Corrosion Inhibitors Market Report Scope & Overview:

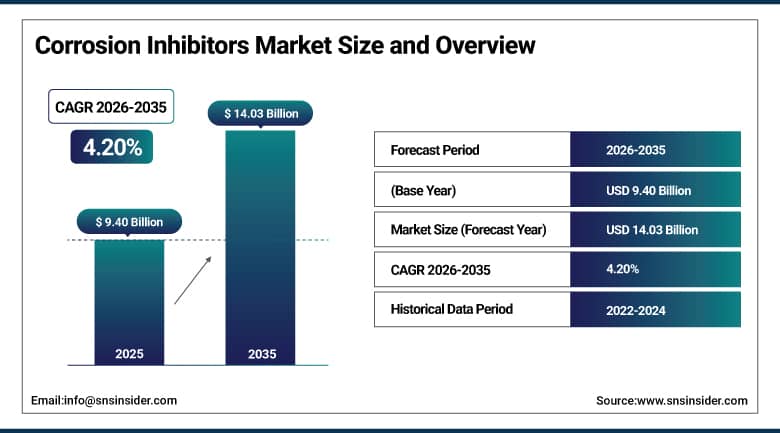

The Corrosion Inhibitors Market was valued at USD 9.40 Billion in 2025 and is expected to reach USD 14.03 Billion by 2035, growing at a CAGR of 4.20% from 2026 to 2035.

The Corrosion Inhibitors Market is growing due to increasing demand from various industries such as oil and gas industry, power industry and industrial processes industry, in which protection of their equipment is crucial to minimize the costs of maintenance and downtimes. Increased infrastructural developments and expansion of water treatment plants will further fuel the demand for corrosion inhibitors. Industrialization in developing nations is also making companies more vulnerable to losses arising out of corrosion, thereby increasing the need for preventive chemicals. Stricter government norms regarding environment safety are also pushing the market forward.

According to the National Association of Corrosion Engineers (NACE), the global cost of corrosion is estimated at approximately USD 2.5 trillion annually, accounting for around 3–4% of global GDP, highlighting the critical importance of effective corrosion prevention and control measures across industries. Furthermore, the International Energy Agency (IEA) reports that global energy investment exceeded USD 2.8 trillion in 2023, with a significant share allocated to oil and gas infrastructure, pipelines, refineries, and power systems, all of which require advanced corrosion protection solutions to ensure operational reliability, safety, and asset longevity.

Market Size and Forecast

-

Market Size in 2026E: USD 9.80 Billion

-

Market Size by 2035: USD 14.03 Billion

-

CAGR: 4.20% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Corrosion Inhibitors Market - Request Free Sample Report

Corrosion Inhibitors Market Trends

-

Rising demand from oil & gas, marine, and petrochemical industries to protect infrastructure and equipment from harsh environmental degradation

-

Growing use in industrial manufacturing and processing plants to extend asset life, reduce maintenance costs, and improve operational efficiency

-

Increasing adoption in construction and infrastructure projects to enhance durability of reinforced concrete and metal structures

-

Expanding application in water treatment systems and power generation facilities to prevent scaling, rust formation, and system failures

-

Continuous development of eco-friendly and low-toxicity corrosion inhibitor formulations supporting environmental compliance and sustainability goals

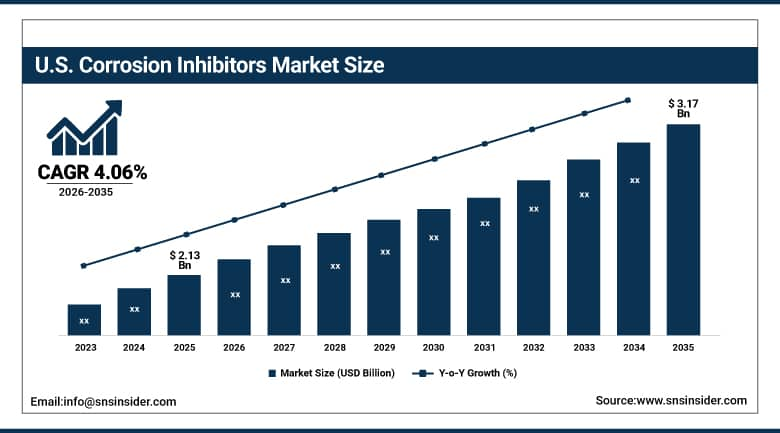

The U.S. Corrosion Inhibitors Market Outlook

The U.S. Corrosion Inhibitors Market was valued at approximately USD 2.13 Billion in 2025 and is expected to reach approximately USD 3.17 Billion by 2035, growing at a CAGR of approximately 4.06%.

The United States is the world's largest national corrosion inhibitors market owing to the local oil and gas production industry, which uses corrosion inhibitors in its pipelines, refineries, and production facilities and has the biggest demand for them among all industries; the aging water distribution infrastructure, where EPA Lead and Copper Rule dictates the need for corrosion inhibitors; and the automotive manufacturing industry, where corrosion inhibitors are used for surface treatments of vehicles made of steel and aluminum.

Corrosion Inhibitors Market Segment Analysis

-

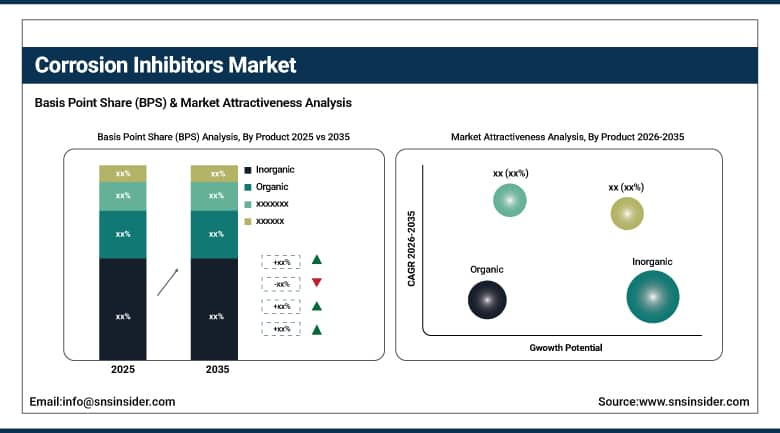

By Product, inorganic segment dominated the Corrosion Inhibitors Market in 2025 with 57% share; organic segment is the fastest growing segment.

-

By Type, water-based segment dominated the market in 2025 with 61% share; oil-based segment is the fastest growing segment.

-

By End Use, oil and gas segment dominated the market in 2025 with 38% share; water treatment segment is the fastest growing segment.

By Product, Inorganic segment dominates the Corrosion Inhibitors Market, Organic segment expected to grow fastest

The inorganic segment dominated the Corrosion Inhibitors Market due to its highly effective nature against metal surfaces exposed to harsh industrial environments. They are extensively utilized in the oil and gas industry, power plants, and heavy manufacturing industries owing to their high temperature and pressure environment. The highly cost-effective, lasting protection and proven efficiency of these inhibitors in inhibiting rusting and corrosion in large infrastructures are some reasons that have increased their dominance in the market.

The organic segment is the fastest growing in the Corrosion Inhibitors Market due to growing demand for eco-friendly and degradable solutions. Strict environmental regulations and increasing environmental consciousness is making industries move towards less toxic materials. Organic inhibitors are more safe and eco-friendly as well as compatible with modern industrial requirements. Increased applications in water treatment, oilfield chemicals, and industrial systems are other factors driving the fast-paced growth of this segment.

By Type, Water-based segment dominates the Corrosion Inhibitors Market, Oil-based segment expected to grow fastest

The water-based segment dominated the Corrosion Inhibitors Market owing to the high applicability of these inhibitors in industries such as industrial cooling systems, boilers, and water treatments. These inhibitors are highly preferred because they offer an environment-friendly solution, easy application process, and prevention from corrosion in water medium. The increased demand in power generation, oil and gas production, and manufacturing sector, along with strict environmental regulations, has boosted the dominance of the segment in the global market.

The oil-based segment is the fastest growing in the Corrosion Inhibitors Market owing to increasing demand in the oil and gas industry. These inhibitors offer superior performance in the non-aqueous medium and under difficult conditions. Increasing global energy consumption, expanding upstream exploration of oil and gas, and focus on asset protection have boosted the demand for oil-based corrosion inhibitors.

By End Use, Oil & Gas segment dominates the Corrosion Inhibitors Market, Water Treatment segment expected to grow fastest

The oil and gas segment dominated the Corrosion Inhibitors Market because of wide use of protective chemicals in pipelines, drilling machinery, refineries, and storage facilities. The corrosion protection is crucial in order to provide safety during operation, decrease equipment breakdowns and prolong assets' life time in the conditions of extreme environment. Exploration activities, massive infrastructure development and exposure to corrosive materials led to solid market position of the segment worldwide.

The water treatment segment is the fastest growing in the Corrosion Inhibitors Market owing to increase in the need for water treatment, wastewater treatment, and industrial effluents. Urbanization, strict environmental norms, and investment in infrastructure development have fueled adoption of this segment. Corrosion inhibitors help in protecting pipelines and treatment facilities along with making the operation efficient and providing quality water.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

42.84% |

|

Middle East & Africa |

Saudi Arabia |

27.84% |

|

Latin America |

Brazil |

43.84% |

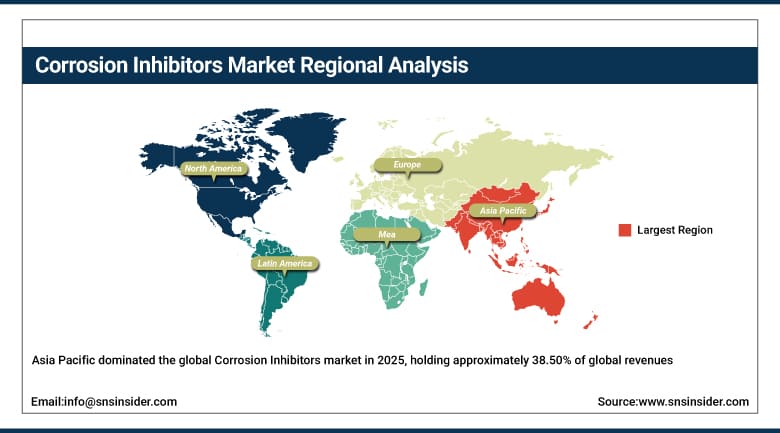

Asia Pacific Corrosion Inhibitors Market Insights

Asia Pacific dominated the global Corrosion Inhibitors market in 2025, holding approximately 38.50% of global revenues, and is projected to maintain its regional leadership while also representing the fastest-growing market through 2035. China accounts for approximately 42.84% of Asia Pacific revenues through its massive manufacturing and industrial base encompassing steel production, chemical processing, power generation, oil and gas infrastructure, and automotive manufacturing whose collective metallic asset base creates the world's largest total corrosion inhibitor demand market.

India is growing particularly rapidly through its accelerating industrial development, expanding oil and gas pipeline network, growing automotive production, and water infrastructure investment. Japan and South Korea contribute sophisticated specialty inhibitor demand through their petrochemical, semiconductor, and precision manufacturing industries.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Corrosion Inhibitors Market Insights

North America held approximately 27.84% of global Corrosion Inhibitors revenues in 2025. The United States accounts for approximately 84.73% of regional revenue through its oil and gas production sector creating the region's largest single industry inhibitor demand, its extensive water distribution infrastructure requiring corrosion control treatment, and its automotive and construction industries whose metal protection requirements sustain broad-based specialty inhibitor demand.

The Infrastructure Investment and Jobs Act's water infrastructure funding is stimulating municipal water utility corrosion control investment that incrementally expands the addressable inhibitor market in drinking water distribution applications. Canada contributes meaningful regional demand through its oil sands and conventional oil and gas operations, pipeline network maintenance, and mining industry applications.

Europe Corrosion Inhibitors Market Insights

Europe held approximately 22.84% of global Corrosion Inhibitors revenues in 2025. Germany accounts for approximately 27.84% of European revenues through its automotive manufacturing sector's metal surface treatment requirements, chemical processing industry, and industrial machinery maintenance operations that collectively sustain large-volume specialty corrosion inhibitor demand.

The European Union's REACH regulation and water discharge standards are driving significant reformulation investment across European corrosion inhibitor manufacturers whose product portfolios must progressively eliminate or replace restricted substances including hexavalent chromium, certain phosphate compounds, and specific biocide active substances. The United Kingdom, France, the Netherlands, and Italy each contribute meaningful European demand through their refining, chemical, and power generation industries.

MEA & Latin America Corrosion Inhibitors Market Insights

Middle East and Latin America are substantial and growing Corrosion Inhibitors markets where oil and gas production dominates application demand. Saudi Arabia leads MEA revenues at approximately 27.84% of the regional total through Aramco's massive oil production and processing infrastructure whose pipelines, storage tanks, refineries, and desalination plants collectively represent one of the world's largest concentrations of corrosion-susceptible metallic assets requiring continuous inhibitor treatment programme maintenance.

UAE, Kuwait, Iraq, and Algeria each contribute meaningful MEA demand through their oil and gas infrastructure. Brazil leads Latin American revenues at approximately 43.84% of the regional total through Petrobras's extensive deepwater oil production and pipeline infrastructure whose pre-salt crude chemistry creates demanding corrosion conditions.

Market Dynamics

Growth Drivers: Oil and gas expansion and aging water networks drive strong corrosion inhibitor demand globally.

The capital expenditure for developing new production facilities within the international oil and gas industry, such as deepwater oil wells, LNG receiving terminals, long-distance transport pipelines, as well as refinery facilities development programs, will result in the corresponding inhibitor demand, which will be tied to the volume of chemical application required to combat the aggressive nature of production processes. The estimate provided by the International Energy Agency for continued fossil fuels production until the 2030s even in energy transition scenarios guarantees that oil and gas corrosion inhibitors will remain a structural market segment during the forecast period.

The aging infrastructure of water supply networks within North America and Europe, with much of the existing pipe infrastructure being at least 50 years old and subject to corrosion, is an additional driver of inhibitor demand among municipal water companies with increasing budgets allocated for treatment.

Restraints: Regulatory limits on toxic chemicals increase reformulation costs and restrict traditional inhibitor usage

Hexavalent chromium, which has long been one of the most effective inhibitors of anodic corrosion for aluminum and steel substrates, is being increasingly banned by European Union REACH regulation, U.S. EPA requirements, and other similar Asian environmental requirements because of its status as a carcinogen and its environmental persistence.

Inhibitor replacement with alternatives to chromate inhibitors has taken many years to develop and test the efficacy in aerospace, automotive, and military applications where chromate conversion coatings have almost universal usage. Phosphate-based inhibitors used extensively in cooling water and residential hot water applications are now subject to more stringent permitting controls in certain jurisdictions where phosphate pollution from industrial cooling water blowdown results in surface water eutrophication.

Opportunities: Bio-based inhibitors and IoT-enabled dosing create advanced, efficient, and sustainable market opportunities

Corrosion inhibitors derived from plant extracts and biomass, such as those derived from natural oils, tannins, amino acids, and polyphenols, are receiving greater commercial and regulatory attention as greener substitutes for synthetic organic inhibitors, which are under increased scrutiny in regulatory assessment frameworks in terms of their ecotoxicological characteristics.

In laboratory studies, some corrosion inhibiting chemicals derived from plants have been found to provide corrosion inhibition efficiency levels above 90 percent, and commercially available plant extract inhibitors are being introduced into cooling water, mild acid pickling, and oil and gas pipelines for treatment where differentiation on the basis of environmental profile allows for higher pricing. IoT-based corrosion monitoring systems capable of measuring corrosion rate in real time and making dynamic adjustments to inhibitor dosing save up to 15 to 30 percent of inhibitor usage compared to static dosing without sacrificing performance.

Recent Developments:

-

2025: Cortec Corporation confirmed record expansion of its VpCI Volatile Corrosion Inhibitor product line due to growing adoption in offshore oil rig pipeline maintenance in the Gulf of Mexico, with the vapour-phase protection mechanism enabling effective corrosion prevention in enclosed equipment geometries where direct liquid inhibitor application is operationally impractical.

-

2025: ICL Group launched three new sustainable corrosion inhibitor products at the European Coatings Show including a phosphate-free cooling water inhibitor, a biodegradable pipeline treatment product, and a non-chromate aluminium surface pre-treatment inhibitor addressing regulatory restrictions on chromate and phosphate compounds in major European market applications.

-

2024: BASF SE expanded its Korrostabil corrosion inhibitor product line with new formulations targeting electric vehicle manufacturing including battery pack enclosure protection, high-voltage connector surface treatment, and aluminium body structure corrosion prevention meeting OEM supplier specifications for the growing EV assembly supply chain.

Corrosion Inhibitors Market Key Players are:

-

BASF SE

-

The Dow Chemical Company

-

Solenis LLC

-

Ecolab Inc.

-

Ashland Global Holdings Inc.

-

Henkel AG & Co. KGaA

-

Lubrizol Corporation

-

Clariant AG

-

Nouryon

-

Solvay S.A.

-

Elementis plc

-

ChampionX Corporation

-

Nalco Water (Ecolab subsidiary)

-

Italmatch Chemicals S.p.A.

-

SUEZ Water Technologies & Solutions

-

Cortec Corporation

-

DAK Americas LLC

-

Afton Chemical Corporation

-

W. R. Grace & Co.

-

Quaker Houghton

Corrosion Inhibitors Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.40 Billion |

| Market Size by 2035 | USD 14.03 Billion |

| CAGR | CAGR of 4.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Composition (Organic, Inorganic) • By Type (Water Based, Oil Based) • By End Use (Oil and Gas, Power Generation, Metal Processing, Water Treatment, Chemical Processing, Paper and Pulp, Other) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, The Dow Chemical Company, Solenis LLC, Ecolab Inc., Ashland Global Holdings Inc., Henkel AG & Co. KGaA, Lubrizol Corporation, Clariant AG, Nouryon, Solvay S.A., Elementis plc, ChampionX Corporation, Nalco Water (Ecolab subsidiary), Italmatch Chemicals S.p.A., SUEZ Water Technologies & Solutions, Cortec Corporation, DAK Americas LLC, Afton Chemical Corporation, W. R. Grace & Co., Quaker Houghton |

Frequently Asked Questions

Oil and gas expansion, ageing water systems, industrial growth, EV manufacturing, and IoT dosing technologies drive corrosion inhibitors market growth.

The Corrosion Inhibitors Market was valued at USD 9.40 Billion in 2025.

The Corrosion Inhibitors Market is expected to grow at a CAGR of 4.20% from 2026 to 2035.

Asia Pacific dominated the Corrosion Inhibitors Market in 2025, holding approximately 38.50% of global revenues, with China accounting for approximately 42.84% of Asia Pacific revenues.

The Inorganic compound segment dominated the Corrosion Inhibitors Market.

Get in Touch