Asthma Therapeutics Market Report Scope & Overview:

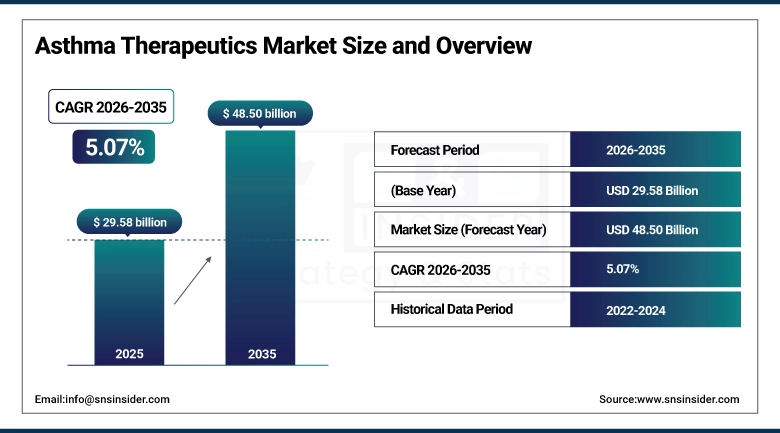

The Asthma Therapeutics Market was valued at USD 29.58 Billion in 2025 and is expected to reach USD 48.50 Billion by 2035, growing at a CAGR of 5.07% from 2026–2035.

Asthma remains one of the more stubbornly persistent chronic respiratory conditions worldwide, and the treatment landscape has been evolving in two directions at once. On one side, the fundamentals, inhaled corticosteroids, long-acting beta-agonists, and increasingly sophisticated inhaler devices, keep improving incrementally, extending the reach of well-established maintenance therapy. On the other, a genuinely new class of biologic treatments targeting specific inflammatory pathways, IgE, IL-4, IL-5, and IL-13 among them, has opened up meaningful options for the subset of patients whose disease simply doesn't respond well to conventional inhaled regimens. The World Health Organization estimated roughly 262 million people were living with asthma in 2019, with the disease responsible for more than 455,000 deaths globally, numbers that make clear this is a well-managed condition in aggregate but still one with real gaps in individual patient outcomes.

In February 2024, the Global Initiative for Asthma reported that fewer than 10% of asthma patients worldwide achieve optimal disease control, a finding that says a lot about where the real commercial and clinical opportunity in this market actually sits. That gap between available therapy and achieved control isn't primarily a supply problem, it reflects underdiagnosis, inconsistent adherence, and formulary access barriers that keep even effective treatments out of reach for a meaningful share of patients who could benefit from them.

Market Size and Forecast

-

Market Size in 2026E: USD 31.08 Billion

-

Market Size by 2035: USD 48.50 Billion

-

CAGR: 5.07% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Asthma Therapeutics Market - Request Free Sample Report

Asthma Therapeutics Market Trends

-

Biologic monoclonal antibody therapies, including anti-IL-5, anti-IgE, and anti-IL-4/IL-13 agents, are increasingly redefining treatment protocols for severe, refractory asthma that doesn't respond to conventional inhaled regimens.

-

Smart inhaler devices with Bluetooth connectivity, dose counters, and real-time adherence tracking are gaining adoption as healthcare systems place more weight on measurable patient compliance.

-

Fixed-dose combination inhalers delivering ICS/LABA and ICS/LABA/LAMA triple therapy are reducing pill burden while meaningfully improving lung function and cutting exacerbation rates.

-

Biomarker-driven prescribing is gaining ground, with fractional exhaled nitric oxide testing and blood eosinophil counts increasingly used to stratify patients and guide treatment selection.

-

Regulatory pressure toward hydrofluorocarbon-free, low-carbon propellant inhalers, particularly across Europe, is accelerating industry investment in next-generation, environmentally sustainable inhaler platforms.

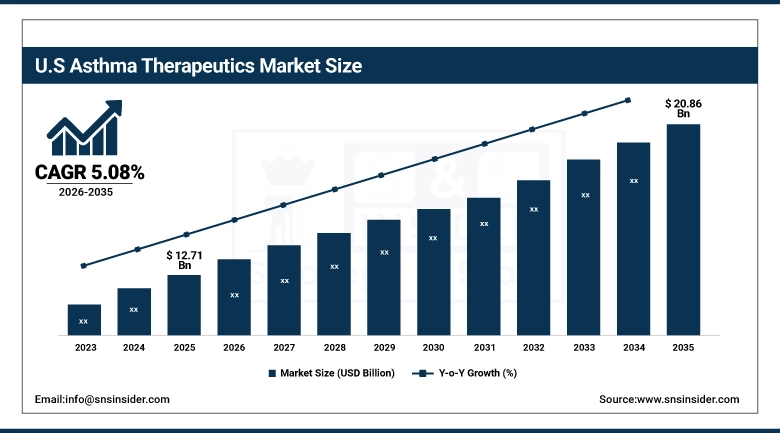

U.S. Asthma Therapeutics Market Outlook

The U.S. Asthma Therapeutics Market was valued at approximately USD 12.71 Billion in 2025 and is expected to reach approximately USD 20.86 Billion by 2035, growing at a CAGR of approximately 5.08%.

The United States leads the global asthma therapeutics market in national share, and a fair amount of that comes down to prevalence alone: adult asthma affects roughly 7.7% of the U.S. population, a genuinely large patient base by international standards. Layer on a well-developed reimbursement system across both private and public payers that supports coverage for branded biologics, along with strong formulary penetration for treatments including dupilumab, mepolizumab, benralizumab, and tezepelumab, and it's not hard to see why premium-priced biologic therapy has scaled so quickly across hospital, outpatient, and home care settings in the U.S. specifically.

In March 2025, AstraZeneca received expanded FDA approval for Fasenra as an add-on maintenance therapy for eosinophilic asthma patients aged 6 to 11, extending its biologic reach into the pediatric severe asthma segment. The approval reinforces AstraZeneca's leadership position in age-inclusive biologic treatment and reflects a broader industry trend toward pushing effective severe-asthma therapies down into younger patient populations that previously had fewer advanced treatment options available to them.

Asthma Therapeutics Market Segment Analysis

-

By Product, the Inhalers segment dominated the Asthma Therapeutics Market with a 72.14% revenue share in 2025, while the Nebulizers segment is expected to register steady growth driven by pediatric and elderly patient populations.

-

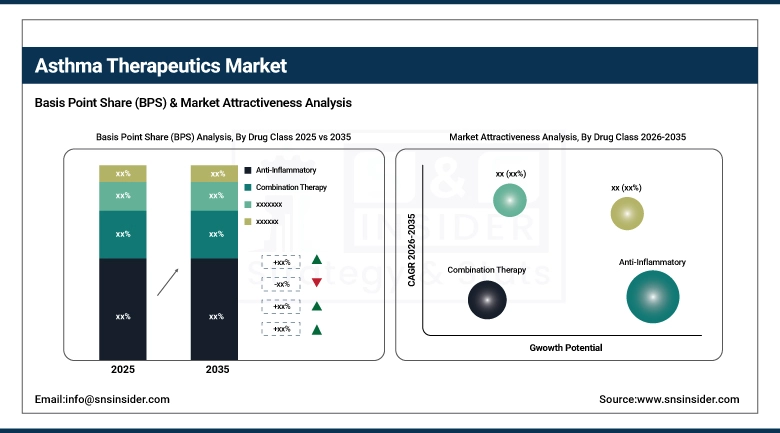

By Drug Class, the Anti-inflammatory segment dominated the Asthma Therapeutics Market with a 44.86% revenue share in 2025, while the Combination Therapy segment is the fastest growing with a CAGR of approximately 6.21%.

-

By Route of Administration, the Inhaled segment dominated the Asthma Therapeutics Market with a 68.43% revenue share in 2025, while the Oral segment is expected to expand with rising adoption of oral biologics and leukotriene receptor antagonists.

By Product, inhalers dominate, nebulizers grow steadily

Inhalers dominated the market with a share of 72.14%, making them the biggest type of product offered on the market due to the high clinical favorability of airway drug delivery and a well-defined set of treatment protocols that recommend using ICS-containing inhalers as the primary controller treatment. In terms of the inhaler product line, metered dose inhalers have the largest part of the device market because of the effectiveness, cost-efficiency, and widespread popularity among prescribing doctors, whereas dry powder inhalers are steadily growing due to environmentally-friendly formula without propellant.

The nebulizer market is one of the smallest participants in terms of revenue generation, however, the segment is projected to grow continuously due to the high utilization of the devices in hospitals and intensive care units for patients suffering from critical or nearly fatal asthma attacks. Soft mist inhalers also become increasingly popular within the device segment since such devices help elderly and pediatric patients to inhale the medication more easily than in case with conventional metered dose inhalers.

By Drug Class, anti-inflammatory agents dominate, combination therapy grows fastest

Anti-inflammatory agents, including inhaled corticosteroids such as fluticasone propionate, budesonide, and beclomethasone dipropionate, held 44.86% of drug-class revenue in 2025, the largest share of any category. Every major clinical guideline recommends these agents for long-term asthma management, and their broad acceptance across every severity level, combined with widely available and affordably priced generic ICS products, has kept this segment firmly in the lead.

Combination therapy is the fastest-growing drug class, at a projected CAGR of approximately 6.21%, as ICS/LABA and ICS/LABA/LAMA fixed-dose combinations gain traction on the strength of mounting clinical evidence supporting once-daily triple therapy for moderate-to-severe asthma. That evidence base, showing meaningful reductions in severe exacerbations, continues to push prescribers toward combination regimens over single-agent therapy for patients whose disease isn't well controlled on inhaled corticosteroids alone.

By Route of Administration, inhaled dominates, oral gains momentum

The inhaled route retained its dominant position with approximately 68.43% share in 2025, a reflection of near-universal clinical guideline support for inhaled delivery of both controller and reliever asthma medication. Direct deposition of drug into the airways offers faster onset of action and a more favorable systemic side effect profile than other administration routes, and continued improvement in inhaler device technology keeps enhancing the bioavailability of inhaled formulations further.

The oral route is gaining momentum, driven by increasing use of leukotriene receptor antagonists including montelukast, alongside rising use of systemic corticosteroids for acute severe exacerbations. The broader 'other' administration category is also expanding rapidly, propelled by growing use of injectable biologics, including anti-IL-5 monoclonal antibodies and subcutaneously administered anti-IgE therapies, that don't fit neatly into either the inhaled or oral categories but represent an increasingly important share of overall treatment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.0% |

|

Europe |

Germany |

24.0% |

|

Asia Pacific |

China |

37.0% |

|

Latin America |

Brazil |

36.0% |

|

Middle East & Africa |

Saudi Arabia |

26.0% |

North America Asthma Therapeutics Market Insights

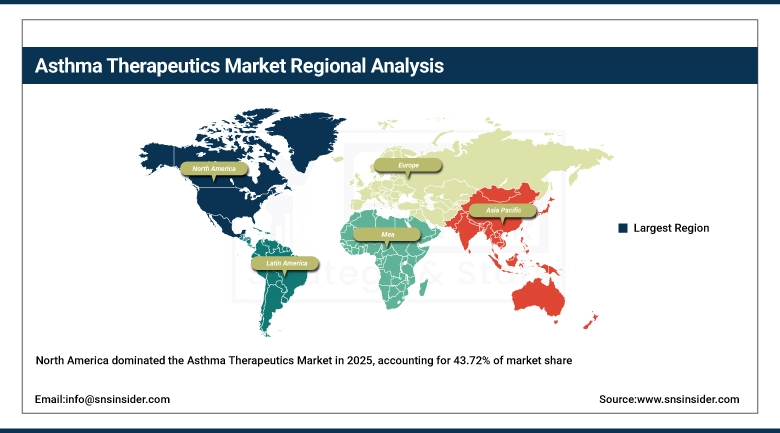

North America held 43.72% of regional revenue share in 2025, driven by high asthma prevalence rates in the United States, a substantial concentration of key pharmaceutical innovators, well-established specialist respiratory care systems, and solid national reimbursement coverage for high-value biologic therapies. Canada is adding meaningfully to regional market size as well, with its public drug program continuing to expand reimbursement indications for biologic asthma therapies.

The U.S. market specifically continues to benefit from expedited FDA approval processes, including Breakthrough Therapy designation for more severe asthma cases, while rising adoption of digital health monitoring solutions, including connected inhalers and telemedicine-based asthma management, continues to improve patient compliance and reduce preventable hospitalizations. That combination of regulatory speed, digital health integration, and strong reimbursement infrastructure keeps North America firmly in the market's leading position.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Asthma Therapeutics Market Insights

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 6.84% through the forecast period, driven by increasing asthma prevalence across the region's densely populated cities, rising purchasing power that's giving more residents access to medical care, and growing government investment in health programs. China, India, Japan, and South Korea represent the region's largest prescription markets, each following a somewhat different growth path.

China is increasingly incorporating advanced controller medications into its National Reimbursement Drug List, while India's strong generic pharmaceutical manufacturing base continues to enable affordable inhaler and bronchodilator access across rural and semi-urban patient populations. Japan and South Korea, meanwhile, are seeing rising demand for advanced inhaler technology and biologics tied to their growing elderly patient populations and the corresponding rise in elderly-onset severe asthma cases.

Europe Asthma Therapeutics Market Insights

Europe represents the world's second-largest asthma therapeutics market, supported by universal healthcare access across the continent's major economies, well-developed regulatory infrastructure through the European Medicines Agency, and growing physician adoption of GINA Step Up Therapy approaches that increasingly incorporate biologics for severe, uncontrolled asthma. The UK's NICE technology appraisal process has expanded label indications for mepolizumab, benralizumab, and dupilumab in asthma treatment specifically.

France, Germany, and Italy are each launching national asthma plans focused on specialist referral and biologic therapy screening, reflecting a coordinated regional push toward earlier identification of patients who could benefit from advanced treatment. Europe's broader drive toward carbon-neutral, HFC-free inhaler platforms is also fueling meaningful R&D investment in low-carbon metered dose inhaler propellants and dry powder devices, a trend that's distinctly more pronounced here than in other major regional markets.

MEA & Latin America Asthma Therapeutics Market Insights

The Latin American market and the Middle East and African market can be viewed as opportunity markets in terms of the asthma therapeutics market since there is an increase in levels of urban air pollution, increasing prevalence of allergy sensitization among the population and programs from the governments intended to upgrade respiratory surveillance and treatment facilities. In the case of Latin America, Brazil and Mexico can be identified as key players in the development of the brand inhaler market and adoption of biologics.

In the case of the Middle East and Africa, countries that are members of Gulf Cooperation Council are focusing on developing hospital formularies and national respiratory care guidelines. This is part of their efforts of upgrading chronic diseases management facilities. The availability of affordable generics and multilingual education programs for patients, along with healthcare partnerships between private and public sectors, have ensured that diagnosis of asthma becomes more common in these regions.

Market Dynamics

Growth Drivers: Rising global prevalence and persistent unmet treatment need sustain demand

The rising global incidence of asthma, driven by urbanization, deteriorating air quality, increasingly sedentary lifestyles, and greater exposure to occupational allergens, remains the primary driver behind this market's growth. With more than 339 million people estimated to be living with asthma worldwide as of 2025, the persistent gap between disease prevalence and optimal treatment control continues to represent a significant, largely unmet commercial and clinical opportunity for pharmaceutical companies and device manufacturers alike.

The CDC reports that asthma accounts for more than 1.6 million emergency department visits annually in the United States alone, a figure that underscores the continued need for better disease management systems capable of reducing acute exacerbations. Rising rates of asthma-COPD overlap syndrome are adding further demand as well, since this patient population requires dual-indication treatment regimens that combine elements of both respiratory disease management approaches, further expanding the addressable market for combination and biologic therapies.

Restraints: High biologic treatment costs and formulary access barriers constrain adoption

While the clinical effectiveness of next-generation biologic agents in asthma treatment has been well established, the cost of these therapies, ranging from USD 15,000 to more than USD 40,000 annually per patient in the United States, remains a significant obstacle to broader adoption, particularly in low- and middle-income economies where out-of-pocket healthcare spending represents a major determinant of overall access. These cost pressures are compounded by stringent prior authorization requirements and step therapy mandates common across many U.S. health insurance plans, which typically require documented failure of conventional ICS/LABA therapy before granting access to biologic agents.

The limited availability of biosimilars for many well-established biologic agents has similarly constrained access across emerging economies in Southeast Asia, Sub-Saharan Africa, and Latin America, a problem compounded by limited awareness among primary care physicians in these regions regarding advanced asthma phenotyping and biomarker-driven treatment selection. Together, these cost and access barriers continue to keep advanced biologic therapy concentrated among wealthier patient populations in developed healthcare markets.

Opportunities: Expanding biologic pipeline and upcoming biosimilar entry unlock high-value growth

The promising new pipeline of biologics directed at emerging asthma endotypes such as TSLP, IL-33, and prostaglandin D2 receptor pathways constitutes an unprecedented growth opportunity for originator pharmaceutical companies as well as specialty biologic manufacturers. The approval of tezepelumab as the first biologic that is efficacious against broad spectrum asthma phenotypes irrespective of the eosinophil level significantly broadened the patient base for biologics treatment and set a precedent which will be followed by future respiratory immunology biologics.

The upcoming launch of biosimilars of omalizumab, mepolizumab, and benralizumab during the period 2026 to 2030 will make access more democratic through reducing resistance from payers and increasing the addressable market by providing cost-effective treatment options for those patients who were previously priced out of treatment in North America, Europe, and Asia Pacific. In January 2025, the FDA has granted approval to two manufacturers' applications for biosimilar versions of Nucala with anticipated launches in mid-2025 and cost savings in annual treatment costs by 25 to 40%.

Recent Developments:

-

2024: In November 2024, GSK and Innoviva announced positive Phase IIb data for an investigational once-daily oral CRTH2 antagonist for mild-to-moderate asthma, signaling a strategic expansion beyond injectable biologics into convenient oral precision respiratory therapy.

-

2025: In January 2025, Sanofi and Regeneron reported that Dupixent global net sales exceeded USD 14.2 Billion across all approved indications in 2024, with the asthma indication representing one of the highest-growth contributory segments, supported by expanded pediatric approval and broadening payer coverage in Europe and Asia Pacific.

-

2025: In March 2025, AstraZeneca received expanded FDA approval for Fasenra as an add-on maintenance therapy for eosinophilic asthma patients aged 6 to 11, extending its biologic reach into the pediatric severe asthma segment.

Asthma Therapeutics Market Key Players

-

AstraZeneca PLC

-

GlaxoSmithKline plc (GSK)

-

Sanofi S.A.

-

Regeneron Pharmaceuticals, Inc.

-

Boehringer Ingelheim GmbH

-

Novartis AG

-

Teva Pharmaceutical Industries Ltd.

-

Merck & Co., Inc. (MSD)

-

Pfizer Inc.

-

Roche Holdings AG (Genentech)

-

Amgen Inc.

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Chiesi Farmaceutici S.p.A.

-

Cipla Limited

-

Sun Pharmaceutical Industries Ltd.

-

Almirall S.A.

-

Vectura Group plc

-

Glenmark Pharmaceuticals Ltd.

-

Hikma Pharmaceuticals PLC

-

Theravance Biopharma, Inc.

Asthma Therapeutics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 29.58 Billion |

| Market Size by 2035 | USD 48.50 Billion |

| CAGR | CAGR of 5.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Inhalers [Dry Powder, Metered Dose, Soft Mist], Nebulizers) • by Drug Class (Anti-inflammatory, Combination Therapy, Bronchodilators) • by Route of Administration (Inhaled, Oral, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AstraZeneca PLC, GlaxoSmithKline plc (GSK), Sanofi S.A., Regeneron Pharmaceuticals, Inc., Boehringer Ingelheim GmbH, Novartis AG, Teva Pharmaceutical Industries Ltd., Merck & Co., Inc. (MSD), Pfizer Inc., Roche Holdings AG (Genentech), Amgen Inc., Johnson & Johnson (Janssen Pharmaceuticals), Chiesi Farmaceutici S.p.A., Cipla Limited, Sun Pharmaceutical Industries Ltd., Almirall S.A., Vectura Group plc, Glenmark Pharmaceuticals Ltd., Hikma Pharmaceuticals PLC, Theravance Biopharma, Inc. |

Frequently Asked Questions

The Asthma Therapeutics Market was valued at USD 29.58 Billion in 2025.

North America dominated the Asthma Therapeutics Market in 2025 with a 43.72% market share, while Asia Pacific is the fastest-growing region.

Inhalers dominated with a 72.14% revenue share in 2025, driven by their clinical effectiveness and widespread adoption.

The rising global prevalence of asthma, combined with persistent gaps in optimal disease control and an expanding pipeline of biologic therapies.

The Asthma Therapeutics Market is expected to grow at a CAGR of 5.07% from 2026 to 2035.

Get in Touch