Aircraft Health Monitoring Market Report Scope & Overview:

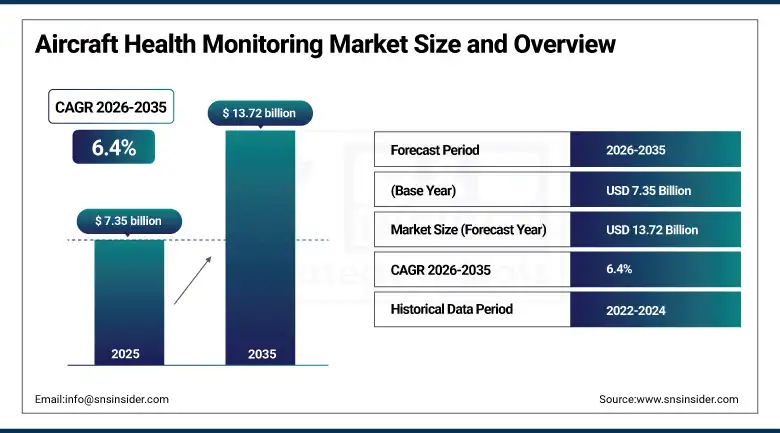

The Aircraft Health Monitoring Market was valued at USD 7.35 Billion in 2025 and is expected to reach USD 13.72 Billion by 2035, growing at a CAGR of 6.4% from 2026–2035.

The global aircraft health monitoring market’s commercial momentum is driven by the compounding economic pressure on airlines to reduce the USD 50 billion annual cost of aircraft maintenance and the USD 8 billion annual cost of unplanned downtime through predictive capabilities that AHMS delivers, the FAA and EASA regulatory environment’s progressive strengthening of requirements for continuous airworthiness monitoring, and the competitive differentiation that OEMs including Airbus and Boeing derive from bundling AHMS data services with new aircraft deliveries through their Skywise and AnalytX platforms. Honeywell’s Forge platform currently processes real-time health data from over 10,000 commercial aircraft globally, while AI-powered AHMS platforms across the industry are achieving 85% fault prediction accuracy that translates directly into maintenance cost reduction and operational reliability improvement for airline customers.

In April 2024, Global Crossing Airlines implemented Airbus’ Skywise Health Monitoring digital solution to support its expanding charter operations across the U.S., Caribbean, Europe, and Latin America, demonstrating the growing adoption of cloud-based AHMS platforms by mid-size and charter carriers seeking the predictive maintenance intelligence that was previously accessible only to major network airlines with the scale to justify proprietary AHMS infrastructure investment.

Market Size and Forecast

-

Market Size in 2026E: USD 7.82 Billion

-

Market Size by 2035: USD 13.72 Billion

-

CAGR: 6.4% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Aircraft Health Monitoring Market - Request Free Sample Report

Aircraft Health Monitoring Market Trends

-

Rising integration of AI and deep neural network architectures in AHMS platforms is improving fault prediction accuracy to 85% or above, enabling maintenance teams to intervene weeks ahead of component failure events.

-

Growing adoption of cloud-based AHMS data platforms including Honeywell Forge, Airbus Skywise, and Boeing AnalytX is shifting the market from hardware-centric to software-as-a-service subscription models with recurring analytics revenue.

-

Expanding deployment of MEMS sensor technology is reducing hardware cost per monitoring point, enabling broader parameter coverage across aircraft systems at economics that justify AHMS installation across mid-size regional jet fleets.

-

Increasing OEM integration of AHMS as standard line-fit equipment in new aircraft programmes is creating growing installed base that drives long-term data services revenue for manufacturers beyond the initial hardware transaction.

-

Rising demand for AHMS in UAV and advanced air mobility platforms is creating a new high-growth application segment as regulators require continuous airworthiness monitoring for commercial drone and eVTOL operations.

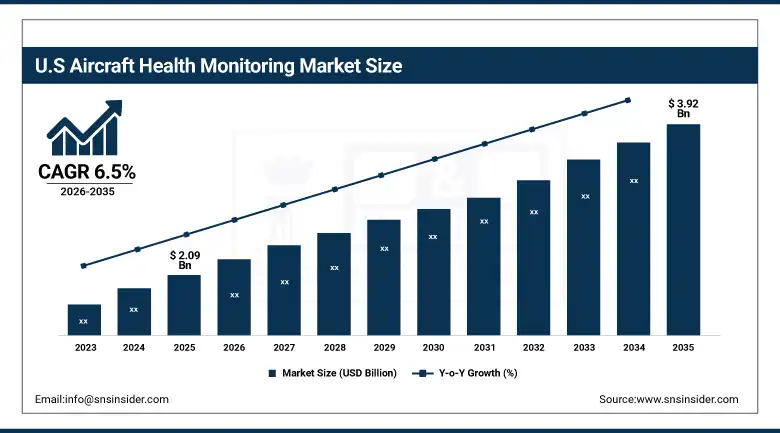

The U.S. Aircraft Health Monitoring Market Outlook

The U.S. Aircraft Health Monitoring Market was valued at approximately USD 2.09 Billion in 2025 and is expected to reach approximately USD 3.92 Billion by 2035, growing at a CAGR of approximately 6.5%.

Demand in the U.S. market is driven by the country’s position as the world’s largest commercial aviation market, whose combination of the largest active commercial fleet exceeding 7,200 aircraft operated by the major network and regional carriers, the most stringent FAA airworthiness continuous monitoring requirements, and the headquarters concentration of the world’s leading AHMS technology providers creates the highest-value and most commercially competitive national AHMS market globally. The U.S. market’s commercial sophistication is exemplified by Honeywell’s Forge platform whose 10,000-plus aircraft data subscription base generates the recurring analytics revenue that is shifting the market’s business model from hardware transaction to SaaS relationship.

Aircraft Health Monitoring Market Segment Analysis

-

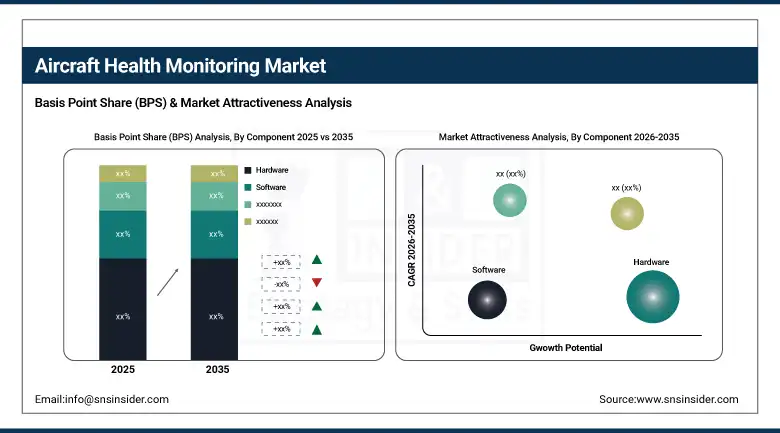

By Component, hardware dominated with approximately 47.95% share in 2025 through sensors, data acquisition units, avionics, and flight data management systems that constitute the essential monitoring infrastructure across every AHMS installation. Software is the fastest-growing component at a CAGR of 8.18%.

-

By Fit, line-fit configurations accounted for approximately 61.88% of market revenues in 2025, favoured by OEMs and airlines for their factory-level integration advantages including weight-neutral sensor placement, reduced certification complexity, and lower lifecycle cost relative to post-delivery retrofit installations. Retrofit is the fastest-growing fit segment at a CAGR of 7.63%.

-

By End User, airlines held approximately 53.68% of market share in 2025 as the primary AHMS investment decision-makers whose operational efficiency, maintenance cost reduction, and on-time performance imperatives define the commercial demand base for monitoring platforms. MRO providers are the fastest-growing end user at a CAGR of 7.31%.

-

By Subsystem, aero-propulsion dominated with approximately 41.85% revenue share in 2025 through engines’ status as the highest-value, highest-risk, and most data-intensive aircraft component whose continuous health monitoring delivers the most commercially significant maintenance cost avoidance and safety assurance outcomes. Avionics is the fastest-growing subsystem.

-

By Aircraft Type, fixed-wing platforms held approximately 56.65% share in 2025 through their dominance of commercial and military aviation fleets generating the majority of aggregate AHMS procurement. UAVs and advanced air mobility platforms are the fastest-growing aircraft type at a CAGR exceeding 10%.

By Component, hardware dominates, software grows fastest

Hardware retained the dominant component position with approximately 47.95% of the aircraft health monitoring market in 2025, reflecting the essential physical monitoring infrastructure that every AHMS installation requires to capture the sensor data streams from which diagnostic and prognostic analytics derive their operational value. The hardware segment encompasses MEMS accelerometers monitoring structural vibration and fatigue cycles, pressure and temperature sensors tracking engine and hydraulic system performance, data acquisition units processing multi-channel sensor inputs for transmission to onboard and ground-based analytics systems, and avionics computing hardware executing onboard diagnostic algorithms in real time during flight operations. Hardware’s market dominance reflects the capital intensity of initial AHMS installation across the global commercial and military fleet, where sensor retrofitting, data acquisition unit integration, and communication infrastructure installation constitute the largest single expenditure in an AHMS programme lifecycle. The hardware segment’s commercial scale is sustained by the continuous expansion of sensor coverage as technology advances enable monitoring of previously inaccessible aircraft systems and as regulatory requirements mandate new monitoring parameters that earlier AHMS installations did not capture.

Software is the fastest-growing component at a CAGR of 8.18% through 2035, propelled by the aviation industry’s progressive transition from hardware-centric periodic maintenance to continuous AI-powered predictive analytics whose commercial value is delivered through software platforms rather than the sensor infrastructure that generates the raw data these platforms analyse. The software segment’s growth is driven by the OEM and avionics major investment in cloud-based analytics platforms whose AI prognostic engines are achieving breakthrough fault prediction performance: Boeing’s AnalytX AI predictive maintenance platform launched in Q2 2024, Airbus’s Skywise Health Monitoring whose Palantir analytics integration announced in Q1 2024 deepened the platform’s predictive capability, and Honeywell’s Forge whose 10,000-aircraft subscriber base generates the data scale that continuously improves its machine learning models’ fault prediction accuracy. The software segment’s SaaS subscription model creates recurring revenue streams whose long-term financial characteristics are substantially superior to the hardware replacement cycle economics that previously defined the AHMS industry’s commercial model.

By Fit, line-fit dominates, retrofit grows fastest

Line-fit configurations retained the dominant fit position with approximately 61.88% of the aircraft health monitoring market in 2025, a commercial dominance grounded in the genuine technical and economic advantages that factory-level sensor integration provides over post-delivery retrofit installation across every dimension of AHMS programme lifecycle cost. Line-fit installation enables sensor placement at structurally optimal monitoring locations that post-delivery access restrictions prevent in retrofit scenarios, eliminates the wiring and structural modification certification costs that retrofit installation incurs, and allows data acquisition unit integration within aircraft systems architecture at the point where weight and power allocation is most efficiently managed. OEM preference for line-fit AHMS as a standard configuration in new aircraft programmes reflects both the technical quality advantages and the commercial opportunity that bundled AHMS data services represent as a recurring revenue source that transforms the OEM-airline relationship from a transactional aircraft delivery into a long-term data services partnership.

Retrofit is the fastest-growing fit segment at a CAGR of 7.63% through 2035, driven by the commercial opportunity presented by the global commercial aviation fleet’s large population of 15-plus-year aircraft whose original avionics and monitoring systems predate modern AHMS capability and whose continued service life extension creates strong airline motivation to invest in monitoring upgrades that reduce the maintenance cost and reliability risk of ageing airframe and powerplant components. The retrofit market’s commercial expansion has been significantly enabled by wireless sensor technology whose elimination of the wiring installation effort that deterred earlier retrofit programmes makes partial monitoring system upgrades economically viable at unit installation costs that airline capital budgets can accommodate within standard maintenance event windows without requiring the extended aircraft out-of-service periods that wired retrofit installation previously imposed on operators.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

26.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Aircraft Health Monitoring Market Insights

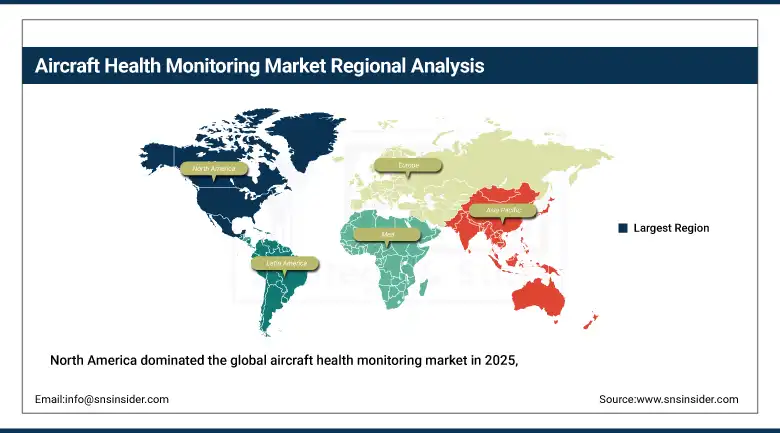

North America dominated the global aircraft health monitoring market in 2025, holding approximately 40% of global revenues, with the United States accounting for approximately 82.5% of North American revenues. The region’s leadership is anchored by the world’s highest concentration of commercial aircraft operators whose large fleets and intensive utilisation rates generate the greatest aggregate demand for AHMS investment, the FAA regulatory framework’s rigorous airworthiness monitoring requirements, and the headquarters locations of the market’s leading technology providers including Honeywell, Boeing, GE Aerospace, RTX Corporation, Curtiss-Wright, and Teledyne Technologies whose R&D investment and enterprise customer relationships collectively define global AHMS technology standards. Honeywell’s Forge platform, Boeing’s AnalytX, and the growing ecosystem of third-party AHMS software providers whose analytics platforms integrate with airline maintenance information systems collectively represent the most commercially advanced and technically sophisticated AHMS deployment environment of any national market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Canada contributes approximately 17.5% of North American revenues through its commercial aviation sector’s AHMS adoption, Bombardier’s regional aircraft product lines whose business jet and regional airliner programmes incorporate health monitoring as standard configuration, and FLYHT Aerospace Solutions’ position as a Canadian-headquartered specialist AHMS provider whose AFIRS real-time aircraft data streaming technology serves both commercial and government aviation customers with monitoring capabilities suited to the remote and northern corridor operations that characterise a significant proportion of Canadian aviation activity.

Europe Aircraft Health Monitoring Market Insights

Europe is the world’s second-largest aircraft health monitoring market, holding approximately 29% of global revenues, driven by Airbus’s dominant position as both the region’s leading commercial aircraft OEM and the operator of the Skywise Health Monitoring platform whose growing airline subscriber base is the most commercially significant European AHMS deployment. Germany accounts for approximately 26.4% of European revenues as the region’s largest national market, driven by Lufthansa Technik’s position as the world’s leading independent aircraft MRO provider whose AHMS data integration capabilities define the most advanced MRO operator use case for predictive maintenance analytics, the German defence aviation sector’s IVHM programme investment, and the engineering and manufacturing capabilities of German aerospace suppliers including MTU Aero Engines whose engine health monitoring expertise serves both OEM and aftermarket customer segments.

The United Kingdom, France, and the Netherlands are significant secondary European AHMS markets where Rolls-Royce’s engine health monitoring service infrastructure for its TotalCare power-by-the-hour contracts, Safran Electronics & Defense’s AHMS product portfolio, and the pan-European airline operators including Ryanair, IAG, and Air France-KLM whose large fleet monitoring programmes represent major AHMS procurement relationships collectively sustain commercially active AHMS development and deployment. The European Union Aviation Safety Agency’s progressive strengthening of continuous airworthiness monitoring requirements under its Part-M and Part-CAMO regulatory frameworks is creating a compliance-driven demand floor that ensures sustained AHMS investment across European commercial operator fleets regardless of economic cycle variation.

Asia Pacific Aircraft Health Monitoring Market Insights

Asia Pacific is the fastest-growing regional aircraft health monitoring market, driven by the extraordinary pace of commercial aviation fleet expansion across China, India, Southeast Asia, Japan, and South Korea whose combined new aircraft delivery pipeline represents the world’s largest regional aviation growth opportunity and consequently the most commercially significant regional AHMS demand growth pool. China accounts for approximately 44.8% of Asia Pacific revenues through its combination of the world’s largest single-country commercial aviation growth market, a domestic AHMS technology development programme supported by COMAC’s C919 aircraft programme that incorporates indigenous health monitoring architecture, and the AHMS procurement of major Chinese carriers including Air China, China Eastern, and China Southern whose combined fleet sizes create large-scale monitoring data service contract opportunities. By 2038, Asia Pacific is expected to account for the largest share of global aircraft deliveries of any region, making its AHMS market’s long-term growth potential proportional to the largest sustained commercial aviation infrastructure investment programme in aviation history.

India represents the most commercially significant emerging market within Asia Pacific for AHMS, as IndiGo’s rapid fleet expansion to over 500 aircraft, Air India’s ambitious modernisation programme, and the Indian government’s UDAN regional connectivity scheme creating hundreds of new route opportunities across underserved markets collectively generate a pace of fleet growth and operational complexity increase that is creating strong demand for the predictive maintenance efficiency and operational reliability improvement that AHMS delivers. India’s Directorate General of Civil Aviation announced eight new stringent safety measures in February 2026 following a period of elevated aviation safety focus, directly strengthening the regulatory motivation for AHMS adoption across the Indian aviation sector whose safety compliance investment is creating new commercial demand.

MEA & Latin America Aircraft Health Monitoring Market Insights

The Middle East and Africa and Latin America are growing aircraft health monitoring markets where expanding commercial aviation networks, fleet modernisation programmes, and the entry of major OEM AHMS platforms through new aircraft deliveries are progressively raising the installed base of monitored aircraft across regions whose historically lower AHMS adoption rates relative to North America and Europe are narrowing as fleet technology standardises around new-generation aircraft with monitoring capability as standard equipment. UAE leads MEA revenues at approximately 38.4% of the regional total through Emirates’ extraordinary fleet scale as the world’s largest wide-body operator, Etihad Airways’ predictive maintenance programme investment, and the concentration in Dubai of global aviation maintenance and engineering expertise that makes the UAE the most technically advanced AHMS deployment market in the Middle East.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through Embraer’s AHMS integration in its E-Jet and E2 programmes, the Brazilian carrier ecosystem’s AHMS adoption, and LATAM Airlines Group’s large combined fleet whose monitoring programme represents the most significant Latin American AHMS procurement relationship. Mexico and Colombia are growing secondary markets whose expanding aviation sectors and Aeromexico’s and Avianca’s fleet renewal programmes incorporating new-generation monitored aircraft are progressively expanding the Latin American AHMS installed base.

Market Dynamics

Growth Drivers: Aviation safety regulatory strengthening, airline predictive maintenance ROI from AHMS-driven downtime reduction, and OEM digital services strategy driving platform adoption across new and in-service fleets

The primary structural growth drivers for the aircraft health monitoring market are the progressive strengthening of aviation safety regulations requiring continuous airworthiness monitoring documentation and the compelling financial return on investment that airlines achieve through AHMS-enabled predictive maintenance, whose demonstrated ability to reduce unplanned aircraft-on-ground events by identifying developing faults weeks before failure generates maintenance cost savings and operational reliability improvements whose value substantially exceeds AHMS programme investment. The commercial aviation industry’s USD 50 billion annual maintenance cost and USD 8 billion unplanned downtime cost together define the addressable value reduction opportunity that AHMS targets, and airline CFOs’ growing ability to quantify AHMS ROI through data from early adopting carriers is accelerating investment decisions among the fleet operators who have not yet deployed comprehensive monitoring programmes. OEM digital services strategy is simultaneously expanding AHMS adoption by embedding monitoring infrastructure in new aircraft deliveries and packaging analytics platform subscriptions within power-by-the-hour, flight-hour, and total care service contracts that create recurring revenue relationships aligned with airline operational economics.

Restraints: High implementation cost for comprehensive retrofit programmes, data interoperability complexity across multi-vendor mixed fleets, and regulatory certification uncertainty for AI-enabled AHMS tools

The deployment of comprehensive AHMS across legacy aircraft fleets requires substantial capital investment in sensor retrofitting, data acquisition unit installation, communication infrastructure, and systems integration with airline maintenance information and enterprise resource planning systems whose complexity and cost create procurement barriers that are particularly significant for smaller regional carriers and low-cost operators whose capital budget priorities compete with mandatory safety compliance investments for limited available aircraft maintenance capital expenditure. Data interoperability across multi-vendor mixed fleets, where airlines operating a combination of Boeing and Airbus aircraft with avionics from multiple suppliers face significant AHMS data integration challenges whose resolution requires costly custom integration work, represents a commercial friction that delays comprehensive monitoring programme deployment and limits the cross-fleet analytics value that unified AHMS data platforms could theoretically deliver.

Opportunities: UAV and eVTOL AHMS regulatory mandate creating new application segment, AI diagnostic accuracy improvement expanding predictive maintenance ROI, and Asia Pacific fleet expansion representing the decade’s largest AHMS installed base growth opportunity

The UAV and advanced air mobility sector’s progressive commercialisation under regulatory frameworks that are universally incorporating continuous airworthiness monitoring requirements for commercial operations represents the most structurally novel near-term AHMS market expansion, as the 50-plus startup participants in the eVTOL and commercial drone AHMS segment are developing monitoring architectures whose lightweight, power-efficient, and cost-optimised designs address the operational constraints of these platforms in ways that directly expand the AHMS technology portfolio beyond its historical optimisation for commercial fixed-wing aircraft. Asia Pacific’s position as the world’s largest aircraft delivery destination through 2038 represents the most commercially significant long-term AHMS market opportunity, as each new aircraft delivery incorporating line-fit AHMS hardware creates a multi-decade data services revenue stream and an entry point for the OEM’s predictive analytics platform subscription.

Recent Developments:

-

2024: Global Crossing Airlines implemented Airbus’ Skywise Health Monitoring digital solution in April 2024 to support its expanding charter airline operations across the U.S., Caribbean, Europe, and Latin America, demonstrating the growing adoption of cloud-based AHMS platforms by mid-size and charter carriers seeking the predictive maintenance intelligence that enables proactive maintenance scheduling across geographically dispersed operations without large internal data engineering teams.

-

2024: Honeywell unveiled its next-generation Forge Health Monitoring Suite for commercial aviation in Q2 2024, featuring enhanced real-time analytics capabilities, expanded connectivity options, and improved AI-powered prognostic algorithms that extend the platform’s fault prediction accuracy across a broader range of aircraft system parameters for its subscriber base of over 10,000 monitored commercial aircraft globally.

-

2024: Airbus announced a strategic partnership with Palantir Technologies in Q1 2024 to integrate Palantir’s advanced data analytics capabilities into the Skywise Health Monitoring platform, enabling airline subscribers to access deeper operational insights, more sophisticated fleet-wide fault pattern analysis, and enhanced predictive maintenance recommendations drawn from the largest commercial aviation health data repository assembled by any single OEM.

Aircraft Health Monitoring Market Key Players are:

-

Honeywell International Inc.

-

The Boeing Company (AnalytX)

-

Airbus SE (Skywise)

-

GE Aerospace (HealthAware)

-

RTX Corporation (Raytheon Technologies)

-

Safran S.A.

-

Rolls-Royce Holdings plc

-

Lufthansa Technik AG

-

Curtiss-Wright Corporation

-

Meggitt PLC (Parker Hannifin)

-

Teledyne Technologies Inc.

-

FLYHT Aerospace Solutions Ltd.

-

Collins Aerospace (RTX)

-

Acellent Technologies Inc.

-

Embraer S.A.

-

Tech Mahindra Limited

-

MTU Aero Engines AG

-

Liebherr-Aerospace

-

Crane Aerospace & Electronics

-

Ventura Aerospace Inc.

Aircraft Health Monitoring Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.35 Billion |

| Market Size by 2035 | USD 13.72 Billion |

| CAGR | CAGR of 6.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Fit (Line-Fit, Retrofit) • By Subsystem (Aero-Propulsion, Airframe, Avionics, Ancillary Systems, Others) • By Aircraft Type (Fixed-Wing, Rotary-Wing, UAV, Others) • By End User (Airlines, OEMs, MRO) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Honeywell International Inc., The Boeing Company (AnalytX), Airbus SE (Skywise), GE Aerospace (HealthAware), RTX Corporation (Raytheon Technologies), Safran S.A., Rolls-Royce Holdings plc, Lufthansa Technik AG, Curtiss-Wright Corporation, Meggitt PLC (Parker Hannifin), Teledyne Technologies Inc., FLYHT Aerospace Solutions Ltd., Collins Aerospace (RTX), Acellent Technologies Inc., Embraer S.A., Tech Mahindra Limited, MTU Aero Engines AG, Liebherr-Aerospace, Crane Aerospace & Electronics, Ventura Aerospace Inc. |

Frequently Asked Questions

North America dominated the Aircraft Health Monitoring Market in 2025, holding approximately 40% of global revenues, with the United States accounting for approximately 82.5% of North American revenues.

Hardware dominated with approximately 47.95% of revenues in 2025.

Progressive strengthening of aviation safety regulations requiring continuous airworthiness monitoring, the compelling financial ROI that airlines achieve through AHMS-enabled predictive maintenance reducing the USD 50 billion annual aircraft maintenance cost burden, and OEM digital services strategies embedding monitoring infrastructure in new aircraft and packaging analytics subscriptions within long-term service contracts.

The Aircraft Health Monitoring Market was valued at USD 7.35 Billion in 2025.

The Aircraft Health Monitoring Market is expected to grow at a CAGR of 6.4% from 2026 to 2035.

Get in Touch