Card Random Number Generator Market Report Scope & Overview:

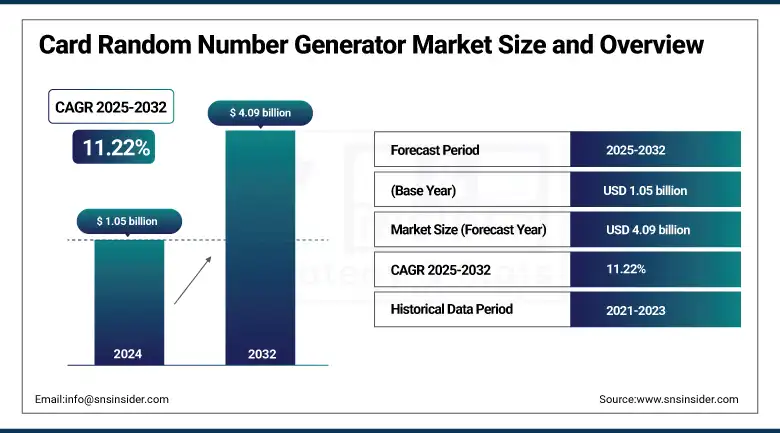

The Card Random Number Generator Market size was valued at USD 1.05 billion in 2024 and is expected to reach USD 4.09 billion by 2032, expanding at a CAGR of 11.22% over the forecast period of 2025-2032.

The Card RNG Market has been gradually rising, given the demand for secure and unbiased random number generation, especially in online gaming, cryptography, and simulations. Hardware RNGs are secure, but software RNGs are flexible and easy to integrate. Market usage is mainly in the gaming sector, led by global casinos and lottery systems, as well as financial institutions and research organizations centered on secure data processing. North America is prominent in the market, owing to mature technology and legislation, while Asia Pacific is the fastest-growing region. The rise of digital transactions combined with the same old concerns about cybersecurity is expected to drive more adoption of RNG, enabled by advancements in both AI and quantum RNG technologies.

According to research, RNG-certified platforms report a 37% reduction in player disputes due to fairer game outcomes, while over 72% of fintech encryption systems in 2024 relied on hardware RNGs, boosting cryptographic strength by 40% compared to pseudo-random alternatives.

To Get more information On Card Random Number Generator Market - Request Free Sample Report

The U.S Card Random Number Generator Market size reached USD XX billion in 2024 and is expected to reach USD XX billion in 2032 at a CAGR of XX% from 2025 to 2032.

The U.S. dominates the Card Random Number Generator (RNG) Market, because it has a very sophisticated technological structure and is a major center for key RNG solution providers, not to mention that both gaming and financial sectors are also well-established in the region, which highly depend on secure number generation systems. Meeting Market Needs The call for digital gaming platforms, the regulation slice of online gambling and growing fears of cybersecurity in finance are the fundamental drivers for growth across the marketplace. Companies in the U.S. have always led the world when it comes to hardware and software innovations in RNG, and continued advances in areas such as artificial intelligence (AI), cryptographic security, and quantum computing will further fuel this space.

Market Dynamics

Drivers:

-

Increasing Adoption of RNGs in Cryptography and Digital Transactions Drives Industry Expansion Globally.

With the increasing demand for strong encryption in financial services, e-commerce, and blockchain technologies, demand for card-based RNGs is expected to drive market growth. It guarantees the secure generation of keys and their authentication in a digital environment. For example, the U.S. and European financial sectors is now utilizing hardware RNGs to increase security and reduce data breaches. For example, in 2024, Infineon and Microchip Technology commercialized RNG integration into secure microcontrollers to fulfill cryptographic standards like FIPS 140-3.

-

Over 80% of the top 50 global fintech companies had adopted hardware RNGs in transaction encryption, up from just 55% in 2021.

-

Financial institutions that deployed hardware RNGs reported a 38% reduction in successful cyberattacks on encrypted data in 2023.

Restraints:

-

High Implementation Costs and Limited Awareness in Emerging Markets Hinder Widespread Technology Deployment.

Despite their growing significance in cybersecurity and gaming, card RNG solutions remain underutilized in several developing regions. High costs associated with secure hardware modules and limited technical expertise are barriers to adoption. Small and mid-sized enterprises often opt for less secure software-based alternatives. Additionally, awareness regarding the role of RNGs in securing digital assets is relatively low outside mature economies. Without broader education and cost-efficient offerings, market penetration in regions like Africa and parts of Southeast Asia remains limited.

Opportunities:

-

Rising Integration of RNGs in Quantum-Resistant Encryption Offers Significant Growth Potential for Technology Vendors.

As concerns about quantum computing’s ability to break current encryption systems grow, demand for quantum-resistant security is surging. This has led to the increasing adoption of high-quality RNGs as core components in next-generation cryptographic protocols. In 2025, Rambus and ID Quantique introduced RNG-enabled solutions designed to meet post-quantum cryptographic standards. Enterprises and governments are now prioritizing RNG infrastructure that aligns with emerging NIST guidelines for post-quantum cryptography.

Challenges:

-

Difficulty in Validating True Randomness and Ensuring Regulatory Compliance Challenges Market Expansion Efforts.

One of the core challenges facing the RNG industry is validating the authenticity of “true” randomness, especially in hardware solutions. Regulatory bodies demand compliance with stringent standards like NIST SP 800-90B, FIPS 140-3, and ISO/IEC 18031. Ensuring compliance while maintaining performance and low latency is complex and resource-intensive. Additionally, improper implementation of entropy sources or poorly validated algorithms can introduce vulnerabilities. The lack of uniform global standards also creates confusion among developers and delays certification processes.

Segment Analysis

By Application

The gaming segment led with 12.22% revenue share in 2024, driven by demand for fairness and unpredictability in digital card-based games. Companies like Light & Wonder and Playtech integrated certified RNG engines to enhance trust in online poker and slot games. Regulatory compliance, immersive experiences, and anti-cheating mechanisms are major drivers. RNG technology ensures fair draws, making it indispensable in digital gaming environments within the Card RNG Market.

The influencer management segment is rapidly expanding with a projected CAGR of 23.84%, as brands and creators adopt gamified campaigns. RNG is used for random winner selection, loyalty draws, and contest mechanisms. Platforms like Upfluence and CreatorIQ are launching plugins that integrate secure randomization for engagement transparency. The rise of social commerce, demand for unbiased reward distribution, and content gamification are driving RNG adoption in influencer ecosystems.

By Type

Hardware RNG dominated the market with 64.72% revenue share in 2024, owing to its true randomness and physical entropy sources ideal for secure systems. Firms like ID Quantique and Microchip Technology released advanced quantum RNG chips embedded in secure modules. Key drivers include increased cybersecurity concerns, regulatory standards, and usage in high-stakes card gaming systems. Hardware RNG ensures unmanipulated outcomes, essential in regulated and cryptographic card-based operations.

Software RNG is projected to grow at a CAGR of 12.03%, driven by its cost-effectiveness, integration ease, and flexibility. Cloud-based platforms like Random.org and Google’s RNG API have been enhancing APIs for gaming, education, and promotional use. Mobile-first applications and digital marketing tools are major adopters. Drivers include rapid deployment, demand from SMEs, and the need for scalable, software-based randomness in the Card RNG Market.

By End User

Financial institutions held the highest share at 30.37% in 2024, using RNGs for encryption, PIN generation, and secure authentication. Vendors like Thales, Entrust, and Utimaco launched RNG-enabled HSMs to support banking-grade security. Drivers include growing fraud, zero-trust frameworks, and regulatory compliance like FIPS 140-3. In the Card RNG Market, RNGs are vital for generating cryptographic keys and ensuring non-deterministic operations in financial systems.

Online gaming platforms are growing fastest with a CAGR of 12.27%, fueled by demand for secure, fair gameplay. Platforms like DraftKings and Stake.com integrate third-party RNGs for verified card shuffling and draw mechanics. Drivers include rising mobile gaming, global betting legalization, and transparency requirements. RNGs form the backbone of online card games, ensuring integrity and randomness that meet gaming authority regulations globally.

Regional Analysis

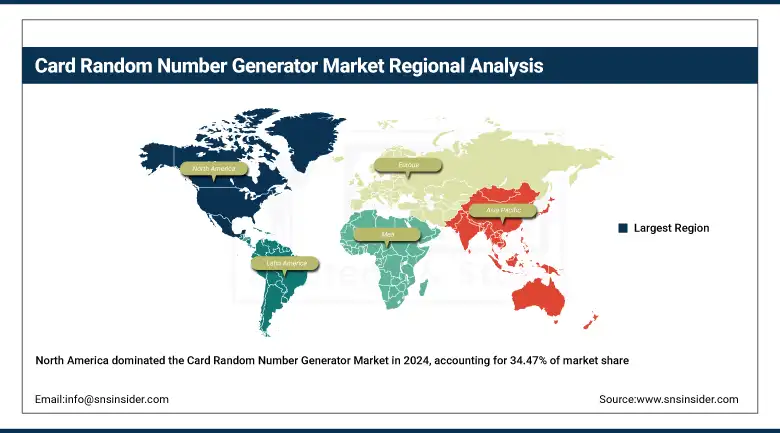

North America dominated the global Non-Terrestrial Network Market, accounting for approximately 34.47% of the total market revenue. The region’s leadership is driven by major satellite deployments, advanced 5G integration trials, and robust public-private partnerships. Companies like SpaceX and AST SpaceMobile have expanded satellite-based broadband and mobile connectivity, benefiting from the region’s mature telecom and aerospace ecosystems. The United States leads North America due to its substantial investment in LEO satellite constellations, government-led space programs, and active private-sector participation in global NTN infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe contributed a significant portion to the market in 2024, backed by government initiatives and regulatory frameworks supporting satellite communication and 5G backhaul solutions. With a focus on bridging connectivity gaps in remote and maritime zones, European nations are collaborating on space and digital strategies through the European Space Agency and national efforts. Germany emerged as the dominant country in Europe, driven by its advanced aerospace R&D, investment in industrial digitalization, and leadership in cross-border NTN pilot programs.

Asia Pacific represented the fastest-growing region in the Non-Terrestrial Network Market in 2024, with a remarkable market share of 30.61%. Rapid urbanization, high mobile penetration, and the need for rural internet access have spurred satellite deployment and innovation across China, India, and Japan. China holds the leading position in Asia Pacific due to state-funded satellite networks, its Belt and Road digital expansion, and a robust national policy pushing NTN integration across public infrastructure and defense.

The Middle East & Africa and Latin America regions demonstrated steady adoption of non-terrestrial network solutions, focusing on bridging connectivity gaps in remote and underserved areas. The UAE led MEA with strategic satellite initiatives like Thuraya, while Brazil dominated Latin America through national satellite programs and global partnerships aimed at expanding rural broadband and digital services.

Key Players

The major key players of the Card Random Number Generator Market are Microchip Technology Inc., Texas Instruments Incorporated, NXP Semiconductors, STMicroelectronics, Analog Devices, Inc., Infineon Technologies AG, Renesas Electronics Corporation, ON Semiconductor, Qualcomm Technologies, Inc., Intel Corporation, and others.

Key Developments

-

In November 2024, Infineon Technologies partnered with Quantinuum to enhance encryption through Quantum Random Number Generators (QRNGs), strengthening cryptographic security in financial and identity-based applications and advancing secure data solutions within quantum computing frameworks.

-

In May 2025, Elmos Semiconductor and ID Quantique launched a compact 2×2 mm quantum RNG chip featuring in-chip photoemission, designed to deliver enhanced entropy for secure communications across automotive, IoT, and other high-security application environments.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 12.96 Billion |

| Market Size by 2032 | USD 35.84 Billion |

| CAGR | CAGR of 13.56% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Software, Services) •By Application (Healthcare, Automotive, Retail, Security and Surveillance, Manufacturing, Others) •By Deployment Mode (On-Premises, Cloud) •By Enterprise Size (Small and Medium Enterprises, Large Enterprises) •By End-User (BFSI, Healthcare, Retail, Automotive, Manufacturing, IT and Telecommunications, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Google LLC, Microsoft Corporation, Amazon Web Services, Inc., IBM Corporation, Intel Corporation, NVIDIA Corporation, Qualcomm Technologies, Inc., Cognex Corporation, Basler AG, Keyence Corporation |

Frequently Asked Questions

North America dominated the Card Random Number Generator Market in 2024, owing to its mature technological infrastructure, regulatory compliance, and a high concentration of key RNG solution providers

The Hardware RNG segment dominated the Card Random Number Generator Market, accounting for the highest revenue share in 2024 due to its physical entropy sources and true randomness.

A major growth factor is the increasing adoption of RNGs in cryptography and digital transactions, driven by growing cybersecurity needs in financial services, blockchain, and online gaming ecosystems.

The market size of the Card Random Number Generator Market was USD 1.05 billion in 2024.

The expected CAGR of the Card Random Number Generator Market over the forecast period of 2025 to 2032 is 11.22%.

Get in Touch