Xanthates Market Report Scope & Overview:

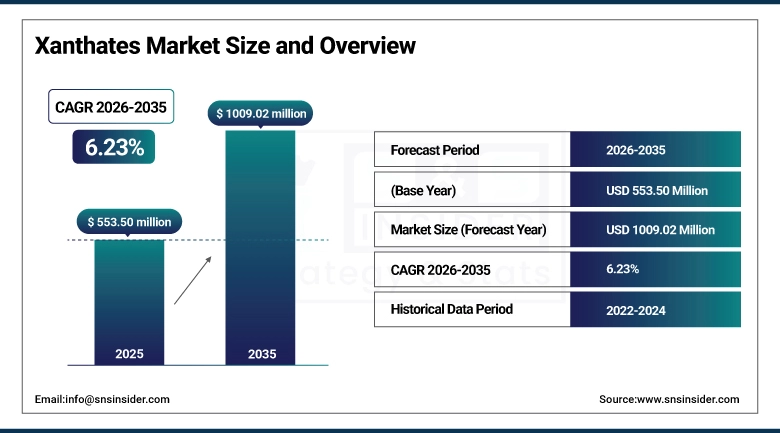

The Xanthates Market size was valued at USD 553.50 Million in 2025 and is projected to reach USD 1,009.02 Million by 2035, growing at a CAGR of 6.23% during 2026–2035.

Xanthates are organosulfur compounds produced by reacting an alkali metal hydroxide with carbon disulfide and an alcohol. Their commercial importance is almost entirely tied to one application froth flotation in mineral processing. When xanthate collectors enter a flotation pulp, they adsorb selectively onto sulfide mineral surfaces, rendering them hydrophobic so that air bubbles carry the target minerals to the surface for recovery. Without an effective collector, froth flotation the process by which the majority of the world’s copper, zinc, lead, and nickel is concentrated does not function at industrial scale.

Market Size and Forecast:

-

Market Size in 2025: USD 553.50 Million

-

Market Size by 2035: USD 1,009.02 Million

-

CAGR: 6.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Xanthates Market - Request Free Sample Report

Key Xanthates Market Trends:

-

Copper demand growth driven by electrification EV batteries, grid infrastructure, and renewable energy hardware is sustaining flotation reagent consumption at copper mines globally, with the volume of copper concentrate required per unit of clean energy deployment making collector chemical demand structurally tied to the energy transition timeline.

-

Selective collector chemistry is gaining traction over single xanthate applications in complex polymetallic ores, with blended reagent programs using combinations of xanthate types and co-collectors improving metal recovery from ore bodies that conventional single-collector programs cannot process efficiently.

-

Asia Pacific mine expansion in China, Indonesia, the Philippines, and Mongolia is driving xanthate consumption growth at a rate that significantly outpaces established Western mining markets, with domestic Chinese xanthate producers scaling capacity in parallel with the mine development programs they serve.

-

Environmental pressure on carbon disulfide uses the primary raw material in xanthate synthesis is prompting suppliers in regulated markets to invest in process enclosure and emission control, while some buyers in markets with high environmental compliance costs are evaluating alternative collector types for specific ore applications.

-

Agrochemical applications for xanthate-derived compounds are growing as crop protection product developers expand their use of xanthate intermediates in dithiocarbonate fungicide and herbicide synthesis, creating a demand pull from agricultural chemistry that operates independently of mining market cycles.

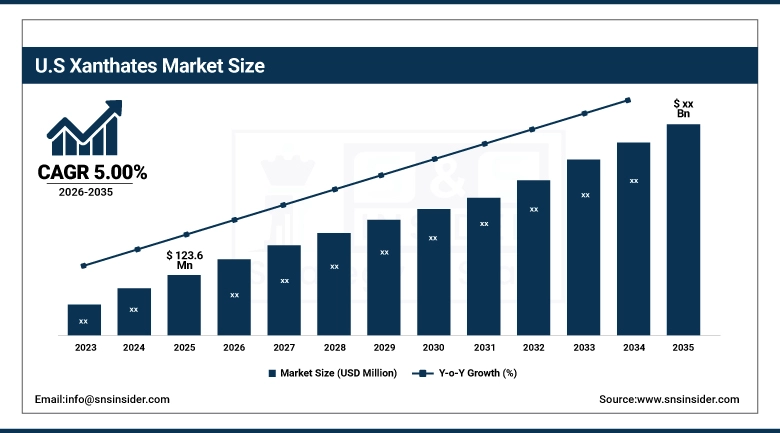

The U.S. Xanthates Market was valued at USD 123.6 Million in 2025 at a CAGR of 5.00% through 2035, anchored by copper and molybdenum mining in Arizona, Nevada, and Montana.

Xanthates Market Growth Drivers:

-

Global Copper and Base Metal Mining Expansion, Tied Directly to Electrification and Energy Transition Demand, Is the Primary and Structurally Durable Driver of Xanthate Market Growth

The connection between xanthate demand and copper production is chemical, not incidental. Copper sulfide ore, which accounts for the majority of primary copper production, is processed almost exclusively through froth flotation using xanthate collectors. Each tonne of copper concentrate requires a defined quantity of collector as a process input, and that relationship is not disrupted by efficiency improvement in the way that energy intensity relationships in other industries have been. The scale of copper demand growth projected through the 2030s driven by EV powertrains, grid transmission capacity, and renewable energy equipment implies mine production expansion that translates directly into xanthate procurement growth. Zinc, lead, and molybdenum add to this demand through the same flotation mechanism, and the polymetallic ore bodies being developed in Mongolia, Kazakhstan, and Southeast Asia for battery materials carry high sulfide mineral content that requires substantial collector inputs per tonne of feed processed. Geographical expansion into regions lacking established local reagent supply chains extends the market reach of xanthate producers into frontier mine sites beyond the established jurisdictions where the category has historically been concentrated.

Xanthates Market Restraints:

-

Raw Material Hazards, Environmental Compliance Costs, and Substitution Pressure from Alternative Collector Chemistries Are Creating Headwinds for Conventional Xanthate Producers

Carbon disulfide, the key raw material in xanthate synthesis, is a volatile, highly flammable solvent with significant occupational exposure and environmental release risks that impose compliance costs on manufacturers in regulated jurisdictions. Producers in North America and Europe carry environmental management obligations emission monitoring, solvent recovery, wastewater treatment that counterparts in less regulated markets do not, creating a structural cost disadvantage that has contributed to the geographic concentration of xanthate production in Asia over the past two decades. Substitution risk is real in certain ore types: thionocarbamates, dithiophosphates, and proprietary collector blends offer performance advantages over conventional xanthates in specific mineralogical conditions. This pressure does not threaten xanthate’s dominant market position, but it does limit the category’s addressable scope in specialty ore processing where technical differentiation matters more than cost.

Xanthates Market Opportunities:

Africa and Southeast Asia Mine Development, Specialty Agrochemical Demand, and Emerging Applications in Battery Material Processing Are Creating Growth Pathways Beyond Conventional Copper Flotation

The pipeline of mine development in sub-Saharan Africa copper-cobalt in the DRC and Zambia, nickel in Zimbabwe, gold-copper in West Africa represents new flotation reagent demand at an earlier stage of procurement infrastructure development than established regions. Xanthate suppliers establishing supply positions ahead of mine commissioning can capture long-cycle procurement relationships that are difficult to displace once metallurgical programs are optimized around a specific collector. In Southeast Asia, nickel laterite and mixed sulfide-laterite deposits in Indonesia, the Philippines, and Papua New Guinea require xanthate flotation for their sulfide mineral portions even when the broader ore body is predominantly oxide. Agrochemical applications provide a demand channel that diversifies cyclical exposure away from pure mining dependence, as dithiocarbamate fungicide demand grows with agricultural intensification in Asian and African markets.

Xanthates Market Segment Analysis:

By Type: Sodium Xanthate Leads While Amyl Xanthate Drives Fastest Growth Through 2035

Sodium Xanthate dominated with a 34.28% share in 2025 at USD 189.7 Million, while Amyl Xanthate is expected to grow at the fastest CAGR of approximately 7.38% through 2035.

Sodium xanthate’s market leadership reflects its established position as the workhorse collector chemistry for copper and zinc sulfide flotation globally it is cost-effective to produce, well-characterized in its performance across a wide range of sulfide mineralogies, and deeply embedded in the metallurgical practice of operating mines that are unlikely to change collector programs without metallurgical justification. Potassium xanthate generally favored in applications requiring slightly higher selectivity than sodium xanthate provides. Amyl xanthate is growing fastest because its longer alkyl chain delivers stronger surface hydrophobicity and improved collector power for complex or low-grade sulfide ores that are increasingly prevalent as higher-grade ore bodies are progressively depleted and mine operators are forced to process more difficult feed material.

By Application: Mining & Mineral Processing Leads While Agrochemicals Drive Fastest Growth Through 2035

Mining & Mineral Processing (Flotation Agents) dominated with a 62.48% share in 2025 at USD 345.8 Million, while Agrochemicals are expected to grow at the fastest CAGR of approximately 8.00% through 2035. The scale gap between mining flotation and all other xanthate applications reflects how foundational the collector function is to global mineral processing no commercial-scale alternative exists for sulfide ore flotation at the cost and performance point that xanthates provide, which gives the application category a captive demand structure that the others do not have. Agrochemicals are growing fastest because dithiocarbamate fungicide applications using xanthate as a chemical building block are expanding with global crop protection demand, particularly in tropical and subtropical agriculture where fungal disease pressure is high and where rising farm productivity expectations are increasing chemical input use.

By End-Use Industry: Mining Industry Leads While Agriculture Drives Fastest Growth Through 2035

Mining Industry dominated with a 64.32% share in 2025 at USD 356.0 Million, while Agriculture is expected to grow at the fastest CAGR of approximately 8.15% through 2035. The mining industry’s overwhelming end-use share simply reflects the flotation application’s scale relative to all other commercial uses of xanthate chemistry. Agriculture is growing fastest because xanthate-derived agrochemical intermediates feed into a crop protection product pipeline that is expanding in step with global agricultural intensification, with the strongest growth coming from Asian and African markets where modern crop protection chemistry is being adopted as food security pressures increase fertilizer and pesticide use.

By Form: Powder Leads While Pellet / Granules Drive Fastest Growth Through 2035

Powder dominated with a 48.36% share in 2025 at USD 267.7 Million, while Pellet / Granules are expected to grow at the fastest CAGR of approximately 6.91% through 2035. Powder xanthate holds its leading position because it dissolves quickly in flotation circuit water, is straightforward to dose accurately through automated reagent addition systems, and remains the default form specification at most operating mine flotation plants where the dosing and storage infrastructure was built around powder. Pellets and granules are growing fastest because they address real operational handling problems that powder creates: dust generation during transfer, caking in humid storage conditions, and the occupational exposure risk associated with fine particulate xanthate. Mine operators who have converted from powder to pellet or granule forms consistently report improved reagent handling safety and storage consistency, and new mine projects increasingly specify pellet or granule forms in their reagent procurement programs.

Xanthates Market Regional Analysis:

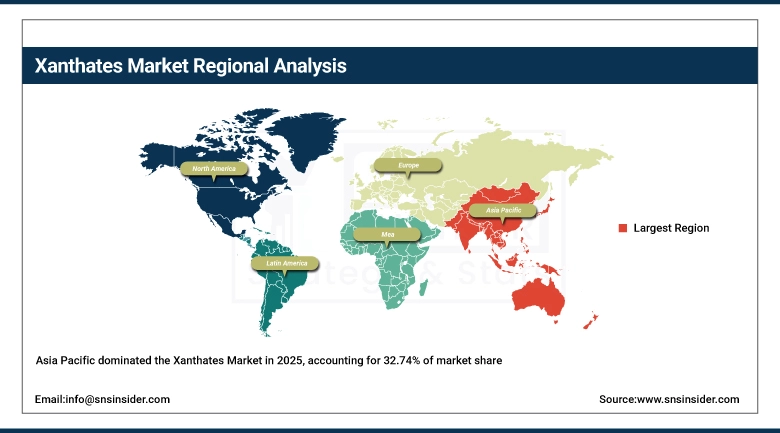

Asia Pacific Xanthates Market Insights

Asia Pacific dominated the Xanthates Market in 2025, accounting for 32.74% of market share at USD 181.2 Million, projected to reach USD 362.8 Million by 2035 at a CAGR of 7.22%. China is the dominant national market within the region, both as the world’s largest consumer of xanthate reagents in its extensive copper, zinc, and lead sulfide mining operations and as the world’s largest xanthate producer, with manufacturing capacity concentrated in Shandong, Shanxi, and Xinjiang provinces supplying domestic mines and export markets across Southeast Asia, Africa, and Latin America. Chinese producers have driven global xanthate prices lower over the past decade through scale and low-cost carbon disulfide sourcing, reshaping the competitive landscape in every region they supply.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Xanthates Market Insights

North America held a 28.46% share in 2025 at USD 157.5 Million, projected to reach USD 263.6 Million by 2035 at a CAGR of 5.32%. The United States is the dominant national market, accounting for 78.5% of North American demand at USD 123.6 Million in 2025, anchored by copper and molybdenum operations in the American Southwest and by industrial chemical procurement on the U.S. Gulf Coast. Canada accounts for 21.5% of regional share and is growing faster at 6.41% CAGR, driven by mine expansions in British Columbia’s copper-gold district and base metal operations in Ontario and Manitoba that are increasing flotation reagent consumption.

Europe Xanthates Market Insights

Europe held a 21.38% share in 2025 at USD 118.3 Million, projected to reach USD 200.3 Million by 2035 at a CAGR of 5.44%. Sweden, Finland, and Poland lead European consumption. Sweden and Finland are anchored by the Scandinavian base metal mining sector, while Poland’s KGHM operates one of Europe’s largest copper flotation complexes at Lubin and Polkowice. Germany and the UK add demand through agrochemical and rubber chemical industries that consume xanthate-derived intermediates.

Latin America and Middle East & Africa Xanthates Market Insights

Latin America held a 9.12% share in 2025 at USD 50.5 Million, projected to reach USD 95.2 Million by 2035 at a CAGR of 6.58%. Chile leads by a substantial margin as the world’s largest copper producer, with Atacama and Antofagasta belt operations at Codelco, Antofagasta Minerals, and Anglo American consuming large xanthate volumes. Peru and Mexico are secondary markets. Middle East & Africa held an 8.30% share in 2025 at USD 45.9 Million, growing to USD 87.2 Million by 2035 at 6.65% CAGR. South Africa leads through its platinum group metal and gold mining sectors. The DRC and Zambia are growing fastest as copper-cobalt mine development accelerates in the Central African copper belt.

Competitive Landscape for Xanthates Market:

AECI Mining

AECI Mining, the mining reagents division of South African chemicals group AECI, is a primary xanthate producer and supplier in the African market, with manufacturing at Modderfontein, South Africa, and a distribution network covering the sub-Saharan copper belt, Southern African platinum group metal mines, and gold operations across the continent.

In February 2025, AECI Mining started up a new production line for sodium isobutyl xanthate at Modderfontein to keep up with the increasing demand from copper-cobalt operations in the DRC and Zambia, backed by long-term supply contracts with three major copper flotation operations that used to buy from Asian manufacturers

Clariant International Ltd.

Clariant’s Mining Solutions business offers xanthate collectors as part of a broader flotation chemistry portfolio that includes frothers and specialty modifiers for copper, zinc, and molybdenum processing. The company competes on application expertise rather than on price, positioning its xanthate products within optimized reagent programs for specific ore types rather than as standalone commodity collectors.

In April 2025, Clariant launched a xanthate-based collector blend under its Hostaflot product line, developed for complex copper-gold porphyry ores with elevated organic carbon content that interferes with conventional sodium xanthate programs.

Xanthates Market Key Players:

-

AECI Mining

-

Senmin International

-

China Xanthate International (CXI)

-

Yantai Humon Chemical Auxiliary Co., Ltd.

-

Clariant International Ltd.

-

SNF Group

-

Charles Tennant & Company

-

Tieling Flotation Reagent Co., Ltd.

-

R.T. Vanderbilt Holding Company, Inc.

-

Orica Limited

-

BASF SE

-

Merck KGaA

-

Thermo Fisher Scientific Inc.

-

Suyog Chemicals

-

Rao A Group of Companies

-

Sellwell Group Flotation Reagent Factory

-

Yantai Aotong Chemical Co., Ltd.

-

China Qingdao Hong Jin Chemical Company

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 553.50 Million |

| Market Size by 2035 | USD 1009.02 Million |

| CAGR | CAGR of 6.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Sodium Xanthate, Potassium Xanthate, Amyl Xanthate, and Ethyl Xanthate) • By Application (Mining & Mineral Processing (Flotation Agents), Rubber Processing, Agrochemicals, and Chemical Intermediates) • By End-Use Industry (Mining Industry, Chemical Industry, Agriculture, and Rubber & Plastics Industry) • By Form (Powder, Pellet / Granules, and Liquid / Solution) and Region | Global Forecast 2026–2035. |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AECI Mining, Senmin International, China Xanthate International (CXI), Yantai Humon Chemical Auxiliary Co., Ltd., Coogee Chemicals, Clariant International Ltd., SNF Group, Charles Tennant & Company, Tieling Flotation Reagent Co., Ltd., Vizag Chemical International, R.T. Vanderbilt Holding Company, Inc., Orica Limited, BASF SE, Merck KGaA, Thermo Fisher Scientific Inc., Suyog Chemicals, Rao A Group of Companies, Sellwell Group Flotation Reagent Factory, Yantai Aotong Chemical Co., Ltd., China Qingdao Hong Jin Chemical Company. |

Frequently Asked Questions

Sodium Xanthate dominated the Xanthates Market with a 34.28% share in 2025.

Rising global mining activities and increasing demand for efficient flotation reagents in mineral processing are the primary drivers of the Xanthates Market.

The Xanthates Market size was USD 553.50 Million in 2025 and is expected to reach USD 1009.02 Million by 2035.

The Xanthates Market is expected to grow at a CAGR of 6.23% from 2026 to 2035.

Get in Touch