IVD Contract Manufacturing Market Report Scope & Overview:

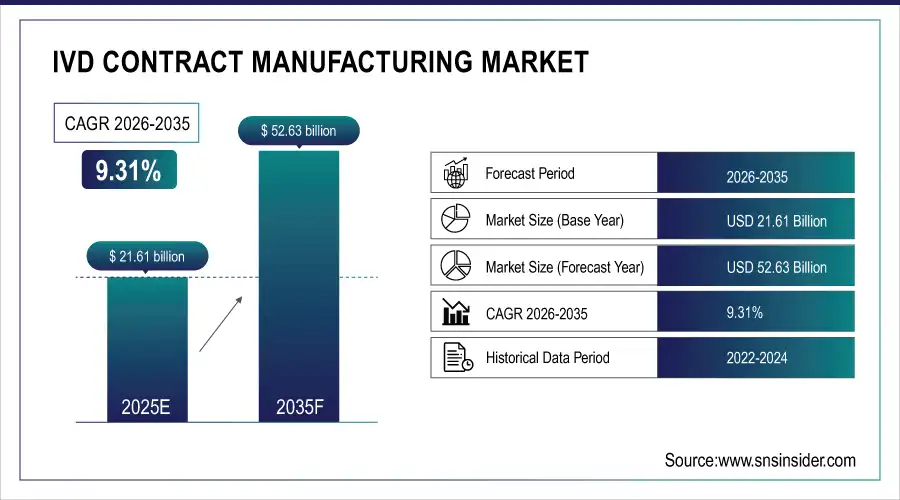

The IVD Contract Manufacturing Market was valued at USD 21.61 billion in 2025 and is expected to reach USD 52.63 billion by 2035, growing at a CAGR of 9.31% from 2026-2035.

IVD Contract Manufacturing Market is growing on account of rising In-vitro diagnostic products demand and upsurge in trend to outsource the production to specialized manufacturers. The growth in the market is attributed to the need for cost-effective and time-saving diagnostic solutions as well as increasing prevalence of infectious diseases. Automation, quality control and regulatory compliance continue to improve in a highly fragmented market as the incidence of chronic disease and infection grows in healthcare and diagnostics, driving increased adoption of contract manufacturing services.

In 2024, global IVD contract manufacturing grew by 16%, with 60% of diagnostic firms outsourcing production to cut costs by 25% and accelerate launch timelines by 35%, fueled by rising chronic and infectious disease testing needs.

IVD Contract Manufacturing Market Size and Forecast

-

Market Size in 2025: USD 21.61 Billion

-

Market Size by 2035: USD 52.63 Billion

-

CAGR: 9.31% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On IVD Contract Manufacturing Market - Request Free Sample Report

IVD Contract Manufacturing Market Trends

-

Growing outsourcing of assay development and instrument production as IVD companies prioritize faster commercialization and reduced internal manufacturing burden

-

Rising demand for customized reagent formulation and bulk consumables driven by expansion of molecular diagnostics and point-of-care testing

-

Increasing adoption of automation and robotics in contract facilities to support high-volume, precision-driven diagnostic manufacturing workflows

-

Expansion of OEM partnerships for end-to-end services, including design, prototyping, validation, regulatory support, and scalable production

-

High focus on quality management and regulatory compliance as global manufacturers align with evolving FDA and IVDR requirements

-

Growth of contract manufacturing for infectious disease, oncology, and genetic testing owing to increased clinical testing volumes

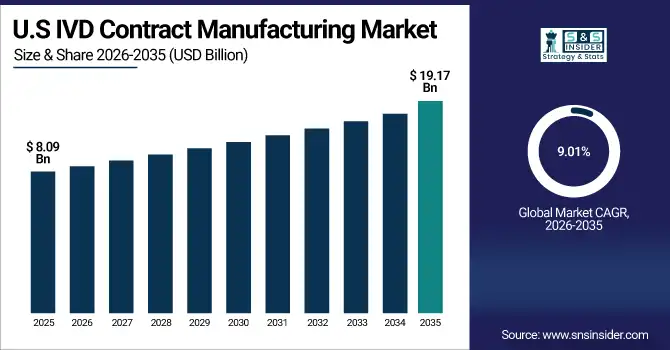

The U.S. IVD Contract Manufacturing Market was valued at USD 8.09 billion in 2025 and is expected to reach USD 19.17 billion by 2035, growing at a CAGR of 9.01% from 2026-2035.

Growth in the U.S. IVD Contract Manufacturing Market is driven by increasing demand for in vitro diagnostic products and the outsourcing of manufacturing to reduce costs and accelerate time-to-market. Advancements in automation, quality standards, and rising prevalence of chronic and infectious diseases are further supporting market expansion.

IVD Contract Manufacturing Market Growth Drivers:

-

Rising demand for diagnostic tests and increasing outsourcing by IVD companies to reduce development costs and accelerate time-to-market are driving contract manufacturing growth

Global demand for diagnostic testing – including infectious diseases, chronic care and preventive screening – has driven many IVD manufacturers to rely on outsourced partners. Contract manufacturing enables companies to lower operational expenses, simplify product development and expedite regulatory pathways. With increasing demand to bring new tests and instruments quickly to market, outsourcing enables scalability as well as access to core technologies and efficient manufacturing. This model allows IVD developers to concentrate on their technology core such as R&D and commercialization while outsourcing high precision manufacturing from the specialists, boosting global market expansion.

In 2024, over 55% of IVD companies increased outsourcing to contract manufacturers, reducing development costs by up to 25% and cutting time-to-market by 35% amid surging global diagnostic test demand.

-

Growing prevalence of chronic and infectious diseases worldwide is boosting production of reagents, consumables, and analyzers through specialized IVD contract manufacturers

The worldwide increasing demand for diagnostic testing (in particular infectious diseases, chronic illness and prophylactic screening) has driven the IVD industry to increase its dependency on partners external to their own operations. Outsourced manufacturing allows companies to save on overhead costs, expedite product development time frames and drive down regulatory timelines. With the increasing pressure to bring new test kits and instruments to market quickly, outsourcing provides scale, access to specialist technologies and high-performance manufacturing. This collaborative approach empowers IVD developers to concentrate on what they do best – such as R&D and commercialization – leaving high-precision manufacturing to the experts, further driving increased market growth around world.

More than 55% IVD companies had scaled up outsourcing to contract manufacturers in 2024, slashing development costs by 25% and shortening time-to-market by 35% as the global demand for diagnostic tests skyrocketed.

IVD Contract Manufacturing Market Restraints:

-

Strict regulatory approvals, complex compliance requirements, and frequent quality audits increase operational challenges and time delays for IVD contract manufacturers

IVD production works under strict regulatory affairs regulations (FDA, EU IVDR etc.), for local and national standards. In addition to that due diligence compliance further including meticulous documentation, validation, audits and ongoing quality control all of which is while adding complications and more importantly contributing to higher cost and longer lead times. The restrictions also extend product development timelines and require large investments in expertise to navigate regulatory requirements as well as facility improvements. Failure to act on time or non-compliance with these requirements can result in the recall of goods or refusal of approval which negatively affects profitability. As a result, the regulatory burden serves as a major impediment for manufacturers and delays entry for smaller companies

In 2024, 70% of IVD contract manufacturers faced delays of 4 months due to stringent regulatory reviews, with compliance and audit-related costs consuming up to 25% of operational budgets globally.

-

High capital investment in advanced manufacturing facilities and skilled workforce limits market entry and expansion for small and mid-sized manufacturers

To manufacture IVDs, you need expensive equipment, clean-room facilities, precision robotics and biologically-trained personnel to ensure accuracy and compliance with regulatory requirements. Construction and upkeep of such infrastructure require enormous capital investment, something not easily affordable by small and medium enterprises. Furthermore, international competition and the continual demand for technological modernization add more pressure on financial resources. Smaller companies find it impossible to obtain the big contracts without a huge investment which is restricting them from growing and being market players. This hurdle benefits the free players and dampens industry variety.

In 2024, over 50% of small and mid-sized IVD manufacturers cited capital costs exceeding USD10 million for advanced facilities and shortages of skilled labor as key barriers to scaling or entering the market.

IVD Contract Manufacturing Market Opportunities:

-

Rising adoption of molecular diagnostics, point-of-care testing, and personalized medicine creates new opportunities for specialized IVD contract manufacturing services

Genomic profiling, rapid diagnostics and decentralized testing have opened up strong growth prospects for contract manufacturers catering to the next-generation technology sector. In the era of molecular diagnosis and personalized medicine, high precision production is necessary for manufacturing patient specific reagents and devices. Point-of-care devices also require small, simple-to-use systems with rapid turn-around times. IVD companies specialized in microfluidics technologies sensitive to biomarker detection, assay development, and multiplex testing are the ones that stand best chances to develop longer-term partnerships. The demand is increasing due to the trend of health care systems becoming focused on early detection, remote monitoring and preventative treatment.

In 2024, 60% of IVD contract manufacturers expanded capabilities in molecular and POC diagnostics, with demand for personalized medicine driving a 35% increase in specialized outsourcing partnerships globally.

-

Growing demand for automation, smart manufacturing, and digital quality control enables IVD manufacturers to scale globally and improve production efficiency

Artificial intelligence process monitoring, robotics, IoT equipment tracking and digitized batch record systems are all modernizing IVD manufacturing. These solutions address the need for increased accuracy, to minimize manual errors and expedite regulatory documentation at lower business costs. Automation also makes it possible to quickly ramp up manufacturing as the demand for healthcare surges and plummets back down around the world particularly for high-volume consumables and rapid diagnostic kits. Digital networks bring traceability closer and help to automate prediction maintenance and supply chain management. And with diagnostic companies looking for cost-effective, high-throughput partners, contract manufacturers that are employing the latest automation have some clear competitive advantages.

In 2024, 65% of IVD manufacturers invested in smart manufacturing, achieving 30% higher production efficiency and 25% faster time-to-market through automated, AI-driven quality control and digital workflow integration.

IVD Contract Manufacturing Market Segment Highlights

-

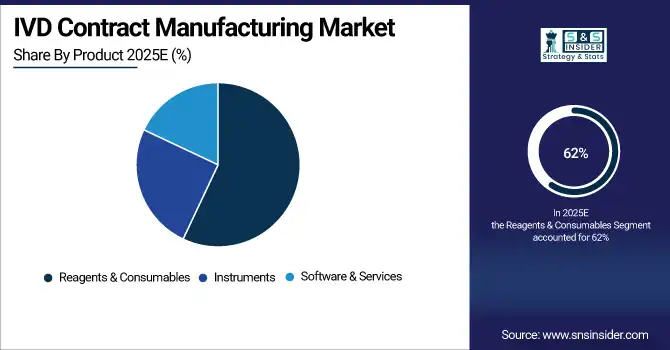

By Product: In 2025, Reagents & Consumables dominated the market with 62% share, while Software & Services is projected to grow at the fastest CAGR from 2026–2035.

-

By Service: In 2025, Manufacturing Services dominated the market with 68% share, while Assay Development Services is projected to grow at the fastest CAGR from 2026–2035.

-

By Technology: In 2025, Immunoassays dominated the market with 32% share, while Molecular Diagnostics is projected to grow at the fastest CAGR from 2026–2035.

-

By End-use: In 2025, Medical Device Companies dominated the market with 78% share, while Others (Startups/New Entrants) is projected to grow at the fastest CAGR from 2026–2035.

IVD Contract Manufacturing Market Segment Analysis

By Product: Reagents & Consumables segment led in 2025; Software & Services segment expected fastest growth 2026–2035

Reagents & Consumables segment dominated the IVD Contract Manufacturing Market with the highest revenue share of about 62% in 2025 due to their constant demand in diagnostic testing, high-volume clinical applications, and recurring replenishment needs. The rise in infectious disease testing, routine lab-based diagnostics and the importance of high-quality consumables to ensure accuracy of an assay have strengthened the segment’s position across the global IVD manufacturing value chain.

Software & Services market to register the highest CAGR from 2026-2035 The Software & Services segment is projected to grow at the highest CAGR during this period, primarily due to growing digital diagnostics and increasing adoption of cloud-based data storage systems and laboratory automation. Demand is also being fuelled by the integration of advanced analytics, AI-powered workflows and remote diagnostic monitoring solutions. In addition, the growing focus on smart labs, efficiency of workflows and IVD platforms interoperability is leading to a considerable market expansion in this segment.

By Service: Manufacturing Services segment led in 2025; Assay Development Services segment expected fastest growth 2026–2035

Based on Service Type, the IVD Contract Manufacturing Market was acquired the largest market share for manufacturing services, contributing to a 68% share of revenue in 2025 as diagnostic companies are increasingly looking for scalable and cost-effective production through outsourcing. Regulatory compliance, technical knowledge and high-volume manufacturing expertise provided by contract manufacturers help the international IVD companies streamline operations, cut down on operating expenses and efficiently meet the increased demands for diagnostics.

The Assay Development Services segment is projected to register the highest CAGR from 2026-2035 owing to the growing need for tailor-made biomarker-based tests, rapid disease screening systems, and personalized medicine. Increasing R&D investments, the advent of new pathogens, and collaborations for novel assay development are driving growth, so that assay development now ranks among IVD contracting’s most crucial and rapidly developing segments.

By Technology: Immunoassays segment led in 2025; Molecular Diagnostics segment expected fastest growth 2026–2035

Immunoassays was a leading segment in 2025 owing to broad applications such as infectious diseases, oncology, autoimmune disorders and chronic disease diagnostics. High sensitivity, reproducibility and the availability of manufacture in routine laboratory testing have maintained these their market position and diagnostic laboratories consistently prefer to use them worldwide.

Molecular Diagnostics is projected to gain the fastest CAGR from 2026-2035 owing to increased deployment of PCR, next-generation sequencing and gene testing in early disease diagnosis and precision medicine. Molecular diagnostic contract manufacturing solutions are increasingly being used in oncology as well as infectious disease testing and personalized medicine applications, which is driving the demand for them across all markets globally.

By End-use: Medical Device Companies segment led in 2025; Others (Startups/New Entrants) segment expected fastest growth 2026–2035

Medical Device Companies segment dominated the IVD Contract Manufacturing Market with the highest revenue share of about 78% in 2025 due to large-scale outsourcing by major diagnostic manufacturers. Outsourcing allows these organisations to lower costs, get to market quickly and remain compliant with complex regulatory requirements. Contract manufacturer services have seen the strongest demand as requirements for high-volume production and multiple products continue to maintain their leadership role.

Startups/New Entrants) segment is expected to witness the highest CAGR during 2026-2035 primarily due to rising trend of outsourcing by research laboratories, biotech start-ups and academic institute. The IVD services segment in this market is the highest growing segment due to its limited in-house manufacturing capabilities, requirement for newer and innovative diagnostic products in hospitals & clinical laboratories, and increasing preference for special endeavors.

IVD Contract Manufacturing Market Regional Analysis

North America IVD Contract Manufacturing Market Insights

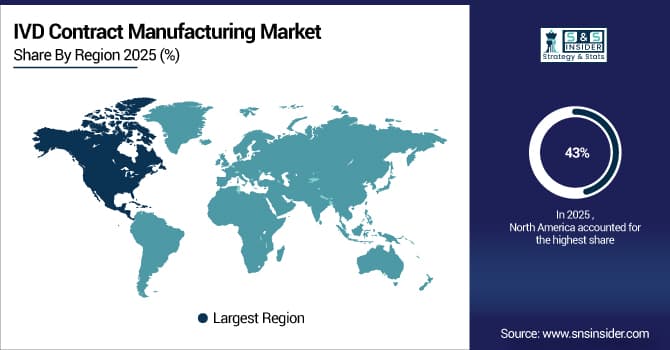

North America dominated the IVD Contract Manufacturing Market with a 43% share in 2025 due to the presence of leading in vitro diagnostic manufacturers, advanced healthcare infrastructure, and high adoption of outsourced manufacturing solutions. Strong R&D capabilities, favorable regulatory support, and growing demand for diagnostic tests further reinforced the region’s market leadership.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific IVD Contract Manufacturing Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 11.36% from 2026–2035, driven by rising demand for affordable diagnostic solutions, expanding healthcare infrastructure, and increasing prevalence of chronic and infectious diseases. Growing investments in IVD manufacturing facilities, favorable government initiatives, and expanding medical device outsourcing trends accelerate market growth across the region.

Europe IVD Contract Manufacturing Market Insights

Europe held a significant share in the IVD Contract Manufacturing Market in 2025, supported by a strong presence of established diagnostic companies, advanced healthcare infrastructure, and well-regulated manufacturing standards. High adoption of outsourced production, ongoing R&D in innovative diagnostic assays, and growing demand for high-quality IVD products further strengthened Europe’s market position.

Middle East & Africa and Latin America IVD Contract Manufacturing Market Insights

The Middle East & Africa and Latin America together showed steady growth in the IVD Contract Manufacturing Market in 2025, driven by expanding healthcare infrastructure, rising prevalence of chronic and infectious diseases, and growing demand for affordable diagnostic solutions. Increasing outsourcing of IVD production, government support, and investments in medical technology further strengthened the regions’ emerging market presence.

IVD Contract Manufacturing Market Competitive Landscape:

TCS Biosciences Ltd.

TCS Biosciences Ltd is a UK based company that manufactures high quality biological products, reagents and kits for the IVD and Life Science markets. The company offers a portfolio of contract manufacturing offerings including assay development, reagent supply and quality testing capabilities supporting global IVD companies. TCS Biosciences is recognized for its high quality which is supported by compliance with regulations and efficient large scale manufacturing. Its offerings are designed for small biotech companies as well as global multinational IVD corporations looking for trusted production partners.

-

2024, TCS Biosciences launched “TCS Rapid Path”, a CE-marked point-of-care immunoassay platform for infectious disease testing (including RSV, influenza, and SARS-CoV-2) that delivers lab-quality results in under 15 minutes using a single drop of whole blood.

Invetech Inc.

Invetech Inc., from US, is a premier automation and contract manufacturing solution provider for in-vitro diagnostics (IVD) market. The company excels in design of instruments and high-throughput automation, with capabilities in device assembly as well – all under one masterful engine to bring end-to-end manufacturing solutions, applying engineering acumen and regulatory understanding. Invetech works closely with IVD developers to simplify manufacturing, improve productivity and reduce time to market. The company’s reputation for innovation, flexibility and value makes it a preferred partner with diagnostic manufacturers across the globe.

-

2025, Invetech announced the launch of “Invetech Flex Cell”, a modular, GMP-compliant cell therapy manufacturing platform designed for decentralized production of CAR-T and regenerative medicines. The system supports closed, automated workflows for academic medical centers and biotech’s with limited cleanroom space.

Bio-Techne Corp.

About Bio-Techne Corporation Bio-Techne Corporation is a leading global life sciences company providing innovative tools and bioactive reagents for the research and clinical diagnostic communities. The Company offers custom assay and antibody development, as well as bulk protein production for both the academic and CRO markets in compliance with GLP/cGMP. Leveraging innovative manufacturing capabilities and years of industry experience, Bio-Techne helps IVD manufacturers provide dependable diagnostic products. With global reach and technical proficiency, it is the #1 partner of choice across the world for companies who want pioneering and reliable diagnostic solutions.

-

2023, Bio-Techne released "Simple Western Auto", a capillary-based immunoassay system that automates the testing process; providing quantitative results with 90% less sample volume than traditional methods such as Western blot. The platform is intended for biopharma QC and research laboratories.

IVD Contract Manufacturing Market Key Players

Some of the IVD Contract Manufacturing Market Companies are:

-

Thermo Fisher Scientific

-

Jabil Inc.

-

Sanmina Corporation

-

TE Connectivity Ltd.

-

Celestica Inc.

-

West Pharmaceutical Services Inc.

-

Merck KGaA

-

Savyon Diagnostics

-

TCS Biosciences Ltd.

-

Invetech Inc.

-

Bio-Techne Corp.

-

Nova Biomedical

-

Cone Bioproducts

-

Maxim Biomedical Inc.

-

Avioq Inc.

-

Meridian Bioscience Inc.

-

Coris BioConcept

-

Cenogenics Corporation

-

KMC Systems Inc.

-

Fujirebio

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.61 Billion |

| Market Size by 2035 | USD 52.63 Billion |

| CAGR | CAGR of 9.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Instruments, Reagents & Consumables, Software & Services) • By Service (Manufacturing Services, Assay Development Services, Other Services) • By Technology (Immunoassays, Clinical Chemistry, Molecular Diagnostics, Hematology, Microbiology, Coagulation, Others) • By End-use (Medical Device Companies, Academic & Research Institutions, Others (Startups/New Entrants)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific, Jabil Inc., Sanmina Corporation, TE Connectivity Ltd., Celestica Inc., West Pharmaceutical Services Inc., Merck KGaA, Savyon Diagnostics, TCS Biosciences Ltd., Invetech Inc., Bio-Techne Corp., Nova Biomedical, Cone Bioproducts, Maxim Biomedical Inc., Avioq Inc., Meridian Bioscience Inc., Coris BioConcept, Cenogenics Corporation, KMC Systems Inc., Fujirebio |

Frequently Asked Questions

North America dominated the IVD Contract Manufacturing Market in 2025 with a 43% share due to advanced infrastructure, leading manufacturers, and high outsourcing adoption.

In 2025, Reagents & Consumables segment dominated the IVD Contract Manufacturing Market.

Growth is driven by rising demand for diagnostic tests, outsourcing to reduce costs, faster commercialization, and technological advancements in manufacturing.

The IVD Contract Manufacturing Market was valued at USD 21.61 billion in 2025, supported by rising diagnostic outsourcing and chronic disease testing.

The IVD Contract Manufacturing Market is projected to grow at a CAGR of 9.31% from 2026 to 2035, driven by outsourcing trends.

Get in Touch