AUTOMOTIVE LIGHTWEIGHT MATERIAL MARKET SIZE:

To get more information on Automotive Lightweight Material Market - Request Free Sample Report

The Automotive Lightweight Material Market Size was valued at USD 82.68 Billion in 2023 and is expected to reach USD 128.02 Billion by 2032 and grow at a CAGR of 5.0% over the forecast period 2024-2032.

The Automotive Lightweight Materials Market is a rapidly evolving sector, driven by the growing need for fuel efficiency, sustainability, and compliance with stringent government regulations aimed at reducing emissions. Lightweight materials such as aluminum, high-strength steel, magnesium, plastics, and composites are pivotal in reducing vehicle weight, enhancing performance, and supporting environmental goals. The adoption of lightweight materials is particularly crucial in electric vehicles (EVs), where reduced weight translates to improved battery efficiency and longer driving ranges. Innovations in material technology, such as advanced composites and aluminum alloys that are 10-15% lighter than traditional materials, are shaping the market dynamics.

Europe is at the forefront of research and development in this field, contributing significantly to global R&D investments, which reached USD 1.35 trillion in 2023. This focus aligns with the automotive industry’s commitment to clean and green transportation technologies, highlighting the essential role of lightweight materials in achieving a sustainable future.

MARKET DYNAMICS

KEY DRIVERS:

-

Stricter Emissions Regulations Propel Adoption of Lightweight Materials in Automotive Manufacturing

Governments across the world are enforcing strict emission rules, which, in turn, compels manufacturers to use lightweight materials. These materials enable lighter vehicles, thereby increasing the fuel efficiency of the vehicles and reducing the carbon emissions as expected to meet standards like that of the EU's CO2 regulation.

Involving increased usage of stricter emissions regulations for the adoption of lightweight materials in the automobile industry is a response to an increase in the number of government mandates involving a reduction in carbon footprints. Setting very ambitious goals, the European Union (EU) has fixed the average emissions limit for new cars to 95 grams of CO2 per KM from 2023. This would entail reducing greenhouse gas emissions by about 55% by 2030 compared with their 2021 level. To achieve such a goal, in the United States, the EPA has set very ambitious goals by the year 2030 for the reduction of emissions from the light-duty vehicle segment by 40%. So far in this respect, these regulatory requirements incite manufacturers to plan more efficient vehicles for which lightweight materials are being considered as an alternative. For instance, it can be demonstrated through statistics that reducing the weight of a vehicle by 10% results in an improvement of 6-8% in the fuel efficiency of the vehicle. This will also target the objectives established by regulatory bodies.

-

Rising Consumer Demand for Fuel Efficiency Sparks Innovations in Lightweight Materials

The modern consumer is concerned first and foremost with gas efficiency in a new vehicle. It allows manufacturers to improve performance without ever diminishing fuel efficiency. Demand is accelerating and will attract investment in aluminium and advanced composites, among other materials.

The automotive lightweight materials market is growing remarkably due to the rising awareness of consumers about sustainability and fuel efficiency. According to the data of 2023, 70% of consumers believed that fuel economy was an important factor in the buying decision for a vehicle. In general, this shift towards more fuel-efficient vehicles will be extensively experienced among the younger generations, of whom 62% of the respondents from Gen Z said that sustainability would decide their choices. This demand is encouraging investors in the automobile sector to look into lightweight materials that will ensure better fuel efficiency with no compromise on performance. Because any weight loss has the potential to enhance fuel economy by as much as 6-8%, a lighter automobile with even a 10% weight reduction is becoming increasingly more attractive for aluminum and other advanced composites.

RESTRAIN:

-

High Production Costs Impede Adoption of Lightweight Automotive Materials

Light-weight solutions in the automotive material market have high production costs with carbon fiber and some composites. These materials are characterized by rather complicated technology, which results in the use of exclusive techniques and technologies, thereby pushing up the cost level. Manufacturers may therefore discourage the implementation of light solutions because they will count more toward cost issues than all those about other factors such as performance and durability. The high initial investment for material could limit the mass take-up of such materials in the industry.

The data also illustrates the involvement of several economic factors besides the largest expense of manufacturing lightweight automotive materials. Advanced materials like carbon fiber can cost between USD 20 and USD 40 per kilogram, whereas normal materials like steel can cost around USD 0.75 to USD 2 per kilogram in terms of average costs. The production facilities also require an investment that runs over a magnitude of USD 100 million; this is an added cost burden by such automotive manufacturers as they look forward to utilizing lightweight solutions. Such high costs will be a major turn-off to widespread adoption even with the environmental benefits thus the need for new manufacturing processes that reduce the cost burden.

KEY MARKET SEGMENTS

BY END USE

In 2023, The Passenger Cars segment represented a significant 68% of the automotive lightweight material market, this trend is mainly influenced by the fuel efficiency and environmental friendliness preferred by consumers. Studies show that a reduction in vehicle weight can boost fuel economy by 6-8% for every 10% reduction in weight. Answering this trend with innovative design solutions, the leading automotive companies have started to roll out new designs.

-

For instance, Ford launched its F-150 boasting high-strength aluminum alloys and BMW rolled out iSeries models made of carbon fiber composites. Such innovation is also crucial at a time when the industry is shifting towards lighter, more fuel-efficient vehicles.

The Light Commercial Vehicles segment is projected to grow at the fastest CAGR of 6.39% during the forecast period, driven by the acute need for fuel-efficient solutions. LCVs account for around 23% of the CO2 generated through road transport worldwide; thus, the lighter, the better becomes imperative to achieve the desired environmental relief. Lightweight materials such as advanced composites and aluminum can increase up to 15% in terms of fuel efficiency with substantial emission reductions.

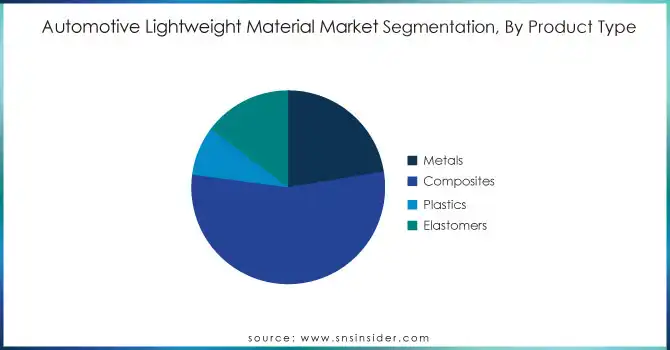

BY PRODUCT TYPE

The Composites segment dominated the automotive lightweight materials market in 2023, however, with a market share of 54%. Increasing demand for durable, yet lightweight solutions that boost fuel efficiency and performance have been driving growth so far. High-profile manufacturers like Boeing and Toray Industries are leading advances in composite technologies, which is expanding its capacity for carbon fiber to match the rising car orders, while Boeing is considering utilizing advanced composites for vehicle design applications. The use of composites also incurs a reduction in weight as high as 20 to 30%, with a direct consequence on fuel efficiency and as high as 15% reduction in CO2 emissions along the lifetime of the vehicle.

The Elastomers segment in this market is expected to witness the fastest CAGR of 7.36% in the forecast period through which the automobile sector, particularly faces the need for more elastic, easy-to-use materials that reduce the weight of a vehicle. BASF has developed the most recent elastomer products related to the increasing demand for car performance with less weight, such as new tire compounds providing better fuel efficiency. Continental puts all its efforts into finding new applications for elastomers in seals and gaskets and focusing on durability and efficiency.

REGIONAL ANALYSIS

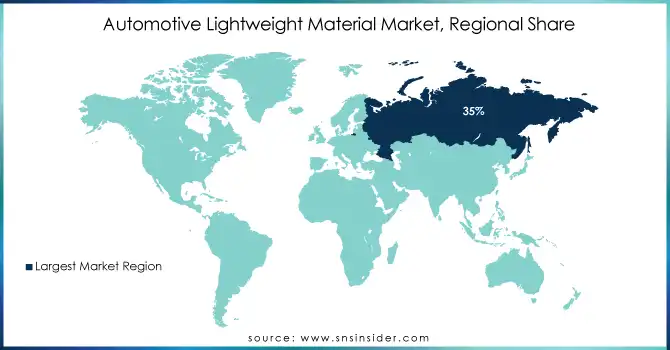

In 2023, the European automotive lightweight materials market captured a substantial market share of approximately 35%, Strict emissions regulations have been the main cause for this dominance as the commitment to such regulations forces heavy investment by manufacturers in lightweight technologies that aim at optimizing fuel efficiency and minimizing CO2 levels.

-

For instance, European Union's aim to reduce greenhouse gas emissions by 55% by 2030, increasing the adoption of lightweight materials, which, as projected, would reduce the overall weight of the vehicle by almost 30% using advanced materials, such as aluminum and carbon fiber. In addition, through lightweight solutions, the European automotive industry will bring about a combined reduction of approximately 220 million metric tons by 2030.

In 2023, North America emerged as the fastest-growing region in the automotive lightweight materials market, with a projected CAGR of 6.86% from 2024 to 2032. This is being spurred by increasing demand for fuel-efficient vehicles, improvements in manufacturing technologies, and positive initiatives from governments to reduce carbon emissions.

-

For example, the U.S. Department of Energy has also invested in development research into lightweight materials that not only drove innovation but also transformed the car industry. These companies, like General Motors and Ford, are actively introducing new models that utilize lightweight materials to improve the efficiency and performance of their vehicles.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key players

Some of the major players in the Automotive Lightweight Material Market are:

-

ThyssenKrupp AG (High-Strength Steel Alloys, Advanced High-Strength Steel (AHSS))

-

Novelis, Inc. (Aluminum Sheet and Plate, Aluminum Extruded Shapes)

-

Alcoa Corporation (Aluminum Sheet and Plate, Aluminum Extruded Shapes)

-

Owens Corning (Glass Fiber Composites, Carbon Fiber Reinforced Composites)

-

Toray Industries, Inc. (Carbon Fiber Reinforced Composites, High-Performance Resins)

-

ArcelorMittal (Advanced High-Strength Steel (AHSS), High-Strength Steel Alloys)

-

BASF SE (Polyurethane Foam, Polyamide Composites)

-

Covestro AG (Polycarbonate Composites, Polyurethane Foam)

-

Magna International (Magnesium Alloy Components, Aluminum Alloy Components)

-

3M Company (Structural Adhesives, Sealing Tapes)

-

Arconic Inc. (Aluminum Sheet and Plate, Aluminum Extruded Shapes)

-

DuPont de Nemours, Inc. (Kevlar Aramid Fiber Composites, Nomex Nomex Fiber Composites)

-

General Motors Company (Carbon Fiber Reinforced Plastic (CFRP) Components, Magnesium Alloy Components)

-

Nippon Steel Corporation (High-Strength Steel Alloys, Advanced High-Strength Steel (AHSS))

-

Sumitomo Chemical Co., Ltd. (Engineering Plastics, Polyurethane Foam)

-

LyondellBasell Industries Holdings B.V. (Polypropylene Composites, Polyethylene Composites)

-

Stratasys Ltd. (3D Printed Polymer Composites, 3D Printed Metal Composites)

-

Tata Steel (High-Strength Steel Alloys, Advanced High-Strength Steel (AHSS))

-

POSCO (High-Strength Steel Alloys, Advanced High-Strength Steel (AHSS))

-

PPG Industries (PPG Automotive Coatings, PPG Automotive Glass)

RECENT TRENDS

-

In October 2024, Gestamp unveiled the most recent innovations in lightweight at the 12th International Suppliers Fair (IZB) in Wolfsburg, Germany. The company there presented its Multipath Platform Concept chassis, which is also adaptable for different powertrains, and can avoid up to 50% of investments in tooling. Gestamp also revealed GES-MULTISTEP 2.0 hot stamping technology that allows the company to add strength to its product through ultra-high-strength steel.

-

In April 2024, Hyundai Motor Group signed a strategic partnership deal with Toray Group, aiming to develop future mobility solutions by using innovative materials such as carbon fiber. Both companies sought to mutually set the production of carbon fiber-reinforced plastics to enhance vehicle performance and safety. By doing so, both firms promised to actively integrate these advanced materials into new mobility products over the next period. The signing ceremony, held at the headquarters of Hyundai, was another monumental step toward increasing efficiency and even durability in mobility applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 82.68 Billion |

| Market Size by 2032 | US$ 128.02 Billion |

| CAGR | CAGR of 5.0 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Metals, Composites, Plastics, Elastomers) • By End-use (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)) • By Application Type (Body in White, Chassis and Suspension, Powertrain, Closures, Interiors, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ThyssenKrupp AG, Novelis, Inc., Alcoa Corporation, Owens Corning, Toray Industries, Inc., ArcelorMittal, BASF SE, Covestro AG, Magna International, 3M Company, Arconic Inc., DuPont de Nemours, Inc., General Motors Company, Nippon Steel Corporation, Sumitomo Chemical Co., Ltd., LyondellBasell Industries Holdings B.V., Stratasys Ltd., Tata Steel, POSCO, Covestro AG |

| Key Drivers | • Stricter Emissions Regulations Propel Adoption of Lightweight Materials in Automotive Manufacturing • Rising Consumer Demand for Fuel Efficiency Sparks Innovations in Lightweight Materials |

| Restraints | • High Production Costs Impede Adoption of Lightweight Automotive Materials |

Frequently Asked Questions

Ans: Composites dominated the Automotive Lightweight Material Market.

Ans: The major growth factor of the Automotive Lightweight Material Market is the increasing demand for fuel-efficient and lightweight vehicles to meet stringent emissions regulations and improve fuel economy.

Ans: The Automotive Lightweight Material Market size was USD 82.68 billion in 2023 and is expected to Reach USD 128.02 billion by 2032.

Ans: Europe dominated the Automotive Lightweight Material Market in 2023.

Ans: The Automotive Lightweight Material Market is expected to grow at a CAGR of 5.0% during 2024-2032.

Get in Touch