High Potency APIs (HPAPI) Market Report Scope & Overview:

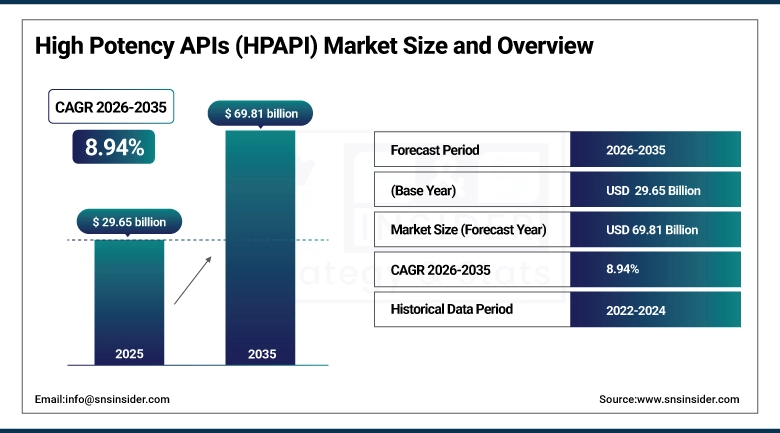

The High Potency APIs (HPAPI) Market size is valued at USD 29.65 Billion in 2025 and is projected to reach USD 69.81 Billion by 2035, growing at a CAGR of 8.94% during the forecast period 2026–2035.

The High Potency APIs (HPAPI) Market analysis report provides a comprehensive overview of drug development trends, therapeutic applications and manufacturing adoption. Rising demand for targeted therapies, increasing oncology and biotech R&D and growing contract manufacturing activities are expected to drive market growth during the forecast period.

The High Potency APIs (HPAPI) Market is expected to see over 5,200 new drug development projects by 2025, driven by rising oncology research and expanding targeted therapy initiatives.

High Potency APIs (HPAPI) Market Size and Forecast:

-

Market Size in 2025: USD 29.65 Billion

-

Market Size by 2035: USD 69.81 Billion

-

CAGR: 8.94% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on High Potency APIs (HPAPI) Market - Request Free Sample Report

High Potency APIs (HPAPI) Market Trends:

-

Rising demand for targeted and personalized therapies is driving growth in HPAPI development.

-

Increasing oncology and specialty drug research is expanding the pipeline for high-potency compounds.

-

Growth in contract manufacturing and CDMO partnerships is accelerating HPAPI production capabilities.

-

Advancements in handling, containment and formulation technologies are improving safety and operational efficiency.

-

Regulatory support for innovative drug development and biologics is facilitating faster market entry.

-

Integration of automation, digital monitoring and high-containment facilities is enhancing manufacturing precision and scalability.

U.S. High Potency APIs Market Outlook:

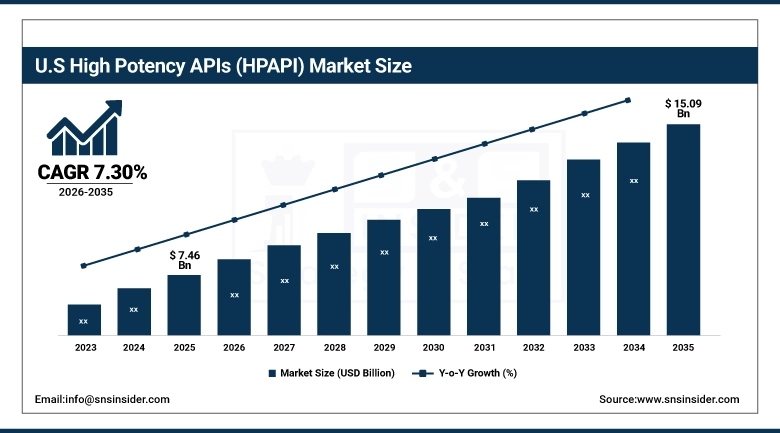

The U.S. High Potency APIs Market is projected to grow from USD 7.46 Billion in 2025 to USD 15.09 Billion by 2035, at a CAGR of 7.30%. Growth is driven by increasing oncology and targeted therapy development, expanding biotech R&D, advanced manufacturing capabilities, and supportive regulatory frameworks.

High Potency APIs (HPAPI) Market Growth Drivers:

-

Increasing demand for targeted and oncology therapies driving rapid High Potency APIs (HPAPI) market growth.

Increasing demand for targeted and oncology therapies is a key driver of the High Potency APIs (HPAPI) Market Growth. Pharmaceutical and biotech companies are focusing on developing specialized, high-potency compounds to address complex and critical diseases. Rising oncology research, expansion of contract manufacturing partnerships and adoption of advanced containment and formulation technologies are accelerating production. Regulatory support for innovative therapies, along with growing healthcare needs, is further enabling market growth and encouraging new product launches.

High Potency APIs (HPAPI) development is projected to increase by over 12% by 2025, driven by rising demand for targeted therapies and expanding oncology research initiatives.

High Potency APIs (HPAPI) Market Restraints:

-

Stringent regulatory requirements, complex handling protocols and high manufacturing costs are restraining HPAPI market growth.

Stringent regulatory requirements, complex handling protocols and high manufacturing costs pose significant restraints for the High Potency APIs (HPAPI) Market. Specialized facilities, advanced containment systems and trained personnel are required to safely produce and handle HPAPIs, increasing operational complexity. Regulatory compliance and quality assurance processes can delay product approvals. High production and infrastructure costs may limit adoption, particularly for small and mid-sized manufacturers. These challenges restrict market scalability, slowing overall growth despite rising demand for targeted therapies and oncology treatments.

High Potency APIs (HPAPI) Market Opportunities:

-

Expansion of targeted therapies and biologics presents significant opportunities for High Potency APIs (HPAPI) market growth.

Expansion of targeted therapies and biologics represents a significant opportunity for the High Potency APIs (HPAPI) Market. Growing demand for oncology, immunotherapy and specialty drugs is encouraging pharmaceutical and biotech companies to develop innovative high-potency compounds. CMO/CDMO are increasing production capabilities to meet rising needs. Advances in formulation technologies, containment systems and regulatory support further enable safe, efficient manufacturing. These developments open new avenues for market growth and adoption.

Targeted therapies and biologics are expected to account for over 28% of HPAPI production by 2025, driven by rising oncology and specialty drug demand.

High Potency APIs (HPAPI) Market Segmentation Analysis:

-

By Type, Cytotoxic APIs held the largest market share of 41.28% in 2025, while Immunomodulators are expected to grow at the fastest CAGR of 10.67% during 2026–2035.

-

By Therapeutic Class, Oncology dominated with a 52.46% share in 2025, while Infectious Diseases are projected to expand at the fastest CAGR of 10.94% during the forecast period.

-

By Molecule Type, Small Molecules accounted for the highest market share of 47.39% in 2025, while Oligonucleotides are anticipated to record the fastest CAGR of 11.36% through 2026–2035.

-

By Application, Pharmaceuticals held the largest share of 49.84% in 2025, while Contract Manufacturing is expected to grow at the fastest CAGR of 10.22% during 2026–2035.

-

By Form, Powder formulations accounted for the largest share of 38.57% in 2025, while Lyophilized APIs are forecasted to register the fastest CAGR of 10.18% during 2026–2035.

-

By End-User, Pharmaceutical Companies dominated with a 44.62% share in 2025, while Biotech Companies are expected to witness the fastest CAGR of 10.57% during the forecast period.

By Type, Cytotoxic APIs Dominate While Immunomodulators Grow Rapidly:

Cytotoxic segment dominated the market due to their extensive use in oncology drug development and chemotherapy treatments. These compounds are central to cancer therapies, with over 3,100 active oncology drug programs relying on cytotoxic APIs in 2025. Their established clinical use and large manufacturing base support dominance.

Immunomodulators is the fastest-growing segment, driven by increasing adoption in immune-oncology and autoimmune disease treatments. In 2025, more than 980 immunomodulatory drug candidates entered advanced development stages, highlighting rapid expansion.

By Therapeutic Class, Oncology Dominates While Infectious Diseases Expand Quickly:

Oncology segment dominated the market as cancer remains a primary focus of pharmaceutical research. More than 2,400 oncology-focused HPAPI-based drugs were in clinical and commercial use in 2025, reflecting strong demand for high-potency compounds. Continuous cancer prevalence and combination therapies reinforce dominance.

Infectious Diseases is the fastest-growing segment, supported by rising antimicrobial resistance and vaccine-related drug innovation. In 2025, over 620 high-potency anti-infective molecules were under development, signaling accelerating adoption.

By Molecule Type, Small Molecules Dominate While Oligonucleotides Grow Fastest:

Small-Molecule segment dominated the market due to their established manufacturing processes, scalability and widespread use across oncology and chronic diseases. In 2025, nearly 4,500 high-potency small-molecule formulations were actively manufactured or under development. This dominance reflects mature infrastructure and production readiness.

Oligonucleotides are the fastest-growing segment, fueled by advances in gene-silencing and RNA-based therapies. 410 oligonucleotide-based HPAPI programs progressed through clinical pipelines in 2025, reflecting strong momentum in precision medicine. Reinforcing the shift toward precision and personalized drug development.

By Application, Pharmaceuticals Dominate While Contract Manufacturing Accelerates:

Pharmaceutical segment dominated the market as branded and generic drug manufacturers continue expanding high-potency drug portfolios. In 2025, more than 3,800 HPAPI-based pharmaceutical products were either commercialized or in late-stage development. Strong pipelines and chronic disease prevalence support sustained demand.

Contract Manufacturing is the fastest-growing segment, driven by outsourcing trends and capacity expansion among CDMOs. Over 290 specialized HPAPI manufacturing facilities were operational in 2025, supporting rapid growth in outsourced production. Increasing focus on cost efficiency and scalability.

By Form, Powder Dominates While Lyophilized Forms Expand Rapidly:

Powder segment dominated the market due to their flexibility in formulation, long shelf life, and compatibility with multiple dosage forms. In 2025, 62% of HPAPI batches were produced in powder form for downstream processing. Widely preferred for high-containment manufacturing environments.

Lyophilized are the fastest-growing segment, supported by rising injectable and biologic drug demand. More than 1,050 lyophilized HPAPI formulations were developed in 2025, driven by stability and enhanced bioavailability requirements. Preference for parenteral oncology therapies is increasing rapidly.

By End-User, Pharmaceutical Companies Dominate While Biotech Companies Grow Fastest:

Pharmaceutical Companies segment dominated the market owing to large-scale production, extensive pipelines, and distribution networks. In 2025, over 1,900 pharmaceutical firms actively utilized HPAPIs in commercial or late-stage drugs. This dominance reflects strong manufacturing and commercialization capabilities.

Biotech companies are the fastest-growing segment, driven by innovation in targeted therapies and personalized medicine. Around 740 biotech firms advanced HPAPI-based candidates in 2025, reflecting rapid growth in specialized and niche drug development. Increased venture funding is accelerating biotech-driven HPAPI innovation.

High Potency APIs (HPAPI) Market Regional Analysis:

North America High Potency APIs (HPAPI) Market Insights:

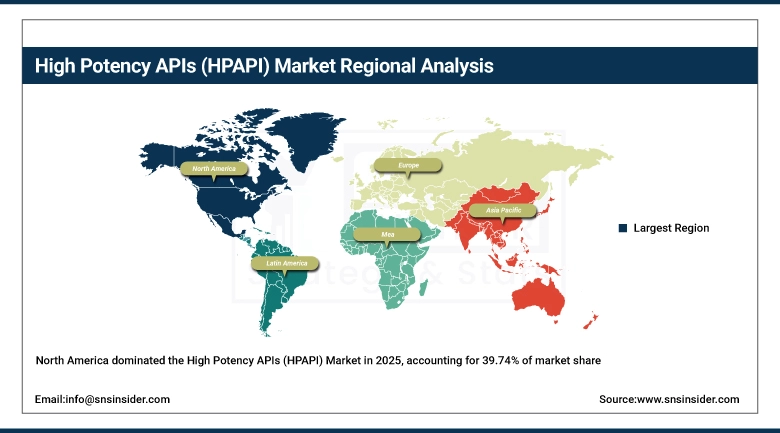

North America dominated the High Potency APIs (HPAPI) Market, holding a 39.74% market share, driven by strong oncology pipelines, advanced pharmaceutical manufacturing capabilities, and high adoption of targeted therapies. The U.S. leads regional growth, supported by robust biotech innovation, extensive CDMO networks, and stringent regulatory standards. Increasing investment in personalized medicine, expansion of high-containment manufacturing facilities, and rising collaboration between pharmaceutical and biotech companies further strengthen North America’s position as a key hub for HPAPI development and production.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. High Potency APIs (HPAPI) Market Insights:

The U.S. Adventure Tourism Market is driven by high traveler awareness, diverse activity offerings and strong safety regulations. Well-developed infrastructure, widespread access to guided tours and growing interest in eco-adventures and extreme sports support sustained participation, reinforcing the country’s leading position within the North American adventure tourism landscape.

Asia-Pacific High Potency APIs (HPAPI) Market Insights:

The Asia-Pacific High Potency APIs (HPAPI) Market is the fastest-growing region, projected to expand at a CAGR of 11.48% during the forecast period. Growth is driven by rising pharmaceutical and biotech R&D, increasing oncology and specialty drug development, and expanding contract manufacturing capabilities across China, India, Japan, South Korea, and Australia. Advancements in high-containment facilities, supportive regulatory frameworks, and adoption of biologics and targeted therapies position Asia-Pacific as a key growth engine for the HPAPI market.

China High Potency APIs (HPAPI) Market Insights:

China’s High Potency APIs (HPAPI) Market is driven by expanding pharmaceutical and biotech R&D, increasing oncology and targeted therapy development, and growing contract manufacturing capabilities. Supportive government regulations, advanced containment facilities, and rising adoption of biologics and high-potency compounds position China as a major growth contributor within the Asia-Pacific HPAPI market.

Europe High Potency APIs (HPAPI) Market Insights:

The Europe High Potency APIs (HPAPI) Market is driven by strong pharmaceutical and biotech industries, increasing oncology and specialty drug development, and advanced contract manufacturing capabilities. Countries such as Germany, France, the UK, and Italy are major contributors, supported by robust regulatory frameworks, well-established production facilities, and skilled workforce. Rising adoption of biologics, targeted therapies, and high-containment technologies, coupled with growing R&D investments, reinforces Europe’s role as a key regional market for HPAPI manufacturing and innovation.

Germany High Potency APIs (HPAPI) Market Insights:

Germany is a key High Potency APIs (HPAPI) market, supported by advanced pharmaceutical infrastructure, stringent regulatory standards, and skilled workforce. Strong oncology and specialty drug development, adoption of biologics, and contract manufacturing capabilities reinforce Germany’s position as a leading contributor within the European HPAPI manufacturing and innovation landscape.

Latin America High Potency APIs (HPAPI) Market Insights:

The Latin America High Potency APIs (HPAPI) Market is witnessing steady growth driven by expanding pharmaceutical R&D, increasing oncology and specialty drug development, and improving manufacturing infrastructure. Countries such as Brazil, Mexico, and Argentina are key contributors, supported by growing contract manufacturing capabilities, biologics adoption, and supportive regulatory initiatives.

Middle East and Africa High Potency APIs (HPAPI) Market Insights:

The Middle East & Africa High Potency APIs (HPAPI) Market is expanding due to increasing pharmaceutical R&D, rising demand for oncology and specialty therapies, and improving manufacturing infrastructure. Countries such as Saudi Arabia, the UAE, and South Africa are key contributors, supported by contract manufacturing growth and regulatory support for high-potency compounds.

High Potency APIs (HPAPI) Market Competitive Landscape:

Pfizer Inc. is a leading biopharmaceutical company headquartered in the U.S., with a broad portfolio spanning oncology, vaccines, and specialty therapies. In the High Potency APIs (HPAPI) market, Pfizer dominates through extensive R&D investments, advanced manufacturing facilities, and strategic acquisitions that expand its high‑potency drug pipeline. The company’s focus on targeted therapies, biologics, and cutting‑edge containment technologies strengthens its production capabilities and market presence, making it a trusted partner for HPAPI supply and innovation.

-

In March 2025, Pfizer announced positive topline results for its Phase 3 LP.8.1‑adapted COMIRNATY COVID‑19 vaccine, reinforcing its advanced high‑potency biologics pipeline and strengthening targeted formulations for diverse patient populations.

Novartis AG, a Swiss multinational pharmaceutical leader, is recognized for its strong emphasis on innovative medicines, including high‑potency APIs for oncology and specialty treatments. The company leverages significant R&D investment and advanced biomanufacturing technologies to expand its HPAPI portfolio and therapeutic reach. Novartis’ collaborations with biotech firms and focus on personalized medicine drive its market influence. Its production footprint and commitment to innovation enable sustained growth and competitive advantage in the HPAPI landscape.

-

In April 2025, Novartis received regulatory approvals for oncology and rare disease therapies, including Pluvicto and Vanrafia, enhancing its high‑potency therapeutic portfolio and expanding precision medicine treatment options across cancer and nephrology markets.

Merck & Co., Inc. is a major U.S. pharmaceutical and life sciences company known for its robust research programs and portfolio of high‑impact therapies. In the High Potency APIs (HPAPI) market, Merck drives growth through innovative drug development especially in oncology and biologics and investments in state‑of‑the‑art manufacturing infrastructure. Its dedication to quality, regulatory compliance, and advanced production technologies supports HPAPI demand while reinforcing Merck’s position as a key contributor to precision medicine and targeted treatment solutions.

-

In May 2025, Merck announced the U.S. launch of a subcutaneous version of Keytruda, improving patient convenience, increasing accessibility, and extending the reach of its high‑impact immunotherapy and HPAPI-based oncology treatments.

High Potency APIs (HPAPI) Market Key Players:

-

Pfizer Inc.

-

Novartis AG

-

Merck & Co., Inc.

-

GSK plc

-

Bristol-Myers Squibb Company

-

Sanofi S.A.

-

AstraZeneca plc

-

Teva Pharmaceutical Industries Ltd.

-

Lonza Group Ltd.

-

Boehringer Ingelheim International GmbH

-

Roche Holding AG (F. Hoffmann‑La Roche Ltd.)

-

AbbVie Inc.

-

Catalent, Inc.

-

Cambrex Corporation

-

Siegfried Holding AG

-

Dr. Reddy’s Laboratories Ltd.

-

CordenPharma International

-

Albany Molecular Research, Inc.

-

Sun Pharmaceutical Industries Ltd.

-

WuXi AppTec

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 29.65 Billion |

| Market Size by 2035 | USD 69.81 Billion |

| CAGR | CAGR of 8.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Cytotoxic, Non-Cytotoxic, Immunomodulators, Hormonal) • By Therapeutic Class (Oncology, Cardiovascular, CNS, Respiratory, Infectious Diseases) • By Molecule Type (Small Molecule, Biologics, Peptides, Oligonucleotides) • By Application (Pharmaceuticals, Contract Manufacturing, Research & Development, Diagnostics) • By Form (Powder, Capsules, Injectable Solutions, Lyophilized, Granules) • By End-User (Pharmaceutical Companies, Biotech Companies, Hospitals & Clinics, Research Institutes, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pfizer Inc., Novartis AG, Merck & Co., Inc., GSK plc, Bristol-Myers Squibb Company, Sanofi S.A., AstraZeneca plc, Teva Pharmaceutical Industries Ltd., Lonza Group Ltd., Boehringer Ingelheim International GmbH, Roche Holding AG (F. Hoffmann La Roche Ltd.), AbbVie Inc., Catalent, Inc., Cambrex Corporation, Siegfried Holding AG, Dr. Reddy’s Laboratories Ltd., CordenPharma International, Albany Molecular Research, Inc., Sun Pharmaceutical Industries Ltd., WuXi AppTec |

Frequently Asked Questions

The High Potency APIs (HPAPI) Market size is valued at USD 29.65 Billion in 2025.

The market is projected to reach USD 69.81 Billion by 2035, indicating strong long-term growth potential.

The market is expected to grow at a compound annual growth rate (CAGR) of 8.94% during the forecast period from 2026 to 2035.

Key growth drivers include the rising prevalence of cancer, increasing demand for targeted therapies, growth in oncology drug development, and advancements in biopharmaceutical manufacturing.

Oncology remains the leading therapeutic segment, followed by hormonal disorders, autoimmune diseases, and other chronic conditions requiring potent drug formulations.

Get in Touch