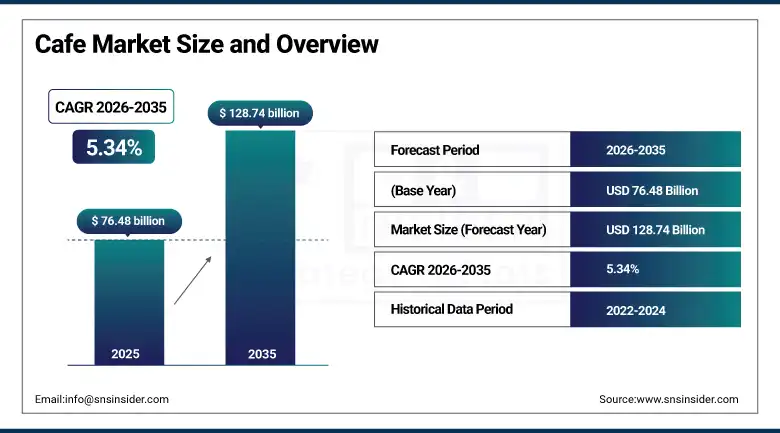

Cafe Market Report Scope & Overview:

The Cafe Market was valued at USD 76.48 Billion in 2025 and is expected to reach USD 128.74 Billion by 2035, growing at a CAGR of 5.34% from 2026 to 2035.

The global trends in the café sector continue experiencing steady growth on the back of evolving lifestyles, increased disposable incomes, and growing penetration of coffee culture in developing markets, and thereby the café emerges as an essential destination for both individual and business purposes. There are approximately 500,000 cafes running worldwide by 2025, with the consumption of specialty coffee registering above average growth in North America, Europe, and urban Asia. The rise in the number of people working from home and flexible work environment is contributing to the growth in consumers of the café owing to productivity-enhancing environments and strong connectivity facilities available in such spaces. Some of the factors responsible for keeping the consumers attached to the cafes include mobile ordering, artificial intelligence-based customization, and increased consumption of cold beverages. Café developments through urban development plans and tourism policies, along with better regulations in the food service industry have paved ways for new café locations in the Asia Pacific and Middle East regions.

Starbucks Corporation introduced its Siren System automation platform across North American flagship locations in 2025, integrating AI-driven beverage customization and predictive demand forecasting into barista workflows. The system reduced average beverage preparation time by 40% during peak periods, establishing a commercial template for technology-driven throughput improvement that major cafe chains globally are actively evaluating for adoption within their own operational frameworks.

Market Size and Forecast

-

Market Size in 2026E: USD 80.56 Billion

-

Market Size by 2035: USD 128.74 Billion

-

CAGR: 5.34% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get more information On Cafe Market - Request Free Sample Report

Cafe Market Trends

-

Rising consumer preference for specialty and third-wave coffee is driving premiumization across both chain and independent cafe formats globally.

-

Mobile ordering, digital loyalty programmes, and contactless payment integration are increasing transaction frequency and customer retention across urban cafe markets.

-

The remote work and hybrid workplace trend has structurally elevated cafe footfall among professional consumers seeking productive out-of-home working environments.

-

Sustainability-driven sourcing practices including direct trade procurement and compostable packaging are becoming key competitive differentiators for cafes targeting environmentally conscious consumers.

-

Cold brew, nitro coffee, and plant-based milk alternatives are growing into mainstream menu staples as health-conscious preferences reshape cafe beverage category composition globally.

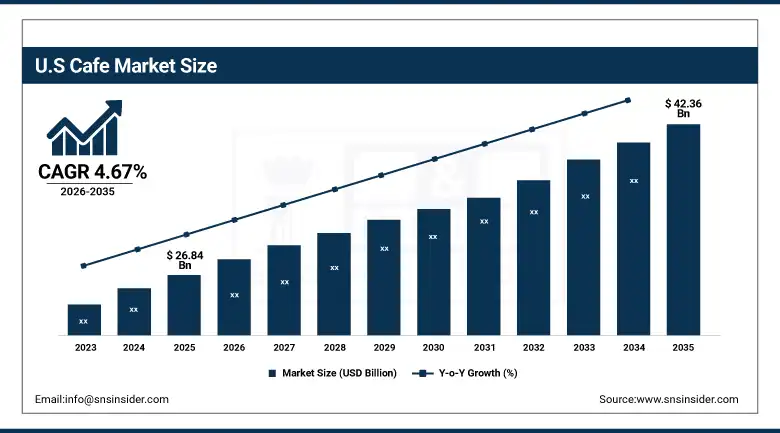

The U.S. Cafe Market Outlook

The U.S. Cafe Market was valued at approximately USD 26.84 Billion in 2025 and is expected to reach approximately USD 42.36 Billion by 2035, growing at a CAGR of approximately 4.67%.

The US is a dominant player in terms of the commercialized cafe market, which includes global cafe chains like Starbucks and Dunkin, specialty cafes, and an enormous market segment of independent cafes. There are over 16,500 Starbucks outlets across the country, and they are all located within high traffic institutional areas. There is a growing trend of consumer adoption of specialty coffee among Generation Millennials and Generation Z, where consumers are willing to pay extra money for craft brewed coffee and knowledge of their origins. The structural shift towards hybrid work has brought significant changes, making cafes much more relevant to work environments, where many individuals choose to work from cafes rather than their offices.

Dutch Bros Coffee surpassed 950 total system locations in 2025 after opening over 150 new drive-thru venues across Sun Belt and Mountain West markets. Its digital loyalty app integration and service speed model generated same-store sales growth of 6.3% in 2024, outperforming the broader U.S. cafe sector average and validating the commercial appeal of convenience-oriented formats that compete effectively against both established chains and specialty independents.

Cafe Market Segment Analysis

-

By Product Type, the espresso-based beverages segment dominated the cafe market with 42.36% share in 2025, while the cold brew & iced coffee segment is the fastest growing during 2026 to 2035.

-

By Ownership Type, the independent cafes segment dominated the cafe market in 2025, while the chain/branded cafes segment is the fastest growing during 2026 to 2035.

-

By Service Format, the dine-in segment dominated the cafe market with 52.48% share in 2025, while the delivery segment is the fastest growing during 2026 to 2035.

-

By Location Type, the standalone segment dominated the cafe market in 2025, while the travel & transit-integrated format is the fastest growing during 2026 to 2035.

-

By End User, the general consumers segment dominated the cafe market in 2025, while the corporate & office workers segment is the fastest growing during 2026 to 2035.

By Product Type, espresso-based beverages dominate, cold brew & iced coffee grow fastest

The espresso range of products continued to lead the product category with their share of 42.36% of the overall café market revenue in 2025. Lattes, cappuccinos, flat whites, and Americanos form the core beverages in all cafe formats worldwide and constitute the most frequent purchase occasion among existing consumers. The fastest-growing category includes cold brew and iced coffee as consumers increasingly show interest in chilled beverages that offer increased caffeine content. Coffee in cold formats enjoys high prices compared to their hot counterparts and thus improves the bottom line for businesses engaged in their production. Growing customer focus on healthy lifestyles and continued innovation in the area of flavored and plant-based coffees, along with the rising acceptance of cold coffee beverages throughout the year, drive this category's high rates of growth.

By Ownership Type, independent cafes dominate, branded chains grow fastest

The independent category was the largest by share in global unit numbers in 2025, representing around 56.84%. Commercial strength in the form of local relevancy, distinctiveness, and differentiation through direct trade is difficult for larger chains to achieve. Social media marketing has leveled the playing field in terms of building brands, allowing small cafes in single locations to build a following within their locality through social media without spending heavily on advertising. Franchise model cafes and chain/branded cafe owners were growing fastest due to the efficiency with which franchises operate and their use of technology to develop customer loyalty programs.

By Service Format, dine-in dominates, delivery grows fastest

The dine-in service format remained the largest revenue generator with 52.48% in 2025. Consumers who are committed to dining in also continue to include more foods and drinks in their orders. The physical space becomes the tangible representation of the brand and thus influences how much consumers stay and the number of times they return to the venue. Delivery is the fastest-growing format due to integration with third-party platforms and enabling the brand to generate revenue beyond the physical geography of its stores. Orders for office meetings, at home breakfasts, and even special events catered through deliveries do not depend on the actual location of the store. Menu design, which includes creating products that are safe for transport and easy-to-carry packaging options, is increasingly important for forward-thinking brands interested in optimizing delivery revenue contributions.

By Location Type, standalone locations dominate, travel & transit-integrated venues grow fastest

The standalone café site continued its position of dominance in 2025, being the archetype form due to its street-level presence and local nature, which creates the most commercially varied competition environment. Standalone sites create the most community involvement and consumer loyalty locally. The third most prominent growth category was that of travel sites, spurred on by consistent growth in the volume of passengers using air and rail transport throughout Asia and Europe. Sites operating in airport settings create average sale values significantly greater than those of street level as consumers show an enduring tendency to pay a premium for convenience in these captive environments. SSP Group is an example of international companies optimizing for travel retail.

By End User, general consumers dominate, corporate & office workers grow fastest

General Consumers continued to remain as the most prevalent end-users for 2025 with people visiting cafes during their routine engagements like their daily trips during the mornings and weekends when they are spending leisure time and afternoons where they hang around and work on their studies. The enrollment of members in loyalty programmes for most of the popular chains with millions of members enrolled worldwide ensures that the visits from general consumers remain regular throughout each product cycle. Corporate consumers and office employees form the quickest growing consumer segment with remote working boosting out-of-office consumption by people who had access to their drinks at the office premises earlier.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.62% |

|

Europe |

Germany |

24.73% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

28.34% |

|

Latin America |

Brazil |

44.28% |

North America Cafe Market Insights

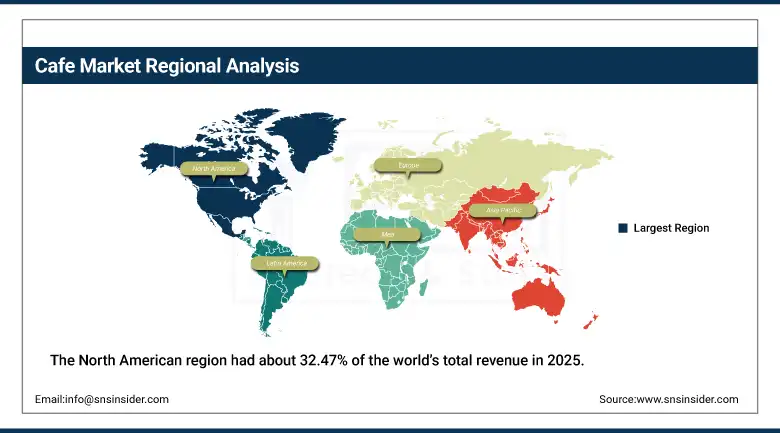

The North American region had about 32.47% of the world’s total revenue in 2025, out of which 84.62% comes from the US. Americans have high absolute levels of expenditure on coffee in cafes relative to their population size, fueled by the habit of drinking coffee every day. In areas where most of the people are dependent on cars and there is no option of walking to the cafes, the drive-thru concept works well and provides higher transaction speed. The Canadian contribution to the revenue is about 15.38%, owing to the popularity of the specialty cafes in Vancouver, Toronto, and Montreal, along with Tim Hortons, a culturally established brand that spans the geography of the entire nation through its franchises.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cafe Market Insights

Europe was leading the worldwide cafes' industry in 2025, accounting for roughly 36.82% of total worldwide revenue shares. Europe has an inherent cafe culture with the countries of Italy, France, Austria, Germany, and the United Kingdom consuming some of the highest coffee-per-capita amounts with a developed knowledge of the origins and production of coffees that keeps the prices high. Germany is responsible for almost 24.73% of Europe's revenue due to the country's tradition of Kaffeehaus and specialty coffees from Berlin and Munich. The United Kingdom's swift shift to becoming part of the third wave of cafes has created important chains like Costa Coffee and Pret a Manger.

Asia Pacific Cafe Market Insights

Asia-Pacific region is witnessing rapid growth in its cafe industry on account of exceptional acceptance of urban coffee culture in China, India, Japan, South Korea, Vietnam, and Indonesia, growing at a CAGR of 7.84%. China is a leading contributor accounting for almost 38.47% share in revenue of the regional market. Luckin Coffee achieved 20,000 stores till 2024, making specialty drinks readily available to consumers and compelling many major international players to come into this competition that favors market growth. India and Southeast Asia are emerging regions offering commercial viability, as coffee culture evolves into regular consumption habits among urban professionals and students alike. The high population density in Vietnam makes it among the top countries in Asia hosting cafes.

MEA & Latin America Cafe Market Insights

The UAE takes first place in MEA revenues with an approximate share of 28.34% of the region thanks to cosmopolitan infrastructure in hospitality, higher traffic of tourists, and a rich population of expats who consume cafes in accordance with premium international standards. The social reform project named 'Vision 2030' undertaken by Saudi Arabia has helped widen the target consumer base for the cafe within its home country. Brazil is the leading country among Latin American revenues, contributing to 44.28% of the regional total being the largest producer of coffee worldwide. Geographical proximity to the farms located in Minas Gerais, Sao Paulo, and Espirito Santo states has resulted in the emergence of a commercially unique specialty cafe industry.

Market Dynamics

Growth Drivers: Rising global coffee culture adoption and the cafe's repositioning as a social and professional destination are creating durable multi-market demand expansion.

Growth in the structure of the café market depends on the development of the coffee culture across emerging nations and the premiumization trend intensification in existing markets. Every year, about 200 million new urban middle-class consumers start drinking coffee as part of the life cycle stage in the Asia Pacific region. Major chains' digital loyalty programs show their ability to boost customer visits by 18 to 22 percent when compared with those who do not participate. Combined efforts in government urban development, tourism infrastructure expansion, and food services regulatory improvement are creating favourable conditions for new cafés in the Middle East, South Asia, and Sub-Saharan Africa.

Restraints: Rising input cost inflation across coffee sourcing, labor, and commercial real estate is compressing operating margins and constraining independent operator expansion viability.

Volatility in coffee commodity pricing due to production disruptions caused by weather factors in Brazil and Vietnam has placed great pressures on input costs for all players in the market during the years 2024 and 2025, with Arabica futures prices hitting record levels in early 2025. The increasing labor costs in North America and Europe have led to increased investment in automated processes and self-service technologies which make less human labor dependent on the processes used. Rent costs for commercial real estate properties in urban areas have increased at a much higher rate than revenue increases in major cities such as London, New York, and Sydney.

Opportunities: Expansion into underserved emerging urban markets and development of integrated digital ecosystem models present transformative growth opportunities for progressive cafe operators globally.

The potential for growth through underpenetrated emerging urban markets of South Asia, Southeast Asia, and Sub-Saharan Africa is by far the largest unexploited potential for growth among global cafe companies. The use of franchise and master franchises allows global brands to expand efficiently via partner financing and local management skills, without compromising quality standards. Digital opportunities include loyalty program monetization, subscription business models, and even delivery services which help create additional income sources outside of actual store locations. Starbucks Rewards contributes around 60% of the company’s total income in the U.S. due to its enrolled membership base, showcasing the true potential of loyalty program-based customer behavior patterns among progressive cafe chains in every market.

Recent Developments:

-

2025: Starbucks Corporation deployed its Siren System AI-powered beverage automation platform across North American flagship locations, reducing peak-hour order completion times by approximately 40% and improving per-location throughput capacity, directly addressing the operational bottlenecks constraining same-store sales performance across its highest-volume metropolitan markets.

-

2024: Luckin Coffee surpassed 20,000 total locations across China, becoming the world's largest coffee chain by outlet count and establishing its technology-first, app-exclusive ordering model as the dominant commercial format for affordable specialty coffee delivery in the Chinese market, attracting significant competitive response from international and domestic challenger brands.

-

2024: Dutch Bros Coffee exceeded USD 1.0 Billion in annual system revenue for the first time, demonstrating the commercial scalability of its drive-thru-only format and digital loyalty programme across the Western United States and validating its geographic expansion strategy into Southeast and Mid-Atlantic U.S. regional markets.

Cafe Market Key Players are:

-

Starbucks Corporation

-

Luckin Coffee Inc.

-

Dutch Bros Coffee

-

Costa Coffee (Coca-Cola Company)

-

Tim Hortons (Restaurant Brands International)

-

Dunkin' (Inspire Brands)

-

Peet's Coffee (JDE Peet's)

-

Blue Bottle Coffee (Nestle)

-

Caribou Coffee

-

Caffe Nero Group Ltd.

-

The Coffee Bean & Tea Leaf

-

Lavazza Group

-

Manner Coffee

-

Cafe Coffee Day (Coffee Day Enterprises)

-

Tata Starbucks Private Ltd.

-

Pret A Manger (JAB Holding Company)

-

Gloria Jean's Coffees

-

Intelligentsia Coffee

-

La Colombe Torrefaction Inc.

-

Second Cup Coffee Co.

Cafe Market Report Scope;

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 76.48 Billion |

| Market Size by 2035 | USD 128.74 Billion |

| CAGR | CAGR of 5.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Espresso-Based Beverages, Brewed Coffee, Cold Brew & Iced Coffee, Non-Coffee Beverages, Food Items & Bakery, Others) • By Ownership Type (Independent Cafes, Chain/Branded Cafes) • By Service Format (Dine-In, Takeaway & Drive-Thru, Delivery) • By Location Type (Standalone, Mall & Retail-Integrated, Travel & Transit-Integrated, Workplace & Campus) • By End User (General Consumers, Corporate & Office Workers, Students, Tourists & Travelers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Starbucks Corporation, Luckin Coffee Inc., Dutch Bros Coffee, Costa Coffee (Coca-Cola Company), Tim Hortons (Restaurant Brands International), Dunkin' (Inspire Brands), Peet's Coffee (JDE Peet's), Blue Bottle Coffee (Nestlé), Caribou Coffee, Caffè Nero Group Ltd., The Coffee Bean & Tea Leaf, Lavazza Group, Manner Coffee, Café Coffee Day (Coffee Day Enterprises), Tata Starbucks Private Ltd., Pret A Manger (JAB Holding Company), Gloria Jean’s Coffees, Intelligentsia Coffee, La Colombe Torrefaction Inc., Second Cup Coffee Co. |

Frequently Asked Questions

Europe dominated the Cafe Market in 2025, holding approximately 36.82% of global revenues, underpinned by the continent's deeply embedded coffee culture and consistently high per-capita consumption rates across Germany, Italy, France, and the United Kingdom.

Espresso-based beverages dominated the Cafe Market with 42.36% share in 2025.

Rising global coffee culture adoption across emerging urban economies, the repositioning of the cafe as a social and professional destination driven by hybrid working trends, specialty coffee premiumization, and digital loyalty programme integration are the primary growth factors sustaining the Cafe market through 2035.

The Cafe Market was valued at USD 76.48 Billion in 2025.

The Cafe Market is expected to grow at a CAGR of 5.34% from 2026 to 2035.

Get in Touch