Minimally Invasive Surgery Market Report Scope & Overview:

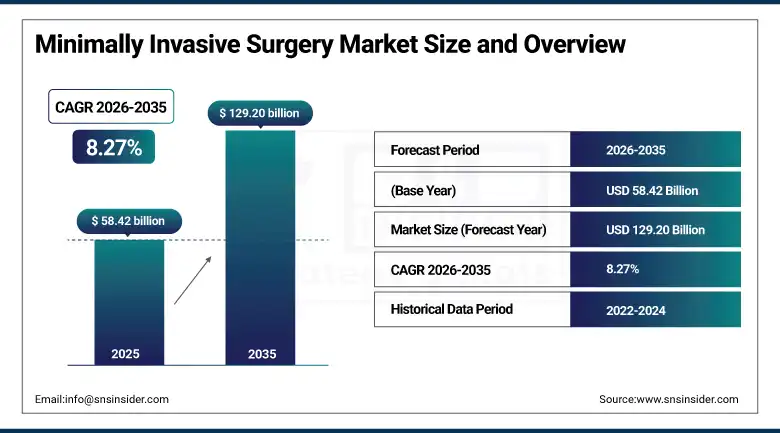

The Minimally Invasive Surgery Market was valued at USD 58.42 Billion in 2025 and is expected to reach USD 129.20 Billion by 2035, growing at a CAGR of 8.27% from 2026 to 2035.

The application of minimal invasive surgery techniques has revolutionized the field of clinical practice by substituting large open wounds with smaller access portals that facilitate the introduction of miniature equipment, cameras, and energy devices for performing complicated surgical interventions with less patient morbidity. Indeed, the business case and clinical evidence of the transformation are well-supported. Those patients who undergo minimal invasive interventions show considerably shorter periods of stay in the hospital, much lesser blood loss, a smaller number of infections during recovery, quicker return to routine activities, and decreased need for medications. In terms of finances, the hospital benefits from the reduction in patient stays in hospital beds, the cost of complications requiring additional visits to the institution, and more efficient performance due to quicker patient recoveries and bed turnover. The simultaneous emergence of robotic surgery, artificial intelligence imaging systems, and modern energy devices with tissue sensing abilities is gradually increasing the limits of the possible complexity of minimally invasive surgeries.

Intuitive Surgical reported that its da Vinci robotic surgical system surpassed 14 million total cumulative robotic-assisted procedures globally in early 2025, with procedure volume growing at approximately 17% year over year as the installed base of da Vinci systems expands into new geographies and surgical specialties beyond its established urology and gynecology strongholds.

Market Size and Forecast

-

Market Size in 2026E: USD 63.25 Billion

-

Market Size by 2035: USD 129.20 Billion

-

CAGR: 8.27% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Minimally Invasive Surgery Market - Request Free Sample Report

Minimally Invasive Surgery Market Trends

-

Adoption of robotic surgical systems is expanding across hospitals and ambulatory surgical centers due to declining system costs and improved clinical training availability.

-

AI-powered imaging and augmented reality platforms are improving surgical precision, visualization, and outcomes during minimally invasive procedures.

-

Advancements in single-port and natural orifice surgeries are reducing patient trauma and recovery time beyond traditional laparoscopic procedures.

-

Increasing shift toward outpatient and ambulatory surgical centers is driving demand for cost-efficient minimally invasive procedures.

-

Flexible robotic and endoluminal devices are enabling minimally invasive treatment in hard-to-access anatomical regions.

The U.S. Minimally Invasive Surgery Market Outlook

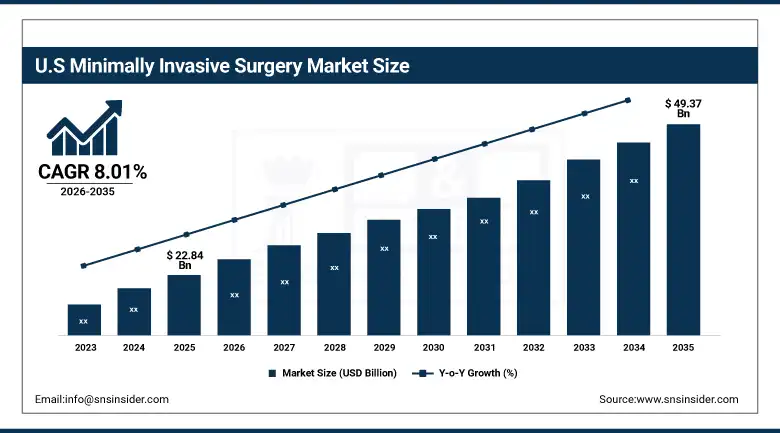

The U.S. Minimally Invasive Surgery Market was valued at approximately USD 22.84 Billion in 2025 and is expected to reach approximately USD 49.37 Billion by 2035, growing at a CAGR of approximately 8.01%.

The United States is considered the world leader in terms of both commercial development and size of the minimally invasive surgery market, featuring the highest number of surgical robotics per capita among countries worldwide, the world’s most developed ambulatory surgical centers network, an excellent payment system for minimally invasive procedures that exists both in the private and government spheres, and the most developed companies providing innovative technologies for performing surgical procedures (such as Intuitive Surgical, Medtronic, Abbott, and Johnson & Johnson MedTech). It should be mentioned that, as part of the Centers for Medicare and Medicaid Services, reimbursements have been shifting increasingly towards ambulatory minimally invasive procedures in favor of inpatient operations, thus making it financially beneficial both for surgeons and health systems to adopt more minimally invasive techniques. Moreover, all training courses in the USA at medical schools include requirements concerning the adoption of minimally invasive surgical skills.

Medtronic launched the Hugo robotic-assisted surgery system in additional U.S. markets throughout 2024 and 2025, establishing a competitive alternative to Intuitive Surgical's da Vinci platform in the rapidly expanding robotic-assisted soft-tissue surgery segment.

Minimally Invasive Surgery Market Segment Analysis

-

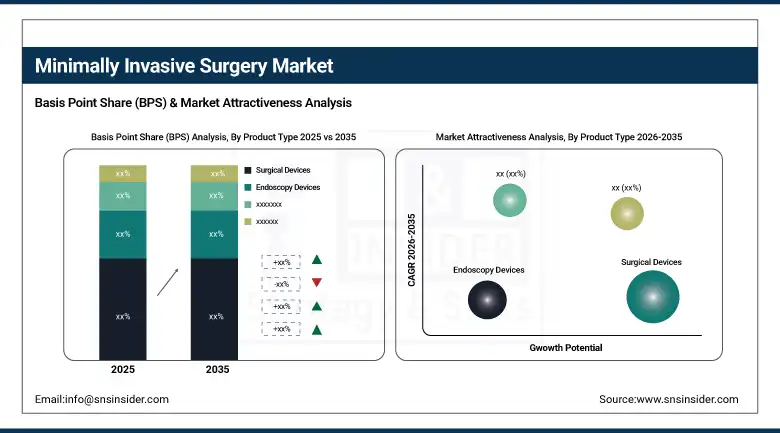

By Product Type, the surgical devices segment dominated the minimally invasive surgery market with 45.32% share in 2025, while the robotic surgical systems segment is the fastest growing product type during 2026 to 2035.

-

By Procedure Type, the laparoscopic surgery segment dominated the minimally invasive surgery market with 38.47% share in 2025, while the robotic-assisted surgery segment is the fastest growing procedure type during 2026 to 2035.

-

By Application, the general surgery segment dominated the minimally invasive surgery market with 34.28% share in 2025, while the urological surgery segment is the fastest growing application during 2026 to 2035.

-

By End User, the hospitals segment dominated the minimally invasive surgery market with 54.31% share in 2025, while ambulatory surgical centers are the fastest growing end user during 2026 to 2035.

By Product Type, surgical devices dominate, robotic surgical systems grow fastest

The segment for surgical devices was the most dominant one, holding a share of 45.32% of market revenues in 2025. Surgical devices include high-volume devices that each minimally invasive surgery needs, such as laparoscopic graspers, laparoscopic scissors, clip appliers, trocars, insufflation devices, and many other specialty instruments designed for specific anatomical areas. It is due to the disposable feature of these products, as the revenue from their usage is recurring and is not associated with the need for buying new capital devices.

The most rapidly growing segment was the robotic surgery system segment. These devices have become popular due to their proven clinical superiority in procedures like prostatectomy, hysterectomy, colorectal resection, and thoracic surgery, which convinced many healthcare facilities about the business sense of investing in such devices.

By Procedure Type, laparoscopic surgery dominates, robotic-assisted surgery grows fastest

The market revenue for laparoscopic surgery was 38.47% in 2025, marking the matured and global dominant minimally invasive surgery system that has an established technique for cholecystectomy, appendectomy, bowel resections, hernia repairs, and various other gynecological and urological surgeries around the world.

Robotic assisted surgery marked the highest growing segment as robotic surgeries increase due to an increasing number of surgeons trained in robotic techniques. Such surgeons are willing to use robotic surgery as it offers a clear advantage over laparoscopic surgery when it comes to intricate anatomy because of its ability to visualize the area in three dimensions and offer instrument tremor reduction.

By End User, hospitals dominate, ambulatory surgical centers grow fastest

Hospitals generated 54.31% of market revenue in 2025. They remain the primary deployment environment for the most complex and capital-intensive minimally invasive surgical equipment including robotic platforms, advanced imaging systems, and hybrid operating theatre infrastructure whose installation and operational requirements demand the clinical support services and critical care backup that only hospital settings can reliably provide.

Ambulatory surgical centers are growing fastest as payer reimbursement policy continues shifting procedure coverage toward outpatient settings and as the clinical safety data for outpatient minimally invasive procedures matures to the point where lower-acuity patients can be reliably managed without overnight hospital observation. The economic advantages of ambulatory surgery, which reduces facility cost per procedure by 40 to 60% compared to inpatient hospital alternatives, create powerful financial incentives for health systems to develop or partner with ambulatory surgical center infrastructure.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.47% |

|

Europe |

Germany |

28.73% |

|

Asia Pacific |

China |

36.84% |

|

Middle East & Africa |

Saudi Arabia |

24.73% |

|

Latin America |

Brazil |

43.82% |

North America Minimally Invasive Surgery Market Insights

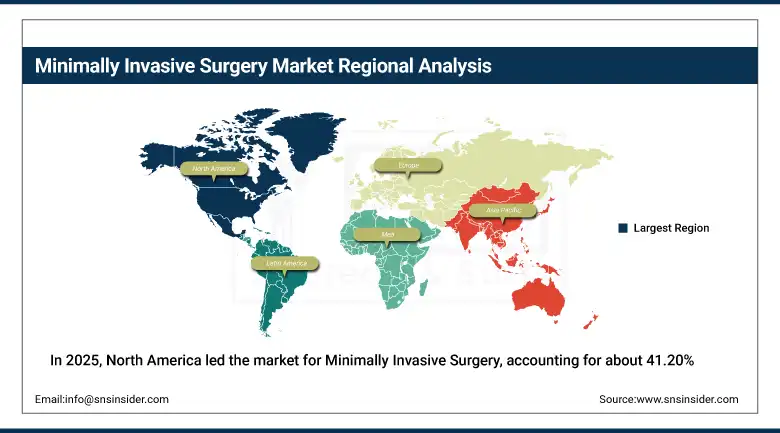

In 2025, North America led the market for Minimally Invasive Surgery, accounting for about 41.20% of total global revenues. The United States accounts for about 83.47% of regional revenues owing to its dominance in robotic surgery, having the most extensive network of robotic surgery units in the world, as well as having the largest ambulatory care centers worldwide coupled with the ability to incentivize minimally invasive procedures using higher payments to healthcare practitioners. Canada accounted for about 16.53% of regional revenues as a result of government investments into surgical robots and laparoscopy through their public healthcare system due to the need to cut down on recovery periods.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Minimally Invasive Surgery Market Insights

Europe held approximately 26.84% of global Minimally Invasive Surgery revenues in 2025. Germany, France, the United Kingdom, Italy, and the Netherlands are the leading national markets, each operating well-developed specialist surgical centers with active robotic surgery programmes and high laparoscopic procedure penetration across standard surgical indications. European health technology assessment bodies including NICE in the United Kingdom and the IQWiG in Germany have progressively issued favourable guidance on robotic-assisted surgery for specific indications, creating reimbursement certainty that accelerates institutional procurement decisions. The EU Medical Devices Regulation's updated certification requirements for surgical systems are shaping product approval timelines across the European market and influencing the competitive positioning of both established and emerging surgical robotics platforms.

Asia Pacific Minimally Invasive Surgery Market Insights

The Asia-Pacific region is expected to grow the fastest in terms of market share for Minimally Invasive Surgery and is estimated to have a CAGR of around 11.24% until 2035 because of increasing surgical procedures in China, India, Japan, South Korea, Australia, and countries in Southeast Asia owing to an increasing burden of chronic diseases, specialist surgeons, and investment in healthcare infrastructure leading to growing demand for minimally invasive surgeries. The majority of revenue from this market in Asia-Pacific can be attributed to China as it is witnessing growth in hospitals, investment in surgical technologies under the Healthy China 2030 program, and growing domestic manufacturers of robotic systems such as MicroPort, Tinavi, and Rokae. India is expected to grow the fastest within this region due to growth in private hospitals and development of medical tourism.

MEA & Latin America Minimally Invasive Surgery Market Insights

Middle East and Latin America are commercially significant and growing minimally invasive surgery market where government healthcare modernization investments, growing private hospital sector development, and rising chronic disease surgical burden are creating expanding institutional demand for advanced surgical technology. Saudi Arabia leads MEA revenues at approximately 24.73% of the regional total through its Vision 2030 healthcare transformation programme whose hospital construction pipeline and clinical quality improvement targets are driving procurement of robotic surgery systems and advanced laparoscopic equipment at major public and private medical centers. Brazil leads Latin American revenues at approximately 43.82% of the regional total through its large private healthcare sector, a well-trained surgical specialist workforce in major urban centers, and growing public health system investment in laparoscopic and endoscopic surgical capacity.

Market Dynamics

Growth Drivers: Rising chronic disease surgical burden, ageing demographics, and accelerating robotic surgery technology adoption are creating compounding structural demand growth across global minimally invasive surgery markets.

Drivers behind market growth in minimally invasive surgeries include demographics, clinical advancements, and technological progress, each one contributing to an increase in both the number of patients who need surgery as well as the techniques associated with minimally invasive procedures. With global cancer cases expected to reach 35 million annually by the year 2050, the demand for minimally invasive oncological surgery increases in parallel with a trend towards laparoscopic and robotic resection techniques as equally effective options.

Restraints: High capital acquisition costs for robotic surgical systems and the steep learning curve for advanced minimally invasive technique adoption constrain deployment velocity in resource-limited and emerging market hospital settings.

The capital expense of purchasing a complete set of robotically assisted surgical systems lies between USD 1.5 million and USD 3 million for the system itself, with a yearly contract for servicing costs being between USD 100,000 and USD 200,000. The financial constraints mentioned above prevent the implementation of robotic systems in hospitals capable of covering the economic expenses of such a purchase, which results in small-scale hospitals in both developed and developing countries being unable to enter the most dynamic segment of the market for MIS systems. The acquisition of skills by surgeons in laparoscopic and robotic surgery demands a specific learning curve that consists of several dozen and even several hundred operations under supervision until the skill level required is reached.

Opportunities: AI-assisted surgical guidance, single-use flexible robotic systems, and procedure migration to ambulatory settings represent transformative commercial frontiers for the minimally invasive surgery market through 2035.

AI integration into minimally invasive surgery workflows is the most significant near-term innovation opportunity. Surgical AI applications including intraoperative anatomical identification, bleeding risk prediction, and autonomous camera navigation are advancing through regulatory clearance pathways toward clinical deployment. Johnson and Johnson MedTech, Medtronic, and Intuitive Surgical each have active AI surgical assistance programmes whose commercial launches will expand per-procedure revenue and create differentiated positioning against non-AI-enabled systems.

Recent Developments:

-

2025: Intuitive Surgical reported cumulative global robotic-assisted procedures exceeding 14 million on its da Vinci platform, reflecting the accelerating adoption of robotic surgery across new geographies and surgical specialties as the company's Ion bronchoscopy platform and next-generation da Vinci 5 system expand its clinical addressable market.

-

2025: Medtronic expanded commercial availability of its Hugo robotic-assisted surgery system across additional markets in Europe and Asia Pacific, pursuing competitive market share against Intuitive Surgical's established position with a modular, multi-specialty system design that supports flexible deployment across diverse institutional and procedural requirements.

-

2024: Johnson and Johnson MedTech received FDA clearance for its Ottava robotic surgical system for soft-tissue surgical applications, entering the competitive surgical robotics market with a differentiated architecture that integrates robotic arm positioning within a single-arm design concept targeting operational simplicity and reduced operating room footprint relative to multi-arm robotic platforms.

Minimally Invasive Surgery Market Key Players are:

-

Intuitive Surgical Inc.

-

Medtronic PLC

-

Johnson & Johnson MedTech

-

Stryker Corporation

-

Boston Scientific Corporation

-

Abbott Laboratories

-

Becton Dickinson and Company

-

Olympus Corporation

-

Karl Storz GmbH & Co. KG

-

Richard Wolf GmbH

-

Smith+Nephew PLC

-

ConMed Corporation

-

Arthrex Inc.

-

Ethicon Inc. (J&J)

-

Applied Medical Resources Corporation

-

Teleflex Incorporated

-

Microbot Medical Inc.

-

MicroPort Scientific Corporation

-

Tinavi Medical Technologies Co. Ltd.

-

Asensus Surgical Inc.

Minimally Invasive Surgery Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 58.42 Billion |

| Market Size by 2035 | USD 129.20 Billion |

| CAGR | CAGR of 8.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Surgical Devices, Endoscopy Devices, Electrosurgical Devices, Imaging & Visualization Systems, Robotic Surgical Systems, Others) • By Procedure Type (Laparoscopic Surgery, Robotic-Assisted Surgery, Endoscopic Surgery, Others) • By Application (General Surgery, Cardiovascular Surgery, Orthopedic Surgery, Gynecological Surgery, Urological Surgery, Neurological Surgery, Others) • By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intuitive Surgical Inc., Medtronic PLC, Johnson & Johnson MedTech, Stryker Corporation, Boston Scientific Corporation, Abbott Laboratories, Becton Dickinson and Company, Olympus Corporation, Karl Storz GmbH & Co. KG, Richard Wolf GmbH, Smith+Nephew PLC, ConMed Corporation, Arthrex Inc., Ethicon Inc. (J&J), Applied Medical Resources Corporation, Teleflex Incorporated, Microbot Medical Inc., MicroPort Scientific Corporation, Tinavi Medical Technologies Co. Ltd., Asensus Surgical Inc. |

Frequently Asked Questions

North America dominated the Minimally Invasive Surgery Market in 2025, holding approximately 41.20% of global revenues, with the United States accounting for approximately 83.47% of North American revenues.

The surgical devices segment dominated the Minimally Invasive Surgery Market with 45.32% share in 2025.

The primary growth factors are rising global surgical procedure volumes driven by ageing demographics and chronic disease prevalence, accelerating robotic-assisted surgery adoption supported by clinical evidence and expanding training infrastructure, payer reimbursement frameworks favoring cost-efficient minimally invasive approaches, and technology innovation in AI surgical guidance and advanced imaging that is progressively extending minimally invasive technique to more complex anatomical and procedural applications.

The Minimally Invasive Surgery Market was valued at USD 58.42 Billion in 2025.

The Minimally Invasive Surgery Market is expected to grow at a CAGR of 8.27% from 2026 to 2035.

Get in Touch