Agricultural Microbial Market Report Scope & Overview:

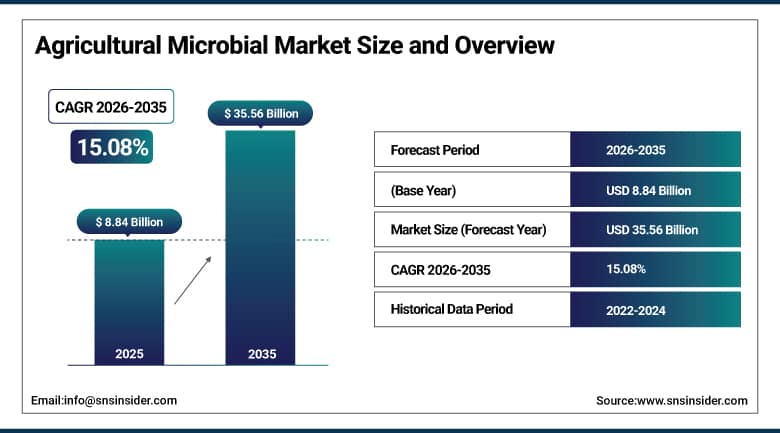

The Agricultural Microbial Market was valued at USD 8.84 Billion in 2025 and is expected to reach USD 35.56 Billion by 2035, growing at a CAGR of 15.08% from 2026 to 2035.

The global agricultural microbial market plays a critical role in advancing sustainable agriculture and improving crop productivity while reducing dependence on synthetic agrochemicals. Agricultural microbial products consist of beneficial microorganisms such as bacteria, fungi, and other naturally occurring microbes that enhance nutrient availability, improve soil health, promote plant growth, and provide biological protection against pests and diseases. Increasing regulatory pressure on chemical inputs, rising adoption of organic and regenerative farming practices, and growing demand for environmentally sustainable crop production solutions are accelerating the deployment of microbial technologies across both developed and emerging agricultural economies. The market encompasses a broad range of microbial-based solutions used throughout the crop production cycle to improve yield performance, nutrient-use efficiency, and overall farm profitability.

UPL Limited, a major global agrochemical and biological solutions provider, reported revenues of approximately USD 5.6 billion in FY2024, with its microbial and natural plant protection portfolio acting as a high-growth segment driven by expansion in bio-solutions, regenerative agriculture initiatives, and increasing farmer transition toward residue-free crop protection systems.

Market Size and Forecast:

-

Market Size in 2026E: USD 10.05 Billion

-

Market Size by 2035: USD 35.56 Billion

-

CAGR: 15.08% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Agricultural Microbial Market - Request Free Sample Report

Agricultural Microbial Market Trends:

-

Rising global adoption of sustainable agriculture practices is accelerating demand for microbial-based crop inputs across conventional and organic farming systems.

-

Increasing regulatory restrictions on chemical fertilizers and pesticides are driving rapid substitution with biofertilizers and biopesticides.

-

Advancements in microbial strain engineering and fermentation technologies are improving product efficiency, stability, and field performance.

-

Growing focus on soil health restoration and regenerative agriculture is boosting long-term adoption of soil-beneficial microbial solutions.

-

Integration of microbial products with precision agriculture and data-driven farming systems is enhancing targeted application and yield outcomes.

The U.S. Agricultural Microbial Market Outlook:

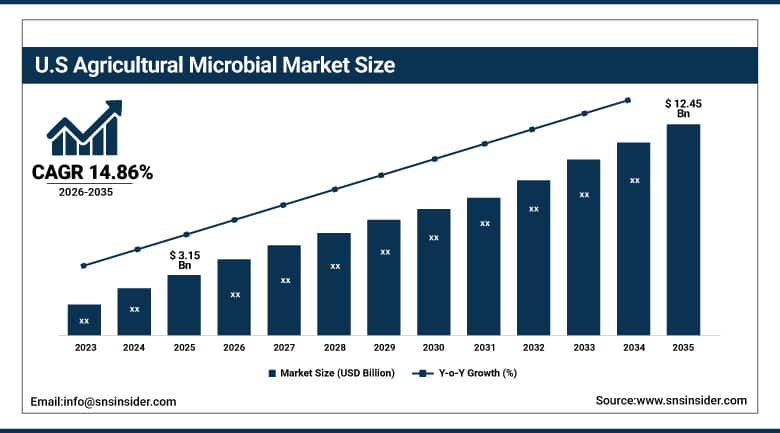

The U.S. Agricultural Microbial Market was valued at USD 3.15 Billion in 2025 and is expected to reach USD 12.45 Billion by 2035, growing at a CAGR of 14.86%.

The United States dominates the agricultural microbial market in North America due to its highly developed commercial agriculture sector, widespread adoption of sustainable farming practices, and strong integration of microbial biofertilizers, biopesticides, and plant growth-promoting microorganisms across major row crops such as corn, soybean, and wheat. The country’s advanced agricultural infrastructure and large-scale farming operations enable rapid deployment of microbial technologies to improve yield efficiency and soil health. Additionally, increasing regulatory pressure to reduce synthetic fertilizer and pesticide usage, along with growing concerns over soil degradation and environmental sustainability, is significantly accelerating the transition toward microbial-based agricultural inputs across U.S. farming systems.

Corteva Agriscience expanded field adoption of its microbial seed-applied technologies in the U.S. corn and soybean belt, with increased farmer uptake driven by improved nitrogen-use efficiency and yield stability under drought-affected and variable weather conditions, reinforcing the role of microbial solutions in next-generation precision agriculture systems.

Agricultural Microbial Market Segment Analysis:

-

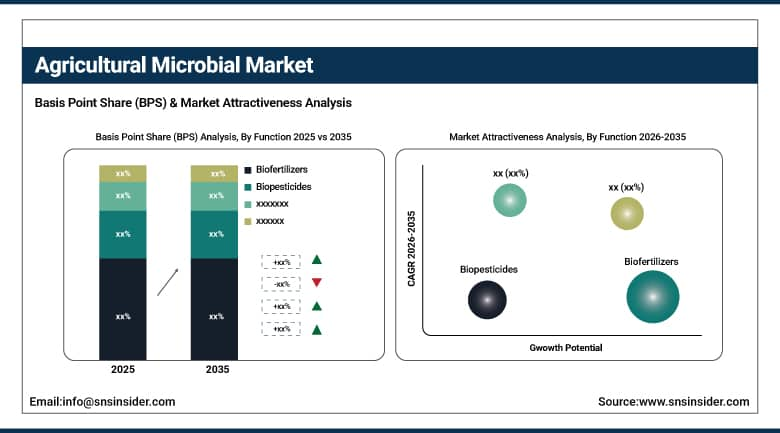

By Function, biofertilizers dominated the market with 38.45% share in 2025, while biopesticides emerged as the fastest-growing segment with the highest CAGR of 15.74% from 2026 to 2035.

-

By Formulation Type, liquid formulations dominated the market with 46.15% share in 2025, while seed treatment formulations is the fastest-growing segment with the highest CAGR of 16.24% from 2026 to 2035.

-

By Crop Type, cereals & grains dominated the market with 41.21% share in 2025, while fruits & vegetables is the fastest-growing segment with the highest CAGR of 15.95% from 2026 to 2035.

-

By Application Method, seed treatment dominated the market with 35.16% share in 2025, while soil treatment is the fastest-growing segment with the highest CAGR of 15.60% from 2026 to 2035.

By Function, biofertilizers dominate the agricultural microbial market, while biopesticides represent the fastest-growing segment.

Biofertilizers segment dominated the market with the highest revenue share of 38.45% in 2025, primarily driven by their large-scale adoption in enhancing soil fertility, improving nutrient availability, and supporting nitrogen fixation in major crops such as cereals, pulses, and oilseeds. Their strong role in reducing dependency on chemical fertilizers, combined with increasing awareness of soil degradation and sustainability practices, has significantly strengthened their position across both developed and emerging agricultural economies. Continuous government support for organic farming programs and subsidies for biological inputs further reinforce market penetration.

Biopesticides segment is expected to register the highest CAGR of 15.74% from 2026 to 2035, supported by rising regulatory pressure on synthetic pesticide usage, increasing global demand for residue-free food, and rapid expansion of export-oriented horticulture and fruit production. In addition, advancements in microbial strains and formulation technologies are improving efficacy, shelf life, and field stability, accelerating adoption across integrated pest management (IPM) systems worldwide.

By Formulation Type, liquid formulations dominate the agricultural microbial market, while seed treatment formulations are the fastest-growing segment.

Liquid formulations held the largest share of 46.15% in 2025, owing to their superior ease of application, faster microbial activation in soil environments, and higher uniformity in field distribution compared to dry alternatives. These formulations are widely preferred in large-scale commercial agriculture due to their compatibility with irrigation systems, foliar sprays, and fertigation techniques, ensuring consistent performance across diverse agro-climatic conditions. Their strong adoption is also supported by improved storage stability and better farmer familiarity.

Seed treatment formulations are projected to grow at the highest CAGR of 16.24% during 2026–2035, driven by increasing adoption of precision agriculture and early-stage crop protection strategies. These formulations provide targeted microbial delivery directly at the seed level, enhancing germination rates, root development, and early plant Vigor. Growing awareness of yield optimization at the initial crop stage, along with rising mechanization in seed processing industries, is further accelerating demand globally.

By Crop Type, cereals & grains dominate the agricultural microbial market, while fruits & vegetables are the fastest-growing segment.

Cereals & grains accounted for the largest revenue share of 41.21% in 2025, attributed to their extensive cultivation area across major agricultural economies and their critical role in global food security. High adoption of microbial inputs in crops such as wheat, rice, and maize is driven by the need to enhance productivity, improve soil nutrient cycling, and maintain yield stability under increasing climatic stress conditions. The scalability of microbial solutions in large-acreage farming further strengthens this segment’s dominance.

Fruits & vegetables segment is expected to record the highest CAGR of 15.95% from 2026 to 2035, supported by rising consumer preference for high-quality, residue-free, and organically grown produce. This segment is also benefiting from increasing export requirements, stricter pesticide residue regulations, and intensive microbial usage in high-value horticultural farming systems such as berries, tomatoes, and leafy vegetables, where yield quality and appearance are critical.

By Application Method, seed treatment dominates the agricultural microbial market, while soil treatment is the fastest-growing segment.

Seed treatment segment dominated the market with 35.16% share in 2025, due to its ability to deliver early-stage crop benefits including improved germination rates, enhanced root establishment, and stronger resistance against soil-borne pathogens. Its cost-effectiveness, ease of integration into existing seed processing workflows, and measurable yield improvement outcomes make it the most widely adopted microbial application method across both commercial and subsistence farming systems.

Soil treatment segment is projected to grow at the highest CAGR of 15.60% during 2026–2035, driven by increasing emphasis on long-term soil health restoration, microbial soil conditioning, and sustainable nutrient cycling practices. Rising concerns over soil degradation, declining organic matter content, and intensive monocropping practices are accelerating adoption of soil-applied microbial solutions that improve soil biodiversity, structure, and long-term productivity.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.54% |

|

Europe |

Germany |

34.45% |

|

Asia pacific |

China |

43.34% |

|

Middle East & Africa |

UAE |

33.91% |

|

Latin America |

Brazil |

42.60% |

North America Agricultural Microbial Market Insights

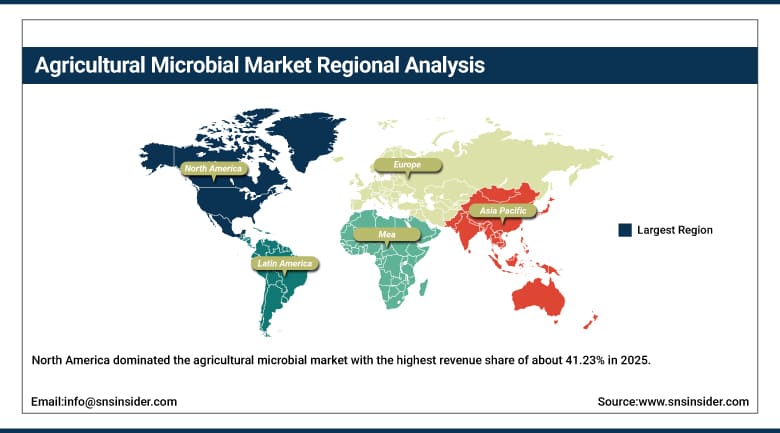

North America dominated the agricultural microbial market with the highest revenue share of about 41.23% in 2025, supported by advanced agricultural practices, high mechanization levels, and continuous reinvestment in sustainable farming inputs. The region benefits from widespread adoption of precision agriculture technologies, where microbial products are increasingly integrated with digital farming platforms, variable rate application systems, and soil health monitoring tools to optimize input efficiency and yield outcomes across large-scale commercial farms. Canada further strengthens regional demand through its Prairie provinces, where microbial adoption is increasingly aligned with oilseed and pulse crop rotations supported by sustainability-linked farm programs.

A key development is the rapid expansion of organic and sustainable farming acreage, with the United States alone operating 4.9+ million acres of certified organic farmland, creating a strong base for microbial input adoption in nutrient management and crop protection. In addition, microbial seed treatment usage is expanding rapidly, supported by documented field trials showing 20–30% yield improvement in nitrogen-fixing bacterial applications under controlled conditions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Agricultural Microbial Market Insights

The European agricultural microbial market is strongly shaped by one of the world’s most stringent regulatory environments, particularly under frameworks restricting chemical fertilizer and pesticide usage. This regulatory pressure is actively accelerating the shift toward biological crop inputs, with microbial solutions being increasingly positioned as compliant, low-residue alternatives that align with the European Union’s Green Deal and Farm to Fork Strategy objectives. Countries such as Germany, France, and the Netherlands are at the forefront of integrating microbial solutions into high-value horticulture and protected cultivation systems, where yield optimization and soil health restoration are critical priorities.

The European Union’s Farm to Fork Strategy is a major structural driver, targeting a 50% reduction in pesticide use and risk and expansion of organic farmland to 25%, significantly increasing microbial product uptake across horticulture and vineyard systems.

Asia-Pacific Agricultural Microbial Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 15.83% during 2026–2035. driven by large-scale agricultural modernization and increasing pressure to improve soil productivity across intensively cultivated regions. Governments in China and India are actively promoting sustainable farming initiatives, including subsidies for biofertilizers and biopesticides, which is significantly accelerating farmer-level adoption of microbial inputs in staple crop production systems. Another major development is the rising integration of microbial technologies in horticulture and export-oriented agriculture, particularly in countries such as China, India, and Australia. The primary growth drivers include rising demand for sustainable, residue-free farming, government support for biological inputs, and worsening soil health.

A major development is the scale of microbial field adoption programs, where China has recorded over 500,000 tons of microbial fertilizer sales, with 72% year-on-year expansion in certain provincial agricultural zones, particularly in rice, tea, and horticulture cultivation systems. In India, adoption is also accelerating rapidly, with biofertilizer usage reaching 3.6 million tonnes across millions of hectares, supported by government subsidy programs covering ₹31,000 per hectare under organic farming schemes such as PKVY.

Latin America &MEA Agricultural Microbial Market Insights

Latin America and Middle East & Africa agricultural microbial market is increasingly shaped by the region’s focus on climate-resilient agriculture and soil productivity enhancement in arid and semi-arid environments. Governments in Gulf countries are actively investing in controlled-environment agriculture, hydroponics, and desert farming initiatives, where microbial solutions are used to improve nutrient efficiency and plant stress tolerance under extreme climatic conditions.

The Latin American agricultural microbial market is strongly influenced by its large-scale commercial agriculture base, where microbial inputs are increasingly being adopted to enhance soil fertility and improve productivity in export-oriented crops such as soybeans, coffee, sugarcane, and fruits. Brazil and Argentina are leading the shift toward biological farming inputs, supported by expanding practices that create favorable conditions for microbial soil activity.

A key development is the rapid expansion of no-till farming practices, which now cover over 60% of soybean cultivation areas in Brazil, creating highly favorable conditions for microbial soil activity and long-term biological nutrient cycling. In Africa, adoption is being driven by large-scale soil restoration initiatives, where microbial products such as Trichoderma and mycorrhiza-based formulations are increasingly deployed across millions of hectares of degraded farmland.

Market Dynamics:

Growth Drivers: Expanding sustainable agriculture adoption and regulatory shift toward biological inputs

The agricultural microbial market is strongly driven by the global shift toward sustainable and regenerative agriculture practices, supported by increasing soil degradation concerns and declining chemical fertilizer efficiency across intensive farming systems. Governments across North America, Europe, and Asia-Pacific are actively promoting bio-based inputs through subsidy programs, soil health missions, and organic farming expansion targets, accelerating microbial adoption across cereals, fruits, and plantation crops. Additionally, rising awareness among farmers regarding long-term productivity benefits has increased field-level adoption, with microbial solutions improving nutrient use efficiency, nitrogen fixation, and crop resilience. The rapid expansion of organic farmland globally further strengthens structural demand for biofertilizers and biopesticides.

Restraints: Performance variability, limited farmer awareness, and shelf-life constraints of microbial formulations

Despite strong growth momentum, the agricultural microbial market faces key restraints related to inconsistent field performance under varying soil, temperature, and moisture conditions, which limits farmer confidence in some regions. Microbial efficacy is highly dependent on environmental factors, making results less predictable compared to synthetic agrochemicals, particularly in degraded or extreme climatic soils. In addition, limited awareness among smallholder farmers in developing economies continues to restrict adoption, especially where traditional chemical inputs dominate established farming practices. Product shelf-life and storage sensitivity of certain liquid and live microbial formulations also create logistical challenges in distribution, particularly in hot and humid regions with weak cold-chain infrastructure.

Opportunities: Precision agriculture integration and expansion in emerging high-value crop markets

The agricultural microbial market presents significant opportunities through integration with precision agriculture technologies, including digital soil mapping, variable rate application systems, and AI-based crop monitoring platforms that optimize microbial input efficiency. The increasing adoption of seed treatment technologies and fertigation-compatible microbial formulations is enabling targeted delivery and improved yield outcomes, particularly in large-scale commercial farming systems. Additionally, rapid expansion of high-value crop cultivation such as fruits, vegetables, and export-oriented horticulture in Asia-Pacific and Latin America is creating strong demand for residue-free crop protection solutions. Emerging economies are also witnessing growth in agri-biotech startups, expanding localized production and distribution networks, which significantly enhances accessibility and market penetration of microbial products.

Recent Developments:

-

2026: Novozymes A/S and Chr. Hansen Holding A/S (Novonesis) expanded their next-generation microbial consortium platform targeting multi-strain biofertilizers designed to improve nutrient efficiency and stress tolerance in cereals and oilseed crops, enhancing field stability under drought-prone conditions.

-

2026: BASF SE introduced an upgraded microbial-based biocontrol portfolio under its biologicals division, focusing on enhanced strain resilience and longer shelf-life formulations for biopesticide applications in high-value fruit and vegetable farming systems across Europe and Latin America.

-

2025: Corteva Agriscience launched new seed-applied microbial inoculant technologies integrated with its seed treatment portfolio, designed to improve early-stage root development and nitrogen fixation efficiency in corn and soybean cultivation across North America and Brazil.

-

2025: UPL Ltd. expanded its ProNutiva biologicals platform with new microbial biofertilizer and biostimulant solutions aimed at sustainable crop yield enhancement, strengthening adoption across Asia-Pacific smallholder farming systems and export-oriented horticulture markets.

Agricultural Microbial Market Key Players are:

-

Novonesis

-

Corteva Agriscience

-

Bayer AG

-

BASF SE

-

Syngenta Group

-

UPL Limited

-

FMC Corporation

-

Valent BioSciences LLC

-

Certis Biologicals

-

Koppert Biological Systems

-

Lallemand Plant Care

-

Bioceres Crop Solutions

-

Andermatt Group AG

-

Rizobacter

-

IPL Biologicals Limited

-

T. Stanes & Company Limited

-

Groundwork BioAg

-

BioWorks Inc.

-

BioConsortia Inc.

-

Symborg

Agricultural Microbial Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.84 Billion |

| Market Size by 2035 | USD 35.56 Billion |

| CAGR | CAGR of 15.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Function (Biofertilizers, Biopesticides, Plant Growth Promoters, Soil Amendments & Nutrient Solubilizers, Others) • By Formulation Type (Liquid Formulations, Dry Formulations (Powder/Granules), Seed Treatment Formulations, Others) • By Crop Type (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, Turf & Ornamentals, Others) • By Application Method (Seed Treatment, Soil Treatment, Foliar Spray, Post-Harvest Application, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novonesis, Corteva Agriscience, Bayer AG, BASF SE, Syngenta Group, UPL Limited, FMC Corporation, Valent BioSciences LLC, Certis Biologicals, Koppert Biological Systems, Lallemand Plant Care, Bioceres Crop Solutions, Andermatt Group AG, Rizobacter, IPL Biologicals Limited, T. Stanes & Company Limited, Groundwork BioAg, BioWorks Inc., BioConsortia Inc., Symborg. |

Frequently Asked Questions

The agricultural microbial market is expected to grow at a CAGR of 15.08% from 2026 to 2035.

The agricultural microbial market was valued at USD 8.84 Billion in 2025.

The primary growth drivers include expanding adoption of sustainable and regenerative agriculture practices, rising global demand for residue-free food production, and increasing government support through subsidies and organic farming initiatives.

Biopesticides is the fastest-growing pump type in the agricultural microbial market, with a CAGR of 15.74% from 2026 to 2035.

North America dominated the agricultural microbial market in 2025, accounting for approximately 41.23% of global revenues.

Get in Touch