Passive Fire Protection Market Report Scope & Overview

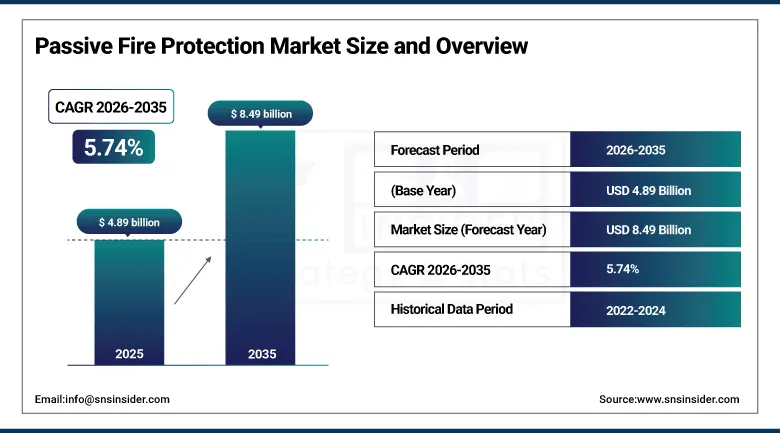

The Passive Fire Protection Market was valued at USD 4.89 Billion in 2025 and is expected to reach USD 8.49 Billion by 2035, growing at a CAGR of 5.74% from 2026 to 2035.

The passive fire protection (PFP) is one of the most important pillars in the area of fire safety engineering that encompasses a wide range of components designed to contain fire and smoke in the absence of any mechanical activation. In contrast to active fire protection methods such as sprinkler and other firefighting systems, the PFP includes designing a structure or an industrial complex through fire containment techniques and safeguarding structural strength by hindering the spread of the fire. Such systems incorporate numerous forms of fireproof paints, boards, and panels, fire stopping sealants and collars, and fire resistant glasses, among others. The international market of passive fire protection continues to thrive and grow steadily because of stricter building codes and urbanization.

Etex Group (Promat brand) supplies fire-resistant boards and passive protection systems used in 60 to 65% of high-rise steel structure fireproofing applications across Europe, reflecting its strong dominance in structural fire protection solutions. The company’s solutions are deployed in 80+ countries globally, with particularly high penetration in commercial high-rise construction, tunnels, and critical infrastructure projects.

Market Size and Forecast

-

Market Size in 2026E: USD 5.13 Billion

-

Market Size by 2035: USD 8.49 Billion

-

CAGR (2026–2035): 5.74%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Passive Fire Protection Market - Request Free Sample Report

Passive Fire Protection Market Trends

-

Stricter fire safety regulations are driving mandatory adoption of passive fire protection systems across construction and industrial projects.

-

Rising use of intumescent coatings is boosting demand due to high fire resistance and design flexibility.

-

Increasing retrofit activity in aging buildings is expanding demand for firestopping systems and fire-resistant boards.

-

Rapid urbanization and high-rise construction in Asia Pacific and MEA are accelerating market growth.

-

Growing oil & gas and infrastructure investments are sustaining demand for high-performance fireproofing solutions.

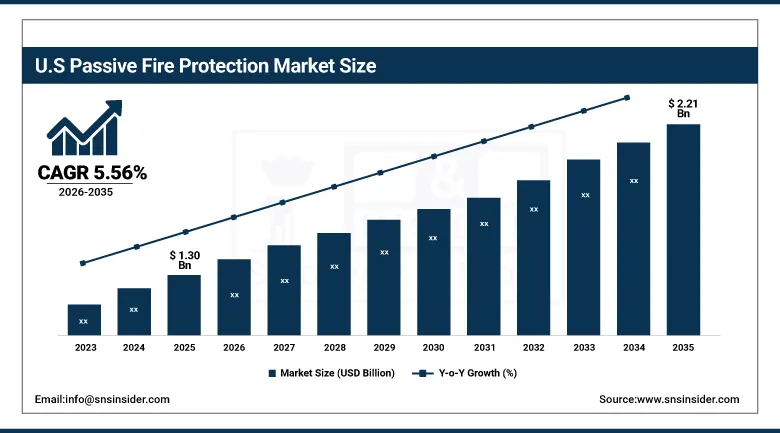

The U.S. Passive Fire Protection Market Outlook

The U.S. Passive Fire Protection market was valued at USD 1.30 Billion in 2025 and is projected to reach USD 2.21 Billion by 2035, growing at a CAGR of 5.56%.

North America's largest market for passive fire protection systems is that of the USA due to having some of the world's most developed laws relating to building and fire regulations, such as NFPA code, IBC code, and UL certification. The demand for passive fire protection systems arises from the growing trends in office building construction, data center construction, hospital construction, and plant construction. In addition to the construction activities, there is a rise in the number of retrofits being carried out in preexisting properties. With the rising preference for energy-efficient buildings and high-performance facades, the use of fire-resistant glass and mineral fiber panels has been on the rise.

In 2025, major U.S.-based passive fire protection contractors and manufacturers reported increased project activity related to commercial office retrofits and life-safety compliance upgrades across metro areas. Demand for intumescent sealants and firestopping collars was notably elevated in data center construction projects, reflecting growing investment in digital infrastructure and the associated fire compartmentation requirements for high-density cabling environments.

Passive Fire Protection Market Segment Analysis

-

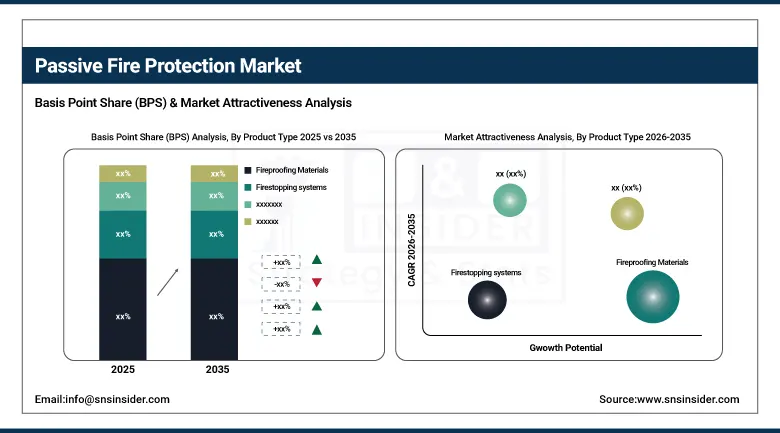

By Product Type, fireproofing materials dominated the market with a 34.12% share in 2025, while fire-resistant glass is the fastest-growing segment with the highest CAGR of 7.38% from 2026 to 2035.

-

By Installation Type, new construction dominated the market with a 60.29% share in 2025, while retrofit/renovation is the fastest-growing segment with the highest CAGR of 6.14% from 2026 to 2035.

-

By Application, commercial buildings dominated the market with a 30.11% share in 2025, while transportation is the fastest-growing segment with the highest CAGR of 6.76% from 2026 to 2035.

-

By End-Use Industry, construction & infrastructure dominated the market with a 34.24% share in 2025, while transportation & logistics is the fastest-growing segment with the highest CAGR of 7.51% from 2026 to 2035.

By Product Type, fireproofing materials dominate the passive fire protection market, while fire-resistant glass is the fastest-growing segment.

Fireproofing Materials segment dominated the market with the highest revenue share of 34.12% in 2025, driven by their extensive application across commercial buildings, oil and gas refineries, power generation facilities, and transportation infrastructure. Intumescent coatings articularly water-based and solvent-based epoxy formulations—have become the product of choice for protecting structural steel and concrete elements in high-value construction. Cementitious coatings remain preferred in industrial environments due to their durability and resistance to mechanical damage and chemical exposure. Continuous investment in fire code compliance programs and the ongoing demand for third-party certified fireproofing systems reinforce segment dominance across global markets.

Fire-resistant Glass segment is projected to grow at the fastest CAGR of 7.38% during 2026–2035, driven by its extensive application in contemporary commercial architecture, high rise buildings, and projects where fire resistance and transparency are both required. The increased deployment of fire resistant glass in escape routes, atriums, curtain walls, and partitions will fuel demand. The growing inclination towards fire-resistant products that provide an aesthetic appearance in high-end commercial and hospitality constructions will further boost the trend. Technological advancements by major players in terms of multi-layer glass and ceramics-based products are raising the benchmark of fire resistant glass.

By Installation Type, New Construction dominates the passive fire protection market, while Retrofit/Renovation is the fastest-growing segment.

New Construction segment dominated the market with the highest revenue share of 60.29% in 2025, due to constant growth in infrastructure development on a global basis, demand created through the process of urbanization for the construction of commercial as well as residential buildings and capital expenditures in industries such as oil and gas as well as power. The installation of passive fire protection systems during the design process in new construction ensures that the demand is high for fireproofing paints, fire boards, and firestopping systems.

Retrofit/Renovation segment is expected to register the fastest CAGR of 6.14% during 2026–2035 because aging commercial and industrial buildings in North America and Europe need improvements to conform with contemporary fire safety codes. Higher levels of awareness about the fire risks associated with such buildings, along with the stronger imposition of retrofit regulations by both local and national governments, are resulting in greater investments in fire stopping systems and improvements in passive fire protection. There has been an increasing trend toward renovating and adapting existing commercial real estate, with office buildings being repurposed for mixed-use and residential buildings.

By Application, Commercial Buildings dominate the passive fire protection market, while Transportation is the fastest-growing segment.

Commercial Buildings segment dominated the market with the highest revenue share of approximately 30.11% in 2025, fueled by active construction in office buildings, shopping centers, hotels, health centers, and educational establishments. Commercial buildings account for the major end-user industry of passive fire protection due to stringent occupancy and safety guidelines, complex structure of the building, and high initial costs invested in fire compartmentation. Increasing constructions of data centers across the globe will drive demand for the commercial sector, as fire protection in such centers is critical.

Transportation segment is projected to grow at the fastest CAGR of 6.76% during 2026–2035, with considerable investments being made in the transportation infrastructure worldwide by governments and the private sector. Increased construction of metro rail systems, upgrade of airport terminals, and rising number of ships built have created strong demand for fireproof boards, firestops, and intumescent coatings that are specifically designed to withstand vibrations and moisture. Increasingly strict standards for fire safety in transportation infrastructure such as the EN and IMO standards are forcing the implementation of certified passive fire protection solutions in various transport vehicles

By End-Use Industry, Construction & Infrastructure dominates the passive fire protection market, while Transportation & Logistics is the fastest-growing segment.

Construction & Infrastructure segment dominated the market with the highest revenue share of approximately 34.24% in 2025, indicating the extensive application of passive fire protection systems in construction projects around the world. The codes requiring compartmentation and fire resistance in buildings from all occupancies will ensure steady demand for passive fire protection products in this end-use sector. Increasing government spending on the development of public infrastructures, such as hospitals, educational institutions, airports, and transit stations, will further confirm the dominant position of the construction and infrastructure end use.

Transportation & Logistics segment is projected to grow at the fastest CAGR of 7.51% during 2026–2035, driven by the global development of freight and passenger transport networks, greater investments in railway infrastructure improvements, and the wider use of fire-resistant materials within logistics complexes and warehouses. The boom of online shopping across the globe is driving the expansion of logistics facilities that need fire resistance to be provided between racks for storage. Finally, more widespread use of electric vehicles and related charging equipment is offering new prospects for using passive fire protection in automotive logistics environments.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.54% |

|

Europe |

Germany |

28.67% |

|

Asia Pacific |

China |

38.45% |

|

Middle East & Africa |

UAE |

40.29% |

|

Latin America |

Brazil |

41.46% |

Asia Pacific Passive Fire Protection Market Insights

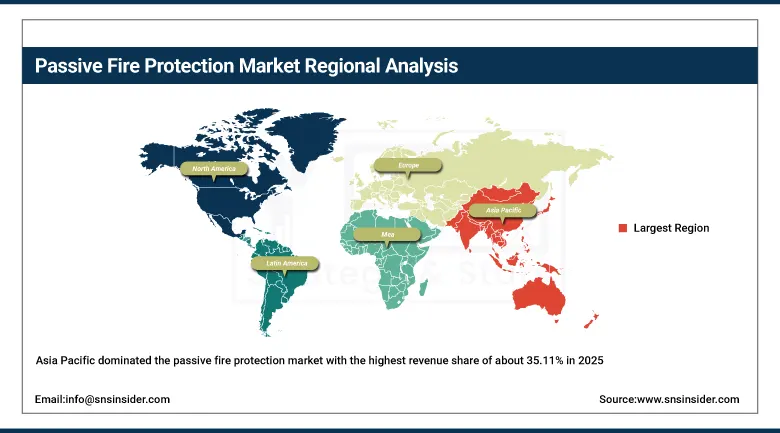

Asia Pacific dominated the passive fire protection market with the highest revenue share of about 35.11% in 2025 and it is also the fastest-growing regional market as projected to expand at a CAGR of 6.20% through 2035 from a 2025. The region is driven by rapid urbanization, large-scale infrastructure development programs, and progressively stringent fire safety codes across China, India, Japan, South Korea, and the ASEAN economies. China remains the dominant national market, underpinned by a massive construction pipeline including commercial towers, industrial parks, and infrastructure projects. India represents one of the fastest-growing national markets, driven by urbanization, commercial real estate expansion, and increasing awareness of fire safety compliance in industrial facilities.

Asia Pacific records the highest project adoption intensity globally, with passive fire protection systems integrated in 80–90% of new high-rise and infrastructure developments, driven by rapid urban expansion and strict fire safety enforcement. In China's Tier-1 cities, specification of certified intumescent coatings and fire-rated boards in commercial construction projects has risen significantly, reflecting enforcement of updated national fire safety standards.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Passive Fire Protection Market Insights

The North American region held a considerable share in the passive fire protection market during 2025 owing to the existence of an established legal structure, robust construction activities, and higher fire safety system compliance mandates, backed by an advanced and well-regulated construction industry, substantial investments in oil & gas infrastructure, and extensive deployment of certified fire protection assemblies. In the North American region, the United States is the primary demand driver, driven by strict fire code mandates by the National Fire Protection Association and International Building Code, which provide equal

requirements for intumescent coatings, fire stopping materials, and fire resistant panels in both commercial and industrial construction.

North America shows high regulatory penetration, with certified passive fire protection systems used in 75–85% of commercial and industrial construction projects, largely driven by NFPA and IBC compliance requirements.

Europe Passive Fire Protection Market Insights

Europe is one of the major regional markets for passive fire protection products that represent of global sales in 2025, and is known for its well-regulated construction sector driven by European fire regulations such as EN 1366 and EN 13501 series regulations. Europe shows high interest in using fire-resistant glass, firestopping products, and intumescent coatings, especially Germany, the UK, France, and Belgium-Netherlands. Building retrofit projects, driven by the need to comply with revised national fire codes, will ensure stable demand from renovations.

Europe demonstrates strong retrofit dominance, with 60–70% of demand coming from renovation and upgrading of aging buildings, particularly in commercial and public infrastructure assets. The U.K. post-Grenfell legislative response has significantly elevated attention to fire safety in residential high-rise buildings, generating substantial incremental demand for fire-rated cladding systems and firestopping assemblies across the building stock.

Middle East & Africa and Latin America Passive Fire Protection Market Insights

Middle East & Africa as well as Latin America are examples of relatively less yet increasing share markets within the overall global passive fire protection industry. The Middle East is experiencing huge demand on account of the rise in development activity in terms of building projects, particularly in Gulf Cooperation Council nations, such as UAE, Saudi Arabia, and Qatar. In these GCC countries, massive project initiatives, involving airports, stadiums, and urban development projects, necessitate the use of passive fire protection solutions. Africa, on the other hand, constitutes long-term potential because of urbanization and stringent fire regulations.

Middle East & Africa exhibit project-concentrated demand, with passive fire protection included in 80% of mega construction and oil & gas infrastructure projects, especially in GCC nations. Latin America reflects moderate but rising adoption levels, with fire protection systems deployed in 55% of new commercial construction projects, supported by gradual regulatory strengthening.

Market Dynamics:

Growth Drivers: Tightening fire safety regulations and rising construction activity globally

The market for passive fire protection is witnessing impressive growth due to increased fire regulations in all regions and global building activity in commercial, residential, industrial, and infrastructure markets. Regulatory organizations around the world are requiring strict standards in terms of fire compartmentalization, structural fire rating systems, and certification of passive fire protection systems by third parties. An increase in hazardous industries such as oil & gas, chemical processing, and power generation is providing stable demand for superior quality intumescent and cementitious materials for fireproofing applications where a structure failure in case of fire can be disastrous.

Restraints: High installation costs and a fragmented certification landscape

Given that the demand drivers for passive fire protection are solid, there are various challenges facing the market from the standpoint of certification and the costs associated with the installation of such products. Installation of passive fire protection systems necessitates careful execution by experienced installers, resulting in high costs and shortage of skills in countries where there are fewer installations. The certification process is highly fragmented, with national standards varying significantly within different regions of the world such as the United States, Europe, and Asia Pacific. Such diversity poses challenges for product marketers looking to introduce their products internationally due to the costs involved in gaining certification. This may affect the adoption rate especially in cost-constrained emerging markets.

Opportunities: Retrofitting demand and digital fire safety integration

The passive fire protection industry stands well-placed to gain from the increasing focus around the world on retrofits and enhancements to buildings’ safety to ensure compliance with the evolving fire standards and codes. In North America and Western Europe alone, there are billions of square feet of commercial buildings that need improvements with regard to passive fire protection systems to make sure that current standards are met, thereby forming a considerable market opportunity for passive fire protection companies. Another factor that is creating new opportunities for such players is the use of BIM and digital specification tools in construction projects.

Recent Developments

-

2025: Hilti Group expanded its firestopping portfolio across Asia Pacific and the Middle East with new intumescent pipe collars and cable firestop systems, strengthening its presence in rapidly growing commercial construction markets.

-

2025: 3M Company enhanced its Fire Barrier range with advanced intumescent sealants and flexible firestopping solutions, targeting rising retrofit and renovation demand across North America and Europe.

-

2026: Sika AG increased intumescent coating production capacity and expanded its passive fire protection business through strategic acquisitions to address growing regulatory-driven demand.

-

2026: Saint-Gobain S.A. introduced next-generation fire-resistant glass and glazing systems for high-rise and façade applications, supporting demand for integrated fire safety and energy-efficient building designs.

Passive Fire Protection Market Key Players

-

3M Company

-

Hilti Group

-

Sika AG

-

Etex Group

-

Rockwool International A/S

-

Morgan Advanced Materials plc

-

Hempel A/S

-

Jotun A/S

-

Akzo Nobel N.V.

-

PPG Industries Inc.

-

Sherwin-Williams Company

-

BASF SE

-

Saint-Gobain S.A.

-

Knauf Insulation

-

Promat International (Etex Group)

-

Rockwool A/S

Passive Fire Protection Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.89 Billion |

| Market Size by 2035 | USD 8.49 Billion |

| CAGR | CAGR of 5.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Fireproofing Materials (intumescent coatings, cementitious coatings), Fire-resistant Boards & Panels, Firestopping Systems (sealants, collars, wraps), Fire-resistant Glass, Others) • By Installation Type (New Construction, Retrofit / Renovation) • By Application (Commercial Buildings, Residential Buildings, Industrial Facilities, Oil & Gas / Petrochemical Plants, Transportation (Rail, Aviation, Marine)) • By End Use Industry (Construction & Infrastructure, Oil & Gas, Manufacturing, Power & Energy, Transportation & Logistics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M Company, Hilti Group, Sika AG, Hilti Corporation, Hilti (Fire Protection Division), Etex Group, Rockwool International A/S, Hilti Firestop Systems, Morgan Advanced Materials plc, Hempel A/S, Jotun A/S, Akzo Nobel N.V., PPG Industries Inc., Sherwin-Williams Company, BASF SE, Saint-Gobain S.A., Knauf Insulation, Promat International (Etex Group), Hilti Fire Protection Systems, Rockwool A/S |

Frequently Asked Questions

The Passive Fire Protection market is expected to grow at a CAGR of 5.74% from 2026 to 2035.

The passive fire protection market was valued at USD 4.89 Billion in 2025.

The primary growth drivers include stricter global fire safety regulations, rising construction activity across commercial and infrastructure projects, and increasing retrofit investments in aging buildings to meet updated fire code requirements.

Fire-resistant Glass is the fastest-growing product segment in the passive fire protection market, with a CAGR of 7.38% from 2026 to 2035, driven by growing adoption in modern high-rise commercial and residential architecture, where aesthetics and fire protection must be simultaneously achieved.

Asia Pacific dominated the passive fire protection market in 2025, accounting for 32.15% of global revenues, with the China representing a 38.45% of the regional market.

Get in Touch