Compounding Chemotherapy Market Report Scope & Overview:

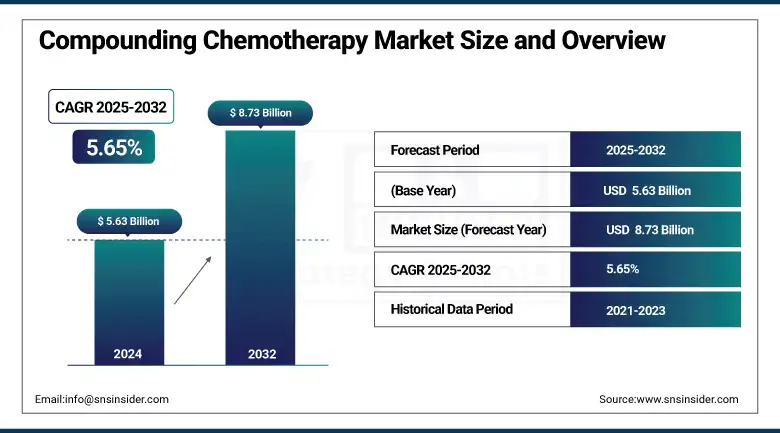

The compounding chemotherapy market size was valued at USD 5.63 billion in 2024 and is expected to reach USD 8.73 billion by 2032, growing at a CAGR of 5.65% over 2025-2032.

Rising prevalence of cancer and demand for a personalized treatment approach, accompanied by a rising need for sterile and safe drug formulations, are propelling the global compounding chemotherapy market. Dose modification requirements, particularly in pediatric and geriatric oncology, are further driving the requirement for compounded chemotherapy services. There is growing evidence that, as of the latest count, close to 60% of oncology treatments are now at levels of drug compounding where treatments need to be mixed or dosages adjusted to tailor regimens for patients.

To Get more information On Compounding Chemotherapy Market - Request Free Sample Report

For instance, Grifols diversified its sterile compounding holdings with investments in oncology infusion centers, and custom chemotherapy dosing solutions are increasingly a focus in the industry.

Moreover, the lack of commercially available chemotherapy drugs is causing a breakdown in the logistics of the supply chain, which is leading healthcare entities to make greater investments in clean rooms. Increasing spending by the government and private sector companies, and a rise in the number of oncology centers in developing countries, are, on the other hand, driving the compounding chemotherapy market growth. Rising USP standards and more FDA approvals are encouraging hospitals to utilize complex compounding technologies. Moreover, there is increased focus on the compounding chemotherapy market analysis with increased R&D spending that has surged over 20% in the last three years in the field of oncology, indicating the industry’s momentum of innovation, maintaining safety, and drug delivery models.

In 2024, Baxter International Inc. partnered with oncology centers in the U.S. to launch robotic IV compounding systems to improve safety and accuracy, marking a fundamental leap in the compounding chemotherapy market growth.

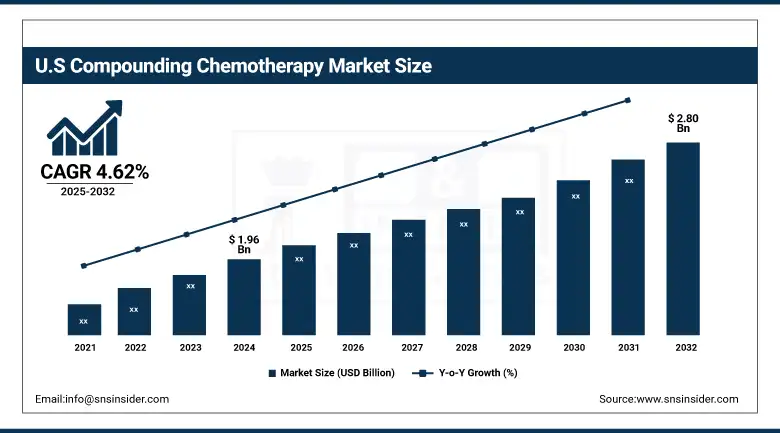

The U.S. compounding chemotherapy market size was valued at USD 1.96 billion in 2024 and is expected to reach USD 2.80 billion by 2032, growing at a CAGR of 4.62% over 2025-2032. The U.S. is a major country and a region driven by over 1.9 million new cases of cancer, as estimated already in 2023 (American Cancer Society), as well as the strong presence of oncology centers and compounding pharmacies. Rising investments in oncology R&D (over USD 20 billion per year) also add to market maturity. Healthcare facilities in Canada are increasingly adopting compounding automation for hospital pharmacies, whereas in Mexico, urban cancer treatment centers are proliferating. Mexico is the fastest-growing region in North America, benefiting from increased public health investment and growing access to compounding infrastructure in tier-1 hospitals.

Table: Top Compounded Chemotherapy Drugs by Frequency (2024)

|

Drug Name |

Primary Use |

Frequency of Compounding (Approximate %) |

|

Cyclophosphamide |

Breast, Lymphoma |

18% |

|

Methotrexate |

Leukemia, Breast |

15% |

|

5-Fluorouracil (5-FU) |

Colorectal, Gastric Cancers |

14% |

|

Paclitaxel |

Lung, Breast |

12% |

|

Dexamethasone |

Supportive Care |

10% |

Market Dynamics:

Drivers:

-

Rising Cancer Burden, Customization Demand, and Regulatory Push Fuel Market Expansion

The growth of the compounding chemotherapy market is significantly attributed to the increase in global cancer prevalence that exceeds 20 million new incident cases annually (WHO, 2023), resulting in requirements for personalized treatment protocols. One-size-fits-all chemotherapy drugs of the past typically fall short in addressing the unique needs of patients, particularly in pediatric and geriatric populations, and are driving demand for compounding chemotherapy solutions.

Rising healthcare spending and government initiatives for improving oncology care are also contributing to the adoption. Additionally, hospitals are building in-house compounding units because of increased drug shortages. The U.S. FDA recorded 130+ shortages of oncology drugs in just the last five years. Furthermore, significant investments are being made in automated sterile compounding systems, which are enhanced in both technology and AI to prevent human error. Oncology R&D costs have escalated beyond USD 75 billion globally, improving the pipeline of novel chemotherapeutic agents that often must be compounded to induce their effects. Regulatory changes, including USP and USP, are also driving the market by requiring strict handling and compounding practices, forcing healthcare facilities to upgrade and stay compliant. This structural shift and advancements in technology will continue to bolster the compounding chemotherapy industry outlook over the years ahead.

Restraints:

-

Infrastructure Gaps, Skilled Labor Shortage, and High Setup Costs Limit Market Penetration

The compounding chemotherapy market, while showing growth potential, still has certain operational and economic limitations. The main hurdle is the absence of sophisticated aseptic compounding facilities, particularly in low- and middle-income countries, where such control of cleanrooms, isolators, and laminar airflow hoods is scarce. For a compliant sterile compounding room, the initial cost can be upwards of USD 1.5 million, and this includes equipment, software, and staff training, a huge financial burden for a smaller hospital or an independent oncology clinic. Additionally, the market is restricted due to a lack of trained compounding pharmacists and technicians in hazardous drug handling.

One in three or more healthcare facilities are struggling to find pharmacists with the skills needed to fill oncology compounding positions, according to the American Society of Health-System Pharmacists (ASHP). Furthermore, adherence to new regulations, such as USP, is economically costly and documentation-heavy, thereby disincentivizing implementation in low‐resource settings. Supply chain inconsistencies, particularly with high-quality API-sourcing (active pharmaceutical ingredients), add to production cycle pressures. Together, all of these factors put the brakes on the adoption curve, especially in the emerging markets, and they could temper the compounding chemotherapy market-share-growth even as global demand mounts.

Segmentation Analysis:

By Drug Type

In 2024, cytotoxic agents were leading with a 42% compounding chemotherapy market share because of their long-standing history across several indications and established clinical efficacy. Such drugs are often compounded for dosage adaptation, especially in children. The rate of growth for targeted therapies is the most rapid, as the market continues to expand, as more personalized oncology treatments are approved, and precision dosing is required. Advancements in biomarker-driven therapies and companion diagnostics have led to an increase in personalized compounding and are thus the prime reasons contributing to the key market driver for this segment for the future compounding chemotherapy market.

By Compounding Method

Aseptic compounding held the largest share of the compounding chemotherapy market analysis in 2024. This is mainly due to the requirement of sterile products in intravenous chemotherapy and mandates governing the quality and storage of compounded drugs through USP and Pharmaceutical companies invest billions in clean rooms, isolators, and automation to comply, overcoming the risk of contamination. This is also the fastest-growing segment, driven by strict safety regulations, particularly with high-risk oncology drugs. Focus on minimization of medication errors, enhancement of drug safety continues to drive investments in aseptic compounding technologies.

By Cancer Type

Breast cancer was the leading segment in 2024 due to the high prevalence of breast cancer globally and an increase in the utilization of compounded hormonal and targeted therapy for each stage of the cancer. This is primarily based on customized treatment schedules and a regimen that is maintained long-term. At the same time, lung cancer, on the other hand, has dynamically become the fastest-growing segment, with the rising incidence of non-small cell lung cancer and the increasing use of targeted agents such as the EGFR and the ALK inhibitors, in need of tailored compounding to guarantee effective, patient-specific dosing.

By Route of Administration

The Intravenous segment was the largest in 2024, with 61% compounding chemotherapy market share, since the majority of cytotoxic and supportive care agents are administered intravenously to allow for immediate bioavailability and effectiveness. The hospital inpatient environment still depends predominantly on IV compounding for safety and sterility. The fastest-growing administration pathway is the oral route, due to the rising availability of oral CHM (chemotherapy drugs), better patient compliance, and greater demand for home care. Pharmacy-directed oral compounding 34 Pharmaceutical compounding allows dose variability, which can be important for pediatric and geriatric oncology patients.

By Distribution Channel

In 2024, hospital pharmacies led with a share of 54% in the compounding chemotherapy market due to more advanced sterile compounding capabilities and better-prepared, trained personnel to handle hazardous chemotherapy medications. Stronger regulations and increasing drug shortages are behind the drive for in-house compounding.

Online pharmacies are the fastest-growing segment, as they profit from surging online consultations between patients and doctors, home cancer treatments, and better logistics. These delivery systems may be particularly beneficial for oral and adjunctively compounded therapies made available directly to patients, thereby creating an increase in convenience and patient access.

Regional Analysis:

The compounding chemotherapy market was led by North America in 2024 due to well well-developed healthcare sector, high burden of cancer, and stringent regulatory compliances, such as USP. The market was dominated by the region, attributed to higher uptake of sterile compounding facilities and automation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is a significant market in the compounding chemotherapy market share, as it is well supported by the government, has centralized healthcare systems, and has a more mature patient base for chronic cancer conditions. Germany tops the region in 2024, due to the established and concurrent established oncology landscape in the country, and the adoption of sterile compounding practices in large hospitals. There were more than 500,000 new cancer cases reported in 2023 in Germany, and the compounding regulations in Germany are very stringent for patient safety. The UK and France are other leading contributors, with the UK’s NHS leading on compounding robotics to enhance cancer care delivery. Poland is the fastest-growing market in the region because of the extensive modernization of hospital pharmacies and increased government allocation for oncology services. The rise in the number of physicians adopting compounding services in Eastern Europe (Turkey included) is anticipated to outpace that of Western countries due to growing private investments.

Asia Pacific is expected to be the fastest-growing market in the compounding chemotherapy market trends due to the increasing number of cancer patients, increasing access to healthcare, as well as the increasing trend of personalized treatments. China leads the regional market on account of the highest number of cancer cases globally, which was more than 4.5 million in 2023, and increasing investments in hospital pharmacy automation and oncology research. China’s National Health Commission is meanwhile pushing for higher standards of chemotherapy compounding in public hospitals. India is moving ahead fast with an increase in the demand for dose-specific cancer treatment, and with the government initiatives for cancer screening. Japan makes another major contribution with its mature population and high use of tailor-made chemotherapy. South Korea and Australia are adopting robotic IV compounding solutions, fostering regional compounding chemotherapies market growth.

Table: Regulatory Compliance Timeline – Key Guidelines by Region

|

Region |

Guideline Implemented |

Year of Enforcement |

Primary Focus |

|

U.S. |

USP <800> |

2023 |

Hazardous Drug Handling |

|

Europe |

EU GMP Annex 1 |

2023 |

Sterile Manufacturing Standards |

|

Asia-Pacific |

China GMP Amendment |

2024 |

Oncology Drug Compounding |

|

Latin America |

ANVISA Update (Brazil) |

2023 |

Chemotherapy Compounding Safety |

Key Players:

Prominent compounding chemotherapy companies operating in the market include Fresenius Kabi AG, Baxter International Inc., Fagron NV, B. Braun Melsungen AG, Medisca Inc., Advanced Pharma Inc., McGuff Compounding Pharmacy Services Inc., Central Admixture Pharmacy Services Inc. (CAPS), PharMEDium Services LLC (AmerisourceBergen), and Dougherty's Holdings Inc.

Recent Developments:

-

In May 2025, Baxter International Inc. posted a 5% year-over-year increase in global sales (totaling USD 2.63 billion) and raised its full-year EPS forecast. The performance reflects robust demand for its Medical Products & Therapies, including compounding syringes and infusion systems.

-

In August 2024, Fresenius Kabi was honored with the Premier Inc. Trailblazer Award for innovative and resilient U.S. supply chain management. This recognition highlights its strengthened capacity in sterile injectables and oncology drug delivery.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.63 billion |

| Market Size by 2032 | USD 8.73 billion |

| CAGR | CAGR of 5.65% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Type (Cytotoxic Drugs, Hormonal Agents, Immunomodulatory Agents, Targeted Therapies, and Supportive Care Drugs) • By Compounding Method (Aseptic Compounding, Non-aseptic Compounding) • By Cancer Type (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Leukemia, Lymphoma, and Other Specific Cancer Types) • By Route of Administration (Intravenous (IV), Oral, Subcutaneous (SC), Intramuscular (IM), and Intrathecal (IT)) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Fresenius Kabi AG, Baxter International Inc., Fagron NV, B. Braun Melsungen AG, Medisca Inc., Advanced Pharma Inc., McGuff Compounding Pharmacy Services Inc., Central Admixture Pharmacy Services Inc. (CAPS), PharMEDium Services LLC (AmerisourceBergen), and Dougherty's Holdings Inc. |

Frequently Asked Questions

Strict guidelines like USP <800> have increased the demand for sterile infrastructure and automated compounding systems to safely manage injectable oncology drugs and hazardous agents.

Major compounding chemotherapy companies include Baxter International, Fresenius Kabi, Fagron NV, Medisca, and CAPS, all focusing on enhancing safe and compliant oncology compounding operations.

The compounding chemotherapy market analysis shows strong growth potential driven by technological upgrades, regulatory alignment (e.g., USP <800>), and expanding oncology-focused compounding services worldwide.

Key pharmaceutical compounding trends include the use of robotic systems for sterile compounding, the adoption of AI in workflow optimization, and increasing demand for home-based chemotherapy care.

Key growth drivers include the rise in cancer treatment demand, increasing drug shortages, and the push for safer, sterile chemotherapy mixing standards, especially for high-risk injectable oncology drugs.

Get in Touch