Wood Preservatives Market Report Scope & Overview:

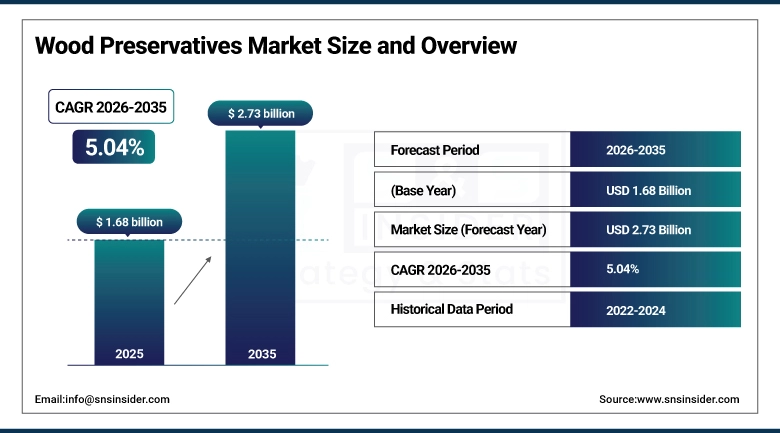

The Wood Preservatives Market size was valued at USD 1.68 Billion in 2025 and is projected to reach USD 2.73 Billion by 2035, growing at a CAGR of 5.04% during 2026-2035.

The market for Wood Preservatives is expanding with the surge in construction activities, increased need for durable and long-lasting wood products, stringent regulations supporting the use of wood preservatives, increased applications in residential decking, and growing recognition of the importance of preserving wood from fungi, termites, and environmental degradation.

Wood Preservatives Market Size and Forecast:

-

Market Size in 2025: USD 1.68 Billion

-

Market Size by 2035: USD 2.73 Billion

-

CAGR of 5.04% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Wood Preservatives Market - Request Free Sample Report

Key Wood Preservatives Market Trends

-

Shift toward eco-friendly and low-toxicity water-based preservatives due to stringent environmental regulations

-

Rising demand from residential construction, especially decking, fencing, and outdoor structures

-

Increasing use of pressure-treated wood for enhanced durability and longer service life

-

Growth in infrastructure and utility applications such as poles, railway sleepers, and marine wood

-

Innovation in bio-based and advanced preservative formulations for sustainable wood protection

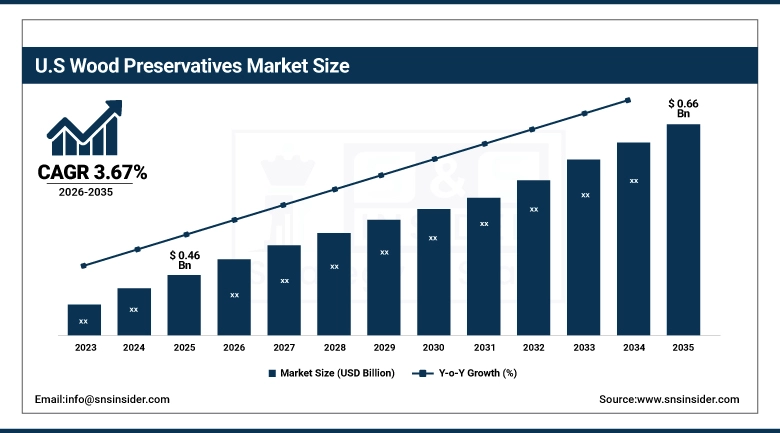

The U.S. Wood Preservatives Market size was valued at USD 0.46 Billion in 2025 and is projected to reach USD 0.66 Billion by 2035, growing at a CAGR of 3.67% during 2026-2035. The U.S. holds a 78.64% share within North America. The American market runs on pressure-treated pine. Southern Yellow Pine, the species that takes copper-based preservative treatment better than virtually any other commercially available timber, dominates U.S. residential construction applications from Florida fence posts to Maine dock pilings.

Wood Preservatives Market Growth Drivers:

-

Expanding Construction, Rising Demand for Durable Wood, and Eco-Friendly Innovations Driving Market Growth

The Wood Preservatives Market is driven by the increase in the global construction industry and infrastructure development activities. The increase in the demand for durable and weather-resistant wood products and the increase in residential renovation activities are the key drivers of the Wood Preservatives Market. Stringent government regulations regarding the use of treated wood products and the increase in the lifespan of the products are also boosting the Wood Preservatives Market. The increase in the use of utility poles, marine structures, and railway sleepers, along with the use of eco-friendly preservative technologies, is boosting the Wood Preservatives Market.

Wood Preservatives Market Restraints:

-

Stringent Regulations, Raw Material Volatility, and Shift Toward Alternatives Limiting Market Expansion

The Wood Preservatives Market is affected by restrains in the form of tough regulations regarding the use of hazardous chemicals, thereby adding costs for manufacturers. Fluctuating costs of raw materials can affect the production of wood preservatives. Also, the use of substitute materials like plastics and composites, as well as the disposal of treated wood, could act as restrains for the Wood Preservatives Market.

Wood Preservatives Market Opportunities:

-

Sustainable Solutions, Emerging Market Growth, and Advanced Technologies Creating New Revenue Opportunities

The Wood Preservatives market is an opportunity with the growing demand for eco-friendly or ‘bio-based’ wood preservatives. The market is growing in emerging countries with high infrastructure development rates and housing expansion. The market is growing with the increasing use of wood in outdoor applications, technological advancements in high-performance wood preservatives, and the expanding utility sector and marine industry.

Wood Preservatives Market Segment Analysis

-

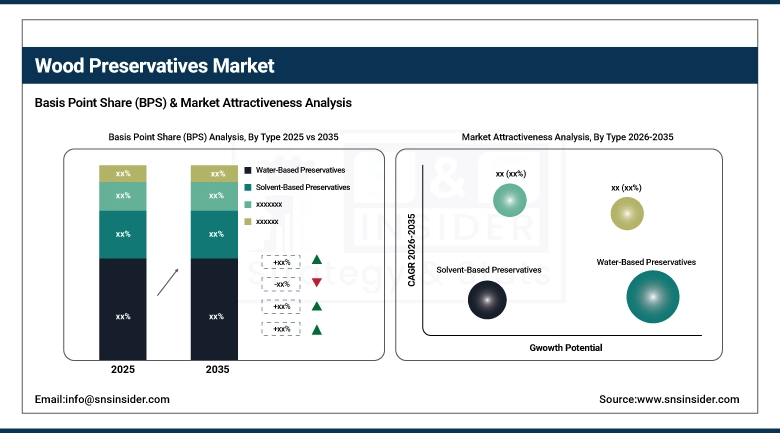

By Type, Water-Based Preservatives dominated with 70.87% in 2025, and Water-Based Preservatives are also expected to grow at the fastest CAGR of 5.89% from 2026 to 2035.

-

By Application, Residential (Decking, Fencing, Furniture) dominated with 39.68% in 2025, and Residential is expected to grow at the fastest CAGR of 5.51% from 2026 to 2035.

-

By End-Use Industry, Construction & Infrastructure dominated with 44.63% in 2025, and Construction & Infrastructure is expected to grow at the fastest CAGR of 5.56% from 2026 to 2035.

-

By Treatment Method / Technology, Pressure Treatment dominated with 54.82% in 2025, and Vacuum-Pressure Processes are expected to grow at the fastest CAGR of 5.28% from 2026 to 2035.

By Type, Water-Based Preservatives Lead and Maintain Fastest Growth in Wood Preservatives Market While Solvent and Oil-Based Formulations Gradually Decline in Share Through 2035

Water-based preservatives hold the highest share in the market because of their least toxic properties, eco-friendliness, and high degree of acceptability in both residential and industrial applications. They are easy to apply and have shown significant effectiveness against decay and insects. Regulatory pressures against the use of hazardous chemicals have boosted the demand for water-based preservatives, and continuous developments in eco-friendly products have made this segment the most attractive and growing segment in the market.

By Application, Residential Leads While Industrial Applications Hold Significant Share in Wood Preservatives Market Across Utility Poles Railway Sleepers and Marine Uses

Residential segment holds the majority of the market share, driven by rising demand for decking, fencing, and outdoor furniture in residential projects and renovation activities. Growing demand for visually appealing and long-lasting wooden structures is positively influencing the market. Growing urban residential spaces and outdoor living trends are fuelling demand for treated wood, while maintenance requirements for existing wooden structures are ensuring steady demand for preservatives in the residential segment worldwide.

By End-Use Industry, Construction and Infrastructure Leads and Grows Fastest While Furniture and Marine Sectors Hold Steady in Wood Preservatives Market

Construction and infrastructure represent the largest end-use segment due to extensive use of treated wood in structural and outdoor applications. Growing investments in infrastructure projects and urban development are driving demand for durable wood materials. Treated wood is widely used for its resistance to moisture, pests, and environmental damage, making it essential for long-lasting construction, especially in bridges, poles, and public infrastructure projects.

By Treatment Method, Pressure Treatment Dominates Wood Preservatives Market While Vacuum-Pressure Processes Set for Fastest Growth 2026 to 2035

Pressure treatment is the most widely adopted technology, offering deep penetration of preservatives and long-term protection against environmental and biological damage. It is extensively used in industrial and large-scale applications where durability is critical. Increasing demand for high-performance wood protection solutions is supporting its dominance, while advancements in treatment technologies are enhancing efficiency, ensuring consistent quality, and expanding its adoption across various end-use sectors.

Wood Preservatives Market Regional Analysis

North America Wood Preservatives Market Insights

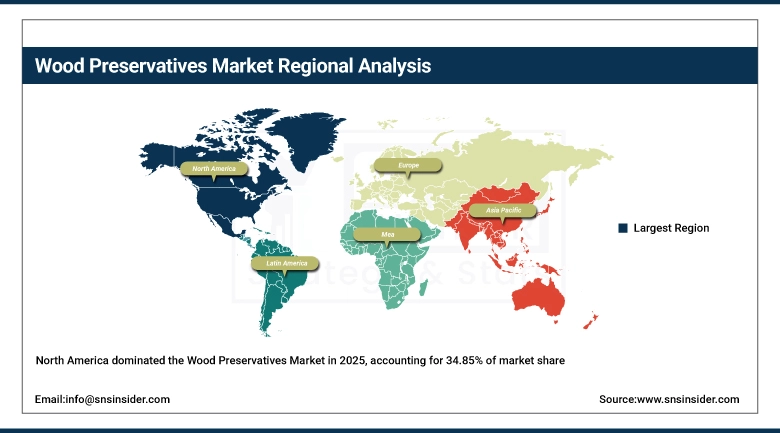

North America held a 34.85% share of the global Wood Preservatives Market in 2025 at USD 0.58 Billion, growing at a CAGR of 3.90% through 2035. The region's market is mature rather than fast-growing, which doesn't mean it's unimportant it means the volume base is large, the competitive structure is entrenched, and growth comes from renovation cycles and modest construction starts rather than greenfield demand expansion. The U.S. Treated Wood Council's product certifications effectively govern what treatments can be sold at mass retail, creating a standards-based market where non-certified formulations can't access the biggest volume channel.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Wood Preservatives Market Insights

The United States dominated North America's wood preservatives market in 2025. Lonza's Arch Wood Protection unit, Koppers Performance Chemicals, and Viance collectively control the majority of U.S. treatment chemical supply, and their relationships with regional pressure treatment operators and major retail lumber programs define the commercial structure of the market. The AWPA (American Wood Protection Association) standards system, updated regularly to reflect new active substances and performance data, functions as the market's de facto regulatory framework and tends to be more adaptive to new formulations than EPA registration timelines alone would suggest.

Europe Wood Preservatives Market Insights

Europe held 27.42% of the global market at USD 0.46 Billion in 2025, CAGR 4.35% through 2035. The EU Biocidal Products Regulation has been the defining force on European wood preservatives chemistry for the past decade. It's comprehensive, science-based, and slow which means producers need 5-10 year planning horizons for active substance registrations that other jurisdictions handle in 2-3 years. Germany leads European consumption volume, fed by the country's active residential renovation market, substantial Bundesbahn railway tie replacement programs, and a furniture manufacturing sector that remains the largest in Europe. The Nordic countries show the highest per-capita consumption of wood preservatives globally because their building traditions rely heavily on timber construction and their climate (wet, freeze-thaw cycling, long winters) demands high treatment standards to achieve acceptable service life from structural and cladding timber.

Germany Wood Preservatives Market Insights

Germany was the market leader in the European Wood Preservatives Market in 2025. This was due to the country’s robust construction industry, developed wood processing sector, and high demand for eco-friendly building products. In addition, environmental regulations and the use of treated woods in construction and domestic properties contributed to this.

Asia Pacific Wood Preservatives Market Insights

Asia Pacific is the fastest-growing region at 7.66% CAGR through 2035, valued at USD 0.36 Billion in 2025 a base that understates the opportunity because much of the region's timber consumption is currently untreated or treated with informal methods. India's railway modernization program, which Vande Bharat Express expansion and the dedicated freight corridor projects sit within, keeps industrial preservative demand elevated in a country where track-side timber use remains substantial. Indonesia's tropical hardwood sector, while facing sustainability pressure, still generates preservative treatment demand for export furniture and domestic construction timber. China's regulatory environment for wood preservatives has been tightening since 2020 toward the EU BPR model, which is simultaneously restricting legacy formulations and creating commercial opportunity for producers who've already invested in compliant water-based chemistry.

China Wood Preservatives Market Insights

China was the market leader in the Asia Pacific Wood Preservatives Market in 2025, owing to factors such as rapid urbanization and the growth in infrastructure and building projects. The expansion in manufacturing capabilities also helped China to maintain its position in the Asia Pacific Wood Preservatives Market.

Latin America (LATAM) and Middle East & Africa (MEA) Wood Preservatives Market Insights

Latin America held 8.94% of the global market at USD 0.15 Billion in 2025, growing at a modest 3.90% CAGR through 2035. Brazil anchors regional demand: the country's Cerrado and Amazon fringe agricultural frontier generates enormous fence post and agricultural structure demand, Eucalyptus plantation forestry produces the primary raw material for treated posts, and urban construction in São Paulo and Rio requires treated timber in coastal and tropical humidity conditions that rapidly degrade untreated wood. Chile's sawmill sector and Colombia's growing construction market add secondary demand. The Middle East & Africa held 7.03% at USD 0.12 Billion, CAGR 5.11%, where demand concentrates in two very different contexts. Gulf state construction, which uses treated timber for pergolas, outdoor decking in extreme heat and UV environments, and marine boardwalk infrastructure along Abu Dhabi and Dubai waterfronts, specifies premium water-based treatments that can handle the thermal stress of 45-degree-plus summers. Sub-Saharan Africa's demand is more utilitarian: railway tie replacement in Kenya, Tanzania, and Zambia; utility pole infrastructure serving rural electrification programs; and timber building stock in East and West African cities where treatment access is limited but the termite and fungal pressure on untreated wood in tropical climates is severe.

Competitive Landscape for Wood Preservatives Market:

Switzerland-based Lonza Group Ltd is the world's largest supplier of wood protection actives and formulated preservative systems to the lumber industry through its Lonza Wood Protection business unit, formerly Arch Wood Protection. Lonza's MicroPro and MCA (Micronized Copper Azole) products are market leaders in the residential pressure treated lumber market in the U.S., and Lonza's connections with virtually all of the large treating operators in North America and Europe translate into a breadth of distribution channels that new entrants find hard to match..

-

In 2024, Lonza Wood Protection expanded its U.S. manufacturing capacity for Micronized Copper Azole at its Conley, Georgia production facility, responding to sustained retail lumber demand that had kept MCA-grade preservative supply tight through the 2021-2024 period and created spot allocation constraints for regional treating operators during peak construction season.

Koppers Holdings Inc. is a Pittsburgh, Pennsylvania-based company that works in the areas of wood preservatives, carbon compounds, and utility and industrial wood products. The company works on a vertically integrated business model for both chemical production and timber treating. Koppers' Performance Chemicals division manufactures copper naphthenate, ACZA, and special water-based formulations. Its Railroad Products and Utility Products divisions are unusual in that they are actually the end customers for Koppers' industrial-grade chemicals, which are produced in a market where there are no pure chemical competitors to Koppers.

- In early 2025, Koppers announced a partnership with a major North American Class I railroad to expand its Treated Products supply agreement covering creosote-treated hardwood ties, with volume commitments extending through 2028 that secured baseload production planning for Koppers' treating plants in Alabama, Mississippi, and Arkansas against the backdrop of the railroad's own accelerating tie replacement program.

Wood Preservatives Market Key Players:

-

BASF SE

-

Koppers Holdings Inc.

-

LANXESS AG

-

Troy Corporation

-

Borax Inc.

-

Viance LLC

-

Remmers AG

-

Kurt Obermeier GmbH & Co. KG

-

KMG Chemicals Inc.

-

The Sherwin-Williams Company

-

RPM International Inc.

-

Akzo Nobel N.V.

-

Nippon Paint Co., Ltd.

-

Hempel A/S

-

Arkema S.A.

-

Ashland Inc.

-

Nisus Corporation

-

Janssen PMP

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.68 Billion |

| Market Size by 2035 | USD 2.73 Billion |

| CAGR | CAGR of 5.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Water-Based Preservatives, Solvent-Based Preservatives, Oil-Based Preservatives, and Others (Creosote, Bio-based, Copper/Boron-based)) • By Application (Residential (Decking, Fencing, Furniture), Commercial (Buildings, Flooring, Public Infrastructure), Industrial (Utility Poles, Railway Sleepers, Marine), and Others (Agriculture, Landscaping)) • By End-Use Industry (Construction & Infrastructure, Furniture & Wood Products, Agriculture, and Marine & Transportation) • By Treatment Method / Technology (Pressure Treatment, Brushing & Spraying, Dipping / Soaking, and Vacuum-Pressure Processes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Lonza Group Ltd, Koppers Holdings Inc., LANXESS AG, Troy Corporation, Borax Inc., Viance LLC, Remmers AG, Kurt Obermeier GmbH & Co. KG, KMG Chemicals Inc., Kop-Coat Inc., The Sherwin-Williams Company, RPM International Inc., Akzo Nobel N.V., Nippon Paint Co., Ltd., Hempel A/S, Arkema S.A., Ashland Inc., Nisus Corporation, Janssen PMP. |

Frequently Asked Questions

North America dominated the Wood Preservatives Market in 2025 with a 34.85% share.

Water-Based Preservatives dominated the Wood Preservatives Market with a 70.87% share in 2025, and they are also projected to grow at the fastest CAGR of 5.89% through 2035.

The Wood Preservatives Market is driven by growing construction and infrastructure development, increasing demand for durable and weather-resistant wood, rising residential renovation activities, expanding use in utility and marine applications, and the shift toward eco-friendly and sustainable preservative formulations.

The Wood Preservatives Market size was USD 1.68 Billion in 2025 and is expected to reach USD 2.73 Billion by 2035.

The Wood Preservatives Market is expected to grow at a CAGR of 5.04% from 2026-2035.

Get in Touch