Cancer Gene Therapy Market Report Scope & Overview:

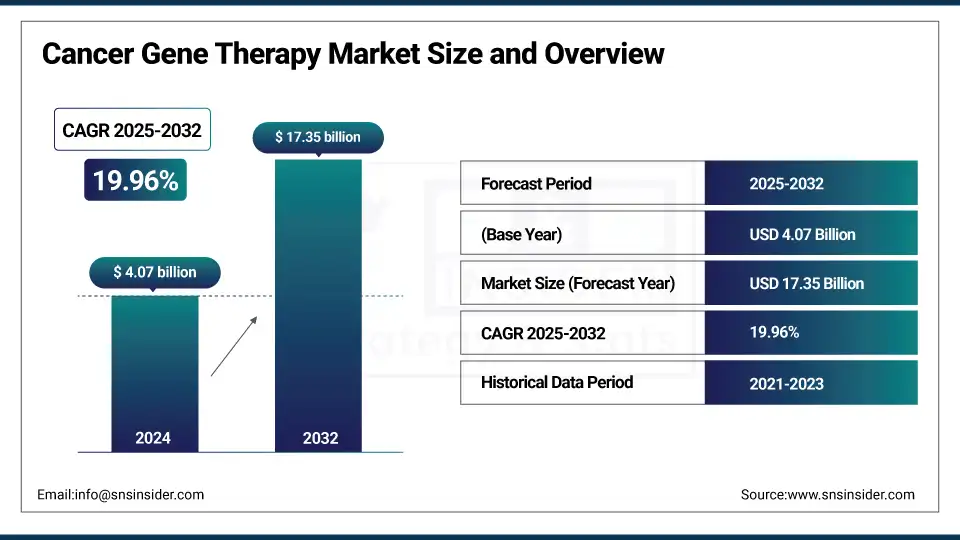

The Cancer Gene Therapy Market size was valued at USD 4.07 billion in 2024 and is expected to reach USD 17.35 billion by 2032, growing at a CAGR of 19.96% over the forecast period of 2025-2032.

The global cancer gene therapy market is growing rapidly due to the growing gene engineering research, the increasing number of approved CAR-T and other gene-targeted therapies, and the increasing global incidence of cancer. The movement toward precision medicine, coupled with its specific relevance to personalized cancer therapy, is rapidly expanding the gene-based treatment of hematologic malignancies. The cancer gene therapy market growth is also supported by ongoing clinical trials, possible strategic collaborations, and increasing capacity. The transformation of cancer therapy through gene therapy is just around the corner, with increasing regulatory support and advancements in gene delivery technologies.

Market Size and Forecast:

-

Market Size in 2024: USD 4.07 Billion

-

Market Size by 2032: USD 17.35 Billion

-

CAGR: 19.96% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

Cancer Gene Therapy Market Trends:

-

Rising global cancer prevalence is significantly driving demand for advanced and targeted gene-based therapies.

-

Increasing investments in biotechnology research and oncology-focused gene editing technologies are accelerating market growth.

-

Growing adoption of viral and non-viral vector platforms is improving treatment precision and therapeutic outcomes.

-

Expanding clinical trials pipeline and regulatory approvals for gene-modified immunotherapies are strengthening commercialization prospects.

-

Strategic collaborations between pharmaceutical companies, biotech firms, and research institutes are enhancing innovation and product development.

-

Advancements in CRISPR, CAR-T, and personalized medicine approaches are transforming the cancer treatment landscape and expanding long-term market potential.

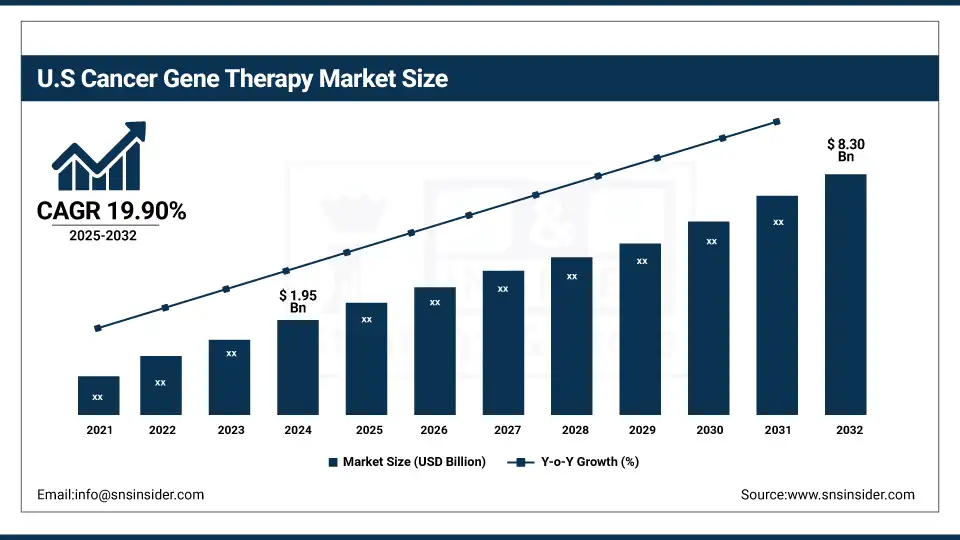

The U.S. cancer gene therapy market size was valued at USD 1.95 billion in 2024 and is expected to reach USD 8.30 billion by 2032, growing at a CAGR of 19.90% over the forecast period of 2025-2032.

North America cancer gene therapy market is led by the U.S., owing to better ecosystems for clinical trials, research & development higher number of key biotech and generic drug companies. It is the birthplace of multiple FDA-approved gene therapies and is well-funded through federal agencies such as the NIH and NCI, enabling further innovations and speed to market of new cancer gene therapies.

Cancer Gene Therapy Market Drivers:

-

Increase In the Incidence of Cancer Globally, Fuelling the Market Growth

The growing global incidence of cancer due to an aging population, environmental, and other risk factors related to lifestyle, has created a large market for new treatments. Traditional therapies (i.e., chemo and radiation) are limited by significant side effects and resistance. An emerging alternative is gene therapy, which has the potential to treat the underlying disease at the genetic level and may be a more precise and effective means of treatment. As a result, healthcare systems and biotech firms are pouring funds into gene-based solutions to combat this explosion in the prevalence of cancer.

According to WHO estimates in 2022, there were approximately 20 million new cases of cancer and 9.7 million cancer deaths. By this measure, an estimated 53.5 million people were alive within 5 years of a cancer diagnosis. One out of five people develops cancer within their lifetime, 1within 9 men and 1in 12 women die of the disease.

-

Advancements in Gene Editing and Vector Technologies are Accelerating the Market Growth

The invention of powerful gene editing tools such as CRISPR-Cas9 and TALENs, as well as enhanced viral vector systems including lentivirus and AAV, has enhanced the therapeutic promise of cancer gene therapy. Consequently, these innovations have enabled advances in specificity, safety, and stability for gene delivery, which can lead to more personalized and durable cancer therapies. This technological advancement is a key enabler for moving gene therapy use beyond rare cancers into common and more complex malignancies.

There are more than 100 CRISPR clinical trials, which have grown rapidly, as CRISPR Medicine News reported that a total of 98 were recorded worldwide by April 2025.

Cancer Gene Therapy Market Restraint:

-

High Cost of Treatment and Limited Accessibility Restraining the Market from Growth

High cost of treatment is one of the major limiting, restraining factors in the Cancer Gene Therapy Market. Certain gene therapies, such as CAR-T cell therapies, can range from USD 350,000 to more than USD 500,000 per patient, excluding the cost of hospital stays, supportive care, or other procedures. These are highly complicated to manufacture, often made to order for patients, which may require special facilities and highly skilled workers, all of which contribute to the cost. That means it is only available to well-heeled health systems in wealthy areas. Affordable prices and appropriate reimbursement frameworks for low- and middle-income countries are critically necessary to ensure patient access and grow the global market; lack of these critical enablers is raising several equity issues in cancer care.

Cancer Gene Therapy Market Segmentation Analysis:

By Indication

In 2024, the cancer gene therapy market share was led by the large B-cell lymphoma segment with a 54.26%, as a result of the successful launch and uptake of CAR-T cell therapies targeted against these indications. Therapies such as Yescarta and Breyanzi have demonstrated major clinical effectiveness and been approved by regulators in dozens of countries, resulting in their widespread utilization in relapsed or refractory settings. Moreover, the increasing availability of treatment facilities capable of delivering gene-based therapies and better reimbursement policies have further facilitated the adoption of these therapies in Large B-Cell Lymphoma.

During the forecast period, the other segment, which encompasses solid tumors, glioblastoma, pancreatic cancer, and other forms of malignancies, is expected to grow at the highest CAGR. Research expansion in the potential applications of gene therapy beyond hematological cancers is driving this growth, along with the increase in clinical trials and innovations in gene delivery systems, leading to increased competition among the major players during the considered period. Increasing interest in personalized and precision medicine is drawing companies to consider more novel vectors and gene-editing approaches for cancers thought to be untreatable or that have become resistant to all known therapies, which provides continued impetus for this diverse and dynamic segment of the commercial focus area.

By Route of Administration

In 2024, the Intravenous segment held the largest share of the cancer gene therapy market with 91.25% due to intravenous being the traditional and most prominent route of delivery for existing gene therapies, particularly CAR-T cell and viral vector-based therapies. This ensures fast introduction into the body, where the targeted cancer cells can be quickly populated with the new cells or genetic material. Hospital and oncology practices often favor IV delivery given its representable and clinically familiar performance coupled with the potential for finer control of dosing via infusion-based therapies. The intravenous segment is also expected to grow at the fastest pace during the forecast period; continuous advances in gene therapy have yet to sway the route of administration from IV, as the pipeline of new-generation therapies remains concentrated on this route. As more IV-administered gene therapies gain approvals and more infusion centers develop their infrastructures, the IV route is anticipated to grow rapidly both in developing and developed markets.

By Vector Type

Lentivirus segment dominated the cancer gene therapy market in 2024 with a 46.18% market share, as it has been the key technology for ex vivo gene therapies, particularly CAR-T cell therapies in hematologic cancers such as large B-cell lymphoma and acute lymphoblastic leukemia. Lentiviral vectors are preferred to deliver transgenes, as they can integrate stably in the host genome, allowing for long-lasting expression of therapeutic genes. Adenoviruses are the most commonly used vector type in current cancer gene therapy applications due to their safety profile, ability to carry large genetic payloads, and successful track record across multiple approved therapies.

The AAV segment is estimated to be the fastest-growing vector-based market during the forecast period, as innovators are targeting breakthroughs in solid tumors and in vivo gene therapy. They also exhibit low immunogenicity, the ability to infect dividing and non-dividing cells, and integration into the host genome is minimal, making AAV vectors safer for clinical purposes in the long term. As the need to directly target tumors becomes more and more present across a wide array of different cancer types, the increasingly significant and fast uptake of tumor-infiltrating T cell therapies in preclinical and clinical trials in more and more tissue types will lead to a broader range of cancer indications undergoing rapid development shortly.

By End User

The cancer research institute's segment dominated the cancer gene therapy market with a 74.5% market share due to that they are significant contributors to research in the advancement, testing, and science of natural and artificial cancer treatments. These institutes are first-movers in early-phase clinical trials, academia-industry synergies, and cancer translational research. Armed with state-of-the-art technologies, ample funding from both governmental and private sector sources, they become the poster children for CAR-T cell therapy, biomanufacturing, gene editing, and viral vector development, the leaders of the gene therapeutic ecosystem.

The others (hospitals and biotechnology companies) segment is predicted to grow at the highest CAGR during the forecast period due to the commercialization of approved gene therapies and hospital-based administration. Hospitals gear up for stores of compounding gene therapy; biotechs up production, speed clinical pipelines to late-stage. Increasing research-translational adoption, expanding reach to patients, and investment dollars for infrastructure and commercialization strategies will contribute to solid tumor growth as more gene therapies progress past research settings into mainstream cancer treatment.

Cancer Gene Therapy Market Regional Analysis:

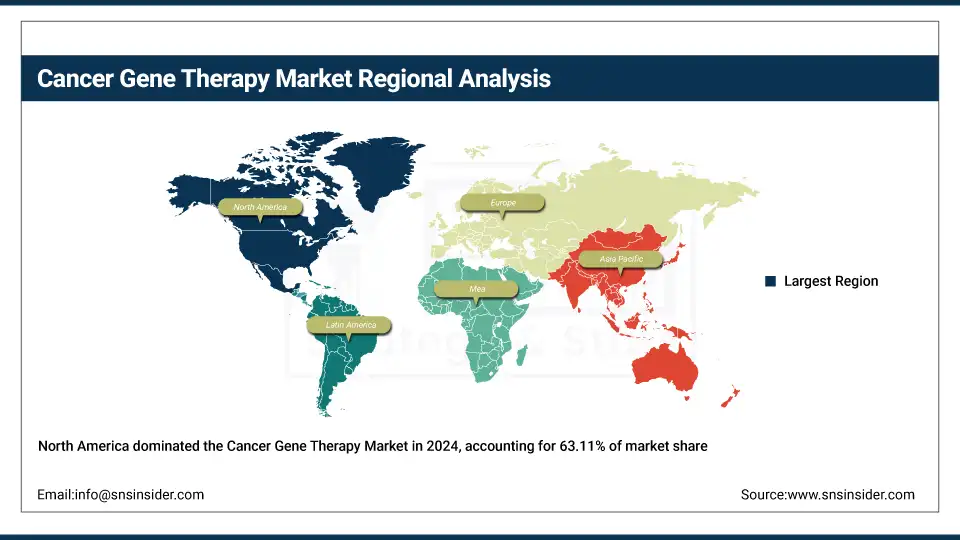

The cancer gene therapy market is dominated by North America, with 63.11% market share in 2024, driven by the highly evolved biotechnology ecosystem in this region, the presence of leading gene therapy developers, and early regulatory approvals of path-breaking therapies, including CAR-T cell therapies. This region benefits from significant public as well as private investment in precision oncology, strong clinical research infrastructure, and a high level of awareness among healthcare professionals and patients. The U.S. is helping the development of the ever-growing list of breakthrough therapies with fee-waived FDA-backed priority review, allowing a relatively rapid pathway to state-of-the-art commercialization and implementation of novel cancer gene therapies.

The cancer gene therapy market analysis in Asia Pacific is growing at a significant rate, followed by North America, as there is a large patient population growing rapidly, a high number of cancer cases are being registered, with high investment in genomics and biopharmaceuticals. Governments from countries such as China, Japan, and South Korea are building up their clinical trial infrastructure—and stimulating home-grown biotech innovation—through a combination of public funding and regulatory changes. As Asia Pacific continues to turn into a notable development center for cancer gene treatment arrangements, it is likely to benefit from expanded access to healthcare services, the developing recognition of precision medicine, and key coordinated efforts between the local and global players.

The cancer gene therapy market in Europe is growing substantially due to the most public–private research efforts, along with favorable regulatory agreements. Innovation is thus being encouraged, and the pace of gene-based cancer therapies is being accelerated thanks to various programs such as the European Union's Horizon Europe Mission on Cancer. Europe is a growing hub for the development of cancer gene therapy, generating a strong pipeline of applications through increasing numbers of clinical trials, broadening biomanufacturing capability, and partnerships between biotech companies and academic institutions.

The mission "Horizon Europe Mission on Cancer" was launched in Sept 2023 and includes an integrative research, public health, and citizen engagement approach towards translating cancer therapeutics innovation into the betterment of the lives of those affected by cancer.

Latin America, expected to experience moderate growth in the market. The cancer gene therapy market trends are due to the growing clinical trials in Latin America, which will gain better infrastructural access to medical resources and increase adoption of oncolytic virotherapy in this region, resulting in high growth prospects. The growth region is expected to grow at a moderate rate through the forecast period.

MEA is experiencing the gradual progression over the forecast period driven by investment into gene therapy platforms, manufacturing services, and domestic regulatory reform. Progressing through active market development, the leading markets such as South Africa, Saudi Arabia, and the UAE that were more concerned with segment-oriented testing are now more concentrated on oncology genomics and CAR-T.

Key Players

The cancer gene therapy market companies, OncoGenex Pharmaceuticals Inc., Merck KGaA, Introgen Therapeutics Inc., GSK plc (GlaxoSmithKline), GenVec, Genelux Corporation, Elevate Bio Inc., Celgene Inc., Bluebird Bio Inc., BioCancell Inc., and other players.

Recent Developments

-

May 2025 – Merck KGaA announced encouraging data from the clinic to justify its $85 million upfront investment in a late-phase tenosynovial giant cell tumor (TGCT) therapy; TGCT is a rare, locally aggressive tumor. As Merck gets primed to face off against Daiichi Sankyo and Ono Pharmaceutical over the TGCT treatment battleground, the data drop positions it.

-

January 2025 — GSK plc announced the acquisition of IDRx, Inc., a clinical-stage Boston-based biopharmaceutical company developing precision therapeutics for GISTs. The upfront consideration consists of an immediate cash payment of US$1 billion and a further USD150 million contingent on regulatory milestones being achieved. The acquisition gives GSK lead asset IDRX-42, a highly selective KIT TKI in development for first- and second-line GIST treatment.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.07 Billion |

| Market Size by 2032 | USD 17.35 Billion |

| CAGR | CAGR of 19.96% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Indication (Large B-Cell Lymphoma, Multiple Myeloma, Acute Lymphoblastic Leukemia (ALL), Melanoma (lesions), Others) • By Route of Administration (Intravenous, Others) • By Vector Type (Lentivirus, Retrovirus & Gamma Retrovirus, AAV, Modified Herpes Simplex Virus, Adenovirus, Others) • By End User (Cancer Research Institutes, Diagnostic Centers, Others [Hospitals and Biotechnology Companies]) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | OncoGenex Pharmaceuticals Inc., Merck KGaA, Introgen Therapeutics Inc., GSK plc (GlaxoSmithKline), GenVec, Genelux Corporation, Elevate Bio Inc., Celgene Inc., Bluebird Bio Inc., BioCancell Inc., and other players. |

Frequently Asked Questions

North America dominated the Cancer Gene Therapy Market in 2024.

The “Intravenous” segment dominated the Cancer Gene Therapy Market.

Advancements in gene editing and vector technologies are accelerating the market growth.

The Cancer Gene Therapy Market was USD 4.07 billion in 2024 and is expected to reach USD 17.35 billion by 2032.

The Cancer Gene Therapy Market is expected to grow at a CAGR of 19.96% from 2025 to 2032.

Get in Touch