5G Device Testing Market Size & Trends:

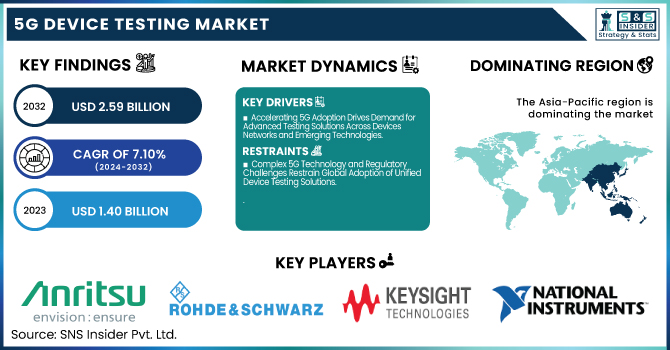

The 5G Device Testing Market was valued at USD 1.40 billion in 2023 and is expected to reach USD 2.59 billion by 2032, growing at a CAGR of 7.10% over the forecast period 2024-2032. 5G Device With the rising complexity of 5G-enabled devices and changing network standards, the market for equipment used in 5G device testing is forecasted to have higher usage. Increased prototype and production testing demands are prompting test labs to operate at ever higher capacity utilization. The technology adoption continues to be fast, particularly in mmWave and standalone 5G areas whereas the validation tools have to be more sophisticated.

To Get More Information About 5G Device Testing Market - Request Free Sample Report

Also, the growing need for compliance and conformance testing as manufacturers must comply with global certification and interoperability standards is expected to boost the Market Industry. Growing adoption of 5G technologies in telecommunications, automotive, healthcare, and other sectors, has led to substantial development in the U.S. 5G device testing market. The ramp-up in availability of 5G services by the major network operators, Verizon, AT&T, and T-Mobile drew more usage out of the testing gear. Manufacturers needed to comply with stringent regulatory standards, consequently, demand for compliance and conformance testing peaked.

The U.S. 5G Device Testing Market is estimated to be USD 0.29 Billion in 2023 and is projected to grow at a CAGR of 7.45%. Growing demand for ultra-low latency and high-speed 5G connectivity in autonomous vehicles, smart cities, and industrial automation is driving the demand for the U.S. 5G device testing market. This has amplified the need for testing nationwide as private 5G networks grow, mmWave technology advances, and demand interoperability over different devices.

5G Device Testing Market Dynamics

Key Drivers:

-

Accelerating 5G Adoption Drives Demand for Advanced Testing Solutions Across Devices Networks and Emerging Technologies

The global 5G device testing market is gaining traction due to the rapid rollout of 5G networks across the globe which is driving the demand for advanced testing solutions to ensure uninterrupted connectivity, ultra-low latency, and high-speed data transfer. Also, the increasing use of IoT, autonomous vehicles, and smart devices is another contributing factor to the growth of SSD Test Equipment markets, as it is mandatory to test the performance for all types of applications. At the same time, the growing number of 5G applications combined with strict regulatory standards and increasing investments in R&D by telecom equipment manufacturers and semiconductor companies continue to drive a greater need for advanced spectrum analyzers for 5G millimeter-wave, network analyzers, and oscilloscopes. In addition to that, the combination of Open RAN (O-RAN) and virtualization in the telecom infrastructure is also helping in the market growth as they need novel testing solutions to ensure network reliability and interoperability.

Restrain:

-

Complex 5G Technology and Regulatory Challenges Restrain Global Adoption of Unified Device Testing Solutions

The complexity of 5G technology is one of the major restraints for the 5G device testing market as the 5G device testing market needs highly specialized testing equipment and expertise. While 5G spans across several frequency bands, including mmWave, which are all more susceptible to signal interference, penetration problems, and beamforming complexity than their predecessors. To test accurately across these varied frequency ranges, we need ongoing innovations in testing methodologies and capabilities. Even currently, unequal standardization worldwide creates a bottleneck for manufacturers due to a necessity to meet various regulatory requirements and testing protocols, making global testing solutions tricky to adopt.

Opportunity:

-

Rising 6G Research and Private Networks Unlock New Opportunities for Advanced 5G Testing Solutions

6G being in the research and development phase also opens a massive opportunity for 5G test equipment manufacturers, as next-gen wireless will require more sophisticated tests. Additionally, the escalation from software-defined and AI-integrated testing solutions paves the way for automation-centric 5G test solutions to accelerate the time to market of 5G devices. The growing adoption of private 5G networks by many industries including manufacturing, healthcare, and smart cities opens new opportunities for dedicated testing solutions. Moreover, there is also a need for low-cost and compact portable 5G testing solutions, especially among IDMs and ODMs, which will promote innovation in payload programming with compact yet high-performance test devices.

Challenges:

-

Evolving Mobile Networks Demand Scalable AI Driven Testing Solutions Beyond Legacy Approaches and Traditional Tools

As 5G matures and 6G looms on the horizon, the ever-evolving nature of mobile technology presents a particular problem for test equipment vendors, which continually have to give constant updating to their solutions to align with new network designs, AI-powered optimization, and virtualized network functions (VNFs). Also, moving to more SDN and cloud-native infrastructures in telecom networks needs new testing strategies that cost companies in terms of new testing tools on a flexible, AI-driven, and automated basis. Yet, massive IoT and edge computing use cases run the risk of being strangled by legacy testing approaches, as traditional validation techniques depending on modeling prescriptive semi-analytical solutions are not scalable for very wide geographical networks needed to reach cost-optimal deployments in 5G nor validate the performance of highly distributed & ultra-low-latency 5G networks.

5G Device Testing Industry Segment Analysis

By Equipment Type

Spectrum analyzers accounted for 36.3% of the share in the 5G device testing market in 2023. The high percentage was due to the essentiality of spectrum analyzers in providing signal integrity, frequency accuracy, and interference level information in 5G networks. As mmWave frequencies and massive MIMO deployments continue to grow in complexity, spectrum analyzers play a critical role in delivering the confidence of proper network performance and compliance with global standards.

The network analyzers segment is projected to expand at the highest CAGR during the forecasting years from 2024 to 2032, due to the increasing demand for high-accuracy testing of 5G network parts, such as antennas, RF modules, and transmission systems. The idea of manipulating and performance validates fully open telecom infrastructure layers based on paradigms like Open RAN, software-defined network (SDN), and end-to-end AI-driven optimizations will need a lot of more comprehensive network analysis & real-time skillsets. As the 5G market expands into new areas and more functionalities, this trend will also force manufacturers to develop advanced, automated, and portable network analyzers to facilitate next-generation 5G and 6G network deployment and testing.

By Equipment Type

The 5G devices testing market in 2023 was dominated by telecom equipment manufacturers, with a 58.4% market share. This strong position was underpinned by their large investments into 5G infrastructure buildout, in terms of both base stations as well as antennas and network elements. While 5G networks continue to flourish across the globe, telecom equipment manufacturers are still utilizing ubiquitous testing solutions like spectrum analyzers, network analyzers, and signal generators to test performance, compliance, and connectivity.

From 2024-2032, IDMs (Integrated Device Manufacturers) & ODMs (Original Design Manufacturers) will have the highest CAGR. This growth is driven by the increasing demand for bespoke 5G devices, chipsets, and RF components, and also due to the wider adoption of private 5G networks in various industries. The focus has turned to AI-powered small, economic testing solutions, through which IDMs & ODMs are earmarking funds for cutting-edge testing tools to fast-track product innovation and time-to-market.

5G Device Testing Market Regional Insights

In 2023, the 5G device testing market in Asia Pacific accounted for the largest revenue share of 36.8%, owing to extensive 5G rollouts in multiple active markets, continuous government and financial backing, and unlimited innovations in 5G in China, Japan, South Korea, India, and other Asia Pacific nations. With top telecom companies including Huawei and ZTE operating across the country, China has attempted a more massive deployment of 5G base stations and networks, generating a high demand for test solutions. With a 5G mmWave technology leadership role assumed by Samsung, South Korea has quickly increased demand for interpreters and system analyzers. Meanwhile, the rollout of 5G in India aided by Reliance Jio and Bharti Airtel is driving testing solutions in this sector as well.

From 2024-2032, North America is anticipated to experience the highest CAGR, thanks to rising investments in 5G and 6G research, private 5G networks, and Open RAN technology. Of course, the USA having its market leaders for telecom like Qualcomm, Verizon, and AT&T is spending aggressively on testing and validation of 5G devices to make sure that they can provide the best network experience. Likewise, Keysight Technologies and Rohde & Schwarz are further innovating 5G testing solutions in response to increasing demand in the industry. The growth of 5G test devices in North America will be propelled by the need for the expansion of smart cities, autonomous vehicles, industrial IoT, and automation.

Get Customized Report As Per Your Business Requirement - Enquiry Now

Key Players Listed in 5G Device Testing Market are:

-

Anritsu (MT8000A Radio Communication Test Station)

-

Rohde & Schwarz (R&S®CMX500 5G One-Box Signaling Tester)

-

Keysight Technologies (Keysight UXM 5G Wireless Test Platform)

-

National Instruments Corp. (NI TestStand)

-

Teradyne, Inc. (UltraFLEX Test System)

-

Advantest Corporation (V93000 SoC Test System)

-

SPEA (Flying Probe Testers)

-

FormFactor (Autonomous RF Measurement Assistant)

-

Viavi Solutions Inc. (TM500 Network Tester)

-

LitePoint (IQgig-5G Non-Signaling Test Solution)

-

Spirent Communications (Spirent 8100 Mobile Device Test System)

-

Teledyne LeCroy (Frontline X500 Wireless Protocol Analyzer)

-

EXFO Inc. (EXFO 5GPro Test Solution)

-

Rohm Semiconductor (LAPIS Development Board for 5G Testing)

-

Tektronix (Tektronix RSA5000 Real-Time Spectrum Analyzer)

Recent Trends

-

In August 2024, Anritsu enhanced its ME7873NR Lite Model, transforming it into a one-box tester for 5G RF and protocol conformance testing, reducing test time by 20%.

-

In March 2025, Rohde & Schwarz and Pegatron 5G showcased a new O-RU test solution using the PVT360A at MWC 2025, enhancing Open RAN production testing.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.40 Billion |

| Market Size by 2032 | USD 2.59 Million |

| CAGR | CAGR of 7.10% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Equipment Type (Oscilloscopes, Signal Generators, Spectrum Analyzers, Network Analyzers, Others) • By End Use (IDMs & ODMs, Telecom Equipment Manufacturer) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Anritsu, Rohde & Schwarz, Keysight Technologies, National Instruments Corp., Teradyne, Inc., Advantest Corporation, SPEA, FormFactor, Viavi Solutions Inc., LitePoint, Spirent Communications, Teledyne LeCroy, EXFO Inc., Rohm Semiconductor, Tektronix. |

Frequently Asked Questions

Asia Pacific dominated the 5G Device Testing Market in 2023.

The Spectrum Analyzers segment dominated the 5G Device Testing market in 2023.

Ans: The major growth factor of the 5G device testing market is the global rollout of complex 5G networks, driving demand for advanced, high-frequency, and automated testing solutions.

5G Device Testing Market size was USD 1.40 Billion in 2023 and is expected to Reach USD 2.59 Billion by 2032.

The 5G Device Testing Market is expected to grow at a CAGR of 7.10% during 2024-2032.

Get in Touch