data platform providers will be positioned to capture recurring software and connectivity revenue that is structurally distinct from and more valuable than traditional equipment replacement cycles. Sustainable product innovation — including PPE made from recycled materials, designed for end-of-life recyclability, and produced with lower carbon intensity manufacturing processes — is creating premium market positioning opportunities as corporate buyers integrate supply chain sustainability criteria into procurement decisions.

Recent Developments:

-

November 2024: Honeywell International completed the sale of its Personal Protective Equipment business to Protective Industrial Products for USD 1.33 billion in cash. The divested unit included major brands such as Fendall, Fibre-Metal, Howard Leight, and KCL, along with operations across 20 manufacturing and 17 distribution facilities globally. The transaction marked Honeywell's full exit from the PPE market as part of a broader portfolio rationalization strategy.

-

October 2024: 3M Company completed the separation of its Safety and Industrial segment healthcare PPE business, reflecting the company's continued portfolio optimization strategy. The reorganization was designed to improve operational focus and capital allocation across 3M's diversified technology businesses while ensuring the PPE operations retained dedicated commercial leadership and investment resources.

Personal Protective Equipment Market Key Players

-

3M Company

-

Honeywell International Inc.

-

DuPont de Nemours Inc.

-

Ansell Limited

-

MSA Safety Incorporated

-

Delta Plus Group

-

Kimberly-Clark Corporation

-

Lakeland Industries Inc.

-

Uvex Group

-

Supermax Corporation Berhad

-

Bullard

-

Avon Rubber plc

-

Protective Industrial Products Inc.

-

Radians Inc.

-

Moldex-Metric Inc.

-

Ergodyne (Tenacious Holdings Inc.)

-

MCR Safety

-

Portwest Ltd.

-

Alpha Pro Tech Ltd.

-

Sioen Industries NV

Personal Protective Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 91.32 Billion |

| Market Size by 2035 | USD 164.2 Billion |

| CAGR | CAGR of 6.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Hand Protection, Head Protection, Eye and Face Protection, Respiratory Protection, Protective Clothing, Foot and Leg Protection, Hearing Protection, Others) • By End Use (Manufacturing, Construction, Oil and Gas, Healthcare, Mining, Food and Beverage, Chemicals, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | 3M Company, Honeywell International Inc., DuPont de Nemours Inc., Ansell Limited, MSA Safety Incorporated, Delta Plus Group, Kimberly-Clark Corporation, Lakeland Industries Inc., Uvex Group, Supermax Corporation Berhad, Bullard, Avon Rubber plc, Protective Industrial Products Inc., Radians Inc., Moldex-Metric Inc., Ergodyne (Tenacious Holdings Inc.), MCR Safety, Portwest Ltd., Alpha Pro Tech Ltd., Sioen Industries NV |

Frequently Asked Questions

Hand Protection dominated the Personal Protective Equipment Market in 2025, accounting for approximately 28.02% of total market revenue, driven by the high frequency of hand injury risk across manufacturing, construction, healthcare, and chemical processing industries globally.

Europe dominated the Personal Protective Equipment Market in 2025, accounting for approximately 42% of global market revenue, supported by stringent EU-OSHA occupational safety directives, high industrial employment across Germany, France, and the UK, and a mature culture of regulatory compliance in workplace safety management.

Stringent global occupational safety regulations creating non-discretionary PPE demand, combined with rapid industrialization in emerging markets, increasing construction and infrastructure spending, and the integration of smart connected technologies into next-generation PPE platforms.

The Personal Protective Equipment Market was valued at USD 91.32 billion in 2025.

The Personal Protective Equipment Market is expected to grow at a CAGR of 6.04% from 2026 to 2035.

Get in Touch