Vision Processing Unit Market Report Scope & Overview:

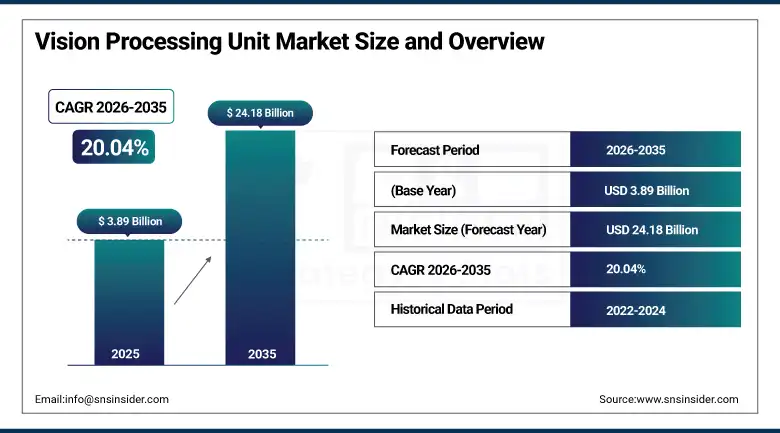

The Vision Processing Unit Market was valued at USD 3.89 Billion in 2025 and is expected to reach USD 24.18 Billion by 2035, growing at a CAGR of 20.04% from 2026–2035.

The global market for vision processing units (VPUs) is growing very fast because of the rise in AI-powered tasks that involve high-speed processing of images, which require minimal amounts of energy usage. The VPUs refer to semiconductor chips tailored explicitly for top performance during deep learning object detection, facial recognition, and quick processing of information that cannot be done effectively by general-purpose processors. The development of VPUs is fueled by advances in deep learning algorithms, edge computing technology, and hardware design in combination with the availability of comprehensive developer tools.

In March 2025, Qualcomm Technologies announced the acquisition of Edge Impulse to enhance its AI and IoT capabilities, aiming to accelerate edge device innovation and real-time visual data processing solutions. The acquisition reflected Qualcomm’s strategy of strengthening its embedded machine learning development platform to support faster, more efficient deployment of vision processing capability across smartphones, industrial sensors, and consumer IoT devices requiring on-device AI inference without cloud dependency.

Market Size and Forecast

-

Market Size in 2026E: USD 4.67 Billion

-

Market Size by 2035: USD 24.18 Billion

-

CAGR: 20.04% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Vision Processing Unit Market - Request Free Sample Report

Vision Processing Unit Market Trends

-

AI and machine learning integration in smartphones, cameras, and drones is driving high-performance, low-power VPU adoption.

-

Growing AR/VR adoption in gaming, healthcare, and industrial training applications is accelerating demand for real-time motion tracking VPUs.

-

ADAS advancement in vehicles is increasing VPU deployment for instant image processing and navigation precision.

-

5G network rollout is enabling faster data transfer for VPU-powered real-time image processing applications at the edge.

-

Intelligent surveillance and smart home device proliferation is creating new VPU demand for efficient visual data processing.

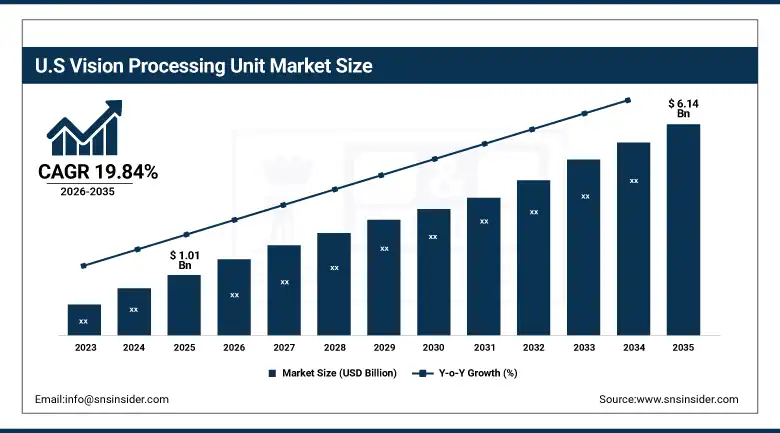

The U.S. Vision Processing Unit Market Outlook

The U.S. Vision Processing Unit Market was valued at approximately USD 1.01 Billion in 2025 and is expected to reach approximately USD 6.14 Billion by 2035, growing at a CAGR of approximately 19.84%.

The US has emerged as the dominant force in the North American region with respect to VPU revenue due to the presence of top-level chip makers such as Intel, Qualcomm, and Ambarella in the country, which make use of advanced architectures of VPU to enable smartphones, surveillance cameras, and AR/VR devices. The increasing demand for AI-driven applications and enhanced capabilities of computer vision technology is spurring the growth in domestic demand for VPU.

Intel’s Movidius Myriad X VPU architecture has become a standard component in smart cameras and drones, enabling affordable, power-efficient visual processing for commercial and consumer applications. Meanwhile, Tesla and General Motors continue deploying cutting-edge vision processing technology in their autonomous vehicle platforms, with North American ADAS adoption driving sustained VPU procurement growth as automakers race to deliver advanced driver assistance capability across their expanding vehicle lineups.

Vision Processing Unit Market Segment Analysis

-

By Fabrication Process, the >16–28 nm segment dominated the vision processing unit market with approximately 58.1% share in 2025, while the ≤16 nm segment is the fastest growing driven by demand for compute-heavy AR/VR and AI applications.

-

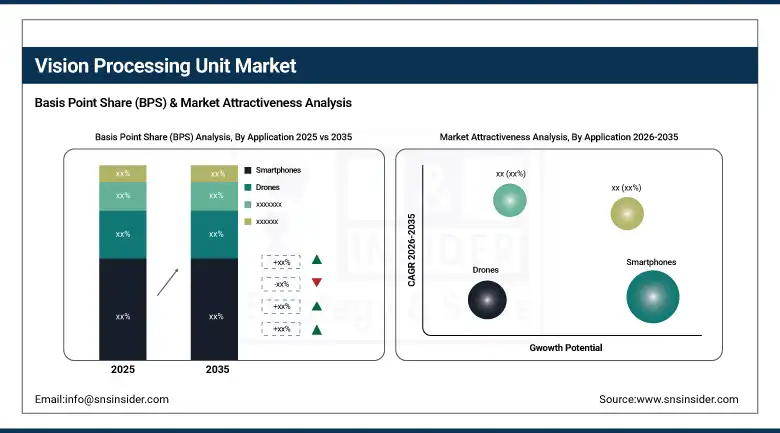

By Application, the smartphones segment dominated the vision processing unit market with approximately 39.3% share in 2025, while the AR/VR segment is the fastest growing driven by immersive gaming, healthcare, and training applications.

-

By Vertical, the consumer electronics segment dominated the vision processing unit market with approximately 28.5% share in 2025, while the security & surveillance segment is the fastest growing driven by real-time video analytics demand.

By Fabrication Process, 16–28 nm dominates, ≤16 nm grows fastest

Technology with >16–28 nm node had a leading position in the vision processing unit market with around 58.1% of shares in 2025. The commercial success of the node is based on the performance, power efficiency, and cost-efficiency delivered by this node, which makes the nodes widely used in smartphone, camera, and automotive-based VPU products. The node can process data with minimum energy loss and heat generation, which is important for a lot of mobile or embedded devices with limited battery capacity and thermal budget, as opposed to the premium leading-edge process nodes. The accumulated production capabilities of this node and their optimized yields ensure the ongoing popularity of the node range in the mainstream application of VPU products.

Node technology ≤16 nm would be growing with the fastest CAGR during the forecast period due to increased demands for premium VPUs with applications such as AR/VR, AI devices, and self-driving vehicles. This range of nodes provides enhanced power and area efficiency compared to other nodes in order to satisfy the needs of modern applications with increasing computational density. It is expected that these changes would transform some industries using VPU products due to increasing demands on VPU performance.

By Application, smartphones dominate, AR/VR grows fastest

Smartphones accounted for nearly 39.3% of the total vision processing unit market share in 2025. This dominance is attributable to the latest smartphones incorporating powerful camera modules, intelligent AI-powered features, and enhanced image processing capabilities that have become standard consumer expectations across both flagship and mid-range device tiers. VPUs are essential for augmented reality applications, battery optimization in camera systems, and facial recognition functionality that collectively define modern smartphone camera performance differentiation. Huawei’s flagship smartphone VPU integration for AI-based photography and Samsung’s equivalent camera processing investment demonstrate how leading device manufacturers compete on visual processing capability as a primary differentiating feature across their premium product portfolios.

The AR/VR market is expected to record a strong CAGR from 2026 to 2035 on account of the growing preference for AR/VR technology across gaming, healthcare, and training sectors. Motion tracking, object detection, and enhanced visual processing capability are enabling VPUs to boost the penetration of AR/VR headsets in various industries, which is otherwise difficult to achieve using traditional computing devices. Considering the future demand for visual processing units in the growing AR/VR market, there are substantial opportunities for VPU developers in the coming years.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

Israel |

22.8% |

|

Latin America |

Brazil |

43.8% |

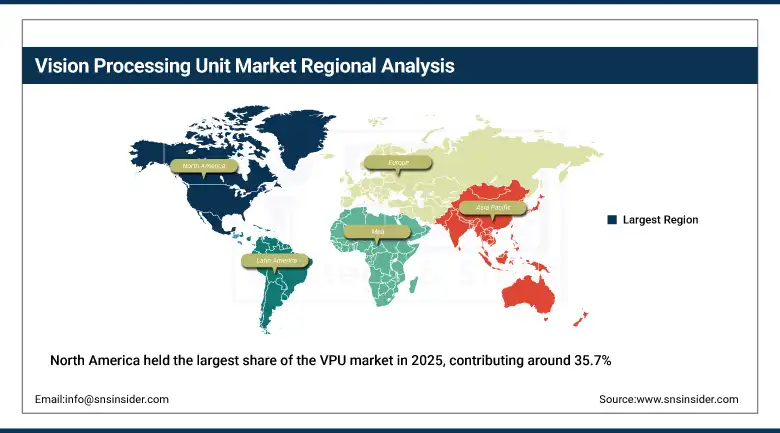

North America Vision Processing Unit Market Insights

North America held the largest share of the VPU market in 2025, contributing around 35.7% to the total market share. Factors bolstering this dominance include the vast presence of top-notch technology companies, high research and development expenditure, and rapid acceptance of advanced technologies. The United States hosts major entities including Intel, Qualcomm, and Ambarella that develop VPUs and integrate these chips into smartphone systems, facial recognition security systems, and AR/VR platforms.

The United States accounts for approximately 82.5% of North American revenues, with Intel’s Movidius VPUs commonly found in smart cameras and drones. The growing adoption of ADAS systems in the automotive field continues increasing VPU demand, with Tesla and General Motors deploying cutting-edge vision processing technology in their autonomous vehicle platforms across the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Vision Processing Unit Market Insights

Europe is a technically sophisticated VPU market where automotive ADAS adoption, industrial automation, and growing surveillance infrastructure investment collectively sustain consistent demand. Germany accounts for approximately 24.6% of European revenues through its world-leading automotive sector’s ADAS chip procurement and advanced industrial robotics vision system investment.

The United Kingdom’s growing security technology sector, France’s automotive and aerospace vision system adoption, and the Netherlands’ semiconductor design ecosystem collectively sustain European VPU market development. European automotive safety regulation requiring advanced driver assistance capability across new vehicle models creates structured institutional VPU procurement.

Asia Pacific Vision Processing Unit Market Insights

Asia Pacific is projected to register the fastest CAGR from 2026 to 2035, driven by increasing demand for consumer electronics, investments in smart city construction, and growth in automotive production. China, Japan, and South Korea lead the way globally with their technology investment, with Huawei including VPUs in its flagship smartphone cameras to boost AI-based photography.

China accounts for approximately 48.6% of Asia Pacific revenues, with Hikvision’s VPU-based smart camera deployment strengthening the country’s surveillance market. Samsung’s equivalent camera processing investment in South Korea and Japan’s advanced robotics and automotive vision system adoption further sustain the region’s rapid technology adoption and high-growth trajectory.

MEA & Latin America Vision Processing Unit Market Insights

Israel leads MEA revenues through its world-class semiconductor design and computer vision technology sector, with leading defence electronics and autonomous vehicle technology companies driving sustained VPU procurement. The UAE’s growing smart city and surveillance infrastructure investment contributes additional regional demand.

Brazil leads Latin American revenues through its growing automotive manufacturing sector’s ADAS adoption and expanding consumer electronics market. Mexico’s automotive manufacturing sector serving the North American market and Argentina’s growing technology sector create additional regional VPU procurement growth.

Market Dynamics

Growth Drivers: Accelerating AI integration in consumer devices and rising ADAS adoption creating sustained VPU procurement growth

The increased use of Artificial Intelligence and Machine Learning in devices like mobile phones, camera, and drones has facilitated considerable profits from VPU usage. VPU devices are developed to give maximum output while using low power because today's electronic devices require such type of image processors due to their limited battery capacity. Another reason behind the high demand for VPU in the market is the fast growth of Augmented Reality and Virtual Reality in gaming, healthcare, and industries where dedicated processing capabilities are needed for these technologies.

Another important aspect behind the increased adoption of VPU is the increased demand for advanced driver assistance systems in cars for better security. Automakers prefer to integrate VPUs to perform tasks related to image processing and object recognition in ADAS, making it easy for them to identify objects within seconds. With every new automobile release, the demand for VPUs increases, leading to the growth of the VPU market owing to the increased production of vehicles worldwide.

Restraints: VPU integration complexity hindering innovation cycles and slowing market penetration in advanced applications

High complexity in integrating VPUs across various devices is a key restraining factor. While momentum is slowly building toward better VPU design, developing VPUs that can effectively implement diverse hardware architectures requires significant technical expertise, causing innovation to proceed gradually. Existing software frameworks can present integration challenges for developers, particularly in applications reliant on fast image recognition and surrounding data processing. Such complexity often results in lengthy development cycles that postpone product launches and slow market penetration across the most demanding application categories.

Power efficiency challenges in high-performance associative memory create ongoing design constraints, as VPUs must continue processing data while generating minimal heat, a particularly important feature for power-dependent devices like smartphones, drones, and AR/VR systems. Security concerns related to VPU-driven devices are becoming increasingly pressing, as these processors handle large volumes of visual data that become attractive targets for data breaches and hacking efforts requiring robust encryption and secure processing environment investment.

Opportunities: Intelligent surveillance expansion and 5G integration creating new VPU deployment frontiers across smart devices

New opportunities in the VPU market are associated with the growing need for intelligent surveillance, smart home gadgets, and robotics. The rise of devices requiring efficient visual data processing opens significant opportunities for VPU manufacturers, as smart cities, connected security systems, and autonomous robotics platforms increasingly specify dedicated visual processing capability. Industry-wide transformation toward automation and intelligence is creating a substantial addressable market for VPUs whose commercial scale extends well beyond traditional consumer electronics applications.

5G technology integration will further extend data transfer speeds, enabling more VPU-powered image processing applications to operate efficiently in real time. This connectivity advancement is expected to accelerate deployment of VPU-powered applications across industrial IoT, autonomous robotics, and next-generation security systems whose real-time processing requirements depend on both on-device VPU capability and high-bandwidth network infrastructure working in combination to deliver acceptable application performance.

Recent Developments:

-

2025: Qualcomm Technologies announced the acquisition of Edge Impulse to enhance its AI and IoT capabilities, aiming to accelerate edge device innovation and real-time data processing solutions across its Snapdragon VPU product portfolio.

-

2024: Ambarella Inc. expanded its CV-series vision processing chip portfolio with enhanced AI inference capability for automotive ADAS and security camera applications, targeting growing demand for on-device computer vision processing without cloud dependency.

-

2023: Intel Corporation enhanced its Movidius Myriad X VPU architecture with improved deep learning inference performance, strengthening its position in smart camera and drone visual processing applications across commercial and consumer markets.

Vision Processing Unit Market Key Players are:

-

Intel Corporation

-

Qualcomm Technologies Inc.

-

NXP Semiconductors N.V.

-

Synopsys Inc.

-

MediaTek Inc.

-

Ambarella Inc.

-

Ceva Inc.

-

Cadence Design Systems Inc.

-

Himax Technologies Inc.

-

Rockchip Electronics Co. Ltd.

-

Samsung Electronics Co. Ltd.

-

Texas Instruments Inc.

-

Google LLC

-

Lattice Semiconductor Corporation

-

Mythic Inc.

-

Renesas Electronics Corporation

-

STMicroelectronics N.V.

-

onsemi (ON Semiconductor Corporation)

-

Xilinx Inc. (AMD)

-

Hailo Technologies Ltd

Vision Processing Unit Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.89 Billion |

| Market Size by 2035 | USD 24.18 Billion |

| CAGR | CAGR of 20.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Fabrication Process (≤16 nm, >16–28 nm) • By Application (Smartphones, Drones, Cameras, AR/VR, ADAS, Others) • By Vertical (Consumer Electronics, Security & Surveillance, Automotive, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel Corporation, Qualcomm Technologies Inc., NXP Semiconductors N.V., Synopsys Inc., MediaTek Inc., Ambarella Inc., Ceva Inc., Cadence Design Systems Inc., Himax Technologies Inc., Rockchip Electronics Co. Ltd., Samsung Electronics Co. Ltd., Texas Instruments Inc., Google LLC, Lattice Semiconductor Corporation, Mythic Inc., Renesas Electronics Corporation, STMicroelectronics N.V., onsemi (ON Semiconductor Corporation), Xilinx Inc. (AMD), and Hailo Technologies Ltd. |

Frequently Asked Questions

The Vision Processing Unit Market is expected to grow at a CAGR of 20.04% from 2026 to 2035.

The Vision Processing Unit Market was valued at USD 3.89 Billion in 2025.

Rising AI and machine learning integration in smartphones, cameras, and drones, growing AR/VR adoption, and increasing ADAS deployment in vehicles are the primary growth factors.

The >16–28 nm segment dominated the Vision Processing Unit Market with approximately 58.1% share in 2025.

North America dominated the Vision Processing Unit Market with approximately 35.7% revenue share in 2025.

Get in Touch