D-Dimer Testing Market Report Scope & Overview:

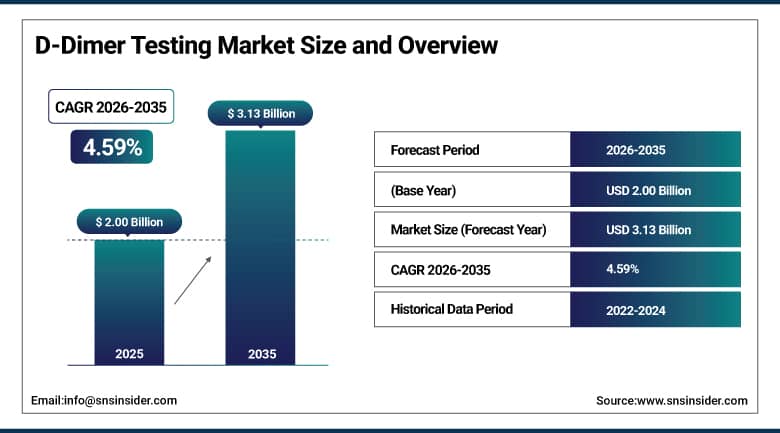

The D-Dimer Testing Market was valued at USD 2.00 Billion in 2025 and is expected to reach USD 3.13 Billion by 2035, growing at a CAGR of 4.59% from 2026 to 2035.

The D-dimer Testing Market is experiencing steady growth owing to the increase in the number of patients with thrombotic diseases like DVT, PE, and DIC. Awareness about early detection of diseases, use of Point of Care Testing (POCT) and increased usage of D-dimer tests in emergency and critical care units is propelling the growth of the market. With technological progress in the area of immunoassay techniques and coagulation analyzers, there has been an improvement in the efficiency of the tests. Besides, the aging population, rising admissions and increased diagnostic services are some other factors that will drive the growth of the market.

According to the World Health Organization, cardiovascular diseases account for approximately 17.9 million deaths annually worldwide, making them the leading cause of mortality globally. A significant proportion of cardiovascular and thrombotic conditions require D-dimer testing for diagnosis, exclusion of thromboembolic events, and risk assessment. Furthermore, the International Society on Thrombosis and Haemostasis estimates that venous thromboembolism (VTE), including DVT and pulmonary embolism, affects nearly 10 million people globally each year, highlighting the growing need for effective coagulation diagnostics. In addition, Siemens Healthineers states that D-dimer testing remains one of the most widely utilized coagulation diagnostic tools in emergency departments due to its high negative predictive value in ruling out thromboembolic diseases, further supporting its widespread adoption across healthcare settings.

D-Dimer Testing Market Size and Forecast:

-

Market Size in 2026E: USD 2.09 Billion

-

Market Size by 2035: USD 3.13 Billion

-

CAGR: 4.59% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

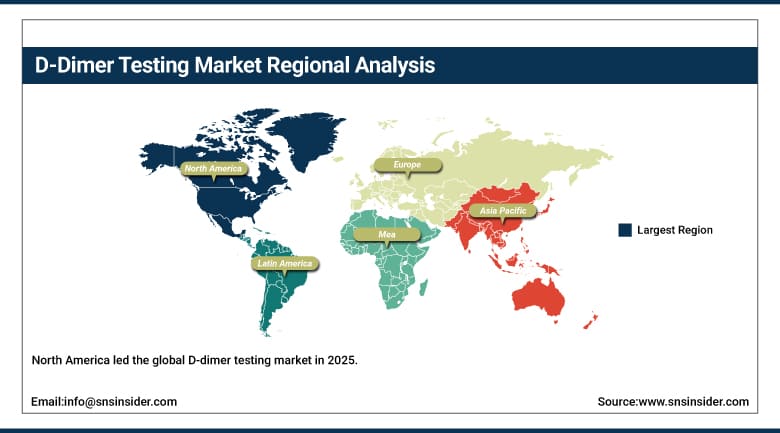

Largest Region: North America

To Get More Information On D-Dimer Testing Market - Request Free Sample Report

D-Dimer Testing Market Trends:

-

Rising prevalence of thrombotic disorders such as deep vein thrombosis (DVT) and pulmonary embolism (PE) driving demand for D-dimer diagnostic testing

-

Growing adoption of rapid and point-of-care testing solutions enabling faster diagnosis and clinical decision-making in emergency and critical care settings

-

Increasing use of D-dimer tests in the assessment and monitoring of coagulation abnormalities, cardiovascular diseases, and postoperative complications

-

Expanding healthcare awareness and preventive screening initiatives supporting early detection of blood clot-related conditions and improved patient outcomes

-

Continuous advancements in immunoassay technologies and automated laboratory systems enhancing test accuracy, throughput, and diagnostic efficiency

U.S. D-Dimer Testing Market Outlook:

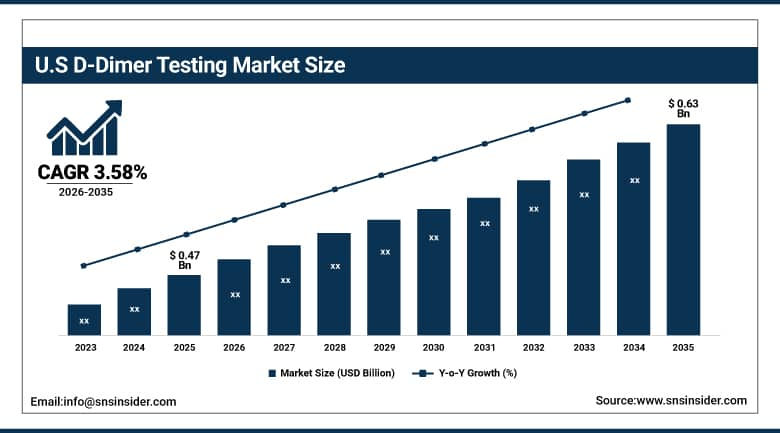

The U.S. D-Dimer Testing Market was valued at approximately USD 0.47 Billion in 2025 and is expected to reach approximately USD 0.63 Billion by 2035, growing at a CAGR of approximately 3.58%.

The U.S. is the most commercially significant D-dimer testing market within North America's leading regional position, supported by the high burden of thrombotic disease affecting approximately 900,000 patients annually with DVT and PE, strong reimbursement policies under Medicare and private insurance for coagulation testing, and the presence of leading diagnostic players including Abbott, Siemens Healthineers, Roche Diagnostics, Thermo Fisher Scientific, and Stago. The increasing use of point-of-care D-dimer testing in emergency departments is further driving market growth as rapid quantitative results enable immediate clinical decision-making without laboratory processing delays.

According to the Centers for Disease Control and Prevention, venous thromboembolism (VTE), including deep vein thrombosis and pulmonary embolism, affects as many as 900,000 Americans annually and contributes to up to 100,000 deaths each year.

D-Dimer Testing Market Segment Analysis:

-

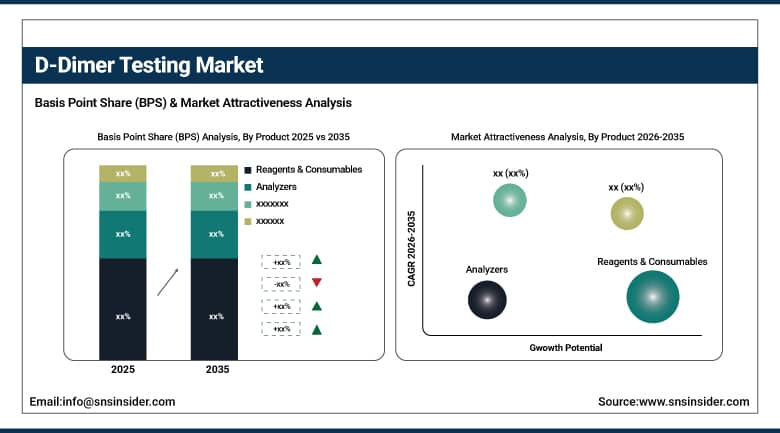

By Product, Reagents & Consumables segment dominated the D-dimer Testing Market in 2025 with 64% share; Analyzers segment is the fastest growing segment.

-

By Test Type, Clinical Laboratory Tests segment dominated the market in 2025 with 72% share; Point-of-Care Tests segment is the fastest growing segment.

-

By Method, Latex-enhanced Immunoturbidimetric Assays segment dominated the market in 2025 with 43% share; Fluorescence Immunoassays segment is the fastest growing segment.

-

By Application, Deep Vein Thrombosis (DVT) segment dominated the market in 2025 with 38% share; Pulmonary Embolism (PE) segment is the fastest growing segment.

-

By End-Use, Hospitals segment dominated the market in 2025 with 58% share; Diagnostic Centers segment is the fastest growing segment.

By Product, Reagents & Consumables Lead Market Growth Through Recurring Testing Demand While Analyzers Gain Momentum with Laboratory Automation

The Reagents & Consumables segment dominated the D-dimer Testing Market in 2025 as it was used repeatedly in every diagnostic test process, which made the demand from laboratories and healthcare facilities constant. The d-dimer test needs a steady supply of assay kits, calibration, controls, and reagents for obtaining proper results. With the increasing number of thrombotic disease tests, emergency diagnoses, and routine coagulation tests, reagent utilization had increased. Moreover, constant replenishment and rising number of tests in hospitals and diagnostic laboratories had reinforced the dominance of the segment.

The Analyzers segment is the fastest growing in the D-dimer Testing Market as there is an increased investment in the development of modern diagnostic infrastructure and laboratory automation. There is an adoption of high-throughput analyzers by healthcare providers to increase testing effectiveness and accuracy. With the increased need for fast diagnosis of thrombotic diseases and growing adoption of automated immunoassay platforms, there is an increased installation of analyzers. Also, technology improvements like increased sensitivity and other features have been driving upgrades to existing systems.

By Test Type, Clinical Laboratory Tests Maintain Dominance Through High Testing Volumes While Point-of-Care Testing Accelerates Rapid Diagnostics Adoption

The Clinical Laboratory Tests segment dominated the market in 2025 due to the fact that centralized laboratories are the prime location where D-Dimer tests are performed due to the greater testing ability and quality control. Centralized laboratories perform a large number of sample tests daily and have advanced analytical systems in order to provide highly accurate results. Doctors still favor the testing done through laboratories as it aids in confirming the diagnosis of suspected thrombotic diseases. Besides, existing network of laboratories, reimbursement support, and rising number of patient tests were among the main reasons behind the dominance of this segment in the market.

The Point-of-Care Tests segment is the fastest growing as there is an increasing requirement for fast diagnostic results in emergency departments, ambulatory care centers, and critical care locations. This segment allows for quick diagnostic decisions as the patient is not required to go to laboratories and wait. The growing use of portable diagnostic instruments, high level of accuracy, and increasing trend towards decentralized healthcare services are the major factors fueling the demand for this segment. In addition, growing number of urgent care centers also contribute to the increasing demand.

By Method, Latex-Enhanced Immunoturbidimetric Assays Lead Due to High Accuracy and Automation Compatibility While Fluorescence Immunoassays Expand Rapidly

The Latex-enhanced Immunoturbidimetric Assays segment dominated the market in 2025 due to their capability to provide fast, precise, and affordable results in the detection of D-dimer. The technology has been adopted by most healthcare facilities since it is easy to integrate into automated instruments and is suitable for high-throughput testing environments. Besides, the efficiency of the technique and high analytical performance make the Latex-enhanced Immunoturbidimetric Assays an ideal option for most healthcare facilities. In addition, the availability of commercial kit products and high demand for D-dimer testing in thrombotic disorder contributed to its leading market share.

The Fluorescence Immunoassays segment is experiencing the fastest growth due to its increased sensitivity and capacity to detect low levels of D-dimer concentration in blood samples. The adoption of the technique by healthcare facilities is growing at an unprecedented rate, mainly owing to its suitability in providing accurate results in the diagnosis of thrombotic diseases in healthcare facilities. Technological improvements in fluorescence immunoassays and increasing demands from healthcare facilities for better diagnostic tools have led to the accelerated growth of this segment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America D-Dimer Testing Market Insights

North America led the global D-dimer testing market in 2025, supported by advanced healthcare infrastructure, widespread awareness of thrombotic disease, rapid adoption of next-generation diagnostics, and strong reimbursement policies. The United States accounts for approximately 87.4% of North American revenues through Abbott, Siemens Healthineers, Roche Diagnostics, Thermo Fisher Scientific, and Stago's enterprise procurement relationships with hospital and reference laboratory networks.

Canada contributes approximately 12.6% of North American revenues through its publicly funded healthcare system's emergency and hospital-based D-dimer testing procurement, the aging population's elevated thrombosis risk creating growing testing volume, and the adoption of validated venous thromboembolism diagnostic pathways across major Canadian hospital networks.

The American Heart Association reports that cardiovascular diseases affect more than 127 million U.S. adults, increasing the need for thrombosis screening, risk assessment, and coagulation monitoring. Furthermore, rising healthcare investments are strengthening diagnostic capabilities across the country, with the Centers for Medicare & Medicaid Services reporting that U.S. healthcare spending exceeded USD 4.9 trillion in 2024.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe D-Dimer Testing Market Insights

Europe is a technically sophisticated D-dimer testing market where an aging population, government-backed initiatives for early coagulation disorder diagnosis, and established clinical guideline frameworks for venous thromboembolism management create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its dense hospital laboratory network, Siemens Healthineers’ and bioMerieux’s domestic commercial presence, and the high emergency department D-dimer testing volume within the German healthcare system.

The United Kingdom, France, and Italy are significant secondary markets where NHS venous thromboembolism prevention programmes, national clinical guidelines mandating D-dimer testing in structured diagnostic algorithms, and the aging patient populations create consistent procurement. Stago's French headquarters and Roche Diagnostics’ European operations sustain regional supply.

According to the European Society of Cardiology, venous thromboembolism (VTE) is responsible for approximately 544,000 deaths annually across Europe, exceeding the combined deaths from breast cancer, prostate cancer, AIDS, and traffic accidents.

Furthermore, data from Eurostat indicates that nearly 21% of the European Union population is aged 65 years or older, increasing the number of individuals at risk of thrombosis, cardiovascular diseases, and coagulation-related complications. In addition, the European Commission reports that healthcare expenditure exceeds 10% of GDP in many European countries, supporting broad access to advanced diagnostic technologies, including automated coagulation analyzers and D-dimer testing platforms.

Asia Pacific D-Dimer Testing Market Insights

Asia Pacific is the fastest growing regional D-dimer testing market, driven by China's expanding hospital diagnostic infrastructure, India's growing cardiovascular disease burden, Japan's aging population's elevated thrombosis risk, South Korea's advanced clinical laboratory adoption, and the ASEAN region's healthcare infrastructure investment. China accounts for approximately 44.8% of Asia Pacific revenues through its hospital laboratory modernisation programme, the growing adoption of automated immunoassay platforms in tier 2 and tier 3 city hospitals, and the government's chronic disease management investment creating coagulation testing demand.

According to the World Health Organization, cardiovascular diseases account for more than 10 million deaths annually across Asia, creating substantial demand for coagulation monitoring and thrombosis diagnostics. In China, the National Health Commission of the People's Republic of China estimates that more than 330 million people are living with cardiovascular diseases, making thrombosis screening and coagulation testing a major healthcare priority.

India represents the most commercially dynamic emerging market within Asia Pacific where the rapidly expanding private diagnostic laboratory sector, the growing cardiovascular disease prevalence, and the increasing adoption of standardised venous thromboembolism diagnostic pathways create above-average D-dimer testing market growth from both institutional and point-of-care procurement sources.

Additionally, the Ministry of Health and Family Welfare reports that cardiovascular diseases account for approximately 28% of all deaths in India, increasing the need for rapid diagnostic solutions such as D-dimer assays in emergency and critical care settings.

MEA & Latin America D-Dimer Testing Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital diagnostic infrastructure, Vision 2030's healthcare investment, and the high cardiovascular disease burden creating structured coagulation testing demand across both public and private healthcare sectors. The UAE's specialised hospital network adds complementary Gulf demand.

According to the World Health Organization (WHO), cardiovascular diseases account for approximately 40% of all deaths in several Middle Eastern countries, highlighting the need for timely diagnosis of conditions associated with thrombosis and coagulation disorders.

Brazil leads Latin American revenues at approximately 44.2% through its large hospital sector, the expanding private diagnostic laboratory network, and the growing cardiovascular disease awareness creating D-dimer testing adoption. Colombia and Argentina collectively sustain regional market growth through 2035.

Meanwhile, the Pan American Health Organization (PAHO) reports that cardiovascular diseases cause approximately 2 million deaths annually across the Americas, making them the leading cause of mortality in the region.

Market Dynamics:

Growth Drivers: Rising thrombotic disorder prevalence and point-of-care testing adoption transforming emergency diagnostic workflows

The increase in prevalence of venous thromboembolism around the world is the most commercially relevant factor driving market growth in the area of D-dimer tests. In particular, the number of cases estimated by CDC at 900,000 cases of DVT and PE annually in the United States along with WHO projections for cardiovascular diseases staying the leading reason for death worldwide generates stable demand for coagulation markers testing in healthcare institutions. Thrombosis susceptibility linked to increased chronic diseases prevalence, postoperative thromboembolism development, and hypercoagulable condition after COVID-19 increases the number of patients requiring D-dimer tests.

The transition to point-of-care testing is changing the workflow in the EDs by making results of D-dimer test available instantly rather than after laboratory processing. Every single emergency department that is using quantitative point-of-care D-dimer test is gaining ability to use its time-saving and noninvasive benefits. Availability of multiple quantitative point-of-care D-dimer tests from different companies makes price more competitive and facilitates the adoption process in various types of care settings.

Restraints: High false-positive rate in elderly patients and reimbursement variation across developing markets

The high false-positive rate of D-dimer tests in the elderly, hospitalized patients, and in patients suffering from inflammatory disorders leads to a loss of diagnostic confidence that reduces its rule-out power among patients with a greater likelihood of developing thrombosis. Every case where D-dimer elevation leads to unnecessary tests such as CT pulmonary angiography and venous duplex ultrasound adds up the cost and work burden of radiation exposure, which drives the quest for more specific and discriminative test methods.

Differences in reimbursement between developing countries hinder access to healthcare services, reducing the adoption of D-dimer tests in healthcare facilities with limited budgets where a direct outcome improvement must be shown to purchase laboratory test kits. Every country whose coagulation test kits cannot show enough value through imaging cost reduction remains restricted in terms of purchase motivation.

Opportunities: Age-adjusted diagnostic threshold adoption and AI-integrated clinical decision support

Adoption of an age-adjusted D-dimer diagnostic threshold is the most clinically valuable short-term enhancement in test use that generates above-average procurement growth through the ability to conduct appropriate high-volume testing in elderly patients without the tradeoff of lower specificity inherent in traditional cutoffs. Every hospital that adopts age-adjusted D-dimer testing protocols in its ED network builds out testing volume increment that will deliver clinical value in terms of avoided unnecessary imaging and sustain procurement growth.

Integration of AI into clinical decision support for ordering D-dimer tests and interpreting their results is the most commercially lucrative product development trajectory, which offers diagnostic value in addition to the test reagent through automatic pre-test probability calculation, interpretation of test results, and recommendation of avoided imaging. Every clinical decision support software system integrating validated D-dimer algorithms builds structured testing protocol compliance and sustains consistent test purchase volumes regardless of physician prescribing practices.

Recent Developments:

-

2024: Siemens Healthineers launched enhanced reagent kits for its INNOVANCE D-Dimer assay in 2024, improving sensitivity to above 98% for DVT and PE exclusion, enabling safe venous thromboembolism rule-out in low-risk patient populations without confirmatory imaging in most presentations.

-

2024: Abbott expanded its ARCHITECT D-Dimer assay availability on additional automated immunoassay analyser platforms in 2024, broadening access to high-throughput laboratory-based D-dimer testing across hospital networks using ARCHITECT or Alinity series analyser configurations.

-

2023: Roche Diagnostics launched the Elecsys D-Dimer II assay in 2023 with enhanced standardisation against the WHO International Standard, improving inter-laboratory result comparability for age-adjusted diagnostic cutoff application across integrated hospital laboratory networks using cobas analyser platforms.

-

2023: QuidelOrtho Corporation received expanded regulatory clearance for its Triage D-Dimer point-of-care assay in 2023, adding new validated clinical decision support algorithm integration that enables emergency physicians to apply structured diagnostic pathways directly at bedside within 15 minutes of specimen collection.

-

2023: Stago introduced enhanced reagent formulations for its STA-Liatest D-Di Plus assay in 2023, improving result stability and reagent on-board time on automated haemostasis analysers, reducing reagent waste and improving operational efficiency in high-volume hospital coagulation laboratories performing large daily D-dimer test volumes.

D-Dimer Testing Market Key Players:

-

Abbott Laboratories

-

Roche Diagnostics (F. Hoffmann-La Roche Ltd.)

-

Siemens Healthineers AG

-

Thermo Fisher Scientific Inc.

-

bioMérieux SA

-

Werfen S.A.

-

Sysmex Corporation

-

QuidelOrtho Corporation

-

Diazyme Laboratories, Inc.

-

Sekisui Diagnostics LLC

-

HORIBA Ltd.

-

BioMedica Diagnostics Inc.

-

Beckman Coulter, Inc.

-

Becton, Dickinson and Company (BD)

-

Bio-Rad Laboratories, Inc.

-

Diagnostica Stago SAS

-

Grifols S.A.

-

Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (Mindray)

-

LumiraDx Ltd.

-

Randox Laboratories Ltd.

D-Dimer Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.00 Billion |

| Market Size by 2035 | USD 3.13 Billion |

| CAGR | CAGR of 4.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Analyzers, Reagents & Consumables) • By Test Type (Clinical Laboratory Tests, Point-of-Care Tests) • By Method (Enzyme-linked Immunosorbent Assay (ELISA), Latex-enhanced Immunoturbidimetric Assays, Fluorescence Immunoassays, Others) • By Application (Deep Vein Thrombosis (DVT), Pulmonary Embolism (PE), Disseminated Intravascular Coagulation (DIC), Others) • By End-Use [Hospitals, Academic & Research Institutes, Diagnostic Centers, Others] |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, Roche Diagnostics (F. Hoffmann-La Roche Ltd.), Siemens Healthineers AG, Thermo Fisher Scientific Inc., bioMérieux SA, Werfen S.A., Sysmex Corporation, QuidelOrtho Corporation, Diazyme Laboratories, Inc., Sekisui Diagnostics LLC, HORIBA Ltd., BioMedica Diagnostics Inc., Beckman Coulter, Inc., Becton, Dickinson and Company (BD), Bio-Rad Laboratories, Inc., Diagnostica Stago SAS, Grifols S.A., Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (Mindray), LumiraDx Ltd., Randox Laboratories Ltd. |

Frequently Asked Questions

The D-Dimer Testing Market is expected to grow at a CAGR of 4.59% from 2026 to 2035.

The D-Dimer Testing Market was valued at USD 2.00 Billion in 2025.

Rising venous thromboembolism prevalence and increasing adoption of point-of-care D-dimer testing are driving demand for rapid diagnosis and treatment.

Deep Vein Thrombosis dominated the D-Dimer Testing Market

North America dominated the D-Dimer Testing Market in 2025.

Get in Touch