AI in Networks Market Size & Overview:

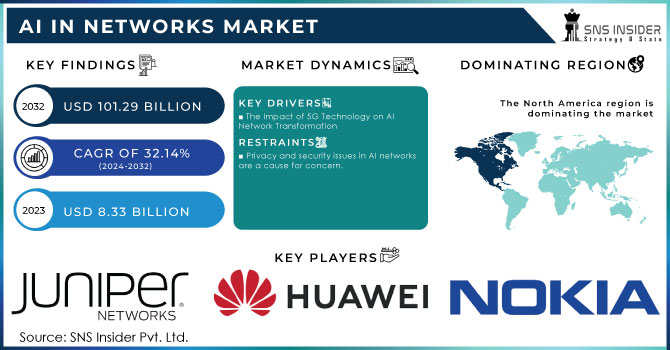

The AI in Networks Market Size was valued at USD 8.33 Billion in 2023 and is expected to reach USD 101.29 Billion by 2032, growing at a CAGR of 32.14% during 2024-2032. The AI in networks market is seeing a rapid rise fueled by the growing use of 5G tech, edge computing, IoT, connected devices, and the growth of smart cities. The growing use of 5G networks has resulted in a large volume of network data from high bandwidth activities like video streaming and online gaming, prompting network operators to incorporate AI solutions to handle data and allocate resources efficiently in order to decrease network congestion.

Get More Information on AI in Networks Market - Request Sample Report

In a world where "AI Everywhere" is prevalent, the importance of data security has surged due to organizations relying more on AI technology for managing networks effectively. AI networking is changing the way IT tasks are carried out by using artificial intelligence to enhance network performance and automate regular tasks, resulting in significant boosts in productivity. Gartner defines this innovative approach as utilizing AI to manage networks and implementing networks that can accommodate AI applications. The growing demands of AI are difficult for traditional network infrastructures to handle, underscoring the necessity for a complete redesign to guarantee security, efficiency, and scalability. Additionally, the rivalry between Ethernet and InfiniBand in data center AI networking demonstrates the changing dynamics of this industry, with analysts from Dell'Oro Group forecasting that Ethernet will gain more market share by 2027 despite InfiniBand's current advantage. The increasing use of AI in networking is directly related to the increasing need for more advanced solutions that improve automation, predictive analytics, and real-time threat detection. As companies face the difficulties presented by the rapid expansion of IoT devices and cloud services, incorporating AI technologies into their network management plans will be essential. This dynamic integration not only meets current operational needs but also prepares organizations to proactively address future challenges, guaranteeing a robust, high-performance network infrastructure that can efficiently support AI projects. Therefore, the AI in network market is at the point of change, ready to become a key aspect of secure and effective digital operations.

The incorporation of Artificial Intelligence (AI) in networking systems is changing the way businesses aim to improve customer-centricity and operational efficiency. Ruckus Networks and other companies are leading the way in providing solutions that meet the needs of a more scattered workforce and complex IT setups with the help of advanced technologies like Wi-Fi 7. India's networking infrastructure market has experienced significant growth, increasing to USD 5.09 billion in 2023 and expected to surpass USD 6 billion by 2028. This growing industry is driven by various sectors like IoT, finance, and telecommunications, all needing reliable, adaptable, and safe networks to manage large data transfers and ensure uninterrupted connectivity. Wi-Fi 7, which offers faster data rates, reduced latency, and improved interference handling, is expected to transform augmented reality, 8K streaming, and the growing IoT sector. The global market for Wi-Fi 7 is forecasted to reach USD 24.2 billion by 2030.Ruckus's creative strategy showcases how companies are changing to meet these requirements with a range of products for cloud management, network analytics, and easy integration with IoT devices. Their solutions not just make it easier to access secure and efficient networks, but also incorporate AI for instant network management and anomaly detection, thus addressing problems before they become service disruptions. As per industry evaluation, there has been an impressive 90% increase in vendor revenue for enterprise-class WLAN on a year-over-year basis, largely propelled by sectors like education, hospitality, and retail, highlighting the growing importance of sophisticated networking solutions. With the ongoing development of AI-driven technologies, the networking environment is becoming smarter, more flexible, and better able to adapt to the changing requirements of present-day businesses.

AI in Networks Market Dynamics

Drivers

-

The Impact of 5G Technology on AI Network Transformation

The quick implementation of 5G technology is transforming digital communication, opening up new growth opportunities in the AI in network market. The rising internet and mobile usage worldwide has led to a surge in the need for high-bandwidth applications like streaming services, online gaming, and IoT devices. Therefore, network providers are required to make significant investments in AI-based solutions that effectively handle and enhance network traffic. These solutions facilitate smooth traffic routing, efficient resource allocation, and strong network security measures, enabling operators to manage the challenges of high-speed data transmission effectively. With the advancement of 5G technology, the focus on cybersecurity solutions intensifies to address the rise in vulnerabilities due to the increased number of connected devices and data transmission. As a result, the importance of AI in networks increases significantly because AI can offer immediate threat detection, identification of abnormalities, and automated reactions to possible security issues. This change not only improves the overall security stance of networks but also guarantees that service providers can uphold the service quality that consumers anticipate with high-speed connections. Additionally, the interaction of 5G and AI is poised to develop novel possibilities like improved augmented reality experiences and self-driving systems that weren't possible before. The close connection between 5G and AI is fueling innovation in different industries, propelling the AI in networks market to unprecedented levels and solidifying its relevance in the future of telecommunications. As companies aim to take advantage of these advancements, the combination of 5G technology and AI-based network solutions is set to change how businesses function and interact with customers, leading to a more connected and streamlined digital environment.

Restraints

-

Privacy and security issues in AI networks are a cause for concern.

The incorporation of AI technology into network systems poses major challenges regarding data privacy and security. As AI-powered networks gather, save, and send large quantities of network traffic information, the risk of privacy violations increases, especially with the growing number of cyber threats. A recent study from the World Economic Forum indicates that 95% of cyber breaches are caused by mistakes made by individuals, underscoring the risks associated with managing confidential data. Utilizing AI in networks entails collecting data from different sources, such as user engagements and network functions, posing a heightened risk for unauthorized entry to confidential data. Network operators are confronted with difficulties in safeguarding the data gathered due to the increasing number of connected devices such as smartphones and smart home systems. A recent study conducted by the Pew Research Center discovered that 81% of Americans believe they lack any significant influence on the data that companies gather on them. Furthermore, the FTC disclosed 1,862 data breaches in the United States in just 2021, revealing more than 300 million records. These worries about privacy and security could impede the uptake of AI in network technologies and require a careful balance between innovation and privacy safeguards.

Segment Analysis of AI in Networks Market

by Deployment Mode

Based on Deployment Mode, Routers and Ethernet Switches captured the largest share revenue in AI in Network with 39.44% in 2023. This dominance is driven by the increasing demand for efficient data transmission and management in complex networking environments. Cisco Systems and Juniper Networks have unveiled innovative products to meet this requirement. An illustration is Cisco's recent release of the Catalyst 9000 series switches that utilize AI and machine learning to streamline network management, enhance security, and enhance performance. Similarly, the Mist AI platform by Juniper utilizes AI-generated data to streamline operations and improve user experiences across both wireless and wired networks. Arista Networks has demonstrated a significant focus on utilizing artificial intelligence algorithms for efficiently managing traffic through advanced routing solutions, highlighting its commitment to intelligent routing features. Furthermore, companies are enhancing their products by integrating edge computing characteristics, allowing routers and switches to process data closer to where it is generated, leading to reduced latency and improved efficiency. With the increasing utilization of AI technologies by businesses for enhanced efficiency and security, the AI network market is expected to experience a surge in demand for routers and Ethernet switches, leading to innovation and product advancement in this field.

by Deployment

by 2023, the AI in network market was primarily led by on-premises deployment, which claimed a significant revenue portion of 61.67%. The reason behind organizations' preference for on-premises solutions is their need for increased security, control, and compliance over their data. Top companies have been actively introducing new products designed specifically for on-site settings. One example is when Cisco introduced their SecureX platform, which combines AI-powered security capabilities to safeguard on-site networks against growing cyber risks. In the meantime, HPE launched the HPE Aruba Networking solution, which utilizes AI to enhance network efficiency and streamline management within on-site settings. NVIDIA has also made progress with its NVIDIA Spectrum X series switches, which aim to provide high performance and minimal latency for on-premises AI applications. Additionally, Fortinet introduced new security appliances powered by AI that improve the ability to detect and respond to threats in on-premises networks. These developments demonstrate the increasing popularity of companies focusing on on-premises solutions for improved data governance and reliability in AI-driven network operations, highlighting the ongoing significance of on-premises deployment in the AI in network market.

AI in Networks Market Regional Outlook

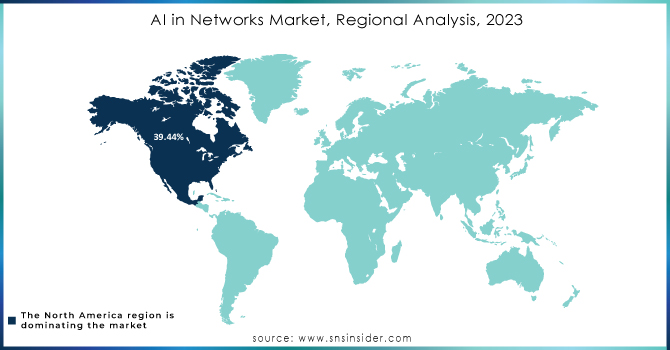

In the AI in network market, North America was the dominant player in 2023, accounting for 39.44% of the revenue share. The region's substantial market dominance is mainly due to its sophisticated technology infrastructure, widespread use of AI technologies, and strong emphasis on research and development. Prominent companies in the area have played a significant role in this expansion by introducing innovative new products. For instance, Cisco launched its AI Network Analytics tool, aimed at improving visibility and performance within enterprise networks through the use of machine learning algorithms to detect issues proactively. In the same way, Juniper Networks introduced its MIST AI platform that incorporates AI-generated insights for automating network management and enhancing user experiences. Arista Networks increased its product range with the introduction of new cloud-based solutions integrating AI to enhance data center networking and lower operational expenses. In addition, NVIDIA improved its AI capabilities with the introduction of NVIDIA BlueField data processing units (DPUs), which allow for better handling of network workloads in cloud settings. The product innovations, along with the growing demand for intelligent networking solutions, have strengthened North America's dominance in the AI in network market, establishing it as a significant influencer in shaping the future of network operations.

Asia Pacific became the top-growing region in the AI in network market in 2023, propelled by fast-paced digital transformation efforts and rising investments in cutting-edge technologies. Nations like China, India, and Japan have been leading the way in implementing AI solutions to improve their networking functions. Huawei's AI Fabric, a notable product launch in the region, utilizes AI for network automation to enhance performance and resource allocation for businesses. Furthermore, ZTE Corporation unveiled its AI-Powered Intelligent Network Management system, which aims to enhance network operations with predictive analytics and real-time monitoring. NTT Data's AI-driven Network Security Solution was also a major advancement in response to cybersecurity worries in our highly connected world. In addition, NEC Corporation introduced its NEC SD-WAN solution with integrated AI for managing traffic dynamically to meet the growing need for secure and dependable network services. These advancements show the area's dedication to utilizing AI technologies for effective network management and operations, establishing Asia Pacific as an important player in the worldwide AI in network market scene. Governmental assistance in adopting technology, along with a growing start-up community, continues to drive the rapid growth.

Need any customization research on AI in network market - Enquiry Now

Key Players

Some of the Major Key Players in AI in Network Market provide their product and offering:

-

Cisco Systems, Inc. (Cisco AI Network Analytics)

-

Juniper Networks, Inc. (Mist AI for Wireless Networking)

-

Huawei Technologies Co., Ltd. (AI Fabric)

-

Nokia Corporation (Nokia AI for 5G Networks)

-

Arista Networks, Inc. (CloudVision AI)

-

Extreme Networks, Inc. (ExtremeCloud AI)

-

IBM Corporation (IBM Watson for Network Management)

-

VMware, Inc. (VMware AI-Driven Networking)

-

Hewlett Packard Enterprise (HPE) (HPE AI Ops for Networking)

-

NetApp, Inc. (NetApp AI-Driven Data Management)

-

Ciena Corporation (Ciena's AI-Driven Adaptive Network)

-

Ericsson AB (Ericsson AI Solutions for Network Automation)

-

Fortinet, Inc. (FortiAI for Threat Detection)

-

Palo Alto Networks, Inc. (Cortex AI for Network Security)

-

NEC Corporation (NEC AI-Powered Intelligent Network Management)

-

Others

Recent Development

-

In September 2024, Telefonaktiebolaget LM Ericsson partnered with T‑Mobile USA, Inc. and NVIDIA Corporation to establish a shared AI-RAN Innovation Center. The AI-RAN Innovation Center aims to drive the standardization and broad adoption of AI-RAN technologies throughout the industry. The focus of the center would be on enhancing network performance, reliability, and efficiency.

-

September 2024 saw the unveiling of Nokia's Event-Driven Automation (EDA) platform, a major AI innovation. Utilizing Kubernetes, this cutting-edge platform revolutionizes the management of data center networks by providing a reliable, streamlined, and adaptable solution for overseeing network operations. Nokia EDA aims to reduce human mistakes in network operations, minimizing interruptions and downtimes for applications, while also decreasing operational efforts by as much as 40%.

-

In June 2024, Cisco Systems Inc. partnered with NVIDIA Corporation to introduce Nexus HyperFabric AI Clusters, a specialized Data Center Infrastructure Solution designed for Generative AI. The resolution combines the technological advancements of Cisco Systems Inc. and NVIDIA Corporation to simplify the deployment of generative AI apps. It guarantees complete visibility and analysis of IT across the entire AI infrastructure stack.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 8.33 Billion |

| Market Size by 2032 | USD 101.29 Billion |

| CAGR | CAGR of 32.14% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Offering (Routers and Ethernet Switches,Software ,AI-Networking Platform,Services) • By Technology(Generative AI ,Machine Learning ,Deep Learning ,Natural Language Processing (NLP),Other technologies) • By Deployment Mode (On-premises ,Cloud-based) • By Network Function(Network Optimization , Network Cybersecurity ,Network Predictive Maintenance ,Network Troubleshooting , Others) • By End-Use Industry(Telecom Service Providers ,Enterprises ,Data Centers , Government ,Other End-use industry) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems, Inc., Juniper Networks, Inc., Huawei Technologies Co., Ltd., Nokia Corporation, Arista Networks, Inc., Extreme Networks, Inc., IBM Corporation, VMware, Inc., Hewlett Packard Enterprise (HPE), NetApp, Inc., Ciena Corporation, Ericsson AB, Fortinet, Inc., Palo Alto Networks, Inc., NEC Corporation & Others |

| Key Drivers | • The Impact of 5G Technology on AI Network Transformation |

| Restraints | • Privacy and security issues in AI networks are a cause for concern. |

Frequently Asked Questions

Ans: The Routers and Ethernet Switches segment dominated the AI in Network Market.

AI enhances network security by detecting and mitigating threats in real-time, analyzing patterns of suspicious behavior, and automating responses to potential security breaches. This proactive approach reduces downtime and increases network resilience.

Telecommunications, cloud computing, data centers, and enterprise IT are leading adopters of AI in network solutions. These industries benefit from AI-driven automation, improved security, and better resource allocation for enhanced performance.

Ans: The AI in Network Market grow at a CAGR of 32.14% over the forecast period of 2024-2032.

Ans: The AI in Networks Market was valued at USD 8.33 Billion in 2023 and is expected to reach USD 101.29 Billion by 2032

Get in Touch