Process Cooling Water Pipe Hanger Market Report Scope & Overview:

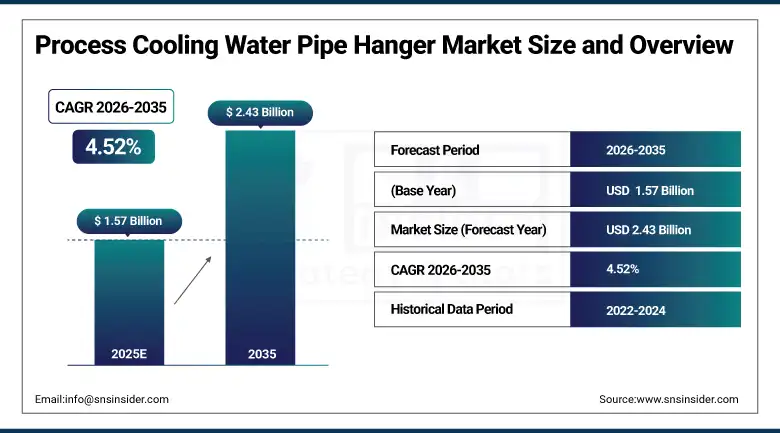

The Process Cooling Water Pipe Hanger Market was valued at USD 1.57 Billion in 2025 and is projected to reach USD 2.43 Billion by 2035, growing at a CAGR of 4.52% during the 2026–2035 forecast period.

Process cooling water pipe hangers support, align, and secure piping systems that carry cooling water across industrial, commercial, and utility settings. Their role is operationally essential poorly supported pipe networks introduce stress concentrations at joints, accelerate fatigue cracking, and create vibration-related failures that are costly to diagnose and repair. Demand is tied directly to the scale and condition of cooling infrastructure across end-use sectors, and that infrastructure is substantial, aging, and actively expanding. Growth through the forecast period reflects new-build activity across data centers, manufacturing plants, and power utilities alongside a meaningful replacement cycle at facilities operating two to three decades of original pipe support hardware. Semiconductor fabrication expansion, AI-driven data center construction, and long-cycle capital programs in the energy sector collectively sustain a broad procurement environment that is unlikely to be disrupted by weakness in any single end-use vertical.

Process Cooling Water Pipe Hanger Market Size and Forecast:

-

Market Size in 2025: USD 1.57 Billion

-

Market Size by 2035: USD 2.43 Billion

-

CAGR: 4.52% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Process Cooling Water Pipe Hanger Market - Request Free Sample Report

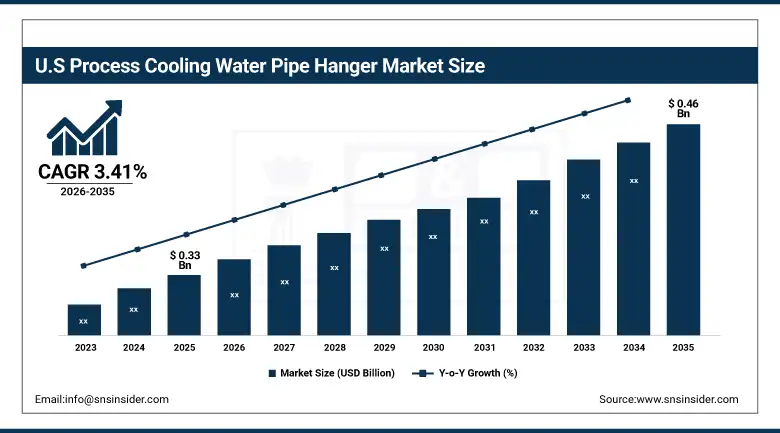

The U.S. Process Cooling Water Pipe Hanger Market was valued at USD 0.33 Billion in 2025 and is projected to reach USD 0.46 Million by 2035, growing at a CAGR of 3.41% during 2026–2035. Demand is driven by manufacturing belt cooling infrastructure, data center investment along major technology corridors, and replacement procurement at power generation facilities built during the 1980s and 1990s expansion programs.

Key Process Cooling Water Pipe Hanger Market Trends:

-

Rising data center construction driven by artificial intelligence, cloud computing, and edge computing workloads is generating significant new procurement of pipe hanger systems to support high-density liquid cooling networks across large-format hyperscale and co-location facilities.

-

Growing preference for stainless steel and polymer-based pipe hangers in pharmaceutical, food processing, and semiconductor cooling applications, where corrosion resistance and contamination control standards rule out standard carbon steel specifications.

-

Increasing adoption of prefabricated and modular pipe support assemblies that reduce on-site labor time, improve installation consistency, and accommodate BIM-integrated design workflows in large commercial and industrial construction projects.

-

Expansion of process cooling infrastructure across Southeast Asian manufacturing hubs, including electronics assembly facilities in Vietnam, Indonesia, and Thailand, is creating meaningful new demand in markets that were not significant for this product category five years ago.

-

Retrofit and upgrade activity at aging industrial facilities in North America and Europe, where original pipe hanger hardware is reaching end of rated service life, is generating replacement procurement volumes that supplement greenfield installation demand across established markets.

Process Cooling Water Pipe Hanger Market Growth Drivers:

-

Rapid Expansion of Data Centers and High-Density Electronics Cooling Is Creating a Sustained New Demand Channel for Pipe Hanger Systems

The growth of data center capacity globally has been exceptional, and cooling infrastructure investment has tracked it closely. High-density server configurations supporting AI training and inference workloads generate thermal loads requiring dense liquid cooling pipe networks that need comprehensive hanger and support systems to manage weight, thermal movement, and vibration under continuous duty. Hyperscale operators across the United States, Europe, and Asia Pacific are commissioning facilities at a pace that maintains consistent procurement demand for pipe support hardware through the entire forecast period.

Process Cooling Water Pipe Hanger Market Restraints:

-

Raw Material Price Volatility and Supply Chain Disruptions Continue to Challenge Margin Stability for Pipe Hanger Manufacturers

Carbon steel and stainless steel account for the majority of materials used in pipe hanger production, and both have experienced significant price swings over 2022–2024 as a result of energy cost increases, trade policy adjustments, and post-pandemic supply chain reconfiguration. Manufacturers operating under fixed-price contracts face margin compression when input costs rise faster than contractual adjustment mechanisms allow. Smaller regional producers with limited hedging capability are particularly exposed, a dynamic that has contributed to industry consolidation in some markets.

Process Cooling Water Pipe Hanger Market Opportunities:

-

Semiconductor Fab Expansion and Pharmaceutical Manufacturing Growth Opening High-Specification Market Segments

Semiconductor fabrication and pharmaceutical manufacturing share demanding requirements for process cooling pipe support systems cleanroom compatibility, corrosion resistance, vibration isolation, and tight installation tolerances that eliminate standard carbon steel catalog products and favor stainless steel, polymer, and specialty alloy solutions at higher unit values. Government-backed semiconductor programs in the United States, Europe, and Asia Pacific are driving fab construction at a scale not seen in decades, with each facility representing a significant multi-system pipe hanger procurement event and the start of a long-cycle maintenance relationship.

Process Cooling Water Pipe Hanger Market Segment Insights

-

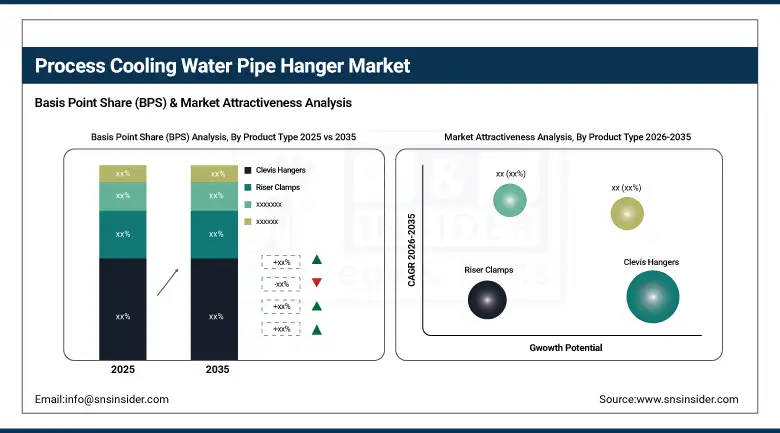

Based on Product Type, Clevis Hangers accounted for the largest market share (~24.6%) in 2025; Riser Clamps segment expected to be the fastest-growing segment (CAGR ~4.96%) through 2035.

-

Based on Material, Carbon Steel accounted for the largest market share (~34.8%) in 2025; Stainless Steel segment expected to be the fastest-growing segment (CAGR ~5.68%) through 2035.

-

Based on Application, Industrial Process Cooling Systems accounted for the largest market share (~30.7%) in 2025; Data Centers & Electronics Cooling segment expected to be the fastest-growing segment (CAGR ~6.03%) through 2035.

-

Based on End-User, Manufacturing & Industrial Plants accounted for the largest market share (~33.5%) in 2025; Data Centers & IT Infrastructure segment expected to be the fastest-growing segment (CAGR ~6.00%) through 2035.

Process Cooling Water Pipe Hanger Market Segmentation Analysis:

Clevis Hangers Lead Product Type Segment While Riser Clamps Register Fastest Growth Through 2035

Clevis Hangers dominated with a 24.6% share in 2025, while Riser Clamps is expected to grow at the fastest CAGR of approximately 4.96% through 2035. Clevis hangers are the most widely specified product type because of their design versatility across pipe diameters, ease of field adjustment, and compatibility with virtually every piping material and insulation configuration encountered in process cooling applications. Riser clamps are growing fastest because vertical pipe support requirements are increasing as facilities move toward multi-story and high-density configurations, particularly in data center and semiconductor fab construction where vertical cooling circuits are integral to system design.

Carbon Steel Leads Material Segment While Stainless Steel Records Fastest CAGR Through 2035

Carbon Steel dominated with a 34.8% share in 2025, while Stainless Steel is expected to grow at the fastest CAGR of approximately 5.68% through 2035. Carbon steel leads because it meets the structural requirements of most general industrial process cooling applications at a cost that makes it the default specification for standard service environments. Stainless steel is growing fastest, driven by expanding demand from pharmaceutical, semiconductor, and high-purity cooling applications where carbon steel is not an acceptable specification, and by a broader trend toward longer-life, lower-maintenance pipe support hardware in facilities that are moving away from five-year hardware replacement cycles.

Industrial Process Cooling Systems Lead Application Segment While Data Centers & Electronics Cooling Grows Fastest

Industrial Process Cooling Systems dominated with a 30.7% share in 2025, while Data Centers & Electronics Cooling is expected to grow at the fastest CAGR of approximately 6.03% through 2035. Industrial process cooling systems represent the largest application because they serve the broadest range of manufacturing, chemical processing, and power generation end-users with extensive and aging cooling infrastructure. Data center and electronics cooling is growing fastest, reflecting new facility construction at scale, high pipe support density per square foot relative to traditional industrial cooling, and above-average specification requirements that favor more durable hanger products.

Manufacturing & Industrial Plants Lead End-User Segment While Data Centers & IT Infrastructure Records Fastest Growth

Manufacturing & Industrial Plants dominated with a 33.5% share in 2025, while Data Centers & IT Infrastructure is expected to grow at the fastest CAGR of approximately 6.00% through 2035. Manufacturing and industrial plants hold the largest end-user share through the depth and breadth of their process cooling installed base across automotive, chemical, metals, and general manufacturing facilities. Data centers are growing fastest because the capital intensity of new facility construction, combined with vibration control and corrosion resistance requirements of liquid cooling serving high-value IT equipment, creates consistent demand for quality pipe support products at procurement volumes growing rapidly year over year.

Process Cooling Water Pipe Hanger Market Regional Analysis:

North America Process Cooling Water Pipe Hanger Market Insights

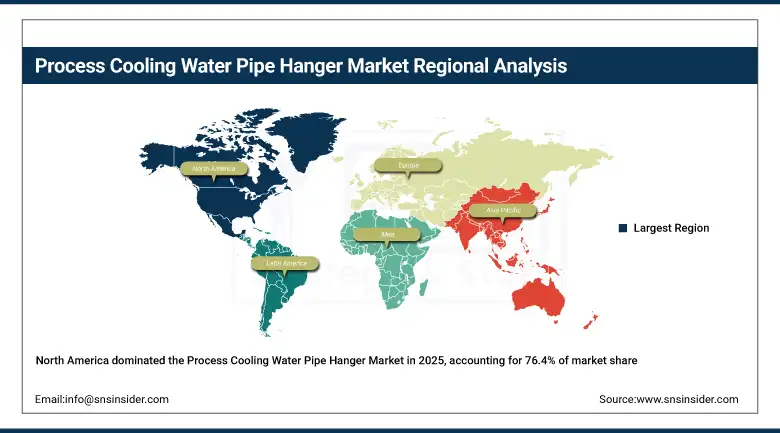

North America Process Cooling Water Pipe Hanger Market was valued at USD 430.18 Million in 2025 and is expected to reach USD 613.41 Million by 2035, growing at a CAGR of 3.64% during the forecast period. Demand is anchored by extensive aging manufacturing infrastructure across the Midwest and Southeast, substantial data center development in Virginia, Texas, and the Pacific Northwest, and long-cycle replacement needs of power generation cooling systems installed under earlier capacity programs.

U.S. Process Cooling Water Pipe Hanger Market Insights

The United States dominates North America with a 76.4% regional share in 2025. Semiconductor manufacturing investment under domestic incentive programs, hyperscale data center expansion, and industrial facility modernization programs sustain consistent procurement through the forecast window.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Process Cooling Water Pipe Hanger Market Insights

Europe Process Cooling Water Pipe Hanger Market was valued at USD 620.21 Million in 2025 and is expected to reach USD 511.17 Million by 2035, growing at a CAGR of 3.98% during the forecast period. Industrial modernization, semiconductor fab investment under the European Chips Act, and data center construction in Germany, the Netherlands, Ireland, and the Nordic countries drive demand. Stringent EU industrial safety standards push pipe support specifications above standard catalog grade across regulated manufacturing and utility applications.

Germany Process Cooling Water Pipe Hanger Market Insights

Germany holds the largest national share in Europe, anchored by its chemical, automotive, and precision manufacturing sectors which operate large process cooling systems requiring ongoing pipe support maintenance. Domestic semiconductor capacity investment and the country's substantial data center market reinforce Germany's regional leadership through the forecast period.

Asia Pacific Process Cooling Water Pipe Hanger Market Insights

Asia Pacific Process Cooling Water Pipe Hanger Market was valued at USD 617.01 Million in 2025 and is expected to reach USD 1,036.95 Million by 2035, growing at the fastest regional CAGR of 5.35% during the forecast period. Manufacturing expansion across China, India, South Korea, Japan, and Southeast Asia, the concentration of global electronics production, and rapidly expanding data center capacity driven by domestic cloud adoption and entry of major U.S. hyperscale operators collectively drive Asia Pacific's growth leadership.

China Process Cooling Water Pipe Hanger Market Insights

China is the dominant national market within Asia Pacific, reflecting its manufacturing scale across electronics, automotive, chemicals, and general industry, the active buildout of domestic data center capacity, and government-driven semiconductor and advanced manufacturing investment requiring high-specification process cooling systems. Domestic producers are competitive at standard specification levels while international suppliers maintain preference in high-specification and certified-material applications.

Latin America and Middle East & Africa Process Cooling Water Pipe Hanger Market Insights

Latin America Process Cooling Water Pipe Hanger Market was valued at USD 100.48 Million in 2025 and is expected to reach USD 153.35 Million by 2035, growing at a CAGR of 4.32% during the forecast period. Brazil, Mexico, and Colombia are the primary demand centers, driven by manufacturing growth, power infrastructure expansion, and selective data center investment serving growing regional digital economy demand. Middle East & Africa Process Cooling Water Pipe Hanger Market was valued at USD 75.36 Million in 2025 and is expected to reach USD 119.27 Million by 2035, growing at a CAGR of 4.70% during the forecast period. Gulf state industrial diversification and sovereign cloud-driven data center investment in the UAE and Saudi Arabia are the primary regional growth drivers.

Competitive Landscape for Process Cooling Water Pipe Hanger Market:

Eaton Corporation operates in the process cooling water pipe hanger market through its B-Line Systems division, which produces one of the broadest pipe support and restraint product ranges available from a single global supplier. The division's catalog covers clevis hangers, riser clamps, swivel ring hangers, U-bolt assemblies, and spring support systems across carbon steel, stainless steel, and galvanized material families. Eaton's global manufacturing footprint and distributor network give it reliable availability across North American, European, and Asia Pacific markets, making it a preferred supplier for large EPC firms managing multi-facility procurement programs

January 2025: Eaton announced the expansion of its B-Line Series 1 stainless steel pipe hanger range, adding fourteen new product configurations for corrosive process cooling environments in pharmaceutical, semiconductor, and food processing facilities. The expansion included new PVDF-lined clevis hanger variants for ultra-high-purity cooling circuits and updated load rating certifications aligned with revised ANSI/MSS SP-69 standards.

Anvil International is a dedicated pipe support and joining products manufacturer whose portfolio is built specifically around the engineering requirements of industrial piping systems, including process cooling water networks across manufacturing, power, and HVAC applications. Its pipe hanger range spans standard catalog items through engineered custom assemblies for seismic restraint, high-temperature service, and vibration isolation. Established relationships with major HVAC and industrial distributors give Anvil broad market access across the United States and Canada, while its technical application support makes it a preferred resource for mechanical contractors specifying pipe support systems in complex cooling applications.

March 2025: Anvil International introduced the CoolFlow Series pipe hangers and clamps engineered specifically for chilled water and process cooling in data centers and electronics cooling facilities. The series features integrated thermal break inserts to reduce condensation-related corrosion at pipe contact points, corrosion-resistant coatings rated for 25-year service life in humid cooling environments, and factory-drilled adjustment slots that reduce installation time relative to field-modified standard hangers. The product line is stocked for immediate delivery from twelve distribution points across the United States.

Key Market Players:

-

Eaton Corporation

-

Walraven Group

-

Hilti Group

-

Piping Technology & Products, Inc.

-

Globe Pipe Hanger Products Inc.

-

PHD Manufacturing, Inc.

-

Gripple Ltd.

-

Rilco Manufacturing Company, Inc.

-

Empire Industries, Inc.

-

Sikla GmbH

-

Carpenter & Paterson Ltd.

-

Bergen Pipe Supports

-

Mason Industries, Inc.

-

Metraflex Company

-

Flex-Strut Inc.

-

Witzenmann GmbH

-

Taylor Pipe Supports

-

Binder Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.57 Billion |

| Market Size by 2035 | USD 2.43 Billion |

| CAGR | CAGR of 4.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Clevis Hangers, Riser Clamps, Split Ring / Swivel Ring Hangers, U-Bolts & Saddle Clamps, and Spring / Adjustable Pipe Hangers) • By Material (Carbon Steel, Stainless Steel, Galvanized Steel, Aluminium, and Plastic / Polymer-Based) • By Application (Industrial Process Cooling Systems, HVAC & Chilled Water Systems, Data Centers & Electronics Cooling, Power Generation Plants, and Chemical & Petrochemical Plants) • By End-User Industry (Manufacturing & Industrial Plants, Energy & Power Utilities, Data Centers & IT Infrastructure, Oil & Gas / Petrochemical Industry, and Commercial Buildings & Infrastructure) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Eaton Corporation; Anvil International; Walraven Group; Hilti Group; Piping Technology & Products, Inc.; Globe Pipe Hanger Products Inc.; PHD Manufacturing, Inc.; National Pipe Hanger Corporation; Gripple Ltd.; Rilco Manufacturing Company, Inc.; Empire Industries, Inc.; Sikla GmbH; Carpenter & Paterson Ltd.; Bergen Pipe Supports; Mason Industries, Inc.; Metraflex Company; Flex-Strut Inc.; Witzenmann GmbH; Taylor Pipe Supports; Binder Group. |

Frequently Asked Questions

The Process Cooling Water Pipe Hanger Market is expected to grow at a CAGR of 4.52% from 2026-2035.

The Process Cooling Water Pipe Hanger Market size was USD 1.57 Billion in 2025 and is expected to reach USD 2.43 Billion by 2035.

Rising industrialization infrastructure expansion and growing demand for efficient process cooling systems drive market growth.

Carbon Steel dominated the Process Cooling Water Pipe Hanger Market.

Europe dominated the Process Cooling Water Pipe Hanger Market in 2025.

Get in Touch