Trocars Market Report Scope & Overview:

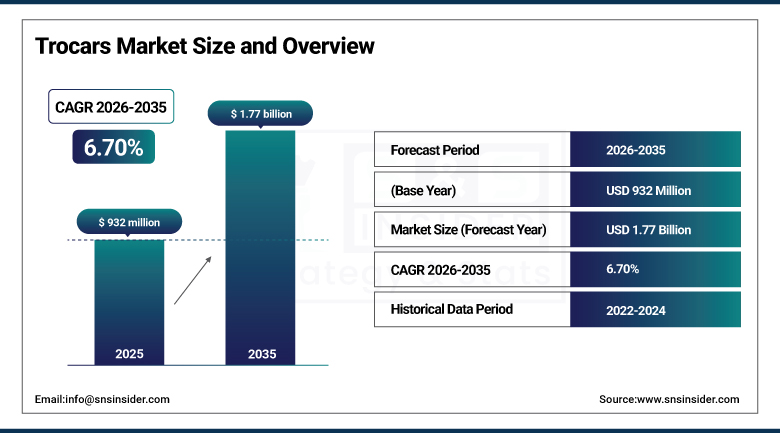

The Trocars Market was valued at USD 932 million in 2025 and is expected to reach USD 1.77 billion by 2035, growing at a CAGR of 6.70% from 2026-2035.

The Trocars Market is experiencing growth owing to the rising uptake of minimally invasive surgery, the incidence of chronic conditions, and the number of surgeries performed worldwide. The technological innovation in trocar design, enhanced safety measures, the development of healthcare facilities, and the growing preference for faster recovery and shorter hospital stays have contributed to market growth.

The World Health Organization's global surgical volume data documents that over 313 million surgical procedures are performed annually worldwide, with laparoscopic approaches now accounting for approximately 30-40% of all abdominal surgical procedures in high-income countries. More than 13 million laparoscopic procedures are performed annually globally, each requiring between 2-5 trocar placements, creating aggregate trocar consumption volumes that reflect the market's scale.

Trocars Market Size and Forecast

-

Market Size in 2025: USD 932 Million

-

Market Size by 2035: USD 1.77 Billion

-

CAGR: 6.70% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Trocars Market - Request Free Sample Report

Trocars Market Trends

-

Robotic surgery platform adoption is creating demand for specialized trocar systems with robotic instrument docking compatibility, as DaVinci Xi and Intuitive Sense robotic cases require dedicated trocar systems optimized for robotic arm attachment.

-

Single-incision laparoscopic surgery (SILS) and reduced-port techniques are driving demand for specialized single-site trocar ports that consolidate multiple instruments through a single umbilical access point.

-

Integrated trocar and haemostatic valve designs are improving instrument exchange speed and reducing gas leakage during laparoscopic procedures where frequent instrument changes are required.

-

Radially expanding sleeve trocars that dilate tissue without cutting are reducing port-site hernia risk compared to conventional cutting trocars by preserving fascial integrity rather than creating cut defects.

-

Infection control regulations tightened post-COVID-19 are accelerating hospital conversion from reusable to disposable trocars, where the sterilization process complexity and contamination risk of reusable devices has become a documented infection control concern.

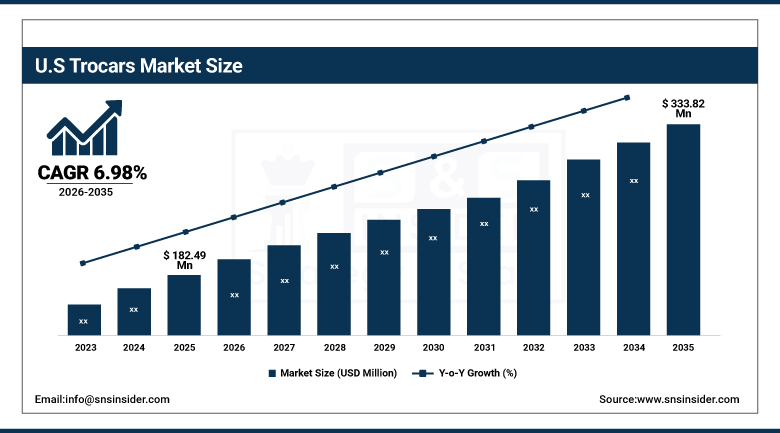

U.S. Trocars Market was valued at USD 182.49 million in 2025 and is expected to reach USD 333.82 million by 2035, growing at a CAGR of 6.98%.

The U.S. Trocars Market will see consistent growth owing to a large number of minimally invasive surgeries, sophisticated healthcare infrastructure, and increased acceptance of novel surgical equipment. Growing instances of chronic disease cases, skilled surgeons, and increased demands for quick recovery surgeries drive market growth.

The American College of Surgeons documents that laparoscopic cholecystectomy the standard treatment for symptomatic gallbladder disease is the most commonly performed elective laparoscopic procedure in the U.S. with over 700,000 cases annually, each requiring 3-4 trocar placements.

Trocars Market Segment Analysis

-

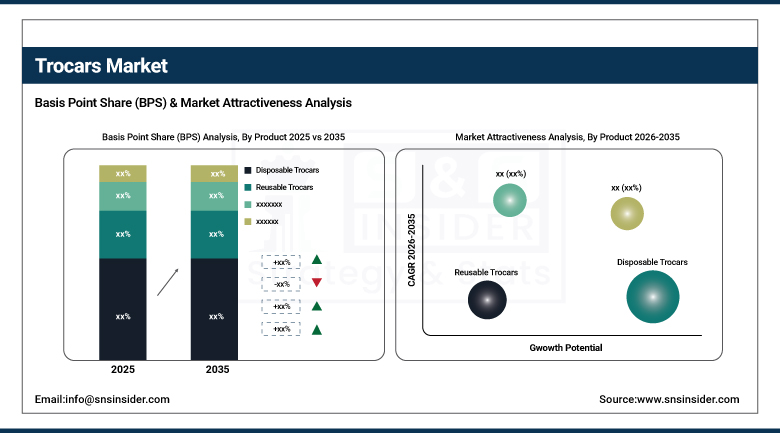

By Product, Disposable Trocars dominated with ~62.86% share in 2025; Reusable Trocars maintaining position in cost-conscious markets.

-

By Type, Bladeless Trocars dominated with ~45.32% share in 2025; Optical Trocars growing for visualization-guided access.

-

By Application, General Surgery dominated and expected to maintain fastest CAGR through forecast period.

-

By End-User, Hospitals dominated the Trocars Market in 2025; Ambulatory Surgical Centers growing fastest.

By Product: Disposable dominates, growing with infection control mandates

Disposable Trocars held approximately 62.86% of the Trocars Market in 2025, driven by the documented infection control advantages of single-use devices over reprocessed reusable alternatives. Hospital infection control programs which became dramatically more rigorous following COVID-19 have accelerated the institutional shift from reusable to disposable surgical instruments across multiple device categories including trocars. WHO data from 2024 indicates that 78% of hospitals in Europe and North America had transitioned to single-use surgical tools for specific categories, with trocars among the instruments most commonly cited in single-use conversion programs. The economics of reusable trocar sterilization including instrument cleaning labor, autoclave energy cost, documentation requirements, and device replacement when damage occurs are increasingly visible to hospital value analysis committees conducting total cost of ownership comparisons that favor disposables at moderate-to-high procedure volumes.

Reusable Trocars maintain a market position in procedure volumes below the economic crossover point where single-use economics become clearly favorable, and in healthcare systems of developing economies where device budgets make reusable instruments a financial necessity rather than a preference. The improvement in reusable trocar design including more surgically aggressive blade profiles, ergonomic handle designs, and improved seal mechanisms that reduce gas leak during instrument exchange sustains clinical preference for reusable systems among surgeons who appreciate their specific performance characteristics over disposable alternatives.

By Type: Bladeless dominates, Optical Trocars growing

Bladeless Trocars held approximately 45.32% of the Trocars Market in 2025 and are expected to maintain their dominant type position through the forecast period. Bladeless designs which use blunt conical or radially expanding obturators that dilate tissue rather than cut it offer a compelling clinical safety profile: by displacing muscle fibers rather than cutting them, bladeless trocars reduce port-site bleeding, reduce port-site hernia risk, and generally require less effort to remove at procedure end because tissue recoil is minimal. The clinical outcome data supporting bladeless trocar advantages over cutting bladed designs has accumulated sufficiently to make bladeless the preferred specification for general, gynecological, and bariatric applications where the abdominal wall is healthy and amenable to dilation.

Optical Trocars which incorporate a clear plastic obturator through which a 0-degree laparoscope can be inserted to provide direct visual access to the tissue layers being traversed during trocar insertion are growing in adoption as the trocar access safety concern has become more prominent in laparoscopic safety literature. Inadvertent vessel and bowel injury during trocar insertion though rare is one of the most serious laparoscopic complications, and optical access trocars address this risk by allowing the surgeon to see each tissue layer as it is entered rather than relying on tactile feedback alone. Major trauma centers, high-acuity surgical programs, and surgeons performing laparoscopy on patients with significant abdominal adhesion risk are the primary adopters.

Trocars Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

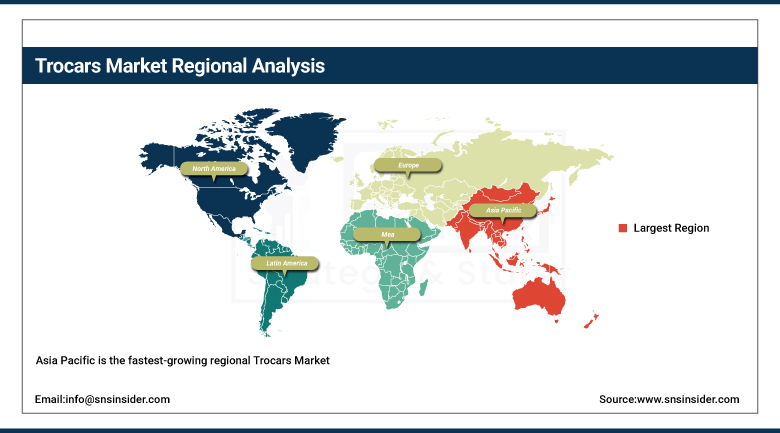

Asia Pacific Trocars Market Insights

Asia Pacific is the fastest-growing regional Trocars Market with an expected CAGR of 7.79% the highest of any region driven by increasing healthcare expenditure, expanding hospital infrastructure, growing surgical procedure volumes across China, India, Japan, and Southeast Asia, and the medical tourism industry that concentrates high-acuity laparoscopic cases at facilities in Thailand, South Korea, and India. China's hospital construction program adding thousands of new hospital beds annually is creating greenfield laparoscopic equipment installation demand. India's growing surgical specialist workforce, trained at facilities increasingly equipped with laparoscopic towers, is expanding the volume of minimally invasive procedures performed domestically. The growth of local trocar manufacturers in China and India is making laparoscopic access devices more affordable at volume levels suited to these markets.

China's National Health Commission 2023 report documents that minimally invasive surgical procedures grew at 18% annually over the preceding five years across the country's public hospital system, reflecting the rapid adoption of laparoscopic technique training by China's expanding surgical workforce. India's growing medical tourism industry which attracted 700,000 international medical visitors in 2023 concentrates laparoscopic bariatric, gynecological, and urological procedures at facilities whose procedure volumes justify premium trocar procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Trocars Market Insights

Europe holds a significant Trocars Market position, with Germany, France, the UK, and the Nordic countries as primary markets. European hospitals have been early adopters of advanced minimally invasive surgical techniques, and Europe's aging demographic requiring more elective laparoscopic procedures for age-associated conditions sustains growing procedure volumes. The EU Needlestick Injury Directive's safety-engineered device requirements, while primarily focused on blood collection, have established institutional preference for single-use safety-engineered surgical instruments that extends to trocar procurement decisions. European trocar manufacturers including Karl Storz (Germany) and Olympus contribute to the region's supply-side sophistication.

Market Growth Drivers:

-

Minimally invasive surgery adoption growth and disposable device safety mandates driving global trocars market expansion

The trocars market's growth follows the minimally invasive surgery expansion curve, which is itself driven by outcomes data that consistently demonstrates laparoscopic approaches superiority over open surgery across the procedure categories where the techniques have been compared. Hospital administrators focused on length-of-stay reduction see laparoscopic surgery as a key discharge acceleration tool. Surgeons trained in minimally invasive technique prefer it for its precision and enhanced visualization. Patients who have experienced laparoscopic recovery recognize the difference and request it. Payers who reimburse care at bundled procedure rates see the same or better clinical outcomes at lower total hospitalization cost. These aligned incentives across every stakeholder in the surgical value chain sustain demand growth that is unlikely to reverse, creating a market whose underlying volume demand is structurally secure.

Market Restraints:

-

High cost of advanced trocar systems and robotic surgery compatibility requirements creating adoption barriers in cost-sensitive markets

Advanced trocar systems particularly robotic surgery-compatible trocars and single-site access systems command premium pricing that creates adoption barriers in healthcare systems where surgical supply budgets are tightly managed. Standard disposable trocars are a commodity in pricing terms, but specialty systems for robotic surgery and SILS applications can cost 3-5x standard disposable equivalents, creating value analysis scrutiny that delays adoption. In developing markets where reimbursement for minimally invasive procedures does not incorporate the device cost differential over open surgery disposables, hospitals face budget constraints that slow the transition from reusable to disposable trocar systems.

Market Opportunities:

-

Robotic surgery integration and emerging market healthcare expansion creating significant trocars market growth opportunities

Robotic surgery represents the most commercially important near-term growth opportunity for premium trocar products. As DaVinci Xi, Hugo RAS, and Versius robotic surgery systems expand their installed base globally, the demand for robotically compatible trocar systems which must accommodate robotic arm docking attachment and provide the stability required for robotic instrument precision grows proportionally with robotic system deployment. Intuitive Surgical's USD 1.85 billion in 2023 instrument and accessory revenue includes significant trocar-related consumable revenue. Emerging market healthcare expansion particularly in China, India, Southeast Asia, and Sub-Saharan Africa represents volume demand growth as growing surgical infrastructure investments bring laparoscopic capability to populations where it has previously been limited by facility and workforce constraints.

Recent Developments:

-

2025: Medtronic launched its Signia Tri-Staple 2.0 laparoscopic trocar system with integrated tissue thickness sensing that automatically adjusts trocar entry force based on real-time abdominal wall thickness measurement, reducing unintended vessel and bowel entry risk during trocar placement reporting a 31% reduction in port-site complications in 500-patient clinical validation across five major academic medical centers.

-

2025: Applied Medical introduced its Kii Balloon Blunt Tip trocar system with a radially expanding balloon dilator that is fully resorbed within the abdominal wall after trocar removal, eliminating the port-site defect that conventional trocars create and reducing port-site hernia incidence to less than 0.1% in 1,200-patient prospective multicenter evaluation.

Trocars Market Key Players

Some of the Trocars Market Companies

-

Medtronic plc

-

Johnson & Johnson MedTech (Ethicon)

-

Stryker Corporation

-

Applied Medical Resources Corp.

-

B. Braun Melsungen AG

-

Olympus Corporation

-

Karl Storz SE & Co. KG

-

CONMED Corporation

-

Teleflex Incorporated

-

Genicon Inc.

-

Ovesco Endoscopy AG

-

Ackermann Instrumente GmbH

-

Covidien (Medtronic)

-

Surgiquest Inc. (Conmed)

-

Lagis Enterprise Co. Ltd.

-

Grena Ltd.

-

Pajunk Medical Products

-

Unimax Medical Systems

-

Endopath (Ethicon)

-

NovaBay Pharmaceuticals

Trocars Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 932 Million |

| Market Size by 2035 | USD 1.77 Billion |

| CAGR | CAGR of 6.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Disposable Trocars, Reusable Trocars) • By Type (Bladeless Trocars, Optical Trocars, Blunt Trocars, Bladed Trocars) • By Application (General Surgery, Gynecology, Bariatric Surgery, Urology, Others) • By End-User (Hospitals, Ambulatory Surgical Centers, Clinics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Johnson & Johnson MedTech (Ethicon), Stryker Corporation, Applied Medical Resources Corp., B. Braun Melsungen AG, Olympus Corporation, Karl Storz SE & Co. KG, CONMED Corporation, Teleflex Incorporated, Genicon Inc., Ovesco Endoscopy AG, Ackermann Instrumente GmbH, Covidien (Medtronic), Surgiquest Inc. (Conmed), Lagis Enterprise Co. Ltd., Grena Ltd., Pajunk Medical Products, Unimax Medical Systems, Endopath (Ethicon), NovaBay Pharmaceuticals. |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 7.79% in the Trocars Market.

Bladeless Trocars dominated with approximately 45.32% share in 2025.

Disposable Trocars dominated with approximately 62.86% share in 2025.

The Trocars Market was valued at USD 932 million in 2025.

The Trocars Market is expected to grow at a CAGR of 6.70% from 2026 to 2035.

Get in Touch