Fibrin Sealant Market Report Scope & Overview:

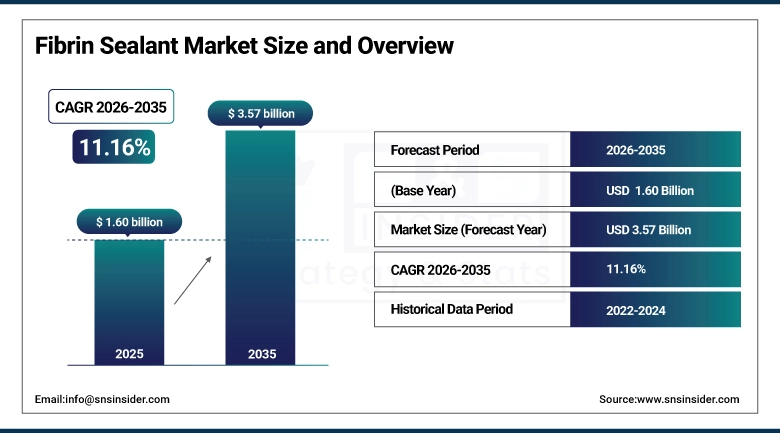

The Fibrin Sealant Market size is valued at USD 1.60 Billion in 2025 and is expected to reach USD 3.57 Billion by 2035, growing at a CAGR of 8.37% over the forecast period of 2026-2035.

The global fibrin sealant market report provides comprehensive analysis of market dynamics, product advancements, and clinical usage trends. Growing surgical procedures, increasing preference for biologically derived sealants, rising minimally invasive surgeries, and expanding applications across trauma and wound care are driving market growth during 2026–2035.

Fibrin sealant usage exceeded 210 million applications in 2025, fueled by rising surgeries and growing adoption of biologic tissue-sealing solutions.

Market Size and Forecast:

-

Market Size in 2025: USD 1.60 Billion

-

Market Size by 2035: USD 3.57 Billion

-

CAGR: 8.37% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Fibrin Sealant Market - Request Free Sample Report

Fibrin Sealant Market Trends:

-

Rising surgical volumes, including cardiovascular, orthopedic, and minimally invasive procedures, are boosting demand for reliable tissue-sealing solutions.

-

Growing adoption in trauma care and emergency surgeries is driving preference for fast-acting fibrin sealants.

-

Increased use of patch-based, spray, and liquid fibrin sealants is enhancing procedural efficiency and patient outcomes.

-

Innovations in recombinant and autologous formulations are improving biocompatibility, safety, and healing performance.

-

Expansion of ambulatory surgical centers and specialty clinics is fueling demand for easy-to-apply, cost-effective fibrin sealants.

-

Collaborations between sealant manufacturers, hospitals, and research institutions are accelerating product innovation and market reach.

U.S. Fibrin Sealant Market Outlook:

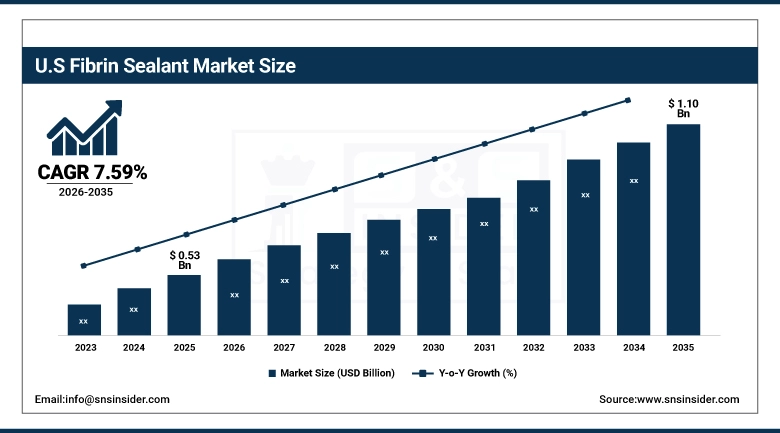

The U.S. Fibrin Sealant Market is projected to grow from USD 0.53 Billion in 2025 to USD 1.10 Billion by 2035, at a CAGR of 7.59%. Growth is driven by rising surgical volumes, increasing minimally invasive procedures, strong adoption of liquid, patch-based, and spray fibrin sealants, and investments in innovative tissue-sealing solutions across hospitals and ambulatory surgical centers.

Fibrin Sealant Market Growth Drivers:

-

Growing adoption of biologic tissue-sealing solutions in minimally invasive surgeries accelerating fibrin sealant demand.

Growing adoption of biologic tissue-sealing solutions in minimally invasive surgeries is a major driver of Fibrin Sealant Market growth. Hospitals, specialty clinics, and ambulatory surgical centers are increasingly using liquid, patch-based, and spray fibrin sealants to enhance surgical efficiency, reduce bleeding, and improve patient recovery. Rising cardiovascular, orthopedic, and trauma procedures, combined with innovations in recombinant and autologous formulations, advanced biomaterials, and user-friendly delivery systems, are further boosting adoption and supporting sustained market expansion.

Over 62% of hospitals and surgical centers adopted fibrin sealants in 2025 to enhance surgical efficiency and bleeding control.

Fibrin Sealant Market Restraints:

-

Limited insurance reimbursement and high costs of fibrin sealants are slowing adoption in emerging healthcare markets.

High costs of fibrin sealants and limited insurance reimbursement remain significant restraints for the Fibrin Sealant Market. Premium liquid, patch-based, and spray formulations increase procedural expenses, limiting adoption in small and mid-sized hospitals, specialty clinics, and emerging markets. Inconsistent reimbursement policies and budget constraints discourage routine use, particularly for elective or minimally invasive procedures. Additionally, procurement challenges, clinician training requirements, and price sensitivity in cost-conscious regions further hinder widespread adoption, slowing market penetration despite rising surgical volumes and growing demand for effective tissue-sealing solutions.

Fibrin Sealant Market Opportunities:

-

Expanding use of recombinant and autologous fibrin sealants in complex surgeries offers significant market growth potential.

Expanding use of recombinant and autologous fibrin sealants in complex surgeries presents significant opportunities for the Fibrin Sealant Market. Hospitals, specialty clinics, and ambulatory surgical centers are increasingly adopting these biologic sealants to improve tissue sealing, minimize blood loss, and enhance patient recovery. Manufacturers introducing innovative, safe, and user-friendly formulations can leverage this trend. Ongoing advancements in biomaterials, patch-based and liquid delivery systems, and bioactive sealants support broader adoption across cardiovascular, orthopedic, and trauma care procedures.

Over 52% of hospitals and surgical centers adopted recombinant and autologous fibrin sealants in 2025, driven by complex and minimally invasive surgeries.

Fibrin Sealant Market Segmentation Analysis:

-

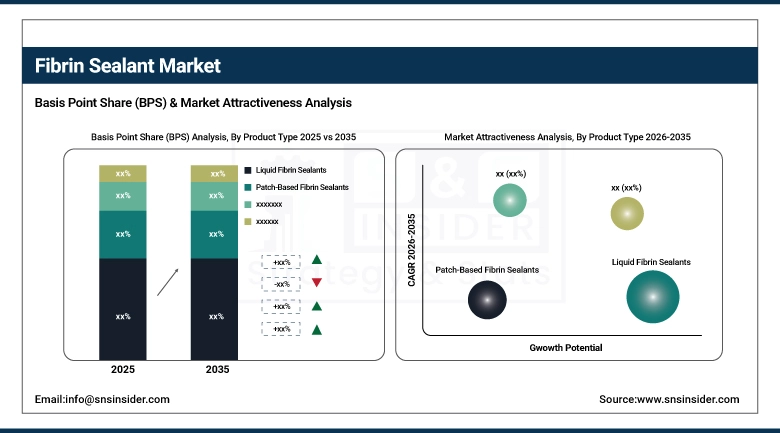

By Product Type, Liquid Fibrin Sealants held the largest market share of 45.32% in 2025, while Spray-Based Sealants are expected to grow at the fastest CAGR of 9.12% during 2026–2035.

-

By Source, Human Plasma-Derived dominated with 52.68% market share in 2025, whereas Recombinant fibrin sealants are projected to record the fastest CAGR of 10.03% through 2026–2035.

-

By Form, Sheet & Patch accounted for the highest market share of 40.55% in 2025, while Matrix & Gel is expected to grow at the fastest CAGR of 9.25% during the forecast period.

-

By Application, Cardiovascular Surgery dominated with a 27.48% share in 2025, while Trauma Care is anticipated to expand at the fastest CAGR of 9.87% through 2026–2035.

-

By End-User, Hospitals held the largest share of 61.24% in 2025, while Ambulatory Surgical Centers are expected to grow at the fastest CAGR of 9.35% during the forecast period.

By Product Type, Liquid Fibrin Sealants Dominate While Spray-Based Sealants Grow Rapidly:

Liquid Fibrin Sealants segment dominated the market due to their ease of application, rapid hemostasis, and wide adoption in cardiovascular, orthopedic, and general surgeries. In 2025, usage exceeded 95 million applications, reflecting strong preference among hospitals and ambulatory surgical centers for reliable tissue-sealing solutions.

Spray-Based Sealants are the fastest-growing segment, driven by rising minimally invasive and complex procedures requiring uniform coverage on irregular tissue surfaces. Adoption surged, with usage surpassing 40 million applications in 2025, particularly in trauma care and laparoscopic surgeries.

By Source, Human Plasma-Derived Fibrin Sealants Dominate While Recombinant Sealants Grow Rapidly:

Human Plasma-Derived segment dominated the market due to their proven safety, clinical familiarity, and widespread regulatory approvals. Hospitals and surgical centers relied on them for cardiovascular and orthopedic procedures, with usage exceeding 105 million applications in 2025.

Recombinant is the fastest-growing segment, benefiting from advances in biotechnology, reduced risk of pathogen transmission, and rising adoption in complex surgeries. Usage of recombinant products exceeded 42 million applications in 2025, particularly in trauma care and minimally invasive surgeries.

By Form, Sheet & Patch Dominate While Matrix & Gel Grows Rapidly:

Sheet & Patch segment dominated the market due to their ease of handling, precise placement, and suitability for a wide range of surgical procedures, including cardiovascular and general surgery. Usage reached 88 million units in 2025, reflecting strong adoption across hospitals and specialty clinics.

Matrix & Gel is the fastest-growing segment, driven by its adaptability to irregular wound surfaces and minimally invasive procedures. Usage surpassed 38 million units in 2025, especially in orthopedic and trauma surgeries, highlighting increasing clinical preference for versatile delivery formats.

By Application, Cardiovascular Surgery Dominates While Trauma Care Grows Rapidly:

Cardiovascular Surgery segment dominated the market due to high surgical volumes, critical bleeding risks, complex procedural requirements, and preference for reliable hemostatic solutions. Applications exceeded 72 million procedures, supported by hospitals and cardiac specialty centers.

Trauma Care is the fastest-growing segment, driven by rising accidents, emergency surgeries, and adoption of rapid-acting sealants in ambulatory and emergency care settings. Usage surpassed 35 million applications in 2025, reflecting growing demand for effective bleeding control in trauma and acute care procedures.

By End-User, Hospitals Dominate While Ambulatory Surgical Centers Grow Rapidly:

Hospitals segment dominated the market due to higher surgical volumes, infrastructure, and adoption of advanced fibrin sealants for cardiovascular, orthopedic, and general surgeries. Usage exceeded 120 million applications, reflecting strong institutional preference and consistent demand across multiple surgical specialties.

Ambulatory Surgical Centers are the fastest-growing segment, fueled by the expansion of minimally invasive procedures and outpatient surgeries. Adoption surpassed 38 million applications in 2025, particularly in orthopedic, cosmetic, and minor trauma procedures, highlighting their increasing role in driving market growth for easy-to-use, cost-effective fibrin sealants.

Regional Insights:

North America Fibrin Sealant Market Insights:

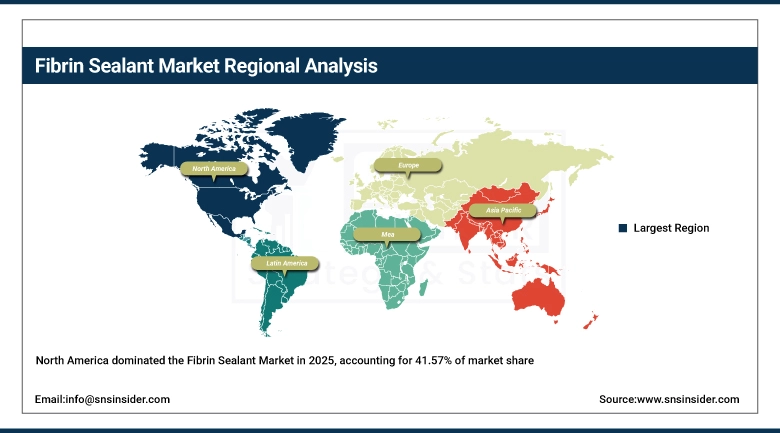

The North America Fibrin Sealant Market is dominated, holding a 41.57% share in 2025, driven by high surgical volumes and well-established hospital infrastructure across the U.S. and Canada. Strong adoption of liquid, patch-based, and spray fibrin sealants in hospitals and ambulatory surgical centers fuels growth. Rising cardiovascular, orthopedic, and trauma procedures, along with increasing minimally invasive surgeries, further support market expansion. Continuous innovations in recombinant and autologous formulations, clinician training, and supportive healthcare policies reinforce North America’s leadership in this mature market.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. Fibrin Sealant Market is driven by high surgical volumes, well-established hospital infrastructure, and extensive adoption of liquid, patch-based, and spray fibrin sealants. Rising demand for cardiovascular, orthopedic, and minimally invasive surgeries, along with increasing trauma care procedures, advanced biomaterials, and clinician training initiatives, reinforces the U.S. as the leading market in North America.

Asia-Pacific Fibrin Sealant Market Insights:

The Asia-Pacific Fibrin Sealant Market is the fastest-growing region, projected to expand at a CAGR of 9.73% during 2026–2035. Growth is fueled by rising surgical volumes, increasing trauma cases, and expanding healthcare infrastructure across China, India, Japan, and Southeast Asia. Strong adoption of liquid, patch-based, and spray fibrin sealants, investments in minimally invasive procedures, and improving hospital and ambulatory surgical center capabilities are accelerating product uptake and driving dynamic market growth in the region.

The China Fibrin Sealant Market is driven by rising surgical volumes, increasing trauma cases, and expanding hospital infrastructure. Rapid adoption of liquid, patch-based, and spray fibrin sealants, growing investments in minimally invasive procedures, and improving emergency care capabilities are accelerating product uptake, positioning China as a major contributor to Asia-Pacific market growth.

Europe Fibrin Sealant Market Insights:

The Europe Fibrin Sealant Market is driven by increasing surgical volumes, advanced hospital infrastructure, and growing investments in minimally invasive procedures. Countries such as Germany, France, and the UK are shaping regional demand through widespread adoption of liquid, patch-based, and spray fibrin sealants. Expansion of ambulatory surgical centers, trauma and emergency care facilities, and supportive regulatory frameworks are boosting product adoption. Continuous innovations in recombinant and autologous formulations, biomaterials, and clinician training reinforce Europe’s importance in the fibrin sealant market.

Germany is a key market in the European Fibrin Sealant landscape, driven by advanced hospital infrastructure and high surgical volumes. Growth is supported by widespread adoption of liquid, patch-based, and spray fibrin sealants, investments in minimally invasive procedures, and strong regulatory focus on surgical safety, clinician training, and procedural efficiency.

Latin America Fibrin Sealant Market Insights:

The Latin America Fibrin Sealant Market is growing due to rising surgical volumes and expanding healthcare infrastructure. Adoption is supported by increasing use of liquid, patch-based, and spray fibrin sealants across Brazil, Mexico, and Argentina, with investments in minimally invasive procedures, trauma care, and clinician training driving regional market growth.

Middle East and Africa Fibrin Sealant Market Insights:

The Middle East & Africa Fibrin Sealant Market is expanding due to increasing surgical procedures and improving healthcare infrastructure. Rising adoption of liquid, patch-based, and spray fibrin sealants in hospitals and surgical centers is driving demand, with Saudi Arabia, the UAE, and South Africa emerging as key regional markets.

Competitive Landscape:

Baxter International Inc. is a leading healthcare company with a strong foothold in the fibrin sealant market through products such as TISSEEL and ARTISS, widely used in cardiovascular, orthopedic, and general surgeries. Baxter dominates due to its advanced R&D, clinically validated formulations, and precision in hemostasis performance. Extensive distribution, strong hospital partnerships, and clinician training programs ensure broad adoption. Continuous innovation in recombinant and plasma-derived sealants, along with supply-chain strength, reinforces Baxter’s position as a key fibrin sealant market leader.

-

In September 2025, Baxter International Inc. launched the updated ARTISS fibrin sealant with expanded FDA indications, optimized preparation, and broader use in autologous skin grafts and tissue flaps, enhancing versatility, improving bleeding control, and supporting burn, facial, and reconstructive surgeries.

Johnson & Johnson, through its Ethicon division, is a dominant player in the fibrin sealant market, offering products such as EVICEL and VISTASEAL, utilized across cardiovascular, orthopedic, and trauma surgeries. Ethicon’s market leadership is supported by high-quality, reliable formulations, strong distribution, and integration with its surgical device portfolio. Strategic investments in R&D, clinician education, and procedural efficiency solutions have reinforced adoption. Its innovative hemostatic technologies and regulatory approvals maintain Ethicon’s position as a preferred fibrin sealant provider.

-

In June 2025, Johnson & Johnson (Ethicon) launched EVICEL fibrin sealant enhancements with improved formulation stability, expanded procedural applications, and faster hemostasis, supporting cardiovascular, orthopedic, and trauma surgeries across hospitals and surgical centers.

CSL Behring, a biotherapeutics leader, is recognized for its plasma-derived and recombinant fibrin sealants, valued for safety, purity, and consistent performance across surgical applications. The company dominates select markets due to its expertise in plasma fractionation, rigorous clinical validation, and international distribution network. CSL Behring invests heavily in R&D for advanced formulations, clinician training, and collaborations with hospitals. Rising surgical volumes, trauma care demand, and minimally invasive procedures are driving adoption, consolidating CSL Behring’s leadership in the fibrin sealant market.

-

In April 2025, CSL Behring obtained European marketing authorization for Tissucol fibrin sealant, expanding neurosurgical indications, improving tissue sealing and bleeding control, and supporting safer and more effective outcomes in complex surgical procedures.

Fibrin Sealant Market Key Players:

-

Baxter International Inc.

-

Johnson & Johnson (Ethicon)

-

CSL Behring

-

Grifols S.A.

-

Pfizer Inc.

-

Takeda Pharmaceutical Company Limited

-

Stryker Corporation

-

B. Braun Melsungen AG

-

CryoLife, Inc.

-

Shanghai RAAS Blood Products Co., Ltd.

-

Hualan Biological Engineering Inc.

-

Vivostat A/S

-

Hemarus (Hemarus Therapeutics / Hemarus)

-

Z-Medica, LLC

-

Integra LifeSciences Corporation

-

Becton, Dickinson and Company

-

Corza Medical

-

Cohera Medical

-

Advanced Medical Solutions Group plc

-

Marquee Biosurgical

Fibrin Sealant Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.60 Billion |

| Market Size by 2035 | USD 3.57 Billion |

| CAGR | CAGR of 8.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Liquid Fibrin Sealants, Patch-Based Fibrin Sealants, Spray-Based Sealants) • By Source (Human Plasma-Derived, Autologous, Recombinant) • By Form (Liquid, Matrix & Gel, Sheet & Patch) • By Application (Cardiovascular Surgery, Orthopedic Surgery, General Surgery, Neurosurgery, Cosmetic & Plastic Surgery, Wound Closure, Trauma Care, Others) • By End-User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Emergency Care Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Baxter International Inc., Johnson & Johnson (Ethicon), CSL Behring, Grifols S.A., Pfizer Inc., Takeda Pharmaceutical Company Limited, Stryker Corporation, B. Braun Melsungen AG, CryoLife, Inc., Shanghai RAAS Blood Products Co., Ltd., Hualan Biological Engineering Inc., Vivostat A/S, Hemarus (Hemarus Therapeutics / Hemarus), Z-Medica, LLC, Integra LifeSciences Corporation, Becton, Dickinson and Company, Corza Medical, Cohera Medical, Advanced Medical Solutions Group plc, Marquee Biosurgical |

Frequently Asked Questions

North America dominated with a 41.57% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 9.73% during 2026–2035.

Liquid Fibrin Sealants dominated with a 45.32% share in 2025, while Spray-Based Sealants are projected to grow at the fastest CAGR of 9.12% during 2026–2035.

Growth is driven by rising surgeries, minimally invasive procedures, trauma care, and adoption of recombinant and autologous sealants.

The market is valued at USD 1.60 Billion in 2025 and is projected to reach USD 3.57 Billion by 2035.

The Fibrin Sealant Market is expected to grow at a CAGR of 8.37% during 2026–2035.

Get in Touch