Business Process as a Service Market Report Scope & Overview:

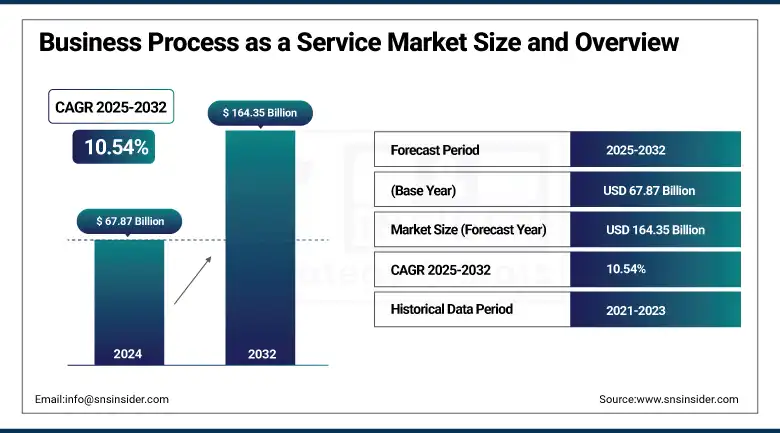

Business Process as a Service Market size was valued at USD 67.87 billion in 2024 and is expected to reach USD 164.35 billion by 2032, growing at a CAGR of 10.54% during 2025-2032.

The Business Process as a Service market growth is being fueled by the rising adoption of cloud computing, cost-effectiveness, automation, and flexibility provided by BPaaS solutions. Organizations are turning towards these services to automate processes, improve customer experiences, and increase scalability, thus contributing to the major market growth.

To Get more information On Business Process as a Service Market - Request Free Sample Report

According to research, 60% of all corporate information is currently housed in cloud infrastructures, and some 94% of enterprise-sized businesses are using cloud computing in their operations.

The U.S. Government Accountability Office (GAO) released a 2024 report affirming that 16 federal agencies have increased cloud services spending since 2015, saving a combined USD 291 million due to cloud implementation.

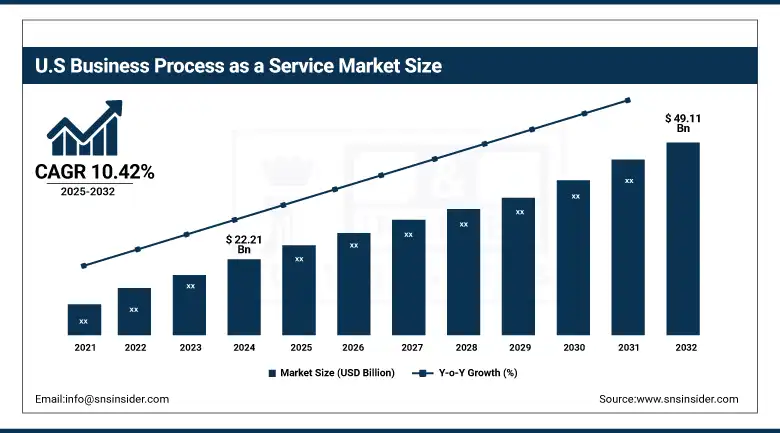

The U.S. Business Process as a Service Market was valued at USD 22.21 billion in 2024 and is expected to reach USD 49.11 billion by 2032, growing at a CAGR of 10.42% from 2025-2032.

While cost-effectiveness, flexibility, and adoption of cloud solutions are expected to be the key growth drivers in the U.S. BPaaS market. Companies are turning to outsourcing non-core functions to become leaner and more productive along with increased overall flexibility.

In 2024, the U.S. Department of the Treasury, along with the Financial Services Sector Coordinating Council, released guides to help financial institutions safely implement cloud computing, with an emphasis on best practices and risk management.

Additionally, the 2024 ABA Legal Technology Survey revealed that about 75% of lawyers currently utilize cloud computing for professional tasks, a rise from 69% in 2023, which reflects a strong cloud trend among legal professionals.

Business Process as a Service Market Dynamics

Drivers:

-

Surging Demand for Cost-Effective and Scalable Solutions is Reshaping How Enterprises Manage Non-Core Business Operations Globally

Enterprises are progressively embracing Business Process as a Service (BPaaS) to control operational costs and enhance scalability. This is triggered by the pressure to maximize budgets without compromising the quality of service. Being a cloud-based solution, it is flexible, deployable at a rapid pace, and can be upgraded efficiently. BPaaS helps firms achieve core competencies by alleviating the need for large-scale related IT infrastructure, enfolding less frugal but affordable financial and operational efficiency in competitive business markets.

According to Cognizant, deploying BPaaS enable businesses to transition to a pay-per-use consumption model, lowering total cost of ownership and supporting changing business requirements through scalable, on-demand solutions.

Furthermore, UST HealthProof indicates that its BPaaS customers have been able to achieve as much as 30% in average savings on operational costs, emphasizing the tremendous cost advantages of implementing BPaaS solutions.

Restraints:

-

Data Security Concerns and Regulatory Compliance Challenges Continue to Slow Enterprise Adoption of Business Process as a Service Solutions

While BPaaS has operational advantages, its uptake is constrained by data security, privacy, and regulatory compliance concerns. Organizations dealing with sensitive information are cautious about outsourcing key processes to third-party platforms. Legal differences, such as GDPR in Europe and HIPAA in the U.S., complicate compliance. Threats, such as data breaches and unauthorized access encourage caution. Until BPaaS providers enhance transparency, enhance security controls, and provide customized compliance solutions, these issues will slow broader adoption.

Furthermore, the U.S. Cybersecurity and Infrastructure Security Agency (CISA) also published a Cybersecurity Performance Goals Adoption Report in January 2025, examining 7,791 critical infrastructure organizations.

In the healthcare sector, a case study pointed out by Cognizant revealed how a one-million-member health plan effectively achieved all levels of regulatory compliance such as HIPAA 5010, ICD-10, HL7, FISMA, FedRamp, SOC2, and HITRUST by utilizing a broad-based BPaaS solution.

Opportunities

-

Embedding AI and Automation within BPaaS Platforms, New Frontiers of Pro-active Intelligence and Operational Excellence are Opening Up

Business process as a service (BPaaS) combined with artificial intelligence, machine learning, and robotic process automation will change business processes. These technologies enable sophisticated analytics, real-time decisions, and process optimization on an ongoing basis. Intelligent BPaaS allows the predictability of customer behavior, automation of manual tasks, and proactive service management. It turns results into smarter, faster, and more proficient results, thus enhancing end-user value. When enterprises seek out-of-the-box solutions, the confluence of AI and BPaaS creates novel applications and underutilized verticals across verticals like health, finance, and retail.

According to IBM, business process automation and AI are merging, with IBM Business Automation Workflow (BAW) leveraging AI-driven capabilities to enhance decision-making, automate manual tasks, and streamline business processes.

Infosys built 'Infosys Topaz', an AI-first solution that speeds up business value. With Infosys' AI and data science strength, a system handling 20 billion transactions delivered more than 50 varieties of intricate analyses within minutes, helping tax officers in India detect frauds that amounted to around ₹42,000 crores.

Furthermore, in 2023, Infosys Cloud, SaaS, and BPaaS services revenues were expected to increase by 40% yearly over the next three years, with an 80% compound annual growth rate (CAAGR) witnessed the last year.

Challenges:

-

Resistance to Change within Traditional Organizations Slows the Transition from Legacy Systems to Cloud-based Business Processes

Cultural resistance and organizational inertia are significant barriers to BPaaS adoption, especially within legacy-encumbered organizations. Internal resistance against cloud-enabled automation comes from employees, who are either afraid they will lose their jobs or are just comfortable with existing systems. Internal resistance is also something IT organizations face when trying to push for digital transformation, which means retraining and redesigning of systems. Without change management, executive sponsorship, no organization ever benefits from BPaaS. Then there is the sticky side of the human element, proving to be the number one barrier to pushing legacy businesses into agile online models.

According to a 2022 report by the Economist Intelligence Unit, 83% of business and IT leaders indicated that becoming more responsive to changing external circumstances depends greatly on upgrades in IT infrastructure and applications.

Additionally, the Indian School of Business (ISB) study pointed out that IT systems integrators are hindered in implementing cost-efficient, agile, and disruptive technologies by institutional resistance and the necessity to remove wasteful spending.

Business Process as a Service Market Segmentation Analysis

By Organization Size

Large enterprises dominated the BPaaS market in 2024 with a 65% revenue share due to their complex process requirements, and the ability to spend on high-end cloud solutions. Focusing on efficiency and scaling, such organizations are positioned to take advantages of BPaaS, optimizing workflows, lowering operating costs, and providing competitively-priced services. Their initial digital transformation strategies and establishment of partnerships with technology providers helped them secure their position as market leaders in this area.

Small and medium enterprises are projected to experience the fastest growth in the BPaaS market over 2025-2032, with a CAGR of 11.69%. This demand is fueled by increased access to cost-effective, cloud-based services for operational efficiency while avoiding large upfront capital exposure. Emerging and developed markets are making more digital infrastructure affordable to these smaller players, which are therefore adopting BPaaS as a means to automate non-core processes, free up new areas of agility, and compete with larger firms.

By Business Process

The accounting and finance category captured the highest proportion of the BPaaS market in 2024, at 24%, as a result of strong demand for automating financial processes. Companies leverage BPaaS to automate invoicing, payroll, compliance, and reporting with greater precision and lower expense. The routine, data-intensive nature of this function makes it ideally suited for outsourcing, with widespread adoption among companies looking to enhance financial transparency and operational efficiency.

Customer service and support is anticipated to grow at the fastest CAGR of 12.42% over 2025-2032, driven by the growing emphasis on customer experience and omnichannel engagement. To meet the soaring expectations, companies are making use of BPaaS powered backs by AI driven solutions (chatbot and help desk and call center). As competitive edge shifts to personalized, 24x7 service, demand for elastic, omnichannel, cloud-based support platforms only seem to strengthen.

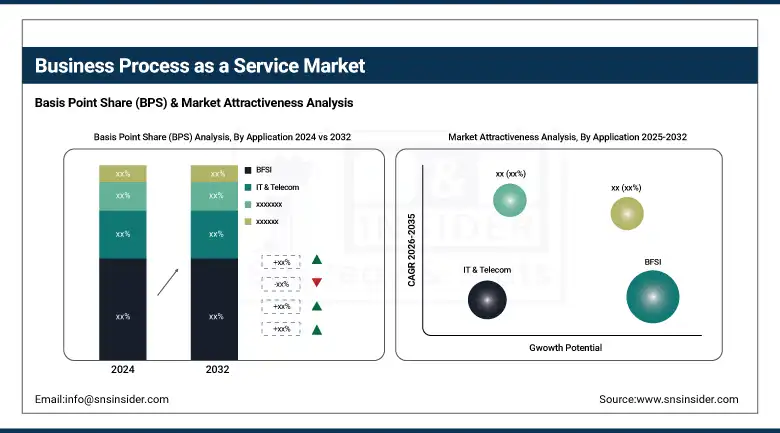

By Application

The BFSI segment dominated the Business Process as a Service market share of 26% in 2024 due to their reliance on processes that are compliant, secure, and highly automated. Financial institutions use BPaaS to ease customer onboarding, transactions, claims processing, and regulatory reporting. The ongoing need to control costs, manage risk, and enhance digital customer experience ensures sustainability of demand, particularly as banks deprivilege legacy technology assets and cloud initiatives become cloud-first.

The healthcare sector is projected to grow at the fastest CAGR of 13.10% from 2025 to 2032, driven by rising demand for digital health management and improved administrative efficiency. To process billing, claims, patient records, and regulatory compliance with higher speed and accuracy, payers, and providers are adopting the BPaaS model within the healthcare domain. As telehealth continues to be a critical modality of care, cloud-based process outsourcing will be required to help scale the business and expand the provision of care via the digital patient engagement.

By Deployment Mode

Public cloud led the BPaaS market in 2024 with a 59% revenue share as it is cost-effective, scalable, and can be deployed quickly. businesses across industries favored public cloud platforms to utilize as a space to host outsourced business processes based without an establishment of physical infrastructure. Public cloud became the preferred choice for enterprises accelerating their digital transformation initiatives due to its strong security capabilities, continuous innovation in services, and global reach.

The hybrid segment is also expected to advance at the fastest CAGR of 13.37% during the forecast period during 2025-2032 due to the ability to deliver balance between flexibility, data control, and regulatory compliance. Many companies are adopting hybrid cloud models to contain sensitive operations domestically and reserving public cloud for tunable scale and innovation. It offers complete end-to-end integration with legacy systems and caters to a number of operational needs, making it perfect for industries that are highly regulated or data-sensitive.

Business Process as a Service Market Regional Analysis

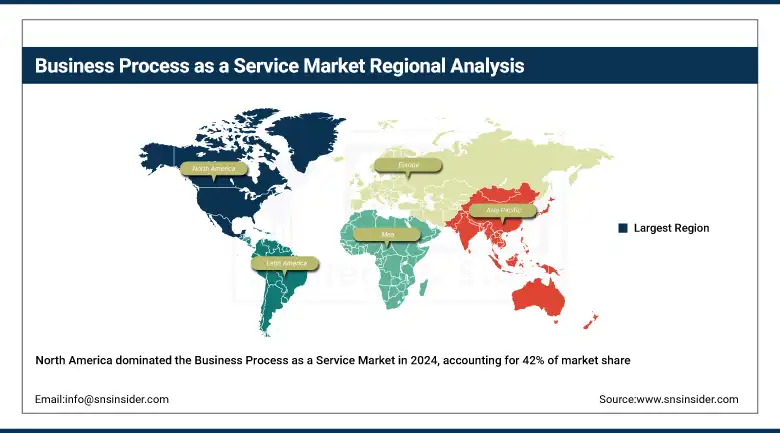

North America dominated the Business Process as a Service (BPaaS) market in 2024 with a 42% revenue share, fueled by high uptake of cloud due to mature digital infrastructure and presence of top market players. With a matured enterprise environment, emphasis on operational efficiencies, and ongoing investment in automation and AI-based solutions, the region has become a leader in BPaaS adoption across industries such as financial services, healthcare, retail, and professional services.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. dominated the BPaaS market due to advanced digital infrastructure, early cloud adoption, and strong presence of major service providers.

Asia Pacific is expected to experience the fastest BPaaS growth during 2025-2032, at a CAGR of 12.71%, due to digital transformation, increasing IT ecosystem and growing small enterprise and medium enterprise adopting cloud. While governments and enterprises are putting their money on automation and scalable infrastructure, the soaring labor costs and proactive population are leading organizations to adopt BPaaS for cost-saving process optimization and gaining a competitive edge aggressively.

China leads the BPaaS market in Asia Pacific because of accelerated digitalization, a huge enterprise ecosystem, and robust government support for cloud services. This expansion is underpinned by the country's enormous computing infrastructure, which, as of September 2023, comprised more than 7.6 million standard racks in data centers and a 45% year-over-year growth in intelligent computational capacity. Additionally, China also boasts the second-largest computing power in the world, at 197 exaflops as of September 2023.

Europe has a strong presence in the BPaaS market because of its well-developed IT infrastructure, growing need for automation, strong regulatory environments, and high adoption rates of cloud technologies in banking, healthcare, manufacturing, and government sectors

The U.K. dominates the BPaaS market trend in Europe because of its well-developed technology infrastructure, early mover advantage in cloud services, and high demand for cost-effective business process outsourcing solutions.

In 2021–2022 financial year, the U.K. government had spent more than £2.8 billion in cloud services through its G-Cloud procurement, with Amazon Web Services (AWS) bagging £147.8 million, indicating the nation's drive to adopt cloud technology.

The Scottish Government's Cloud Platform Service introduced in 2023 is meant to speed up the take-up of AWS and Microsoft Azure services within the public sector, paving the way for cloud integration.

The Middle East & Africa and Latin America are on the rise in the BPaaS market as a result of increasing digital transformation efforts, rising cloud usage, and pressure for low-cost business process optimization across emerging economies.

Key Players:

The leading players operating in the market are Accenture, Capgemini, Cognizant, DXC Technology Company, ExlService Holdings, Inc., Fujitsu, Genpact, HCL Technologies Limited, IBM, Infosys Limited, NTT DATA Group Corporation, Sutherland, TATA Consultancy Services Limited, Tech Mahindra Limited, and Wipro.

Recent Developments:

-

In October 2024, Accenture and NVIDIA launched the Accenture NVIDIA Business Group, enhancing enterprise AI adoption through the AI Refinery platform, powered by NVIDIA's AI stack.

-

In October 2024, Wipro, Microsoft, and SAP collaborated to offer near-zero-cost SAP migrations to RISE with SAP on Microsoft Cloud, aiding clients before SAP's 2027 support deadline.

-

In August 2024, Wipro integrated Google Cloud's Gemini models into its FullStride Cloud Studio, enhancing developer productivity and accelerating cloud migrations with GenAI solutions.

-

In November 2024, Tech Mahindra and AWS partnered to create an Autonomous Networks Operations Platform, transforming telecom operations with AWS AI and machine learning services on hybrid cloud.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 67.87 Billion |

| Market Size by 2032 | USD 164.35 Billion |

| CAGR | CAGR of 10.54% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Business Process (Human Resource Management (HRM), Accounting and Finance, Sales & Marketing, Customer Service and Support, Procurement & Supply Chain Management, Operations, Others) • By Deployment Mode (Public Cloud, Private Cloud, Hybrid) • By Organization Size (Small and Medium Enterprises, Large Enterprises) • By Application (BFSI, IT & Telecom, Manufacturing, Retail & E-commerce, Healthcare, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Accenture, Capgemini, Cognizant, DXC Technology Company, ExlService Holdings, Inc., Fujitsu, Genpact, HCL Technologies Limited, IBM, Infosys Limited, NTT DATA Group Corporation, Sutherland, TATA Consultancy Services Limited, Tech Mahindra Limited, Wipro |

Frequently Asked Questions

North America led the BPaaS market in 2024, with a 42% revenue share, driven by early cloud adoption and strong industry presence.

The accounting and finance segment dominated the BPaaS market in 2024, due to high demand for automation in repetitive, compliance-heavy processes.

The major growth factor is the increasing demand for cost-effective, scalable, and cloud-based solutions that streamline business operations and enhance flexibility.

The BPaaS market was valued at USD 67.87 billion in 2024 and is expected to reach USD 164.35 billion by 2032.

The BPaaS market is expected to grow at a CAGR of 10.54% from 2025 to 2032.

Get in Touch