Thermal Management Technologies Market Report Scope & Overview:

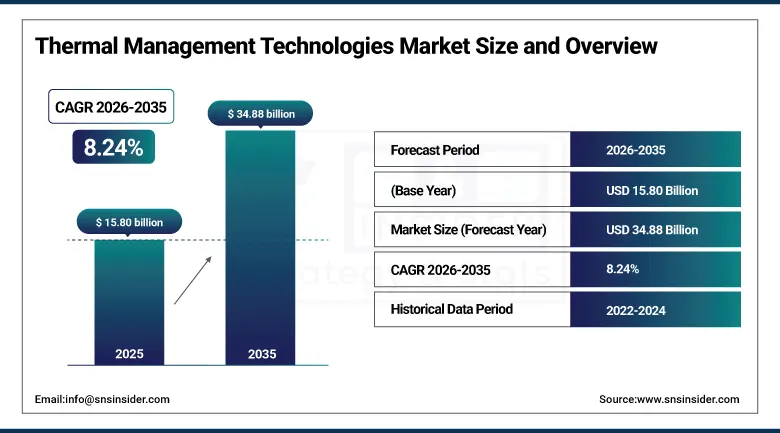

The Thermal Management Technologies Market size was valued at USD 15.80 billion in 2025 and is expected to reach USD 34.88 billion by 2035, growing at a CAGR of 8.24% from 2026-2035.

Thermal management technologies are witnessing growth owing to the growing requirement for effective heat transfer technology in the electronics industry, electric vehicles, and data centers. The use of high performance computing, 5G network, and renewable energy technology is driving the need for sophisticated thermal management technology. The reduction in the size of the device along with high power density levels is also driving innovation in the market.

The U.S. Department of Energy reports that data center cooling currently accounts for approximately 40% of total data center energy consumption. The DOE's Better Buildings program has set 25% data center energy intensity reduction targets that make advanced thermal management investment commercially and regulatorily compelling for U.S. data center operators.

Market Size and Forecast

-

Market Size in 2025: USD 15.80 Billion

-

Market Size by 2035: USD 34.88 Billion

-

CAGR: 8.24% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Thermal Management Technologies Market - Request Free Sample Report

Thermal Management Technologies Market Trends

-

Liquid cooling adoption in data centers is accelerating from niche high-performance computing installations to mainstream hyperscale deployments as AI GPU cluster heat densities exceed air cooling limits at scale.

-

Phase change materials with higher latent heat capacities and improved thermal conductivity are being developed for EV battery pack temperature regulation applications where conventional liquid cooling adds unacceptable weight and complexity.

-

AI-driven thermal control systems using CNN-LSTM-based predictive algorithms are replacing conventional thermostatic control in EV battery management, improving thermal stability while reducing cooling energy consumption.

-

Immersion cooling submerging server components directly in dielectric fluid is transitioning from experimental to commercial deployment at hyperscale data centers where density requirements have outpaced air and cold-plate liquid cooling solutions.

-

Graphene and carbon nanotube-infused thermal interface materials are achieving thermal conductivity values 5-10x higher than conventional silicone-based TIMs, enabling heat dissipation from increasingly dense electronic packages.

U.S. Thermal Management Technologies Market Size Outlook:

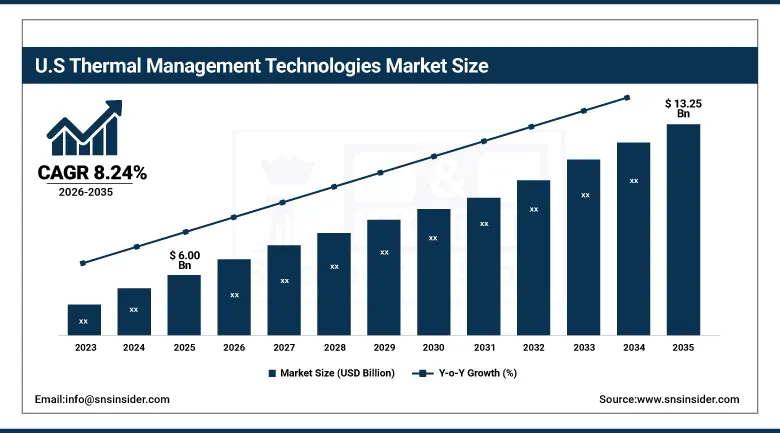

The U.S. Thermal Management Technologies Market was valued at USD 6.00 billion in 2025 and is expected to reach USD 13.25 billion by 2035, growing at a CAGR of 8.24% from 2026-2035. The US market for thermal management technologies is expected to register steady growth owing to the robust demand in the country from the automotive industry, data centers, and advanced electronics.

The U.S. Lawrence Berkeley National Laboratory estimates that U.S. data centers consumed approximately 200 TWh of electricity in 2023, with cooling representing the largest discretionary energy consumption category. The IRA's Advanced Manufacturing Production Credit (Section 45X) directly incentivizes domestic production of battery components including thermal management systems for EV battery packs.

Thermal Management Technologies Market Segment Analysis

-

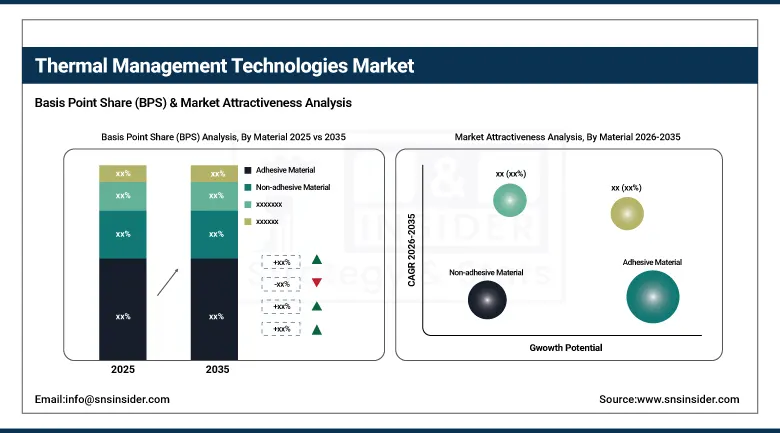

By Material, Adhesive Material dominated with ~65% share in 2025; Non-adhesive Material fastest growing (CAGR).

-

By Device, Conduction Cooling Device dominated the Thermal Management Technologies Market in 2025; Advanced Cooling Device fastest growing.

-

By Service, Installation & Calibration segment dominated; Optimization & Post Sales Service growing steadily.

By Material, Adhesive Material segment dominates the Thermal Management Technologies Market, Non-adhesive Material expected to grow fastest

Adhesive materials held approximately 65% of the Thermal Management Technologies Market in 2025. These include thermal interface adhesives, conductive epoxies, and phase-change adhesive films that bond electronic components to heat sinks or heat spreaders while simultaneously filling the microscopic air gaps at contact surfaces that dramatically increase thermal resistance. Adhesive thermal interface materials combine mechanical attachment with thermal performance in a single product, simplifying assembly processes in consumer electronics, automotive electronics, and power electronics manufacturing. As electronic components continue to miniaturize while running at higher power densities, demand for advanced adhesive materials including nanomaterial-infused adhesive formulations with thermal conductivity approaching 10-20 W/mK continues to grow.

Non-adhesive materials are the fastest-growing category, driven by increasing demand for alternative cooling solutions phase change materials, thermal interface films, pyrolytic graphite sheets, and advanced metal-based heat spreaders that offer superior heat dissipation performance in applications where adhesive bonding is impractical, reversible assembly is required, or the performance limitations of adhesive materials are insufficient. Non-adhesive thermal interface materials are particularly valued in high-performance computing and electric vehicle applications where components require periodic replacement or where the cumulative thermal resistance of adhesive materials at extended operating temperatures degrades below specification.

By Device, Conduction Cooling Device segment dominates the Thermal Management Technologies Market, Advanced Cooling expected to grow fastest

Conduction cooling devices heat sinks, heat spreaders, thermal straps, and cold plates held the dominant device market share in 2025, reflecting their widespread deployment across the full spectrum of electronic equipment from consumer smartphones to data center servers. Passive conduction cooling through aluminum and copper heat sinks remains the most cost-effective thermal management approach for applications where component power densities are moderate and ambient temperatures are controlled. The conduction cooling device market benefits from the enormous installed base of electronics equipment using heat sinks, the continuous demand for upgraded heat sink designs as component power increases, and the material innovation in graphene composites and vapor chamber heat spreaders that are extending conduction cooling performance to previously unmanageable heat flux levels.

Advanced cooling devices including liquid cooling systems, immersion cooling infrastructure, and two-phase cooling technologies are growing at the fastest CAGR, driven by the AI data center heat density challenge and EV battery thermal management requirements that conduction and convection cooling cannot adequately address at scale. Data centers deploying NVIDIA H100 and B200 GPU clusters are retrofitting or constructing facilities with direct liquid cooling infrastructure that delivers coolant directly to chip-level cold plates, removing heat 1,000 times more efficiently per unit flow than air cooling at equivalent power density. The immersion cooling market, while still a fraction of total thermal management revenue, is growing at exceptional rates as operators of AI computing clusters find that conventional cooling architectures cannot be economically scaled to 80kW+ rack densities.

Thermal Management Technologies Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

45% |

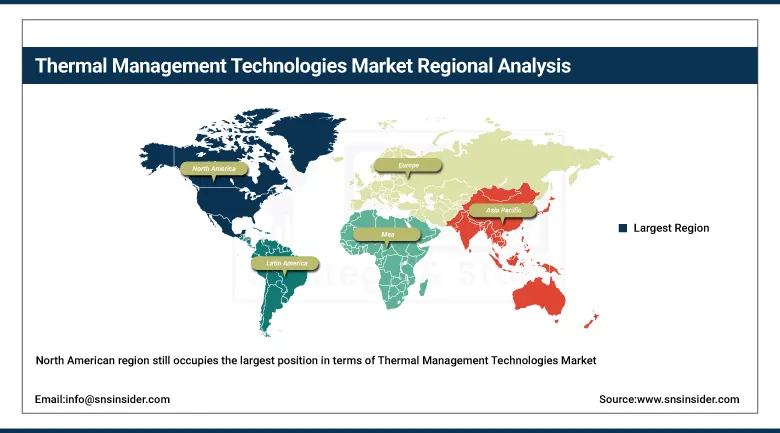

North America Thermal Management Technologies Market Insights

The North American region still occupies the largest position in terms of Thermal Management Technologies Market, with the United States leading the demand by means of hyperscale data center construction, EV manufacturing production, and aerospace and defense thermal management initiatives. The heavy investments in AI computing made by companies like Microsoft, Google, Amazon, and Meta are pushing the boundaries of liquid cooling systems and thermal interface material procurements in the supply chain. Domestic semiconductor manufacturing growth made possible by funds from the CHIPS Act needs advanced thermal management technologies for the new generation of fabs and semiconductors.

U.S. data center investment reached a record USD 49 billion in 2023 according to CBRE research, with liquid cooling infrastructure representing the fastest-growing capital expenditure category within data center construction budgets. The U.S. Department of Defense's thermal management technology research portfolio focused on high-power electronics for directed energy weapons and radar systems sustains government-funded development of advanced cooling technologies that transition to commercial markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Thermal Management Technologies Market Insights

Asia Pacific leads the way in terms of the growth rate of the Thermal Management Technologies Market, thanks to China’s mass-scale production of electric vehicles, the leadership in the manufacturing of consumer electronics, cutting-edge manufacturing of semiconductors in Japan and South Korea, and a boom in data center investments taking place in China, India, Singapore, and Australia. Chinese automotive industry, which produces more than 8 million EVs per year and counting, comprises the largest single EV battery thermal management purchase market in the world. The concentration of electronics manufacturing in Taiwan, South Korea, and China ensures steady sales of thermal interface materials in huge quantities unparalleled elsewhere geographically.

China's Ministry of Industry and Information Technology reports that EV production exceeded 9 million units in 2023, each requiring sophisticated battery thermal management systems. The Semiconductor Equipment and Materials International (SEMI) reports that Asia Pacific accounts for over 75% of global semiconductor manufacturing capacity, creating the world's largest regional thermal management material demand base for electronic device production.

Europe Thermal Management Technologies Market Insights

Europe is the fastest-growing regional market with respect to CAGR due to the investments made by companies towards building high performance computing systems and AI-based systems infrastructure, demand for thermal management in the automotive EV domain by Germany and other European OEMs, and the substantial investment by the European Union into HPC infrastructure via EuroHPC projects. Germany, the UK, and France are the major regions in Europe where automotive demand drives the procurement of thermal management materials and systems owing to the scaling-up of Volkswagen, BMW, Mercedes, Stellantis, and Renault electric vehicle manufacturing programs.

The EuroHPC Joint Undertaking has invested over EUR 1 billion in high-performance computing infrastructure across EU member states, with direct thermal management infrastructure implications for facilities housing GPU-based HPC systems. The EU's battery regulation mandates thermal management performance specifications for EV batteries placed on the European market, driving investment in thermal management technology qualification for EV supply chains.

Middle East & Africa and Latin America Thermal Management Technologies Market Insights

Both areas have developing thermal management technologies markets due to increased investments in data centers, rising electronics manufacturing, and increasing electric vehicles usage. The UAE and Saudi Arabia are making large investments in hyperscale data centers to provide cloud computing services and artificial intelligence, which results in a growing need for thermal management technologies from a very small starting point. The hot weather conditions in Dubai make the need for thermal management technologies more intense for data centers since there is a greater need for cooling than using air cooling methods. In Latin America, Brazil's developing technological market and Mexico's automotive industry that exports cars abroad drive the need for thermal management technologies.

Growth Drivers: AI data center heat density surge and EV battery safety requirements driving global thermal management technology investment

The thermal management industry finds itself in an environment where it is impacted by the two most expensive infrastructure development initiatives in the history of technology at the same time. AI computing infrastructure development creates a need for thermal management that is unprecedented in any commercial computing infrastructure development in the past. NVIDIA's GB200 NVL72 rack system requires 120kW power consumption and direct liquid cooling, which all operators of AI infrastructure are required to provide. The other driving force is thermal management of electric vehicle batteries. Thermal sensitivity of the lithium-ion battery is understood, and its effects on reduced efficiency, shortened lifecycle, and potential thermal runaway accidents create business and regulatory drivers for advanced thermal management investments in parallel to increased production of EVs.

Next-generation design Battery Thermal Management Systems using PCM-foam with liquid cooling can save up to 53% in system weight and approximately 90% in total cooling power consumption according to published engineering studies. AI engine CNN-LSTM-based thermal control strategies demonstrate thermal stability enhancement of 40-43% while maintaining temperature control at ±0.3°C, improving energy efficiency by 2.1%.

Restraints: Complex system integration requirements and high implementation costs limiting broad thermal management technology adoption

The incorporation of innovative thermal management solutions in the design of modern electronics and automobiles needs intricate engineering to facilitate integration, and this engineering difficulty translates into obstacles in the actualization of adoption. Liquid cooling solutions for data centers necessitate the creation of a pressure system to distribute the coolant, as well as a detection mechanism to identify leaks and additional mechanical works in the building. Phase change materials must be designed alongside the battery cells and the batteries themselves, thus implying that phase change materials will not be able to be integrated into existing battery designs. In the case of automotive manufacturers designing vehicles with compressed development cycles, innovative thermal management solutions demand supplier evaluation and testing, increasing risks associated with their programs. Standardized methods for integration in various industries do not exist, which means that custom engineering is needed for each application, inhibiting the potential cost savings of large-scale manufacturing.

Opportunities: Immersion cooling innovation and AI-optimized thermal control creating significant new thermal management growth opportunities

Immersive cooling through dielectric fluid immersion and evaporative immersion cooling is currently the most commercially viable thermal management approach in the AI data center industry. Due to the rack power density requirements for AI applications exceeding the capability of the direct liquid cooling system using a cold plate in removing heat from components, the immersion cooling technique offers an inherent physics-based performance benefit that will support continued commercial uptake as the deployment of AI hardware proceeds. Companies such as Submer, GRC, Vertiv, and Schneider Electric are developing businesses in immersion cooling at a rate higher than the industry average in the thermal management space. An AI thermal management system that uses machine learning algorithms to optimize the provision of cooling based on workload and sensor temperature data is a third potential opportunity, which replaces conventional rule-based cooling control methods with AI-based cooling, resulting in a 15%-30% reduction in energy consumption.

Recent Developments:

-

2025: Vertiv Group launched its Liebert CoolPhase 2 two-phase cooling system for AI GPU clusters, achieving heat removal capacity of 120kW per rack through a hybrid liquid-to-air heat exchanger design that eliminates the need for on-site chilled water infrastructure, enabling AI computing deployment in facilities without existing chilled water distribution networks.

-

2025: Henkel AG introduced its LOCTITE TIM Series 7000 thermal interface material incorporating boron nitride nanosheet fillers achieving 12 W/mK bulk thermal conductivity with maintained printability for automated dispensing systems, targeting automotive power electronics and EV inverter thermal management applications requiring high throughput production compatibility.

-

2026: Submer Technologies commissioned its largest commercial megapod immersion cooling system at a European hyperscale data center, achieving a Power Usage Effectiveness (PUE) of 1.03 essentially eliminating cooling overhead energy consumption — while cooling GPU racks at 80kW density, demonstrating immersion cooling's scalability for AI data center deployment at commercial scale.

Thermal Management Technologies Companies are:

-

Honeywell International Inc.

-

Laird Thermal Systems

-

Parker Hannifin Corporation

-

Boyd Corporation

-

Vertiv Holdings Co.

-

3M Company

-

Vishay Intertechnology Inc.

-

Bergquist (Henkel)

-

Momentive Performance Materials Inc.

-

Shin-Etsu Chemical Co., Ltd.

-

Fujipoly America Corp.

-

Celanese Corporation

-

Indium Corporation

-

Submer Technologies S.L.

-

GRC (Green Revolution Cooling)

-

Asetek A/S

-

Aavid Thermalloy (Boyd)

-

Wakefield-Vette Inc.

Thermal Management Technologies Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.80 Billion |

| Market Size by 2035 | USD 34.88 Billion |

| CAGR | CAGR of 8.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Adhesive Material, Non-adhesive Material) • By Device (Conduction Cooling Device, Convection Cooling Device, Advanced Cooling Device, Others) • By Service (Installation & Calibration, Optimization & Post Sales Service) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., Gentherm Incorporated, Laird Thermal Systems, Parker Hannifin Corporation, Boyd Corporation, Vertiv Holdings Co., Henkel AG & Co. KGaA, 3M Company, Vishay Intertechnology Inc., Bergquist (Henkel), Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd., Fujipoly America Corp., Celanese Corporation, Indium Corporation, Submer Technologies S.L., GRC (Green Revolution Cooling), Asetek A/S, Aavid Thermalloy (Boyd), Wakefield-Vette Inc. |

Frequently Asked Questions

Ans: North America dominated the Thermal Management Technologies Market in 2025.

Ans: The Advanced Cooling Device segment is expected to register the fastest CAGR through 2035.

Ans: The Adhesive Material segment dominated with approximately 65% share in 2025.

Ans: The Thermal Management Technologies Market was valued at USD 15.80 billion in 2025.

Ans: The Thermal Management Technologies Market is expected to grow at a CAGR of 8.24% from 2026 to 2035.

Get in Touch