Point-of-Care Diagnostics Market Report Scope & Overview:

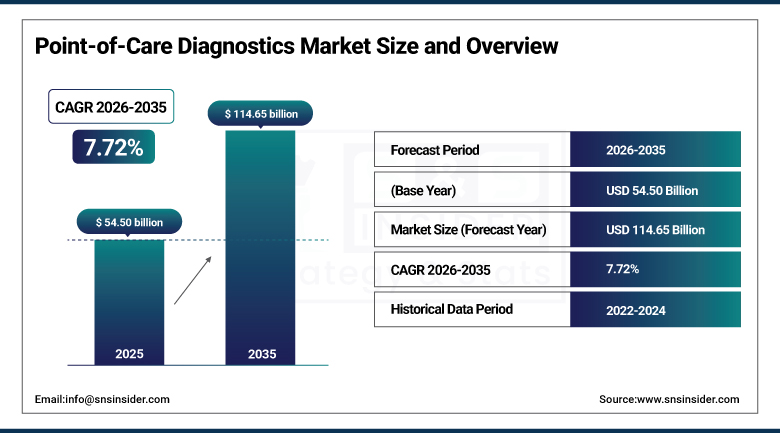

The Point-of-Care Diagnostics Market size was valued at USD 54.50 Billion in 2025 and is projected to reach USD 114.65 Billion by 2035, growing at a CAGR of 7.72% during 2026–2035.

Point-of-Care Diagnostics Market Overview The global Point-of-Care Diagnostics Market has witnessed significant growth due to the increasing demand for rapid and accurate diagnostic solutions to optimize clinical decision-making and patient outcomes in various healthcare settings. POC diagnostics allows testing to be performed at or near the site of the patient care, with a quicker turnaround time than traditional laboratory testing, leading to more prompt therapeutic decision making. Technological advances in biosensors; microfluidics; compact diagnostic devices; and AI-assisted result interpretation analytics are driving improvements in device accuracy, portability, connectivity, and clinical utility for all POC diagnostic applications through the forecast period 2026–2035.

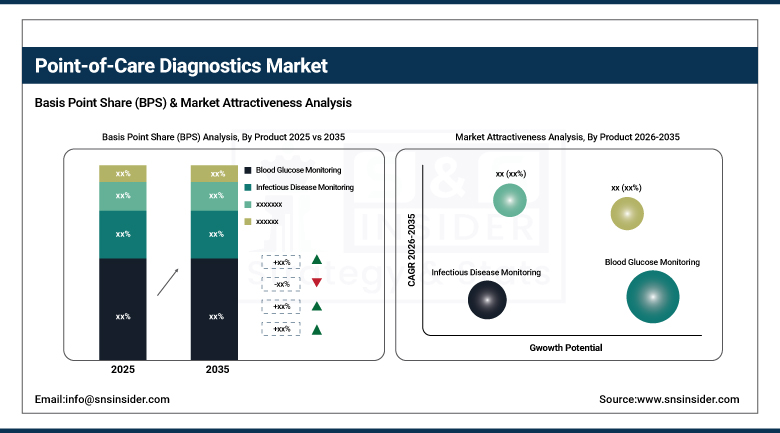

Global point-of-care diagnostics market is led by blood glucose monitoring product segment with about 54% market share of the global revenue, due to the global diabetes pandemic that threatens the lives of over 537 million adults worldwide, thus needing frequent, convenient and accurate measurement of blood glucose levels along with proper disease management & prevention of serious potential diabetic complications in all care settings that ranges from hospitals to home monitoring.

Point-of-Care Diagnostics Market Size and Forecast:

-

Market Size in 2025: USD 54.50 Billion

-

Market Size by 2035: USD 114.65 Billion

-

CAGR: 7.72% (from 2026 to 2035)

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Point-of-Care Diagnostics Market - Request Free Sample Report

U.S. Point-of-Care Diagnostics Market:

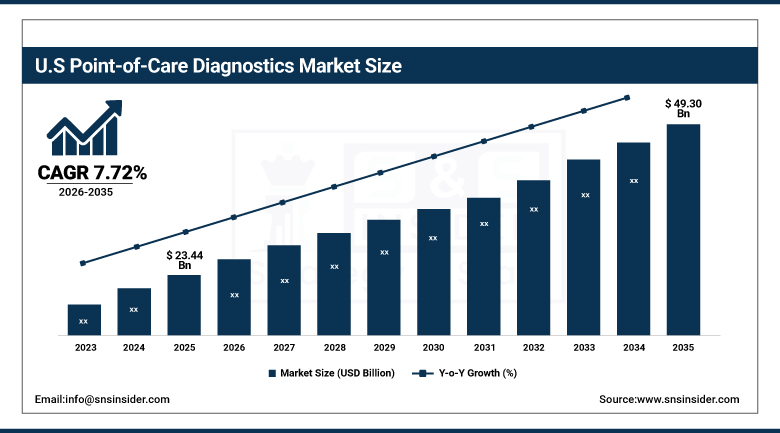

The U.S. Point-of-Care Diagnostics Market was valued at USD 23.44 Billion in 2025 and is expected to reach USD 49.30 Billion by 2035, growing at a CAGR of 7.72% from 2026–2035.

U.S. market for POC diagnostics is the largest in the world owing to high infrastructure for healthcare, high expenditure on healthcare, high presence of chronic disease particularly diabetes and cardiovascular diseases, and quick adoption of new diagnostic technologies. The U.S. market continues to grow steadily through the forecast period, accreting significant momentum from a regulatory environment that favors strong use of the FDA, laboratory-developed tests (compensating for in what are today, few FDA-cleared point-of-care (POC) tests and indeed given the less stringent requirements for certification versus clearance), and continuously increasing opportunities for home testing propelled by American awareness of wellness and health.

Point-of-Care Diagnostics Market Highlights:

-

Blood glucose monitoring dominating at 54% share driven by the global diabetes epidemic requiring frequent convenient testing

-

Blood-based sample type leading as the most clinically comprehensive and widely applicable diagnostic matrix

-

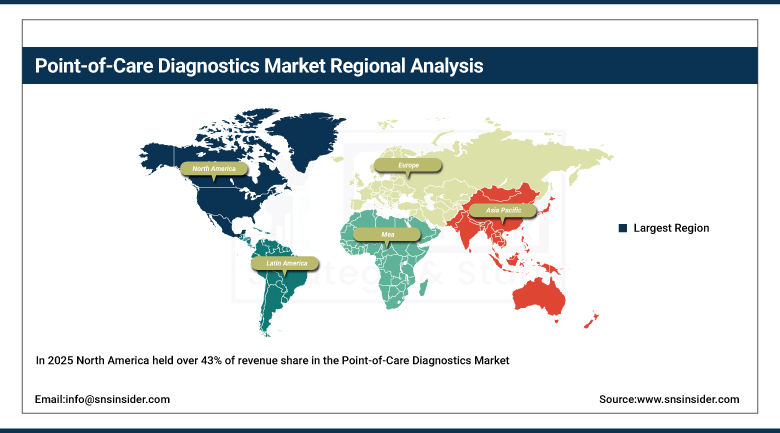

North America maintaining leadership at 43% share supported by advanced diagnostics infrastructure and high chronic disease rates

-

Asia-Pacific projected as the fastest-growing region at 8.97% CAGR driven by healthcare expansion and rising disease prevalence

-

AI integration into POC diagnostic devices enhancing accuracy, automating analysis, and reducing human error progressively

-

Home care testing expanding rapidly as consumer health awareness and chronic disease management needs grow globally

Point-of-Care Diagnostics Market Segment Highlights:

-

By Product: Blood Glucose Monitoring (Dominant – 54% share in 2025); Molecular Diagnostics (Fastest Growing through 2026–2035)

-

By Sample Type: Blood (Dominant); Urine (Fastest Growing driven by CKD prevalence increase)

-

By End User: Hospitals (Dominant); Home Care (Fastest Growing through 2026–2035)

Point-of-Care Diagnostics Market Segment Analysis:

Blood Glucose Monitoring (Dominant) and Molecular Diagnostics Fastest-Growing – By Product

In 2025, the blood glucose monitoring segment captured over 54% revenue share of the Point-of-Care Diagnostics Market between global diabetes prevalence—the IDF estimates >537 million adults now living with diabetes—translate into continuous, high-frequency demand for convenient, accurate blood glucose measurement across hospital, clinic, pharmacy, and home settings. The continuous glucose monitoring systems based on subcutaneous sensors and throughout the market is currently evolving through advances in connected CGM devices that transmit glucose readings directly to smartphones. Of the POC product categories, molecular diagnostics is the strongest growth region as isothermal amplification, lab-on-chip and microfluidic platforms are becoming feasible for nucleic acid-based testing in a near patient setting for infectious diseases, respiratory pathogens and STIs.

Blood Dominating and Urine Fastest-Growing – By Sample Type

The sample type segment of the Point-of-Care Diagnostics Market is primarily dominated by blood-based testing, as blood remains the most widely used clinical sample due to its high diagnostic accuracy, broad applicability across infectious diseases, metabolic disorders, cardiovascular conditions, and rapid compatibility with a wide range of POC diagnostic devices. Blood samples are extensively utilized in emergency care, chronic disease monitoring, and critical care settings where precise and immediate biomarker detection is essential for clinical decision-making.Conversely, the urine segment is expected to witness the fastest growth over the forecast period, driven by the rising prevalence of chronic kidney disease (CKD), urinary tract infections (UTIs), and metabolic disorders such as diabetes. Urine-based POC diagnostics are gaining traction due to their non-invasive nature, ease of collection, cost-effectiveness, and growing adoption in home care and screening applications, further supported by advancements in rapid urine testing technologies and increasing preventive healthcare awareness.

Hospitals Dominating and Home Care Fastest-Growing – By End User

The end-user landscape of the Point-of-Care Diagnostics Market by 2025 is conspicuously led by the hospitals, as these clinical facilities present an integrated medical infrastructure, large patient volume and trained clinical personnel who are capable of performing and interpreting a full spectrum of POC diagnostic tests along with the indispensable requirement of accommodating patient bedside results in emergency departments, ICUs, and operating rooms where treatment decisions cannot suffer from lengthy turnaround times of the central laboratory. The home care segment is anticipated to grow the most rapidly, linked in part to the faster commercialization of consumer-accessible POC testing for diabetes management, pregnancy, COVID-19, influenza, and an ever-expanding range of chronic disease monitoring applicationspartially driven by increasing consumer health awareness, increases in direct-to-consumer marketing of POC devices, and the global trend toward greater patient empowerment in chronic disease management.

Point-of-Care Diagnostics Market Regional Analysis:

|

Region |

Major Country |

Share (%) |

|---|---|---|

|

North America |

United States |

43.0% |

|

Europe |

Germany |

22.0% |

|

Asia Pacific |

China |

20.0% |

|

Middle East & Africa |

Saudi Arabia |

8.0% |

|

Latin America |

Brazil |

7.0% |

North America Point-of-Care Diagnostics Market Insights:

In 2025 North America held over 43% of revenue share in the Point-of-Care Diagnostics Market, owing to advanced healthcare infrastructure, high per-capital healthcare spending & high prevalence rates of chronic disease such as diabetes & cardiovascular disorders, along with increasing adoption of innovative diagnostic technologies, across hospitals, laboratories, physician offices, urgent care centers & home settings. The U.S. FDA's favorable regulatory path for CLIA-waived POC tests has opened the possibility of extending POC testing into a larger number of settings, and strong private insurance and government healthcare program coverage for diagnostic testing further supports availability of the market. The strong presence of global POC diagnostics companies such as Abbott, Roche, Siemens Healthineers, and Becton Dickinson continues to maintain a steady pace of product innovation that consolidates North America's leadership in diagnostic technology.

The potential market is enormous, persistent and almost certainly growing with more than 32 million adults living with diabetes in the U.S. and the International Diabetes Federation estimating that number will grow to nearly 35 million by 2032—demanding convenience, regular monitoring of blood glucose, and distinguishing diabetes management as one of the largest and most sustainable demand drivers in the global POC diagnostics market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Point-of-Care Diagnostics Market Insights:

Asia-pacific is anticipated to have the fastest CAGR (Approximately 8.97% through 2026 – 2035)due to the rise in healthcare expenditure, development of hospital networks and health access, increase in population suffering from diabetes, cardiovascular diseases, and infectious diseases, and increase in adoption of rapid diagnostic solutions across clinical and community settings. The expansion in China's large-scale health care infrastructure, along with the government efforts to improve the quality of primary health care, is generating strong demand for low-cost, hand-held POC diagnostic devices positioned for use at community health centers and rural clinics. There are new streams of demand arising due as a result of the growth of the private hospital sector in India and from expanding insurance coverage. Domestic players are strengthening the market self-sufficiency for infectious and cardiac marker POC segments with a rich product pipeline.

Introduction China has been driving point-of-care (POC) diagnostic adoption via its National Health Commission as part of the 2016–2020 'Healthy China 2030' blue print [1], along with investment in primary healthcare center equipment including POC diagnostic devices aiming to increase rates of early disease detection and lower the burden on hospital-based centralized laboratory systems for routine testing.

Europe Point-of-Care Diagnostics Market Insights:

In 2025, Europe had the Point-of-Care Diagnostics Market share of around 22%, propelled by impressive national health care facilities, the establishment of extensive disease management approaches among chronic disease populations, and widespread adoption of POC diagnostic technologies in high-volume facilities such as hospital emergency departments as well as in GP offices and community pharmacy settings. The UK's National Health Service has been most innovative in utilizing POC testing to minimize diagnostic delays in emergency departments, while Germany and France have directed comprehensive programs for POC diabetes monitoring and cardiovascular risk assessment in the community setting. The EU launched a new in vitro diagnostic devices (IVDR) regulation in 2022, which is increasing performance expectations and robust clinical evaluation criteria that are influencing product innovation and market access for all European POC diagnostics.

Middle East & Africa and Latin America Point-of-Care Diagnostics Market Insights:

Increasing POC diagnostics market participation in 2025 for Middle East & Africa and Latin America was due to high burden of infectious disease, increasing investment over healthcare infrastructure, and rising awareness of chronic disease management in rapidly urbanising populations. Healthcare modernization programs in the Gulf states of the Middle East have included investments in advanced diagnostic technologies, and the large burden of infectious diseases (such as malaria; human immunodeficiency virus, or HIV; and tuberculosis) and seasonal respiratory diseases in Sub-Saharan Africa has created a large demand for low-cost, portable point-of-care (POC) diagnostic devices that can operate in resource-limited environments. Brazil and Mexico make up the foundation of this trend in Latin America, where varying prevalence of diabetes, cardiovascular disease and infectious disease continues to drive a constant level of infrastructure-supporting POC diagnostics use in various healthcare settings.

Point-of-Care Diagnostics Market Drivers:

-

Rising global burden of chronic and infectious diseases creates expanding and persistent demand for convenient POC diagnostic solutions

The growing pandemic of non-communicable diseases (NCD) or chronic conditions such as diabetes, cardiovascular disease, chronic kidney disease, and chronic respiratory disease, in conjunction with continuing pressure from the heavy load of infectious disease due to influenza, HIV, tuberculosis, hepatitis and the emergence of significant new pathogens, is the main structural global demand driver for POC diagnostics. Frequently and easily accessible rapid and timely diagnostic tests will be needed to manage these conditions as reliably as the centralised laboratory testing cannot address the spectrum of clinical, community and home care settings in an efficient manner on the patient side for monitoring. The COVID-19 pandemic illustrated the massive unmet need for timely, easy-to-access testing diagnostics outside of laboratories, really increasing public awareness of and acceptance of POC testing which supported even higher levels of adoption across infectious disease testing segments throughout the forecast.

Point-of-Care Diagnostics Market Restraints:

-

Regulatory complexity, reimbursement limitations, and accuracy concerns restrain POC diagnostic market growth in some segments

Regulatory complexity presents another significant limit to the Point-of-Care Diagnostics Market, most damage caused from the EU's IVDR, which imposes very stringent clinical evidence requirements on POC diagnostic devices versus previous EU frameworks, imploring horrendous development costs and lengthening market access timelines. While the readiness of newer molecular POC testing categories for clinical adoption as the opportunity, reimbursement challenges in some markets present a barrier to adoption by limiting clinical economic viability for some device categories. Thus, clinical reluctance regarding their adoption for use in applications for which test accuracy directly informs high-stakes therapeutic choices. The need for quality control and maintenance of these devices in non-laboratory settings also poses significant barriers to adoption in low-resource environments.

Point-of-Care Diagnostics Market Opportunities:

-

Continuous Glucose Monitoring Expansion, Molecular POC Growth, and Home Diagnostics Create Substantial Commercial Opportunities

Continuous glucose monitoring (CGM) is perhaps the most commercially significant growth opportunity in the POC diagnostics market today, quickly advancing from traditional fingerstick glucose meters toward wearable subcutaneous sensors providing real-time continuous readings, with adoption among insulin-dependent and non-insulin-dependent diabetes patients benefiting from continuous versus episodic blood glucose data. This is reflected in the step-wise development of affordable, rapid molecular POC tests for an increasing number of respiratory pathogens, STIs, AMR markers, and cancer biomarkers, which are generating new high-value categories of POC diagnostics that were previously only movable on centralized laboratory platforms. Aging populations, trends toward empowering consumers for their health and expanding telemedicine ecosystems are the key drivers of the home-based chronic disease monitoring market that is rapidly globalizing, creating a substantial and rapidly growing global direct-to-consumer POC diagnostics market segment.

Recent Developments:

-

In 2024, Abbott launched the ID NOW point-of-care testing expansion with new infectious disease assays, extending its rapid molecular POC platform to additional respiratory and infectious pathogen targets beyond COVID-19 and influenza for clinical settings globally.

-

In 2024, Roche introduced the cobas Liat System expansion with a new POC molecular test panel, increasing the respiratory pathogen testing menu available for near-patient testing in hospital and outpatient clinic settings.

-

In 2023, Siemens Healthineers launched the Atellica VTLi Immunoassay Analyzer, an AI-enhanced POC immunoassay system offering laboratory-quality cardiac troponin and other biomarker testing at the point of care in emergency department settings.

-

In 2022, Danaher Corporation's Cepheid division expanded its GeneXpert POC molecular testing platform globally, particularly targeting tuberculosis and antimicrobial resistance testing in resource-limited settings as part of the WHO's global TB elimination program.

Point-of-Care Diagnostics Market Key Players:

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd.

-

Siemens Healthineers

-

Danaher Corporation (Cepheid, Radiometer)

-

Becton Dickinson and Company

-

Thermo Fisher Scientific

-

Quidel Corporation (QuidelOrtho)

-

bioMérieux SA

-

Chembio Diagnostics

-

Alere Inc.

-

Binax

-

OraSure Technologies

-

Nova Biomedical

-

Mindray Medical International

-

i-STAT

-

Boehringer Ingelheim

-

Nihon Kohden Corporation

-

Sekisui Diagnostics

-

Polymer Technology Systems

-

LumiraDx

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 54.50 Billion |

| Market Size by 2035 | USD 114.65 Billion |

| CAGR | CAGR of 7.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Blood Glucose Monitoring, Infectious Disease Monitoring, Cardiometabolic Disease Testing, Hematology Testing, Others) •By Sample (Blood, Nasal and Oropharyngeal Swabs, Urine, Others) •By End-User (Hospital Bedside, Physician’s Office Lab, Urgent Care & Retail Clinics, Home & Self Testing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers, Danaher Corporation (Cepheid, Radiometer), Becton Dickinson and Company, Thermo Fisher Scientific, Quidel Corporation (QuidelOrtho), bioMérieux SA, Chembio Diagnostics, Alere Inc., Binax, OraSure Technologies, Nova Biomedical, Mindray Medical International, i-STAT, Boehringer Ingelheim, Nihon Kohden Corporation, Sekisui Diagnostics, Polymer Technology Systems, LumiraDx. |

Frequently Asked Questions

Growth is driven by rising global chronic and infectious disease burden, technological innovations in biosensors and microfluidics, AI integration enhancing diagnostic precision, expanding home care testing adoption, and increasing demand for rapid near-patient diagnostic results across all care settings.

North America dominated with approximately 43% revenue share in 2025, while Asia-Pacific is expected to register the fastest CAGR of 8.97% through 2035.

Blood Glucose Monitoring dominated with approximately 54% revenue share in 2025, while Molecular Diagnostics is the fastest-growing product segment through 2035.

The Market was valued at USD 54.50 Billion in 2025 and is projected to reach USD 114.65 Billion by 2035.

The Point-of-Care Diagnostics Market is expected to grow at a CAGR of 7.72% during 2026–2035.

Get in Touch