Bone Void Fillers Market Report Scope & Overview:

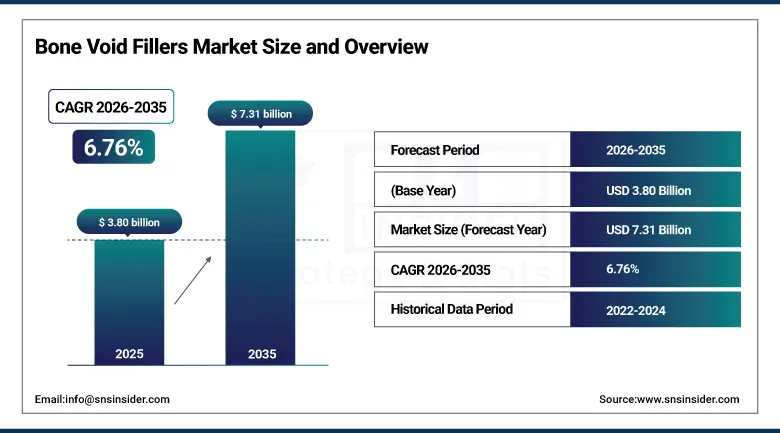

The Bone Void Fillers Market was valued at USD 3.80 billion in 2025 and is expected to reach USD 7.31 billion by 2035, growing at a CAGR of 6.76% from 2026–2035.

The Bone Void Fillers market is forecasted to see strong, sustained growth as the multi-level structural forces of a rapidly aging global population at inherently higher risk for pathways leading to osteoporotic fractures continues to combine with growing epidemiology of orthopedic trauma and sports-related oscillatory fractures; dramatic ascension in surgical volumes for spinal fusion; and unprecedented innovation in tissue-regenerative biomaterials, anticipated to yield next-generation synthetic bone graft substitutes w/ enhanced osteoconductive & osteoinductive capabilities. More than 8.9 million osteoporosis fractures are reported every year globally and thus this translates to a vast and increasing patient population needing to have their structural bone repaired, while in the US one spinal fusion surgery is performed every eight minutes with each representing an area of clinical need where bone void fillers provide the required structural support and regenerative stimulus. Bone void fillers not only fill structural voids from fractures, tumour resections, infections and surgery but also provide osteoconductive scaffold and Osteoinductive growth factors in the form of demineralised bone matrix (DBM), synthetic calcium phosphate and sulphate ceramics, collagen matrices bioactive glasses, composite materials.

Bone Void Fillers Market Size and Forecast

-

Market Size in 2025: USD 3.80 Billion

-

Market Size by 2035: USD 7.31 Billion

-

CAGR: 6.76% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Bone Void Fillers Market - Request Free Sample Report

Bone Void Fillers Market Trends

-

Accelerating innovation in synthetic calcium phosphate and sulfate bone void fillers including bioceramics, hydroxyapatite, and tricalcium phosphate that eliminate disease transmission risk associated with allograft-derived DBM while offering controllable porosity, customisable resorption rates, and superior structural properties matching cortical and cancellous bone.

-

Growing adoption of pre-filled syringe and ready-to-use putty formulations as exemplified by LifeNet Health's PliaFX Flo pre-filled syringe DBM that eliminate intraoperative mixing steps, improve handling convenience, and reduce surgical time, driving preference over traditional powdered or granular formats.

-

Increasing clinical adoption of bioactive glass bone void fillers which actively stimulate bone formation through ionic dissolution products that activate osteoblast activity particularly in dental and orthopaedic applications where enhanced bioreactivity can accelerate healing.

-

Growing development of antibiotic-eluting bone void filler platforms including calcium sulfate-antibiotic composites for infected bone defect management in osteomyelitis and orthopaedic implant infection cases where local antibiotic delivery directly to the defect site is clinically superior to systemic administration.

-

Rising integration of 3D printing and additive manufacturing in patient-specific bone void filler scaffold fabrication, enabling anatomically precise, customised defect filling geometries for complex cranial, maxillofacial, and spinal reconstruction procedures.

-

Expanding dental and maxillofacial surgery applications for bone void fillers driven by the global dental implant market's growth and the clinical requirement for bone augmentation procedures prior to implant placement creating a high-growth adjacent market segment.

-

Increasing minimally invasive surgical adoption in orthopaedics driving demand for injectable, flowable bone void filler formulations including calcium phosphate cements and injectable DBM pastes that can be delivered through small-bore cannulas without large surgical exposures

U.S. Bone Void Fillers Market Size Outlook:

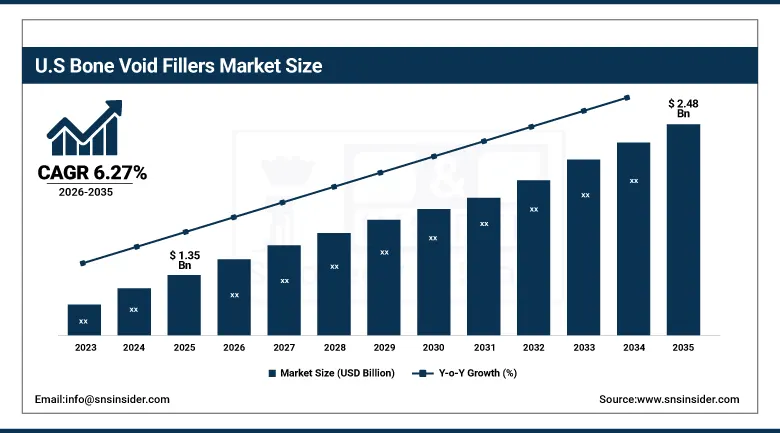

U.S. Bone Void Fillers Market was valued at USD 1.35 billion in 2025 and is expected to reach USD 2.48 billion by 2035, registering a CAGR of 6.27% during 2026–2035.

The U.S. continues to be the largest market for bone void fillers in the world, fueled by global high per-capita orthopedic and spinal surgical volumes, one of the world's oldest populations more prone to osteoporosis and degenerative bone diseases, as well as a strong FDA 510(k) pathway encouraging rapid commercialization of new synthetic bone graft substitutes. The world´s best ortho-biologics companies, whose never-ending product innovation cycles slowly, but reliably produce clinically superior bone void filler solutions with market capitalization levels are anchored to the U.S. Qualified products like Acuitive Technologies' CITREPORE Bioactive Synthetic Filler and LifeNet Health's PliaFX Flo Pre-Filled DBM Syringe have received FDA clearance in just the past few months, assuring a vigorous product development pipeline to maintain U.S. market leadership throughout the forecast period.

The FDA's clearance of Acuitive Technologies' CITREPORE a bioactive synthetic filler using CITREGEN biomaterial that metabolically guides bone healing by actively modulating the biochemical environment of the defect site represents the leading edge of next-generation bone void filler innovation, where synthetic materials are progressively evolving beyond passive osteoconductive scaffolds into active, bioresponsive platforms that dynamically interact with the host bone biology to guide, accelerate, and optimise bone regeneration outcomes across the clinical indications that comprise the U.S. bone void fillers market.

Bone Void Fillers Market Segment Insights

-

Based on Type, Demineralized Bone Matrix (DBM) accounted for the largest revenue share (28.45%) in 2025; Synthetic Bone Void Fillers (Calcium Phosphate/Sulfate) expected to be the fastest-growing type segment (CAGR of 7.52%).

-

Based on Form, Putty accounted for the largest revenue share (32.18%) in 2025; Injectable/Flowable forms expected to be the fastest-growing form segment (CAGR).

-

Based on Application, Orthopedic Surgery accounted for the largest market share in 2025; Dental & Maxillofacial expected to be the fastest-growing application segment (CAGR).

-

Based on Application, Hospitals dominated with a share of 62.35% in 2025; Specialty Clinics expected to be the fastest-growing end-user segment (CAGR of 7.41%).

By Type: DBM dominates, Synthetic Bone Void Fillers grow fastest

The largest type segment revenue share of ~28.45% in 2025, was captured by Demineralized Bone Matrix however the time-tested reliability of DBM as a grafting material offering an optimal combination of osteoconductive collagen matrix and osteoinductive growth factors (including BMPs and TGF-β retained through the demineralisation process), which promotes bone formation across a broad range of defect types and clinical scenarios made it obvious that its success would continue here. The availability of DBM in multiple formulations (putty, gel, paste and strip) permits application tailored to the surgeon-across various defect geometries reinforcing its clinical preference across a wide range of orthopaedic and spinal surgical practices worldwide.

Synthetic bone void fillers, most notably calcium phosphate ceramics—a product area that includes hydroxyapatite and beta-tricalcium phosphateand calcium sulfate are expected to post the highest type segment CAGR of 7.52% from 2026–2035 on account of ongoing materials science advancements continuing to close biological performance gaps with allograft-derived products while offering significant siteless advantages: an absence of disease transmission risk, unlimited scalability, expandable porosity and resorption kinetics based on design preferences tailored for the target application at hand, and consistency batch-to-batch afforded through static donor variability independence. A body of clinical evidence substantiating the safety and efficacy endpoints for synthetic grafts coupled with several recent FDA clearances of novel bioactive synthetic formulations has continued to improve surgeon acceptance and clinical utilization of next-generation premium synthetic bone void filler platforms.

By Form: Putty dominates, Injectable grows fastest

Putty formulations dominated the Bone Void Fillers Market in 2025 with approximately 32.18% of revenue, driven by putty's superior handling characteristics including moldability to conform to irregular defect geometries, cohesive consistency that maintains containment at the surgical site, immediate structural support provision, and compatibility with the intraoperative workflow of most orthopaedic and spinal surgeons. The advent of pre-formulated putties contained in ready-to-use syringes that eliminate the intraoperative mixing of putty components and reduce preparation time has further accelerated putty format adoption across both hospital-based and ambulatory surgical settings.

In 2025, The injectable and flowable bone void filler format is expected to be the fastest growing segment of the bone void fillers market due to a global trend toward less invasive orthopaedic surgical modalities that facilitate access using small-diameter cannulas as opposed to large open surgical exposures. Within this therapeutic segment, calcium phosphate cements and injectable DBM paste formulations are leading the way to percutaneous vertebroplasty, kyphoplasty and minimally invasive fracture fixation procedures with minimal third operative trauma, blood loss, hospital stay and patient convalescence..

By End-User: Hospitals dominate, Specialty Clinics grow fastest

Hospitals retained the dominant end-user position in the Bone Void Fillers Market in 2025 with approximately 62.35% of revenues, reflecting their role as the primary centres for complex orthopaedic trauma surgeries, spinal fusion procedures, joint reconstruction, tumour resections, and major dental-maxillofacial operations that collectively represent the highest-acuity bone void filler applications. Hospital orthopaedic departments, operating room supply chains, and hospital value analysis committees are the principal procurement decision-making centres for bone void filler products, giving leading manufacturers' hospital sales forces and clinical education programmes decisive influence over product adoption.

Specialty clinics — including ambulatory surgical centres, dedicated orthopaedic surgery centres, and specialised dental and maxillofacial clinics — are projected to record the highest end-user CAGR of 7.41% from 2026 to 2035, driven by the accelerating global migration of appropriate orthopaedic and spinal procedures from inpatient hospital settings to outpatient ASCs where bone void fillers are increasingly used in minimally invasive fracture repair, spinal decompression, and dental bone augmentation procedures. The growing ASC surgical volume base, superior cost efficiency relative to hospital facilities, and patient preference for outpatient recovery are collectively propelling specialty clinic growth as the fastest-expanding bone void filler end-user segment.

Bone Void Fillers Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

47% |

|

Europe |

Germany |

33% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

43% |

North America Bone Void Fillers Market Insights

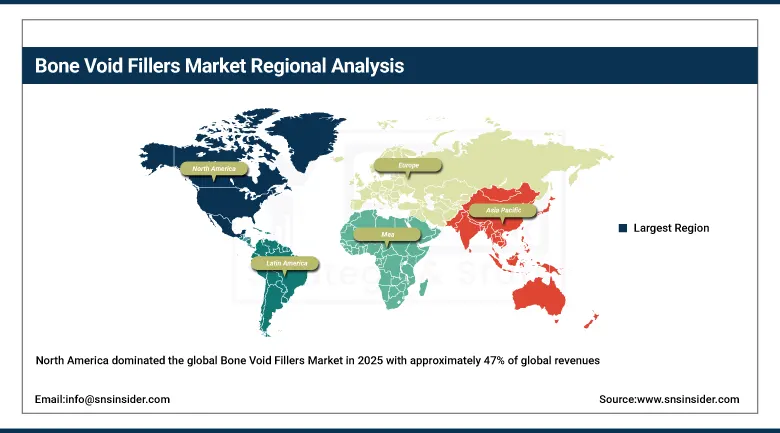

North America dominated the global Bone Void Fillers Market in 2025 with approximately 47% of global revenues, led by the United States the world's largest orthopaedic and spinal surgery market. U.S. market leadership is reinforced by advanced healthcare infrastructure, the highest orthopaedic surgical volumes globally, strong FDA regulatory frameworks supporting rapid bone void filler innovation, comprehensive insurance reimbursement for approved orthopaedic procedures, and the commercial presence of the world's leading orthopaedic biomaterials companies. The rapidly aging U.S. baby boomer population with the youngest members reaching 61 years in 2025 — represents a massive and growing orthopaedic patient pool creating sustained structural demand for bone void filler products through 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Bone Void Fillers Market Insights

Asia Pacific is the fastest-growing regional Bone Void Fillers Market with a CAGR of 7.89% from 2026 to 2035, supported by ongoing advancements in healthcare infrastructure across China, India, Japan, south-Korea and Australia with an increasingly aging population susceptible to osteoporotic fractures (supported through a strong medical tourism market), as well as extensive government-backed biomaterials development programmes including Chinas "Made in China" technology initiative focused on improving health outcomes and boosting economic growth. Trauma and cancer-related bone surgeries are growing rapidly in China and India supported by improving orthopaedic healthcare access, domestic medical device manufacture growth, and rising healthcare expenditure of the middle classes.

Europe Bone Void Fillers Market Insights

Europe represents a major bone void fillers market, characterised by comprehensive national healthcare system coverage of orthopaedic procedures, sophisticated orthopaedic and trauma surgery clinical networks, and the presence of advanced European orthopaedic biomaterials companies including Biocomposites, BONESUPPORT AB, and Graftys. Germany, France, the UK, Italy, and Spain are the leading European markets, each supported by well-established orthopaedic trauma care systems and growing adoption of synthetic bone graft substitutes that meet EU medical device regulatory requirements.

Middle East & Africa and Latin America Bone Void Fillers Market Insights

MEA and Latin America are growing bone void filler markets, supported by improving orthopaedic healthcare infrastructure, rising surgical volumes, and increasing adoption of advanced bone repair solutions. Brazil leads Latin American revenues with approximately 43% of regional share, anchored by its large population and improving orthopaedic healthcare access. The UAE leads MEA adoption through its advanced healthcare system, high surgical quality standards, and strong medical tourism sector attracting orthopaedic patients from across the region.

Bone Void Fillers Market Growth Drivers:

-

Aging global population, rising osteoporotic fractures, and biomaterial science innovation

The primary structural growth drivers for the Bone Void Fillers Market are the compounding epidemiological forces of global population aging with the WHO projecting that 2.1 billion people will be aged 60 years or older by 2050, a demographic disproportionately affected by osteoporosis and fragility fractures combined with the extraordinary innovation velocity of orthopaedic biomaterials science delivering next-generation synthetic and bioactive bone void filler products with progressive clinical performance improvements. The global spinal surgery market's continuous growth with procedures increasing as degenerative disc disease affects a larger fraction of aging populations creates an expanding clinical application base that sustains premium bone void filler demand growth through 2035.

The renewed partnership between Orthofix and MTF Biologics that will extend through 2032 to introduce a new DBM product under the Legacy brand — adding a unique formulation of cortical bone powder and sodium hyaluronate (RegenaForm) as a carrier in spine and orthopaedic applications which exemplifies these robust trends in both product development momentum and commercial partnership model responsible for driving sustained growth within this indication, where the blend of cutting-edge formulation science with established clinical heritage gated by strong distribution partnerships generates differentiated products commanding share whilst further sustaining value increases over an expanding global ortho surgical volume base.

Bone Void Fillers Market Restraints

-

Allograft supply constraints, high product costs, and complex regulatory approval pathways

The Bone Void Fillers Market faces a considerable restraint due to the limited availability of allograft bone tissue for DBM production which is regulated based on various factors such as cadaveric donation rates, tissue bank processing capacity and FDA regulatory oversight thereby creating supply constraints which limit their availability further keep pressure on pricing compared to synthetic substitutes. For example, the high costs of these advanced bone void filler products especially premium synthetic calcium phosphate and bioactive glass systems create reimbursement and adoption barriers to guidelines in many healthcare systems that have limited spend on orthopaedic implants, notably developing markets. This extended approval timeline creates a significant barrier for novel bone void filler products containing new materials or biological parts in obtaining 510(k) and PMA regulatory pathways from the FDA, pushing back commercial launch of these innovative technologies by years at additional expense.

Bone Void Fillers Market Opportunities

-

Antibiotic-eluting composites, dental bone augmentation, and Asia Pacific market penetration

Antibiotic-eluting bone void filler composites—biomaterials consisting of osteoconductive scaffolds with a local antibiotic delivery capacity—provide the ultimate solution to one of orthopaedic surgery's most important problems: how best to manage infected bone defects in such conditions as osteomyelitis and periprosthetic joint infection, thereby creating a high-revenue clinical opportunity. With the global dental implant market experiencing rapid growth, there is an increased demand for bone augmentation void filler products that are used to augment insufficient bone volume before placing a dental implant both empty cavities addressing in form of dedicated dental bone void filler products and diversifying applications using orthopaedic bone graft platforms. The large, untapped bone void filler market across aging populations and burgeoning orthopaedic healthcare infrastructure in Asia Pacific presents an attractive long-term growth opportunity for product makers that secure clinical relationships, reimbursement coverage, and penetration of distribution channels throughout China, India, and Southeast Asia through 2035.

Recent Developments:

-

January 2025: LifeNet Health launched PliaFX Flo, a pre-filled syringe format of its fiber demineralized bone matrix, significantly enhancing surgeon convenience through elimination of intraoperative mixing requirements and providing consistent, ready-to-use DBM delivery for orthopaedic and spinal applications.

-

November 2024: Acuitive Technologies received FDA clearance for CITREPORE, a bioactive synthetic bone void filler using CITREGEN biomaterial that metabolically guides bone healing by actively modulating the biochemical defect environment, representing a significant advance in next-generation synthetic graft technology.

-

2024: Zimmer Biomet expanded its bone void filler portfolio with enhanced calcium phosphate formulations offering improved handling properties and optimised porosity profiles for spinal fusion and trauma repair applications in both hospital and ambulatory surgical centre settings.

-

2025: Stryker advanced clinical validation of its synthetic bone void filler platform with new prospective clinical evidence demonstrating equivalent bone healing outcomes to autograft in tibial plateau fracture repair — a landmark endpoint that is expanding surgeon acceptance of synthetic alternatives in historically autograft-preferred applications.

-

2022–2025: Orthofix extended its partnership with MTF Biologics through 2032, launching a new demineralized bone matrix product under the Legacy brand featuring cortical bone powder and sodium hyaluronate carrier for spinal and orthopaedic applications, strengthening its DBM portfolio and global distribution reach.

Bone Void Fillers Market Key Players:

-

Zimmer Biomet Holdings, Inc.

-

Stryker Corporation

-

DePuy Synthes (Johnson & Johnson MedTech)

-

Medtronic plc

-

Smith & Nephew plc

-

NuVasive, Inc.

-

Globus Medical, Inc.

-

Wright Medical Group N.V. (Stryker)

-

Arthrex, Inc.

-

BONESUPPORT AB

-

Biocomposites Ltd.

-

Collagen Matrix, Inc.

-

LifeNet Health

-

MTF Biologics

-

Orthofix Medical Inc.

-

Acuitive Technologies

-

Graftys S.A.

-

Baxter International, Inc.

-

RTI Surgical, Inc.

-

Exactech, Inc.

Bone Void Fillers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.80 Billion |

| Market Size by 2035 | USD 7.31 Billion |

| CAGR | CAGR of 6.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Demineralized Bone Matrix, Synthetic Bone Void Fillers, Calcium Phosphate/Sulfate, Collagen Matrix, Bioactive Glass, and Others) • By Form (Putty, Granules, Paste/Gel, Strips, Beads, and Others) • By Application (Orthopedic Surgery, Spinal Fusion, Dental & Maxillofacial, Trauma Surgery, and Others) • By End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zimmer Biomet Holdings, Inc., Stryker Corporation, DePuy Synthes, Medtronic plc, Smith & Nephew plc, NuVasive, Inc., Globus Medical, Inc., Wright Medical Group N.V., Arthrex, Inc., BONESUPPORT AB, Biocomposites Ltd., Collagen Matrix, Inc., LifeNet Health, MTF Biologics, Orthofix Medical Inc., Acuitive Technologies, Graftys S.A., Baxter International, Inc., RTI Surgical, Inc., Exactech, Inc |

Frequently Asked Questions

Ans: The Bone Void Fillers Market is expected to grow at a CAGR of 6.76% from 2026 to 2035.

Ans: The Bone Void Fillers Market was valued at USD 3.80 billion in 2025.

Ans: The rapidly aging global population creating an escalating burden of osteoporotic fractures and degenerative bone conditions, combined with rising global orthopaedic and spinal surgical volumes and continuous biomaterial science innovation delivering clinically superior synthetic and bioactive bone void filler products, are the primary structural growth drivers through 2035.

Ans: Demineralized Bone Matrix (DBM) dominated the Bone Void Fillers Market in 2025 with approximately 28.45% of global revenue, driven by its time-tested clinical reliability offering the unique combination of osteoconductive collagen matrix and osteoinductive growth factors that promote bone formation across spinal, orthopaedic, and trauma surgical applications globally.

Ans: North America dominated the Bone Void Fillers Market in 2025 with approximately 47% of global revenues, led by the United States — the world's largest orthopaedic and spinal surgery market — supported by the highest surgical volumes, advanced healthcare infrastructure, comprehensive insurance reimbursement, and the concentration of world-leading orthopaedic biomaterials innovation companies.

Get in Touch