Chip-on-Bord LED Market Report Scope & Overview:

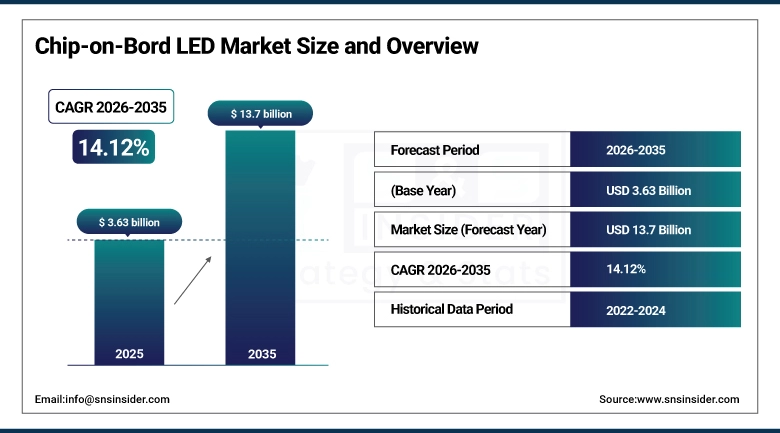

The Chip-on-Board (COB) LED Market was valued at USD 3.63 billion in 2025 and is expected to reach USD 13.7 billion by 2035, growing at a CAGR of 14.12% from 2026–2035.

Technology of COB (Chip-on-Board) LED uses direct placement of many LEDs on the substrate materials (mainly, ceramic or metal core PCBs) where no encapsulation process is required. This leads to improved light source that produces high brightness light along with better heat dissipation compared to conventional LED with its packaging. These LEDs work efficiently because of their higher lumen-per-square-millimeters capacity, better color consistency because of phosphors coating and improved thermal efficiency due to absence of any packaging layers in between the LED chips and the substrates. COB LEDs have become popular for use in high-lumen and long-life applications like commercial downlights, track lights, car head lights, stadiums, and plant growth lights. The worldwide trend toward energy efficiency in lighting, intelligent city lighting systems, and electric cars is creating favorable structural tailwinds for COB LEDs. The luminous efficacy of COB LEDs ranges from 100 to more than 200 lumens per watt, depending on the technology generation and product quality, putting them among the most efficient light sources in the white light spectrum currently available. Additionally, the small size and singularity of the optical source in COB LEDs allow for easier design freedom in the optics system compared to traditional multi-die solutions.

Automotive applications represent the largest growth area for COB LEDs, thanks to the replacement of traditional halogen and HID headlights with all-LED front lights. An advanced LED headlight assembly can feature more than one COB LED package, depending on their wattage levels, in order to perform different tasks. COB LEDs have also been adopted in automotive cabin lighting, where precise color rendering and dimming functionality are required.

Market Size and Forecast

-

Market Size in 2025: USD 3.63 Billion

-

Market Size by 2035: USD 13.7 Billion

-

CAGR: 14.12% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Chip-on-Board (COB) LED Market - Request Free Sample Report

Market Trends

-

COB retrofit opportunities where metal halide lamps are replaced by COB LED systems for efficiency and lower maintenance costs.

-

Growing use of COB LED automotive headlamps from high-end cars to mid and lower-end cars, increasing the number of COB LED automotive headlamps.

-

Increasing requirement of light sources for horticulture applications requiring adjustable spectrums for optimized plant growth.

-

High-intelligence COB LED systems equipped with embedded sensors to provide adaptive lighting through Internet of Things (IoT).

-

Superior ultra-high power COB LEDs exceeding 50W that serve as light sources in stadiums, airports, and huge industrial plants replacing metal halide technology.

-

Tiny sized COB LEDs for use in spotlight and track lighting fixtures used in retail and hospitality facilities.

-

Medical and UV COB applications growing for sterilization, phototherapy, and optical inspection equipment.

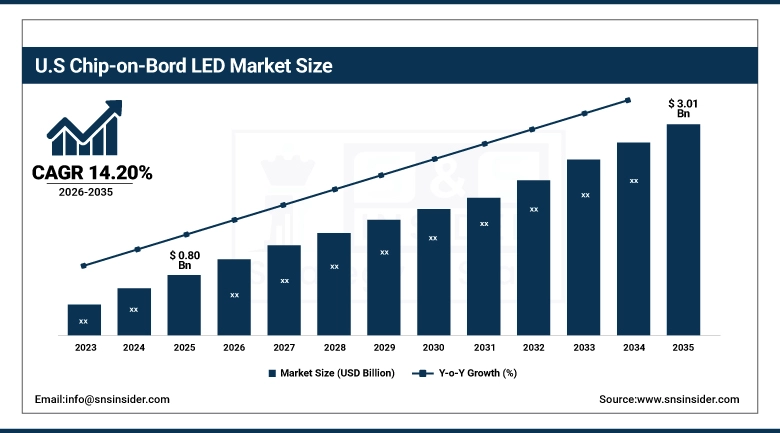

U.S. Chip-on-Board (COB) LED Market was valued at USD 0.80 billion in 2025 and is expected to reach USD 3.01 billion by 2035, at a CAGR of 14.20% from 2026 to 2035.

The US COB LED lighting market enjoys very high demand from commercial retrofit lighting projects, increasing popularity of the emerging horticulture lighting sector especially cannabis growers, automotive lighting applications, and advanced retail and hospitality lighting requirements, which value COB lighting's superior quality in terms of dimming capabilities and spotlight color rendering index. The United States Department of Energy continues to offer incentives towards the use of LEDs in commercial buildings, and COB LEDs are well positioned to exploit this opportunity. US lighting fixture makers such as Cree, Acuity Brands, and Hubbell are already using COB LEDs in high-end products.

The US agricultural indoor growing industry, especially legal cannabis grows farms where optimal light spectrum translates into higher yields and potency levels, has become one of the highest valued and most technologically advanced segments of COB LED lighting application opportunities. Growers have been found to be willing to invest extra money for LED COB lighting with ability to control light spectrums.

Market Segment Insights

-

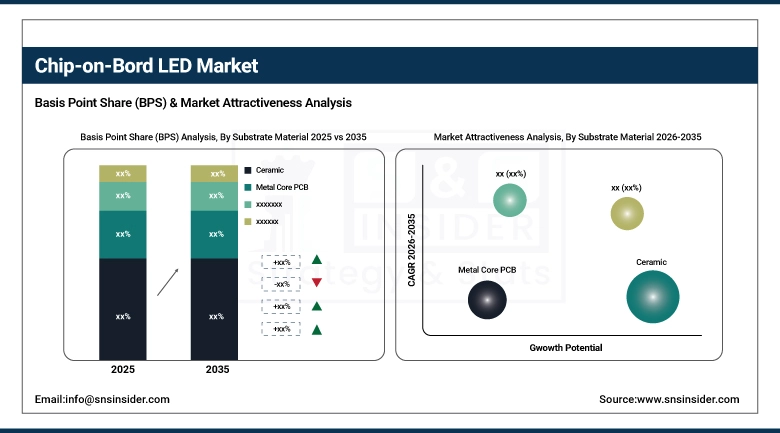

Based on Substrate, Ceramic COB substrates dominate for high-power applications with superior thermal conductivity; Metal Core PCB serves mid-power applications.

-

Based on Application, General Illumination holds the largest share; Automotive is growing at the fastest CAGR as LED headlamp adoption expands globally.

-

Based on End-Use, Commercial holds the largest share driven by retail and hospitality high-quality lighting demand; Industrial grows for high-bay applications.

-

Based on Power Range, 10–30W is the core commercial sweet spot; Above 30W grows fastest for industrial, stadium, and outdoor infrastructure applications.

Market Segment Analysis

By Substrate Material: Ceramic dominants, Metal Core PCB fastest growing CAGR

Ceramic substrates, primarily aluminum nitride (AlN) and alumina (Al2O3), are the leading COB LED substrate material for high-power applications because of their excellent thermal conductivity, electrical insulation, and long-term reliability under thermal cycling. AlN ceramic offers the highest thermal conductivity (170-200 W/m·K), making it the preferred choice for COB LEDs above 30W where junction temperature management is critical to maintaining efficacy and lifetime. Ceramic substrates also provide superior dimensional stability and resistance to moisture, enabling COB LEDs to meet automotive qualification standards (AEC-Q102) and medical device requirements.

Metal Core PCB substrates use aluminum or copper base plates with a dielectric polymer layer between the metal core and the copper circuit traces. MCPCBs offer good thermal performance at lower cost than ceramic substrates, making them the practical choice for mid-power COB LEDs in mainstream commercial and residential lighting applications. The well-established PCB manufacturing infrastructure for MCPCB production enables competitive pricing for volume applications.

By Application: General Illumination dominates, Automotive Lighting fastest growing CAGR

General illumination is the dominant COB LED application, encompassing commercial downlights, track lights, spotlights, high-bay industrial lights, streetlights, and general-purpose indoor and outdoor fixtures. The global transition from legacy light sources including metal halide, halogen, and fluorescent to LED is still ongoing in many markets, and COB technology is capturing the high-performance segment of this retrofit wave. Commercial retail lighting—where COB's high CRI (>90) and precise beam control make merchandise look its best—is particularly important for premium fixture specifications.

Automotive lighting is the fastest-growing COB LED application, encompassing headlamps, daytime running lights (DRL), fog lights, tail lights, and interior ambient lighting. LED headlamps using COB components deliver superior nighttime visibility compared to halogen alternatives while consuming significantly less power.

By End-Use: Commercial dominates, Industrial fastest growing CAGR

Commercial end-uses include retail stores, hotels, restaurants, offices, galleries, and public institutions where quality lighting affects consumer satisfaction, branding, and workplace efficiency. The commercial end-user demands the use of COB LEDs owing to its superior light-beam management, excellent color rendering properties, and increased longevity, reducing the need for frequent maintenance when installed at high ceilings and hard-to-reach fixtures.

The uses of COB LEDs for industrial purposes are found in high bay warehousing lighting, floodlighting for sports stadiums, transport lighting such as road tunnels and underpasses, and outdoor lighting for expansive industrial complexes. Industrial users opt for high-powered COB LEDs over 30 watts owing to their ability to generate enough lumens to illuminate extensive areas with high energy efficiency compared to existing technologies.

By Power Range: 10–30W dominates, Above 30W fastest growing CAGR

The 10-30W power range is the core of the commercial COB LED market, serving mainstream commercial downlights, retail track lights, architectural spotlights, and mid-range automotive headlamp modules. This range delivers the combination of luminous flux output, efficacy, and manageable thermal requirements that makes it the most broadly specified COB LED tier.

High-power COB LEDs above 30W is growing fastest as industrial, sports, and outdoor infrastructure applications adopt LED technology. These products require ceramic substrates and sophisticated thermal management to operate reliably at elevated junction temperatures. Stadium floodlights, large outdoor area luminaires, horticulture lighting systems, and cinema light engines use COB LEDs in the 50-200W range.

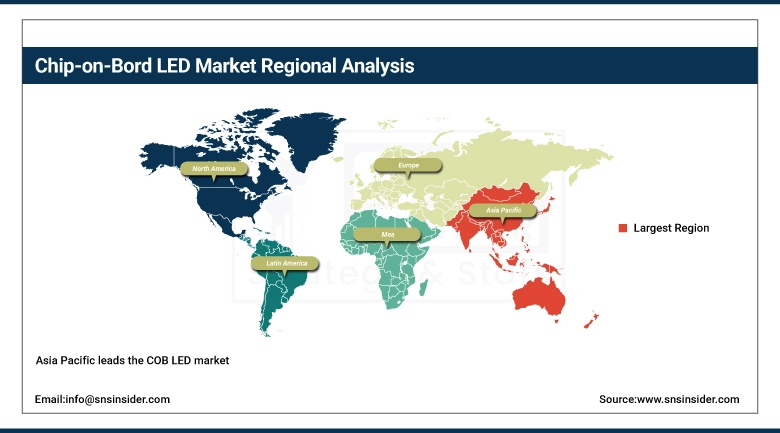

Chip on Board LED Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

73% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

55% |

|

Middle East & Africa |

UAE |

40% |

|

Latin America |

Brazil |

49% |

Asia Pacific Chip on Board LED Market Insights

Asia Pacific leads the COB LED market, driven by China's dominant position in LED manufacturing—China produces the majority of global LED chips and packaged products including COB modules. Major Chinese manufacturers including San'an Optoelectronics, Refond, and Zhuhai Enraytek supply COB LED products to global fixture manufacturers. Japan's Nichia, which pioneered high-CRI COB technology, and Korea's Seoul Semiconductor are important premium COB LED suppliers. The region's large consumer electronics and automotive manufacturing sectors also create significant domestic COB LED demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Chip on Board LED Market Insights

The North American region is one of the leading markets for commercial-grade COB LEDs because of its needs for renovations within commercial buildings, its expanding indoor farming, and its extensive application of automotive LEDs. In America, there are COB LEDs that are incorporated into high-end commercial fixtures produced by Cree, Acuity Brands, and Lutron. Professional lighting equipment for films and entertainment in the United States constitutes a niche COB LED segment. Energy efficiency initiatives within governments have been boosting COB LED applications within high-performance lighting.

Europe Chip on Board LED Market Insights

The key drivers behind Europe's COB LED industry are the energy efficient nature of EU lighting regulations, the incorporation of LED technology into buildings during renovation works, and the advanced lighting supply chain within the region, mainly located in Germany. COB LED lighting products are favored by European lighting experts because of their ability to render better colors in luxury hospitality and retail sectors. The technological leadership of German OEM car makers like Audi, BMW, and Mercedes in LED headlamp technologies also contributes to this regional demand.

Middle East & Africa and Latin America Chip on Board LED Market Insights

Middle Eastern investments in advanced lighting for public and commercial installations through smart cities and tourism infrastructure projects have become a major area for COB LEDs. Saudi Arabia's Vision 2030 infrastructure projects and growth in the UAE's hospitality industry are key markets for COB LEDs.

COB LEDs are emerging in Latin America due to commercial LED retrofits in Brazilian, Mexican, and Colombian buildings. Brazil's large retail and hospitality industries are leading users of superior LED lighting solutions, and COB LEDs are increasingly being used in sophisticated lighting systems. Several Latin American nations are encouraging commercial LED use through their energy efficiency programs.

Chip on Board LED Market Growth Drivers

Energy efficiency regulations and automotive LED adoption are the core structural growth drivers

Global regulations phasing out inefficient light sources—mercury-containing fluorescent lamps in the EU, halogen lamps in multiple markets, and metal halide in commercial applications—are creating mandated replacement demand that directly benefits LED technology including COB. Simultaneously, the automotive industry's global transition to full-LED front lighting across all vehicle segments is creating a new high-growth application where COB LED technology's performance advantages in compact headlamp module design are particularly valuable.

Smart city lighting programs across Asia Pacific, the Middle East, and Europe are accelerating adoption of high-performance LED street and area lighting where COB technology's efficiency, reliability, and lifetime advantages over traditional lighting are most pronounced. As city governments upgrade infrastructure for safety, sustainability, and cost reduction objectives, they are specifying COB LED products that will operate for 50,000+ hours without replacement.

Chip on Board LED Market Restraints

Intense price competition from commodity LED alternatives and thermal management complexity

Over the last decade, the commoditized LED industry experienced huge drops in the cost of products, where affordable filament LEDs and simple LEDs are sold at highly discounted prices. COB LEDs carry a hefty price premium over those options, which may not necessarily prove justifiable for the cost-conscious buyer when applying them in residences and small-scale commercial applications. The fact that the junction temperature of COB LED is relatively high due to its high-power density means that a good thermal design has to be incorporated in the fixture.

Chip on Board LED Market Opportunities

Horticultural and UV-C disinfection applications represent high-growth premium opportunities

The indoor agriculture revolution—driven by vertical farming, urban food production, and cannabis cultivation—is creating a specialized, premium market for spectrum-optimized COB LEDs where performance directly affects crop yield and quality. Growers pay premium prices for COB LED systems that precisely deliver the photosynthetically active radiation spectra needed for different plant growth stages. UV-C COB LEDs for air and surface disinfection, a market that received enormous visibility during the COVID-19 pandemic, continue to grow in healthcare, food processing, and HVAC applications where chemical-free sterilization is valued.

Recent Developments

-

2026: OSRAM introduced new COB LEDs to their lineup, which concentrated on high-efficiency solutions for the auto and architectural lighting markets. OSRAM highlighted superior thermal management capabilities and high luminance COB LEDs suited for intelligent mobility, industrial and precision optics.

-

2026: Signify strengthened its COB LED-based smart lighting ecosystem under its Interact platform. The company focused on integrating COB technology into connected commercial lighting solutions, supporting energy-efficient buildings, smart cities, and IoT-enabled infrastructure projects worldwide.

-

2026: Cree LED advanced its high-power COB LED solutions for industrial, horticulture, and outdoor lighting applications. The company focused on improving lumen density and energy efficiency, targeting smart agriculture systems and high-performance commercial illumination markets.

Key Players

Some of the companies in the Chip-on-Board (COB) LED Market:

-

Nichia Corporation

-

Cree LED

-

Seoul Semiconductor Co. Ltd.

-

Lumileds Holding B.V.

-

Samsung LED Co. Ltd.

-

Osram Opto Semiconductors

-

Citizen Electronics Co. Ltd.

-

Luminus Devices Inc.

-

Bridgelux Inc.

-

Citizen Electronics Co., Ltd.

-

Toyoda Gosei Co. Ltd.

-

MLS Co. Ltd.

-

Stanley Electric Co. Ltd.

-

LG Innotek Co., Ltd.

-

San'an Optoelectronics Co. Ltd.

-

Refond Optoelectronics Co. Ltd.

-

Enraytek Optoelectronics Co. Ltd.

-

Lextar Electronics Corporation

-

Epistar Corporation

-

Everlight Electronics Co. Ltd.

Chip-on-Bord LED Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.63 Billion |

| Market Size by 2035 | USD 13.7 Billion |

| CAGR | CAGR of 14.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Substrate Material (Ceramic, Metal Core PCB, Silicon) • By Application (General Illumination, Automotive Lighting, Backlighting, Horticulture Lighting, Medical & UV Applications, Others) • By End-Use (Commercial, Industrial, Residential, Automotive) • By Power Range (Below 10W, 10–30W, Above 30W) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nichia Corporation, Cree LED, Seoul Semiconductor Co. Ltd., Lumileds Holding B.V., Samsung LED Co. Ltd., Osram Opto Semiconductors, Citizen Electronics Co. Ltd., Luminus Devices Inc., Bridgelux Inc., San'an Optoelectronics Co. Ltd., Refond Optoelectronics Co. Ltd., Enraytek Optoelectronics Co. Ltd., Lextar Electronics Corporation, Epistar Corporation, Everlight Electronics Co. Ltd., LG Innotek Co. Ltd., Stanley Electric Co. Ltd., Toyoda Gosei Co. Ltd., MLS Co. Ltd. |

Frequently Asked Questions

Asia Pacific leads the market due to China's dominant LED manufacturing base and significant domestic commercial and automotive lighting demand.

Automotive lighting is the fastest-growing application, driven by global adoption of LED headlamp systems across all vehicle segments.

Ceramic substrates dominate for high-power applications due to superior thermal conductivity; Metal Core PCB serves the cost-sensitive mid-power commercial market.

The COB LED Market was valued at USD 3.63 billion in 2025.

The COB LED Market is expected to grow at a CAGR of 14.12% from 2026 to 2035.

Get in Touch