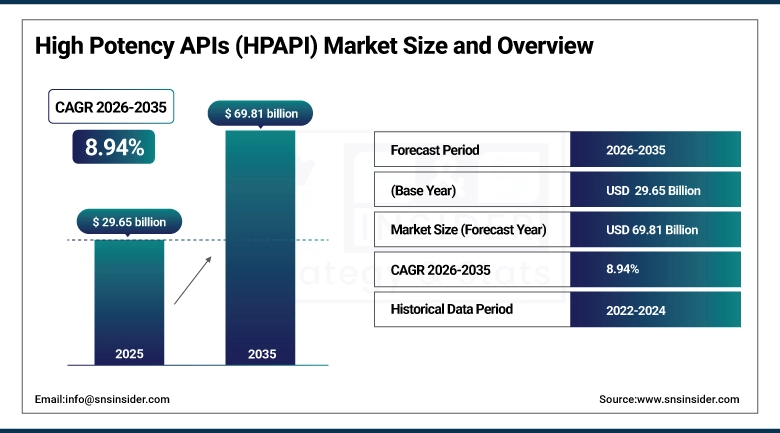

As per the SNS Insider Report titled, High Potency APIs (HPAPI) Market by Type, Therapeutic Class, by Molecule Type, by Application, by Form, by End-User, and Region, and Global Forecast 2026–2035, “The global High Potency APIs (HPAPI) Market size was valued at USD 29.65 billion in 2025, is anticipated to grow to USD 69.81 billion by 2035, registering a CAGR of 8.94% during the forecast period 2026–2035.”

Key Takeaways

-

Cytotoxic APIs accounted for the largest market share of 41.28% in 2025, driven by their extensive use in oncology therapeutics and targeted cancer treatment regimens.

-

Immunomodulators are projected to witness the fastest CAGR of 10.67% during 2026–2035 due to growing demand for advanced therapies targeting autoimmune disorders and immune-related diseases.

-

Oncology dominated the therapeutic class segment with a 52.46% revenue share in 2025, supported by the increasing global cancer burden and continued innovation in targeted oncology drugs.

-

Infectious Diseases are anticipated to expand at the fastest CAGR of 10.94% during the forecast period owing to rising investments in advanced anti-infective and antimicrobial therapies.

-

Small Molecules held the highest market share of 47.39% in 2025 due to their widespread application in commercial pharmaceutical manufacturing and established production capabilities.

-

Oligonucleotides are expected to record the fastest CAGR of 11.36% through 2035, reflecting growing interest in gene-targeted therapies and precision medicine.

-

Pharmaceuticals represented the largest application segment with a 49.84% market share in 2025 as demand for highly potent active ingredients continued to rise across therapeutic areas.

-

Contract Manufacturing is projected to grow at the fastest CAGR of 10.22% during 2026–2035 as pharmaceutical companies increasingly outsource complex HPAPI production processes.

-

Powder formulations accounted for the largest market share of 38.57% in 2025 owing to their versatility, stability, and broad usage across drug development pipelines.

-

Lyophilized APIs are forecast to register the fastest CAGR of 10.18% during the forecast period due to increasing requirements for enhanced stability and extended shelf life of biologically sensitive compounds.

-

Pharmaceutical Companies dominated the end-user segment with a 44.62% share in 2025, while Biotech Companies are expected to witness the fastest CAGR of 10.57% through 2035.

-

North America held the largest regional market share of 39.74% in 2025, while Asia-Pacific is projected to emerge as the fastest-growing regional market with a CAGR of 11.48% during 2026–2035.

Why High Potency APIs (HPAPI) Market is Growing?

The High Potency APIs (HPAPI) Market is experiencing robust growth due to the increasing prevalence of cancer, autoimmune disorders, and other chronic diseases that require highly targeted therapeutic interventions. Pharmaceutical manufacturers are increasingly investing in potent active pharmaceutical ingredients to improve treatment efficacy while minimizing systemic side effects.

The growing adoption of precision medicine and targeted therapies is significantly driving demand for HPAPIs across oncology, immunology, and rare disease applications. Advances in molecular biology, antibody-drug conjugates (ADCs), and gene-based therapeutics are further expanding the utilization of highly potent compounds in drug development pipelines.

The rising number of biologics, specialty drugs, and next-generation therapeutics entering clinical development is creating substantial demand for specialized HPAPI manufacturing capabilities. At the same time, pharmaceutical companies are increasingly relying on contract manufacturing organizations (CMOs) to manage complex production requirements, containment technologies, and regulatory compliance standards.

Furthermore, expanding healthcare expenditures, growing pharmaceutical R&D investments, and favorable regulatory support for innovative therapies are expected to sustain long-term market growth globally.

High Potency APIs (HPAPI) Market Statistics:

-

Cancer is still among the leading causes of deaths in the world, hence continued developments in oncology treatments through highly potent APIs.

-

The expansion in pharmaceutical research is centered on the area of antibody drug conjugates, cell treatments, and precise medication requiring manufacturing knowledge on HPAPIs.

-

The amount of specialty medicines undergoing clinical trials keeps increasing, thus necessitating more high containment manufacturing facilities and advanced API technologies.

-

Contraction organizations are building up HPAPI manufacturing capabilities due to an increasing outsourcing trend from global pharmaceutical and biotech firms.

-

Progress in genomic research has made more oligonucleotide medicines and other innovative forms of medicines come into existence faster than before.

-

Regulatory bodies have kept highlighting the need for stringent containment and occupational safety of highly potent substances, thus encouraging development of HPAPI manufacturing systems.

-

Rising pharmaceutical markets in Asia Pacific region are continuing with the investments in their pharmaceutical manufacturing capacity.

Emerging Trends

The market for high potency APIs (HPAPI) is currently experiencing tremendous technological innovation due to the increased uptake of targeted therapies and personalized medicine approaches. Manufacturers have been increasingly adopting advanced containment technology, continuous manufacturing techniques, and automation to ensure efficiency and enhanced safety measures.

Among the key trends that are currently impacting the market is the increased growth and development of antibody drug conjugate therapy that utilizes highly potent payloads for delivering effective targeted cancer treatments. Success in clinical trials involving ADCs has created the need for increased manufacturing of HPAPI.

Another trend in this industry is the growing uptake of novel treatment options such as oligonucleotide and peptide-based therapeutics and gene-targeted drugs. These require sophisticated expertise in the manufacture of HPAPI.

Also, collaborations between pharma companies and contract manufacturing organizations have become common practice. Such partnerships are meant to enable firms to bring products to market faster and reduce capital expenditures in building new plants.

Top 10 Companies

-

Lonza Group AG

-

Cambrex Corporation

-

Piramal Pharma Solutions

-

WuXi AppTec

-

Thermo Fisher Scientific Inc.

-

Merck KGaA

-

CordenPharma International

-

Siegfried Holding AG

-

Catalent, Inc.

-

Teva Pharmaceutical Industries Ltd.

About the Author

Get in touch