Coal Mining Market Report Scope & Overview:

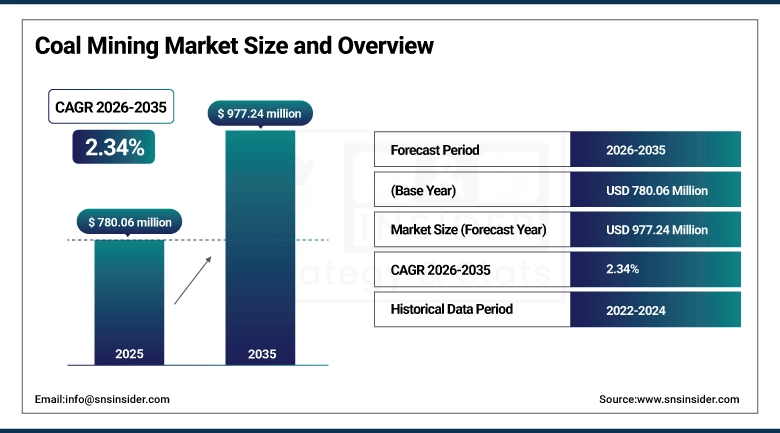

The Coal Mining Market was valued at USD 780.06 million in 2025 and is expected to reach USD 977.24 million by 2035, growing at a CAGR of 2.34% from 2026-2035.

Coal Mining Market growth is supported by rising global electricity demand, particularly in developing economies where coal remains a reliable and cost-effective energy source. Expanding industrial activities, especially in steel and cement production, continue to drive coal consumption. Infrastructure development and urbanization further increase energy requirements. Additionally, advancements in mining technologies and sustained demand for metallurgical coal in steelmaking contribute to steady market expansion despite the gradual shift toward cleaner energy sources.

The International Energy Agency states that coal supplies over one-third of global electricity generation, reinforcing its role as a dependable energy source.

Furthermore, steel production increased by 6.3% in 2024, while coal-based industrial processes such as sponge iron grew by 10%, significantly boosting coal demand across industrial sectors.

Coal Mining Market Size and Growth Forecast:

-

Market Size in 2025: USD 780.06 Million

-

Market Size by 2035: USD 977.24 Million

-

CAGR: 2.34% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Coal Mining Market - Request Free Sample Report

Coal Mining Market Trends

-

Rising demand for energy generation and industrial fuel is driving the coal mining market.

-

Growing use of coal in power plants, steel production, and cement manufacturing is boosting market growth.

-

Expansion of infrastructure and industrial activities is fueling coal consumption.

-

Increasing focus on efficient mining operations and cost optimization is shaping market trends.

-

Advancements in mining technologies, automation, and safety systems are enhancing productivity and reducing risks.

-

Rising demand from emerging economies for electricity and industrial output is supporting market expansion.

-

Strategic collaborations between mining companies, equipment manufacturers, and governments are accelerating operational efficiency and global supply.

U.S. Coal Mining Market Size Outlook:

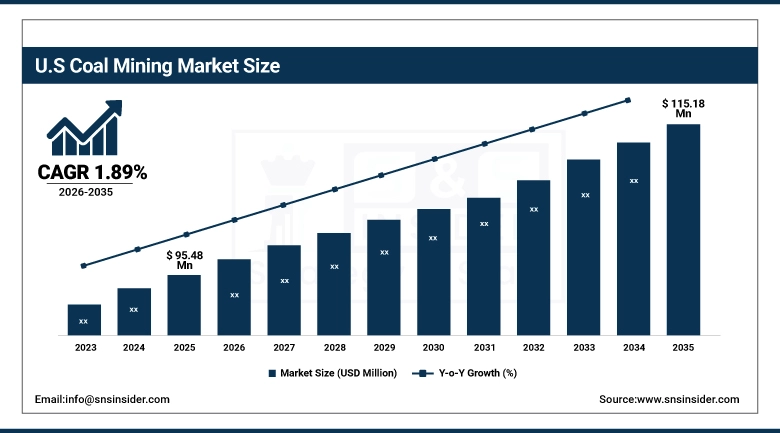

U.S. Coal Mining Market was valued at USD 95.48 million in 2025 and is expected to reach USD 115.18 million by 2035, growing at a CAGR of 1.89% from 2026-2035. U.S. Coal Mining Market growth is driven by steady demand from industrial sectors such as steel and cement, along with continued coal exports. Existing power infrastructure and energy reliability needs also support coal usage, despite increasing adoption of renewable energy sources.

U.S. coal consumption reached 410.9 million short tons in 2024, with the electric power sector accounting for 87.6% of total usage, highlighting coal’s continued importance in electricity generation.

Total U.S. coal stocks stood at 156.2 million short tons in 2024, including 128.3 million short tons held by the power sector, indicating a stable supply-demand balance supporting ongoing coal consumption.

Coal Mining Market Growth Drivers:

-

Rising global electricity demand and continued dependence on coal-based power generation ensure steady consumption despite increasing renewable energy integration trends worldwide

Rising electricity demand across developing and industrial economies continues to drive coal consumption due to its affordability and reliability in large-scale baseload power generation. Coal remains a primary energy source for utilities where renewable infrastructure is still developing or insufficient to meet peak demand. Rapid urbanization, industrialization, and population growth further increase energy requirements, particularly in emerging markets. Additionally, coal-fired power plants offer stable output compared to intermittent renewable sources, ensuring grid stability. Governments in several economies continue to support coal usage to maintain energy security and reduce dependence on imported fuels.

According to the International Energy Agency, global coal demand increased by around 1% in 2024, reaching a record of approximately 8.77 billion tonnes, primarily driven by rising electricity demand in emerging economies.

The agency also reports that global electricity demand surged by 4.3% in 2024, significantly above historical averages, supported by industrial growth, electrification, and increasing cooling needs worldwide.

Coal Mining Market Restraints:

-

Increasing environmental regulations and carbon emission concerns are limiting coal mining activities and accelerating transition toward cleaner energy alternatives globally

Increasing environmental concerns and strict government regulations on carbon emissions are significantly restricting coal mining operations. Policies aimed at reducing greenhouse gas emissions are encouraging the shift toward renewable energy sources such as solar, wind, and hydroelectric power. Carbon pricing mechanisms, emission caps, and stricter environmental compliance requirements are raising operational costs for coal producers. Additionally, financial institutions are reducing investments in coal-related projects due to sustainability commitments. Public pressure and global climate agreements are further discouraging coal usage, leading to declining demand in several developed regions.

Coal Mining Market Opportunities:

-

Advancements in clean coal technologies and carbon capture solutions enabling more sustainable coal utilization while reducing environmental impact significantly

Advancements in clean coal technologies, including carbon capture, utilization, and storage (CCUS), are creating opportunities for more sustainable coal usage. These technologies help reduce carbon emissions from coal-fired power plants, addressing environmental concerns while maintaining energy output. Governments and companies are investing in research and development to improve efficiency and reduce environmental impact. Adoption of high-efficiency, low-emission (HELE) technologies further enhances coal utilization. Such innovations enable coal to remain relevant in the energy mix, especially in regions where transitioning fully to renewables is challenging due to infrastructure or economic constraints.

According to the International Energy Agency, over 500 CCUS projects were at various stages of development globally in 2024, spanning power generation and industrial sectors including coal-based facilities.

The U.S. Department of Energy also launched major CCUS demonstration initiatives in 2024 aimed at decarbonizing power plants and industrial operations.

Companies such as Shell plc are expanding large-scale carbon capture and storage projects to reduce emissions from heavy industries, while Mitsubishi Heavy Industries has deployed post-combustion carbon capture systems capable of capturing up to 90% of CO₂ emissions from thermal power plants.

Coal Mining Market Segment Highlights

-

By Type, Thermal Coal dominated the Coal Mining Market with ~77% share in 2025; Coking Coal fastest growing (CAGR).

-

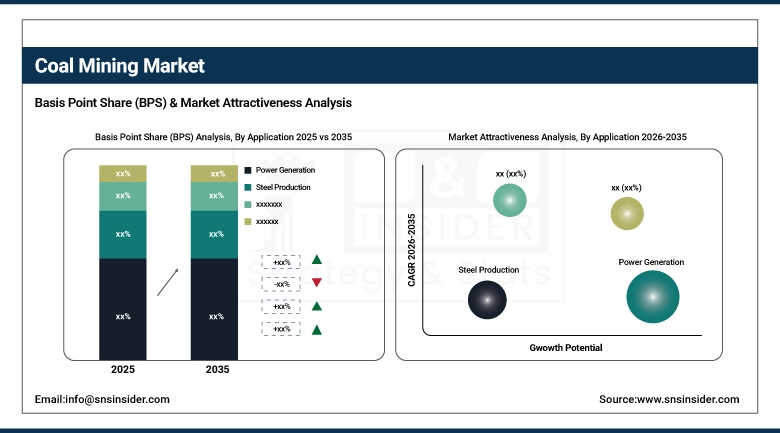

By Application, Power Generation dominated the Coal Mining Market with ~67% share in 2025; Steel Production fastest growing (CAGR).

-

By End-User Industry, Utilities (Power Plants) dominated the Coal Mining Market with ~64% share in 2025; Industrial (Steel, Cement, Manufacturing) fastest growing (CAGR).

-

By Method, Surface Mining dominated the Coal Mining Market with ~58% share in 2025; Surface Mining fastest growing (CAGR).

By Application, Power Generation segment dominates the Market, Steel Production expected to grow fastest

Power Generation segment dominated the Coal Mining Market with the highest revenue share in 2025 due to the continued reliance on coal-fired power plants for stable and large-scale electricity production. Coal’s affordability and ability to deliver uninterrupted energy supply support grid stability, particularly in regions experiencing rapid electricity demand growth and limited renewable energy integration capacity constraints.

Steel Production segment is expected to grow at the fastest CAGR from 2026-2035 due to increasing global infrastructure investments and industrial activities requiring high steel output. Coking coal remains indispensable in traditional steelmaking processes, and ongoing urbanization alongside transportation and construction projects is accelerating demand for steel, thereby driving coal consumption significantly across key industrial economies.

By Type, Thermal Coal segment dominates the Market, Coking Coal expected to grow fastest

Thermal Coal segment dominated the Coal Mining Market with the highest revenue share in 2025 due to its extensive use in power generation across developing and industrial economies. Its cost-effectiveness, abundant availability, and ability to provide continuous baseload electricity make it essential for energy security, especially where renewable infrastructure remains insufficient for consistent supply reliability needs.

Coking Coal segment is expected to grow at the fastest CAGR from 2026-2035 due to rising steel demand driven by infrastructure development, urbanization, and industrial expansion. Its critical role in blast furnace steelmaking, combined with limited substitutes for high-quality metallurgical processes, continues to strengthen demand across construction, automotive, and heavy manufacturing sectors globally.

By End-User Industry, Utilities (Power Plants) segment dominates the Market, Industrial (Steel, Cement, Manufacturing) expected to grow fastest

Utilities (Power Plants) segment dominated the Coal Mining Market with the highest revenue share in 2025 due to heavy dependence on coal for large-scale electricity generation. Utilities prioritize coal for its consistent supply, established infrastructure, and cost efficiency, ensuring reliable energy distribution to residential, commercial, and industrial sectors where uninterrupted power availability remains critically important for operations.

Industrial (Steel, Cement, Manufacturing) segment is expected to grow at the fastest CAGR from 2026-2035 due to increasing industrialization and construction activities worldwide. Coal is widely used as both an energy source and raw material in industrial processes, particularly in steel and cement production, where consistent heat generation and process efficiency are essential for large-scale manufacturing operations.

By Method, Surface Mining segment dominates and is expected to grow fastest in the Coal Mining Market

Surface Mining segment dominated the Coal Mining Market with the highest revenue share in 2025 due to its cost efficiency, higher productivity, and easier accessibility of coal reserves compared to underground methods. It enables large-scale extraction with lower operational risks and reduced labor intensity. The segment is also expected to grow at the fastest CAGR from 2026-2035 as demand increases for bulk coal production, supported by technological advancements, automation, and expansion of open-pit mining projects to meet rising global energy and industrial requirements.

Coal Mining Market Regional Analysis

Asia Pacific Coal Mining Market Insights

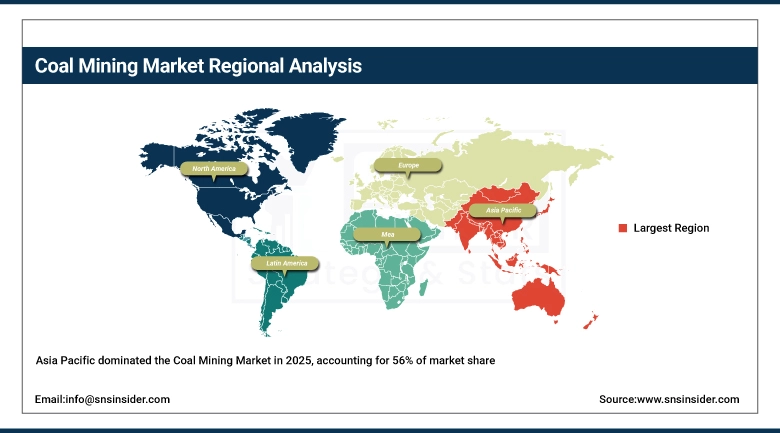

Asia Pacific segment dominated the Coal Mining Market with the highest revenue share of about 56% in 2025 due to strong coal demand from power generation and industrial sectors in countries such as China and India. Rapid urbanization, infrastructure development, and rising electricity consumption continue to drive coal usage. The region is also expected to grow at the fastest CAGR from 2026-2035, supported by expanding energy needs, abundant coal reserves, ongoing mining investments, and continued reliance on coal for energy security and industrial growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Coal Mining Market Insights

North America holds a significant position in the Coal Mining Market due to established mining infrastructure and stable demand from power generation and industrial applications. The United States remains a key contributor with large coal reserves and advanced mining technologies. However, gradual transition toward cleaner energy sources is moderating demand growth. Despite this, coal continues to support industrial processes, export markets, and energy reliability, maintaining its relevance across select applications in the region.

Europe Coal Mining Market Insights

Europe represents a declining yet strategically transitioning region in the Coal Mining Market due to stringent environmental regulations and aggressive decarbonization targets. Many countries are reducing coal dependency in favor of renewable energy sources, leading to mine closures and reduced production. However, limited coal demand persists for industrial applications and energy security concerns. Ongoing geopolitical uncertainties and energy supply disruptions have temporarily supported coal usage, sustaining short-term demand across select European markets.

Middle East & Africa and Latin America Coal Mining Market Insights

Middle East & Africa and Latin America regions in the Coal Mining Market show moderate growth driven by increasing energy demand and industrial expansion. Coal usage remains important for power generation and cement production in select countries with limited alternative energy infrastructure. In Latin America, resource availability supports domestic consumption and exports, while in Middle East & Africa, growing electrification and infrastructure development continue to create steady demand for coal across emerging economies.

Coal Mining Market Competitive Landscape:

BHP Group Limited – Company Overview

BHP Group Limited is one of the world’s largest mining companies, producing key commodities including iron ore, copper, and metallurgical coal. The company focuses on high-quality resource extraction, operational efficiency, and portfolio optimization to maintain long-term value. BHP’s coal operations primarily support global steelmaking demand, with a strategic emphasis on productivity improvements and disciplined asset management. The company is also advancing mine transition planning, integrating sustainability initiatives and energy transition strategies across its mining operations.

-

2025: BHP reported increased steelmaking coal production driven by strong mining rates at Broadmeadow and improved stripping performance, reflecting operational efficiency and resilient global metallurgical coal demand.

-

2025: BHP announced a pumped hydro study at Mt Arthur Coal, supporting long-term mine transition planning while continuing mining operations through 2030.

-

2024: BHP completed divestment of Blackwater and Daunia metallurgical coal mines, streamlining its portfolio and focusing on higher-value mining assets.

-

2024: BHP progressed approvals to extend Mt Arthur Coal operations to 2030, enabling continued production with structured closure planning and reduced mining rates.

Coal India Limited

Coal India Limited is the world’s largest coal-producing company, supplying thermal coal primarily for power generation and industrial applications. The company plays a critical role in supporting energy security through large-scale mining operations across India. Coal India focuses on expanding production capacity, improving mechanization, and strengthening logistics infrastructure. Its initiatives aim to enhance coal evacuation efficiency, reduce supply bottlenecks, and meet rising domestic demand from power plants and industrial sectors.

-

2023: Coal India invested in first-mile connectivity projects to improve coal evacuation efficiency, reducing transportation bottlenecks and strengthening supply reliability for power and industrial sectors.

Anglo American plc

Anglo American plc is a diversified mining company producing commodities including diamonds, platinum, copper, and metallurgical coal. Its steelmaking coal operations are primarily located in Australia, supporting global steel production. The company focuses on productivity optimization, operational efficiency, and strategic portfolio management to enhance long-term value. Anglo American aligns its coal business with evolving market demand, emphasizing cost efficiency, sustainable mining practices, and optimized asset utilization across its global operations.

-

2024: Anglo American updated its metallurgical coal strategy, focusing on productivity improvements and asset optimization aligned with long-term steelmaking coal demand trends.

-

2023: Anglo American reported strong steelmaking coal performance, supported by improved mining productivity and operational efficiencies across its Australian operations.

Peabody Energy Corporation

Peabody Energy Corporation is a leading coal producer supplying both thermal and metallurgical coal to global markets. The company operates mining assets across the United States and Australia, serving power generation and steelmaking industries. Peabody focuses on cost optimization, operational efficiency, and production growth to meet global coal demand. Its strategy includes enhancing mine productivity, expanding export capabilities, and maintaining a strong presence in seaborne coal markets.

-

2024: Peabody improved operations across its coal portfolio, increasing production volumes and optimizing costs to meet global thermal and metallurgical coal demand.

-

2023: Peabody expanded seaborne metallurgical coal shipments, supported by strong steel industry demand and improved productivity across Australian mining operations.

Teck Resources Limited

Teck Resources Limited is a Canadian resource company focused on mining and mineral development, with a strong presence in steelmaking coal production. The company supplies metallurgical coal to global steel producers, emphasizing operational efficiency and value optimization. Teck continues to strengthen its coal business through productivity improvements and strategic evaluations of its mining assets. Its operations are aligned with global demand for steelmaking materials while maintaining a focus on sustainability and responsible mining practices.

-

2024: Teck advanced its steelmaking coal business through operational improvements and strategic evaluations, focusing on production efficiency and value optimization.

-

2023: Teck reported strong metallurgical coal production, supported by improved operational performance and favorable market conditions.

Coal Mining Companies are:

-

Rio Tinto Group

-

Glencore plc

-

China Shenhua Energy Company Limited

-

Coal India Limited

-

Peabody Energy Corporation

-

Arch Resources Inc.

-

Teck Resources Limited

-

Yankuang Energy Group Company Limited

-

Shaanxi Coal Industry Company Limited

-

China Coal Energy Company Limited

-

PT Bumi Resources Tbk

-

PT Bayan Resources Tbk

-

PT Alamtri Resources Indonesia Tbk

-

Sasol Limited

-

Jindal Steel & Power Limited

-

NTPC Limited

-

Bogatyr Komir

-

ČEZ Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 780.06 Million |

| Market Size by 2035 | USD 977.24 Million |

| CAGR | CAGR of 2.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Thermal Coal, Coking Coal) • By Method (Surface Mining, Underground Mining, In-situ Gasification) • By Application (Power Generation, Steel Production, Cement Manufacturing, Industrial Heating, Chemical & Synthetic Fuels, Others) • By End-User Industry (Utilities (Power Plants), Industrial (Steel, Cement, Manufacturing), Residential & Commercial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BHP Group Limited, Rio Tinto Group, Glencore plc, China Shenhua Energy Company Limited, Coal India Limited, Anglo American plc, Peabody Energy Corporation, Arch Resources Inc., Teck Resources Limited, Yankuang Energy Group Company Limited, Shaanxi Coal Industry Company Limited, China Coal Energy Company Limited, PT Bumi Resources Tbk, PT Bayan Resources Tbk, PT Alamtri Resources Indonesia Tbk, Sasol Limited, Jindal Steel & Power Limited, NTPC Limited, Bogatyr Komir, ČEZ Group. |

Frequently Asked Questions

Asia Pacific dominated the Coal Mining Market in 2025.

The Power Generation segment dominated the Coal Mining Market in 2025.

Rising global electricity demand and continued dependence on coal-based power generation ensure steady consumption despite increasing renewable energy integration trends worldwide.

The Coal Mining Market was valued at USD 780.06 million in 2025.

The Coal Mining Market is expected to grow at a CAGR of 2.34% from 2026 to 2035.

Get in Touch